Archive for September, 2008

-

Should Lehman Have Been Allowed to Fail?

Eddy Elfenbein, September 29th, 2008 at 12:02 pmI certainly though so, but now the evidence may point the other way:

Lehman’s bankruptcy filing in the early hours of Monday, Sept. 15, sparked a chain reaction that sent credit markets into disarray. It accelerated the downward spiral of giant U.S. insurer American International Group Inc. and precipitated losses for everyone from Norwegian pensioners to investors in the Reserve Primary Fund, a U.S. money-market mutual fund that was supposed to be as safe as cash. Within days, the chaos enveloped even Wall Street pillars Goldman Sachs Group Inc. and Morgan Stanley. Alarmed U.S. officials rushed to unveil a more systemic solution to the crisis, leading to Sunday’s agreement with congressional leaders on a $700 billion financial-markets bailout plan.

The genesis and aftermath of Lehman’s downfall illustrate the difficult position policy makers are in as they grapple with a deepening financial crisis. They don’t want to be seen as too willing to step in and save financial institutions that got into trouble by taking big risks. But in an age where markets, banks and investors are linked through a web of complex and opaque financial relationships, the pain of letting a large institution go has proved almost overwhelming.

In hindsight, some critics say the systemic crisis that has emerged since the Lehman collapse could have been avoided if the government had stepped in. Before Lehman, federal officials had dealt with a series of financial brushfires in a way designed to keep troubled institutions such as Fannie Mae, Freddie Mac and Bear Stearns Cos. in business. Judging them as too big to fail, officials committed billions of taxpayer dollars to prop them up. Not so Lehman.One of the major problems with this mess is that we don’t know what we don’t know. If we had saved Lehman, would it have made things much better?

-

A Vote is Due Today

Eddy Elfenbein, September 29th, 2008 at 10:22 amIt looks like the House will vote today on the bailout plan. You can read the bill here. The market, however, is not in a good mood today. Ultimately, I’m sure the House will pass the plan. If credit markets recover, however is another matter.

-

WaMu Is Undo

Eddy Elfenbein, September 25th, 2008 at 10:46 pmRemember these used to be that company Washington Mutual (WM)?

Washington Mutual Bank, the country’s largest savings and loan, was seized late today by federal regulators and immediately sold to JPMorgan Chase & Co., the New York banking giant that has long coveted the thrift’s California and Florida branches.

With assets of $307 billion and deposits of $188 billion, Washington Mutual is the largest bank to fail in U.S. history.

Washington Mutual depositors won’t lose access to any of their money, even if it wasn’t fully insured, the Federal Deposit Insurance Corp. said.

“For all depositors and other customers of Washington Mutual Bank, this is simply a combination of two banks,” FDIC Chairman Sheila C. Bair said. “For bank customers, it will be a seamless transition. There will be no interruption in services and bank customers should expect business as usual come Friday morning.”

Washington Mutual, one of the country’s largest mortgage lenders, was a victim of the housing downturn, recording $6.1 billion in losses in the nine months that ended June 30.WaMu is a victim?

-

Bill O’Reilly on the Bailout Plan

Eddy Elfenbein, September 25th, 2008 at 10:42 pmBill O’Reilly gets angry and incoherent, but mostly angry.

-

German Finance Minister Blames “Anglo-Saxon” Banking Model

Eddy Elfenbein, September 25th, 2008 at 1:58 pmFrom Bloomberg:

Steinbrueck, in a speech on the financial-market crisis to lawmakers in Berlin today, set out an eight-point plan urging greater regulation and larger capital reserves for banks. He championed the German banking system over its U.S. counterpart, dismissing the “Anglo-Saxon” model as having “an exaggerated fixation on returns.”

Paul Kedrosky neatly fillets this comment with a good amount of contempt (“Right, as opposed to the Teutonic banking system’s fixation on what, nice drapes?”).

As for me, if the Germans are prepared to call our banks, “Anglo-Saxon” banks, then I consider it an improvement. -

Oh Dear Lord

Eddy Elfenbein, September 25th, 2008 at 12:17 pmAn actual news story written by actual adults:

Michael Douglas asked about Wall Street crisis

Michael Douglas had to field questions Wednesday about the financial turmoil shaking world markets from reporters recalling his role in the 1987 film “Wall Street.”

The actor sought to focus on the subject of Wednesday’s news conference — urging the United States and eight other holdout nations to ratify a nuclear test ban treaty.

Douglas won an Academy Award for portraying the rapacious banker Gordon Gekko, who popularized the phrase “greed is good” in the movie.

After world leaders here condemned the “boundless greed” of world markets, Douglas was asked to compare nuclear Armageddon with the “financial Armageddon on Wall Street.”

But the likening to Gekko did not end there, with a reporter asking: “Are you saying Gordon that greed is not good?”

“I’m not saying that,” Douglas replied. “And my name is not Gordon. He’s a character I played 20 years ago.”I’ve always wanted to ask Mark Hamill how those levitating cars worked.

(Via: DealBreaker) -

Bush’s Speech

Eddy Elfenbein, September 25th, 2008 at 11:57 amHere’s part of the president’s speech from last night:

First, how did our economy reach this point? Well, most economists agree that the problems we’re witnessing today developed over a long period of time. For more than a decade, a massive amount of money flowed into the United States from investors abroad because our country is an attractive and secure place to do business.

This large influx of money to U.S. banks and financial institutions, along with low interest rates, made it easier for Americans to get credit. These developments allowed more families to borrow money for cars, and homes, and college tuition, some for the first time. They allowed more entrepreneurs to get loans to start new businesses and create jobs.

Unfortunately, there were also some serious negative consequences, particularly in the housing market. Easy credit, combined with the faulty assumption that home values would continue to rise, led to excesses and bad decisions.

Many mortgage lenders approved loans for borrowers without carefully examining their ability to pay. Many borrowers took out loans larger than they could afford, assuming that they could sell or refinance their homes at a higher price later on.

Optimism about housing values also led to a boom in home construction. Eventually, the number of new houses exceeded the number of people willing to buy them. And with supply exceeding demand, housing prices fell, and this created a problem.

BUSH: Borrowers with adjustable-rate mortgages, who had been planning to sell or refinance their homes at a higher price, were stuck with homes worth less than expected, along with mortgage payments they could not afford.

As a result, many mortgage-holders began to default. These widespread defaults had effects far beyond the housing market.

See, in today’s mortgage industry, home loans are often packaged together and converted into financial products called mortgage-backed securities. These securities were sold to investors around the world.

Many investors assumed these securities were trustworthy and asked few questions about their actual value. Two of the leading purchasers of mortgage-backed securities were Fannie Mae and Freddie Mac.

Because these companies were chartered by Congress, many believed they were guaranteed by the federal government. This allowed them to borrow enormous sums of money, fuel the market for questionable investments, and put our financial system at risk.

The decline in the housing market set off a domino effect across our economy. When home values declined, borrowers defaulted on their mortgages, and investors holding mortgage-backed securities began to incur serious losses.

Before long, these securities became so unreliable that they were not being bought or sold. Investment banks, such as Bear Stearns and Lehman Brothers, found themselves saddled with large amounts of assets they could not sell. They ran out of money needed to meet their immediate obligations, and they faced imminent collapse.

Other banks found themselves in severe financial trouble. These banks began holding on to their money, and lending dried up, and the gears of the American financial system began grinding to a halt. -

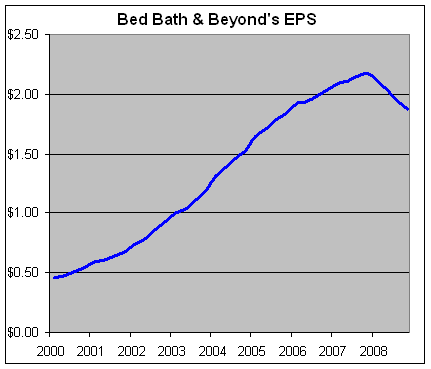

Bed, Bath & Beyond’s Earnings

Eddy Elfenbein, September 25th, 2008 at 9:48 amAmid all the credit market ruckus, Bed, Bath & Beyond (BBBY) reported earnings of 46 cents a share yesterday which was inline with the Street’s consensus. For the same quarter last year, the company earned 55 cents a share.

The market seems to be responding well to the earnings report. For this quarter, BBBY is expecting earnings-per-share between 41 and 47 cents, compared with last year’s 52 cents. The Street is expecting 45 cents.

Here are the earnings results going back a few years:Quarter Sales Gross Profit Operating Profit Net Profit EPS $356,633 $146,214 $28,015 $17,883 $0.06 $451,715 $185,570 $53,580 $33,247 $0.12 $480,145 $196,784 $50,607 $31,707 $0.11 $569,012 $238,233 $77,138 $48,392 $0.17 $459,163 $187,293 $36,339 $23,364 $0.08 $589,381 $241,284 $70,009 $43,578 $0.15 $602,004 $246,080 $64,592 $40,665 $0.14 $746,107 $311,802 $101,898 $64,315 $0.22 $575,833 $234,959 $45,602 $30,007 $0.10 $713,636 $291,342 $84,672 $53,954 $0.18 $759,438 $311,030 $83,749 $52,964 $0.18 $879,055 $370,235 $132,077 $82,674 $0.28 $776,798 $318,362 $72,701 $46,299 $0.15 $903,044 $370,335 $119,687 $75,459 $0.25 $936,030 $386,224 $119,228 $75,112 $0.25 $1,049,292 $443,626 $168,441 $105,309 $0.35 $893,868 $367,180 $90,450 $57,508 $0.19 $1,111,445 $459,145 $155,867 $97,208 $0.32 $1,174,740 $486,987 $161,459 $100,506 $0.33 $1,297,928 $563,352 $231,567 $144,248 $0.47 $1,100,917 $456,774 $128,707 $82,049 $0.27 $1,273,960 $530,829 $189,108 $120,008 $0.39 $1,305,155 $548,152 $190,978 $121,927 $0.40 $1,467,646 $650,546 $283,621 $180,980 $0.59 $1,244,421 $520,781 $150,884 $98,903 $0.33 $1,431,182 $601,784 $217,877 $141,402 $0.47 $1,448,680 $615,363 $205,493 $134,620 $0.45 $1,685,279 $747,820 $304,917 $197,922 $0.67 $1,395,963 $590,098 $148,750 $100,431 $0.35 $1,607,239 $678,249 $219,622 $145,535 $0.51 $1,619,240 $704,073 $211,134 $142,436 $0.50 $1,994,987 $862,982 $309,895 $205,842 $0.72 $1,553,293 $646,109 $154,391 $104,647 $0.38 $1,767,716 $732,158 $211,037 $147,008 $0.55 $1,794,747 $747,866 $203,152 $138,232 $0.52 $1,933,186 $799,098 $259,442 $172,921 $0.66 $1,648,491 $656,000 $118,819 $76,777 $0.30 $1,853,892 $739,321 $187,421 $119,268 $0.46

-

Jessica Hagy on the Paulson Plan

Eddy Elfenbein, September 24th, 2008 at 2:34 pm -

More Market History

Eddy Elfenbein, September 24th, 2008 at 1:13 pmToday is the 139th anniversary of Black Friday. This was when Jay Gould and Jim Fiske tried to corner the gold market. It didn’t work and the bottom fell out of the gold market on September 24, 1869. Fisk was ruined and eventually shot by an angry creditor.

Forty-three years ago, President Eisenhower had a heart attack and that sent the market down 6.5%. This was a time of very low volatility so that sell-off was one of the biggest in years.

(Via: Gary Alexander)

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His