Archive for August, 2007

-

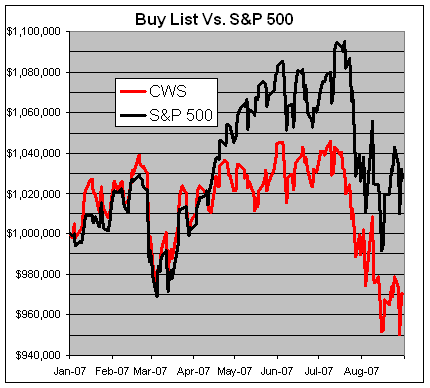

Buy List Update

Eddy Elfenbein, August 30th, 2007 at 5:06 pmNow that 2007 is nearly two-thirds over, let’s have a look at how our Buy List is doing.

So far, the 20 stocks on the Buy List are down 2.95% (not including dividends) while the S&P 500 is up 2.78%. The Buy List has been 8.7% less than volatile than the S&P 500.

Here’s how the Buy List has performed:

-

Dell’s Earnings

Eddy Elfenbein, August 30th, 2007 at 4:36 pmDell (DELL) just reported surprisingly good earnings of 32 cents a share.

Dell, like competitors Hewlett-Packard and Apple, profited from lower costs for computer components amid a supply glut. But profit was reduced by payments to its former CEO and 400 employees for stock options that could not be exercised during the company’s internal audit, which found that executives adjusted accounts to meet financial targets.

The big problem is that these aren’t official results. Dell hasn’t filed with the SEC for over a year. Here are the numbers, but bear in mind that they’ll be changed.

Quarter…..Sales….Oper. Income…..EPS

1-97………$2,588………$198………..$0.0675

2-97………$2,814………$296………..$0.0725

3-97………$3,188………$346………..$0.085

4-97………$3,737………$397………..$0.10

1-98………$3,920………$429………..$0.11

2-98………$4,331………$483………..$0.12

3-98………$4,818………$539………..$0.14

4-98………$5,173………$595………..$0.15

1-99………$5,537………$600………..$0.16

2-99………$6,142………$694………..$0.19

3-99………$6,784………$650………..$0.18

4-99………$6,801………$513………..$0.16

1-00………$7,280………$625………..$0.19

2-00………$7,670………$736………..$0.22

3-00………$8,264………$818………..$0.25

4-00………$8,674………$589………..$0.18

1-01………$8,028………$588………..$0.17

2-01………$7,611………$545………..$0.16

3-01………$7,468………$544………..$0.16

4-01………$8,061………$594………..$0.17

1-02………$8,066………$590………..$0.17

2-02………$8,459………$677………..$0.19

3-02………$9,144………$758………..$0.21

4-02………$9,735………$809………..$0.23

1-03………$9,532………$811………..$0.23

2-03………$9,778………$840………..$0.24

3-03………$10,622…….$912………..$0.26

4-03………$11,512…….$981………..$0.29

1-04………$11,540…….$966………..$0.28

2-04………$11,706…….$1,006……..$0.31

3-04………$12,502…….$1,089……..$0.33

4-04………$13,457…….$1,187……..$0.37

1-05………$13,386…….$1,174……..$0.37

2-05………$13,428…….$1,173……..$0.38

3-05………$13,911…….$944………..$0.39

4-05………$15,183…….$1,246……..$0.43

1-06………$14,216…….$949………..$0.33

2-06………$14,094…….$605………..$0.22

3-06………$14,383…….$824………..$0.30

4-06………$14,402…….$801………..$0.30

1-07………$14,622…….$947………..$0.34

2-07………$14,771…….$896………..$0.32 -

The Bin Laden Trade

Eddy Elfenbein, August 30th, 2007 at 9:32 amSteven Smith and Aaron Task at TheStreet report on unusual options trades:

The first area of focus is that open interest on September 700 S&P puts is 116,000 contracts, an unusually high number for such a low-probability trade. A put is a defensive bet that gives the holder the right to sell a security at a specified price, in this case more than 50% below the S&P 500’s current level of 1463 as of Wednesday’s close.

For comparison’s sake, according to the Option Clearing Corp., the open interest in the July 700 strike some three weeks prior to expiration on July 20 was 790 calls and 7,300 puts, and the August 700 strike showed 1,250 calls and 14,800 puts prior to Aug. 17 expiration.

And the volume completely outstrips anything seen last September, when the S&P was around 1300, some 20% below current levels. In September 2006, the 700 strike had 600 calls and 7,500 puts, and no strike below 1000 had open interest surpassing 42,000 contracts, and that was the 900 puts.

The bulk of the September SPX trades in question have been put on since June 1. Similar bets have also been placed on the DJ Eurostoxx 50 index, which won’t pay off unless the index tumbles nearly 25% to 2800, or below, by expiration on the third Friday of September. -

GDP Revised Higher

Eddy Elfenbein, August 30th, 2007 at 9:18 amSecond-quarter GDP growth was revised higher this morning from 3.38% to 3.96%. The WSJ runs through some of the numbers.

Trade gave the economy a bigger push than first estimated — because U.S. exports were revised up, rising by a rate of 7.6% instead of the originally reported 6.4%. Imports fell 3.2%; originally, the decrease was seen at 2.6%.

The revised data showed trade added 1.42 percentage points to GDP in the second quarter. Originally, trade was seen contributing just 1.18 percentage points to GDP.

Businesses elevated spending more than previously thought. Outlays rose by 11.1% in April through June; originally, spending was estimated rising 8.1%. Business spending climbed 2.1% in the first quarter. Second-quarter investment in structures by business surged by 27.7%. Equipment and software increased 4.3%.

Consumer spending advanced by 1.4%, up from a previously reported 1.3% increase but below the first quarter’s 3.7% climb. Consumer spending accounts for about 70% of economic activity. It contributed 1.03 percentage points to GDP in the second quarter; the original estimate was a contribution of 0.89 percentage point.

Durable-goods purchases increased 1.7% in April through June, above the previously reported 1.6% increase but below an 8.8% climb in the first quarter. Durable goods are expensive items designed to last at least three years, such as refrigerators.

Second-quarter nondurables spending fell by 0.3%. Services spending went 2.3% higher.

Residential fixed investment, which includes spending on housing, tumbled by 11.6% in the second quarter, a drop bigger than the previously reported 9.3% plunge. Housing fell 16.3% in the first quarter. -

Hump Day Redux

Eddy Elfenbein, August 30th, 2007 at 9:16 amYesterday was the 14th time in the last 19 Wednesdays that the S&P has rallied.

The numbers here are truly remarkable. The market is up for 35 of the last 50 Wednesdays. That’s better a better winning percentage than both the Red Sox and Yankees.

Going back to September 28, 2005–that’s an even 100 Wednesdays, the S&P rose 68 times including a run of 13 straight in early 2006. Combined, the other four days of the week are slightly negative. -

It felt like `Apocalypse Now,

Eddy Elfenbein, August 30th, 2007 at 8:46 amThe latest problem with the Hamptons–a surge in helicopter traffic:

“It felt like ‘Apocalypse Now,'” East Hampton resident Kathi Goldman said at a recent public hearing, describing choppers over her house in the northwest woods. Goldman, a retired science teacher at Grace H. Dodge High School in the Bronx, said choppers were so noisy on July 3 that she fled to her apartment on Manhattan’s Upper West Side.

-

How Much Would You Pay?

Eddy Elfenbein, August 29th, 2007 at 11:03 amLet’s say some kids in your neighborhood have a lemonade stand. You’re impressed by their entrepreneurial spirit so you order a glass and ask them how business is going.

“Great! We sold $20 worth of lemonade.”

“Wow! That’s really good. How much profit did you make?”

“Well, our costs were $17 so we made a $3 profit.”

You come back in a year (let’s suspend reality for a bit) and you want to see how the biz is going.

“We had a great year! We sold $55 worth of lemonade and our cost was just $35, so we made $20.”

This impresses you a lot. After a lengthy discussion of just-in-time inventory, first-mover advantage and Nassim Taleb’s latest, you decide to make the kids an offer for the lemonade stand.

How much would you pay? Say, $400?

Remember, it’s growing fast. How about $700? Maybe $1,000??

Well, it turns out, the kids have hired Goldman and they inform you that the price of the stand is $3,500 and not one penny less.

That’s about the current valuation for Baidu.com. -

‘Subprime Chuck’ Schumer Plays the Fool

Eddy Elfenbein, August 29th, 2007 at 9:36 amThe subprime mess has ushered in a new level of clueless political grandstanding. Naturally, Chuck Schumer is around to take first prize.

The chairman of Congress’s Joint Economic Committee then called on the firms to “assist this country’s mortgage crisis” and “urge your clients to do their part to keep our housing markets afloat, by modifying subprime loans that are at risk of default.”

In so doing, Subprime Chuck made a blithering fool of himself, though he probably doesn’t realize why. So far, none of the four firms — PricewaterhouseCoopers, Deloitte & Touche, Ernst & Young, and KPMG — has responded publicly to his plea for lobbying help.

You see, management’s job is to manage, and the auditor’s job is to audit. There’s also the decades-old requirement under U.S. securities laws that accounting firms must be independent of the companies they audit, both in appearance and in fact.

Under the Securities and Exchange Commission’s rules, that means the auditors, among other things, “must act in an unbiased and objective manner.” Lobbying audit clients to change their business practices is the mark of a biased auditor, not a disinterested one. -

Major Investment Banks

Eddy Elfenbein, August 29th, 2007 at 9:31 amHere’s a look at how the major investment banks have fared:

-

Great Moments In Aviation History

Eddy Elfenbein, August 29th, 2007 at 9:16 amTwo passengers on Spirit Airlines wrote the company to complain about their delayed flight which caused them to miss a concert.

Baldanza (Spirit’s CEO) supposedly told one of his staff in an email to handle the complaint and said, “we owe him nothing as far as I’m concerned. Let him tell the world how bad we are. He’s never flown us before anyway and will be back when we save him a penny.”

He then hit “reply to all” which included the couple’s email address as well.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His