Archive for November, 2005

-

The Market Today

Eddy Elfenbein, November 30th, 2005 at 7:11 pmAfter rising 0.0016% yesterday, the S&P 500 fell 0.64% today while our Buy List gave back 0.43%. For the month of November, the Buy List was up 5.88% and the S&P 500 was up 3.52%.

For monthly tracking purposing, I’m going to rebalance the entire Buy List based on today’s closing pricing. I’m going to equally weight all 25 stocks. Then on January 1, we’ll start tracking the 2006 Buy List (which I’ll have for you in about two weeks).

Our worst performer today was the best performer for the month. Quality Systems (QSII) gained 21.3% during November despite giving back 8% today. The best stock today was Donaldson (DCI) which jumped nearly 6% to a new 52-week high.

Looking over today’s GDP, here are some thoughts about interest rates and the economy. Over the last 10 quarters, the U.S. economy has grown by 17.6% (including inflation). That’s about 6.7% on an annualized basis. That’s very good.

At the beginning of that period, a 10-year Treasury bond yielded about 4%—so you can see that borrowing has really paid off (for now). My concern is that the Treasury market will soon start demanding a larger piece of the action, and rates will rise. If you were loaning money and saw your borrower making such nice returns, wouldn’t you want some of it? I would.

Here’s your odd stat for the day, along with a small lesson. There are only eight stocks that have beaten the S&P 500 for the last seven straight calendar years. That’s a lot lower than what I would have guessed.

If we assume that every stock has a 50-50 chance of beating the market each year, then seven straight victories would be 1-in-128 (one over two to the seventh). Given that a few thousand stocks have traded continuously over that time, I would have guessed that a few dozen stocks had seven-year win streaks. Over 500 stocks have beaten the market the last five years. What happened? 1999. The S&P 500 was up a lot that year, but most stocks weren’t. The reason is that the index is weighted by market value. The bigger you are, the more say you have. And the big boys were soaring that year. For everyone else, 1999 wasn’t much fun. The median return was 0%.

The eight stocks that beat the S&P 500 from 1998 through 2004 are Canterbury Park (ECP), Chico’s FAS (CHS), Cohesant Technologies (COHT), Electronic Arts (ERTS), FactSet Research Systems (FDS), K-Swiss (KSWS), Oshkosh Truck (OSK) and Rare Hospitality (RARE).

Here’s how the eight are doing so far this year:

Chico’s FAS 93.76%

Oshkosh Truck 32.21%

K-Swiss 7.68%

Rare Hospitality International 0.53%

FactSet Research Systems -0.03%

Electronic Arts -8.63%

Canterbury Park Holding -25.93%

Cohesant Technologies -27.23%

The S&P 500 is up about 3.1% for the year, so it looks like Chico’s and Oshkosh will keep their streaks alive, while a few more are on the fence.

Beating the market one year isn’t so hard. Doing so consistently is very tough.

Today’s Link: John Mugarian. -

The Dual Market

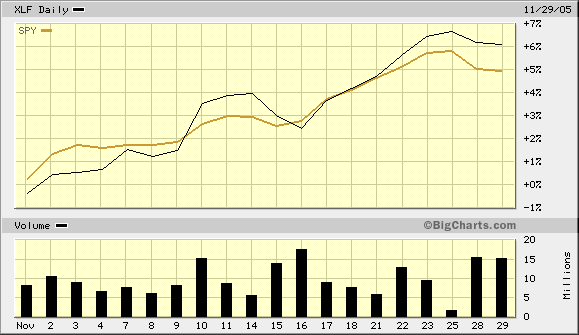

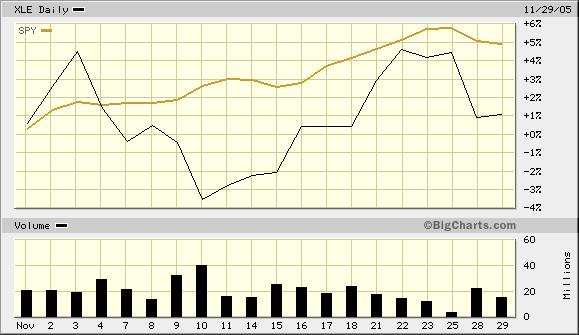

Eddy Elfenbein, November 30th, 2005 at 3:40 pmWe basically have two stock markets right now, energy stocks and everything else. All the other industries are highly correlated to each other. The big outlier is energy stocks. Also, the daily volatility of the other sectors is still very low. Energy is the only place that’s showing any action.

The most popular way of investing in energy stocks is through the S&P 500 Energy Spyders (XLE). This is almost akin to what the Nasdaq 100 ETF (QQQQ) was during the tech bubble.

Look at this chart of the Financial Spyders (XLF) compared with the S&P 500 ETF (SPY):

They move together like waltzing partners. I just used the finacials as an example, but several other sectors are moving just like that. Now look at the Energy Spyders:

Talk about following your own drummer! The overall market has almost no bearing on energy stocks (and vice versa). -

Credit Suisse First Boston: Dell Undervalued

Eddy Elfenbein, November 30th, 2005 at 2:22 pmFrom Forbes:

Credit Suisse First Boston maintained an “outperform” rating on Dell and advised investors to buy shares of the PC giant at current levels.

At a technology conference hosted by CSFB, Dell’s Chief Executive Jim Schneider said he expects continued demand for PCs, particularly for lower-priced computers, an area Dell has shied away from due to the slimmer profit margins.

“Although we believe the strength at the low-end of the PC market is not ideal for Dell, we believe its operating model is still advantaged and the company will still likely grow its top line 10% to 12% on a long-term basis,” said analyst Robert Semple.

“The derivative takeaway is suppliers into the PC industry should continue to benefit for the foreseeable future.”

Semple said hard-drive makers such as Western Digital and Maxtor should benefit the most from this trend.

The research analyst reiterated a $35 price target on Dell. “With its shares trading at 17 times calendar 2006 earnings per share, an 8% premium to the market, we believe Dell is undervalued relative to the growth and profit characteristics it is poised to deliver,” he said. “As a result, we would be buyers of Dell’s stock at current levels.”

CSFB rates Western Digital at “outperform” with a $17 price target while Maxtor has a “neutral” rating with a price target of $5.50. -

Private Equity Strikes Again

Eddy Elfenbein, November 30th, 2005 at 1:16 pmThe 80’s are back! Today’s buyout is of TDC, the Danish phone company. The private equity group includes Apax Partners, the Blackstone Group, Kohlberg Kravis Roberts, Permira Advisers and Providence Equity Partners. They’re looking to pay $12 billion for TDC.

This isn’t over. I expect to see many more. -

Today’s GDP Report

Eddy Elfenbein, November 30th, 2005 at 1:08 pmAs many of you know, I’ve been saying that the economy is much stronger than a lot of experts think. When the first report on third-quarter GDP came out last month, I wrote: “According to surveys, Wall Street’s estimate for third-quarter GDP growth is 3.6%. That’s way too low. I expect to see a number over 4%. In fact, I wouldn’t be surprised to see a number over 5%.”

It turned out to be 3.8%. I still thought that was too low. Today I found out that I was right. The government revised GDP growth higher to 4.3%. Today’s report suggests that economic growth is accelerating—the rate of growth is itself increasing. Also, inflation continues to be benign. This is excellent news for investors.

The market is down a bit today. Quality Systems (QSII) is taking a hit due to an analyst downgrade. Our Buy List is holding up well so far. All told, November has been a great month for the Buy List. I’ll have final numbers later today, but we should be up around 6%, and the S&P 500 is up about 4% (that doesn’t include dividends). Also, Donaldson (DCI) is rallying on its strong earnings announcement from yesterday. -

Big Value in Small-Caps

Eddy Elfenbein, November 29th, 2005 at 5:56 pmFor the last 10 years, small-cap stocks have been the leading sector.

Looking at 10-year returns of major fund categories, it’s clear that the leading category, small-cap value, got a big leg up during the bull market that began in 2003.

Among top performers in this group tracked by Standard & Poor’s Micropal the past 10 years has been RS Partners. It’s risen an average annual 17.44% in the 10 years ended Oct. 31 and an average annual 37.9% from March 31, 2003.

“All companies have benefited from expanding margins in the past few years,” noted David Kelley, a co-manager of RS Partners. “But small caps have seen more margin expansion. The main reason is they have smaller operations and more operational leverage than larger companies.”

Other leading small value funds were Keeley Small Cap Value, up an average annual 36.4% since the bull market began, and FPA Capital, up 28.3% a year.

It should come as no surprise that energy has played a big role in these funds’ performance. RS Partners had 16% of its assets in the sector as of Sept. 30, according to data collected by Morningstar. That was more than 1.5 times the S&P 500’s weighting in the sector and nearly twice that of the average small-cap value fund. Keeley Small Cap Value had 21% in energy and FPA Capital 32%.

Top-performing stocks among these funds’ biggest holdings as of their latest reporting periods included Toronto-listed Compton Petroleum in RS Partners. FPA Capital counted Ensco International among its top holdings. Keeley’s fund had McDermott International and Range Resources. -

Gold at $500

Eddy Elfenbein, November 29th, 2005 at 3:52 pmGold finally broke $500 an ounce.

“People are looking for an alternative investment to U.S. dollar-based instruments. The expectations of inflation in the coming year are very high,” said Albert Cheng, Far East managing director for the industry-backed World Gold Council.

But jewelry manufacturers and buyers may need time to adjust to the high prices, Cheng said. The council said this month that global demand for gold in the third quarter totaled 838 tonnes, a rise of 7 percent from the same quarter a year earlier, as surging investment demand helped offset a slowdown from the jewelry sector.

GOLD VULNERABLE

Some analysts said gold prices could fall to as low as $475 an ounce on liquidation by investment funds to book profits.

The latest weekly Commitments of Traders report issued by the Commodity Futures Trading Commission on Monday showed the speculative net long position in New York’s COMEX gold were closer to record high levels.

But the rally was also helped by reports that Russia, Argentina and South Africa had decided to increase the amount of gold in their reserves, reversing a six-year trend of central bank sales, mainly from Europe.

Platinum stood at $993/996 an ounce after spiking earlier to $1,002. It closed in New York at $989/993.

This year, not enough platinum is being mined and recycled to meet demand for catalytic converters and jewelry, so fundamentals have factored into the buoyant market.

Refining and chemical company Johnson Matthey, which provides fundamental analysis of platinum group metals, said in a recent report that 6.71 million ounces of platinum would be used in 2005, exceeding supply of 6.59 million ounces as demand rises from the auto sector and other industries.

It predicted that output from South Africa, the world’s top producer, would be lower than planned and the shortfall would continue to support prices. -

Consumer Confidence Rises

Eddy Elfenbein, November 29th, 2005 at 12:49 pmMore good news. Consumer confidence had its biggest gain since 2003.

Consumer confidence rose in November by the most in more than two years as falling gasoline prices encouraged shoppers before the start of the holiday season.

The Conference Board’s consumer confidence index rose to 98.9 from a revised 85.2 in October, the New York-based research group said today. The gauge was at 105.5 in August, before the full effects of the recent hurricanes were measured, and averaged 97.5 over the past five years.

Falling fuel prices after post-hurricane highs are increasing confidence and spending, economists said. Consumers splurged over the Thanksgiving weekend at discount retailers such as Wal-Mart Stores Inc., leading the National Retail Federation to predict this will be the second-biggest holiday selling season since 1999. Job creation is also helping sentiment.

“Confidence was healthy,” said Alan Ruskin, director of U.S. research at 4Cast.com in New York. “A lot of it is normalization post-hurricanes, and the energy prices coming off their highs is part of that.”

The Conference Board compiles its index of consumer confidence by surveying 5,000 households on general economic conditions, their employment prospects and spending plans. A Bloomberg News survey of 58 economists expected the index to rise to 90.2, with estimates ranging from 86 to 95.3. October confidence was originally reported to be 85. The November increase was the most since April 2003.

Expectations

The component of the index that tracks consumers’ expectations for the next six months increased to 88.8 from 70.1 in October, the biggest gain since April 2003. The gauge of optimism about the present situation rose to 114 from 107.8, the biggest jump since December 2004.

The share of consumers that said jobs were hard to get fell to 23.2 from 25.3 percent last month. The share who said jobs were plentiful in November rose to 20.8 percent from 20.7 percent.

The percentage of consumers expecting to buy a home increased to 3.1 percent from 2.8 percent. The percentage that plan to purchase major appliances rose to 29.1 percent from 25 percent. The share of those who expect to buy a car fell to 4.9 percent from 6.4 percent.

The results compare with those from the University of Michigan’s survey of consumer sentiment, which rose to 81.6 in November from a 13-year low of 74.2 the previous month, according to a report released Nov. 23.

U.S. new home sales unexpectedly rose to a record last month, suggesting people bought houses in anticipation of even higher mortgage rates, a government report showed today. Purchases increased 13 percent, the biggest rise since April 1993, to a 1.424 million annual rate from a September’s 1.26 million pace, the Commerce Department said in Washington. -

The Morning Market

Eddy Elfenbein, November 29th, 2005 at 10:32 amDon’t worry. Brown & Brown’s (BRO) stock hasn’t been cut in half. The stock split 2-for-1 this morning. So if you own, you now have twice as many shares. Brown & Brown even got a shout-out from Cramer last night. The bad news is that Frontier (FRNT) didn’t split, it’s just down today. The company announced a debt offering and the stock is currently down about 10%.

The market is regaining some lost ground from yesterday. Energy and small-caps are leading the charge. Dell (DELL) is also looking good. -

Southwest Goes to Denver

Eddy Elfenbein, November 29th, 2005 at 5:07 amThe Wall Street Journal has a front page story this morning about Southwest Airlines (LUV) entering the Denver market. Whenever Southwest enters a new market, its competitors cut and run.

Not this time.Frontier Chief Executive Jeffery Potter caught wind of Southwest’s move the night before the announcement, he recalls. Mr. Potter knew that other airlines, including Alaska Airlines, had successfully competed against Southwest in some cities, and felt reassured that Frontier compared favorably to those airlines, he says.

Southwest has a near-mythic reputation in the industry as an airline that usually can’t be beat. Airlines far bigger than Frontier, including US Airways Group, had decided to cut back service to cities that Southwest entered.

Mr. Potter stayed late at his office composing a letter to rally his employees. “We are not about to cower or back away,” Mr. Potter wrote, assuring his employees that “not everything you have heard about Southwest is necessarily true.”

In an interview, Mr. Potter argued that fliers will prefer Frontier’s extras, such as more legroom in its seats and personal television screens that offer programs and onboard movies for a fee. He maintained that fliers are turned off by Southwest’s first-come-first-serve seating, which sometimes results in long lines of passengers waiting to board.

“Pricing is Southwest’s big advantage,” notes Frontier spokesman Joseph Hodas. “Take that away, and what do they have?” Frontier immediately matched Southwest’s introductory Denver fares, and Mr. Potter maintains the airline can make money at the lower prices.The article includes an interesting table. Including fuel costs, Southwest is a bit cheaper than Frontier. Excluding fuel costs, Frontier is cheaper.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His