Archive for January, 2009

-

It Was 40 Years Ago Today….

Eddy Elfenbein, January 30th, 2009 at 8:04 pm

-

Peter Schiff Responds

Eddy Elfenbein, January 30th, 2009 at 7:51 pmSince I posted Mish’s take down of Peter Schiff, I feel obliged to posts Schiff’s response. The Wall Street Journal also weighs in.

-

Two More Earnings

Eddy Elfenbein, January 30th, 2009 at 4:49 pmYesterday, Eli Lilly (LLY) reported fourth-quarter earnings, after charges, of $1.07 a share, two cents more than expectations. That’s 19% growth although revenue growth was flat. The company sees 2009 earnings coming between $4.00 and $4.25 a share. That means the stock is going for less than 10 times this year’s earnings, plus it currently yields over 5%.

SEI Investments (SEIC) reported Q4 earnings of 25 cents a share, three pennies below estimates. This will be a difficult year for SEIC, but I still think it’s a solid company. -

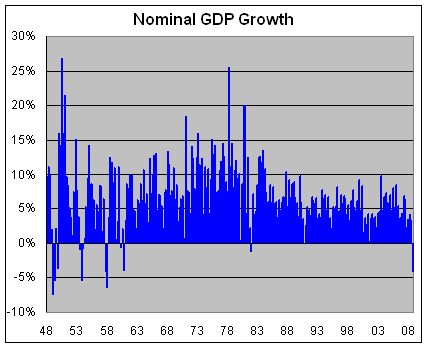

Today’s GDP Report

Eddy Elfenbein, January 30th, 2009 at 12:21 pmThe GDP report for the fourth quarter was pretty ugly, though not as ugly as it could have been. Let’s also wait for the subsequent revisions, and revisions of those revisions. The initial report showed real growth of -3.8%.

Since inflation has been so tame, I was curious to look at nominal growth which was -4.05%. That’s the first down quarter in 25 years and the worst quarter in 50 years.

-

Poll: Super Bowl XLIII

Eddy Elfenbein, January 29th, 2009 at 6:26 pm

Let’s see how good my readers are. -

Oh Charlie You Can’t Say That

Eddy Elfenbein, January 29th, 2009 at 3:38 pm35 second mark.

-

Davos Love Fest

Eddy Elfenbein, January 29th, 2009 at 3:30 pmMichael Dell asked Putin how we can help Russia expand its IT.

Putin: “We don’t need help. We are not invalids.”

Alrighty then…. -

The Case for Profits

Eddy Elfenbein, January 29th, 2009 at 3:23 pmArnold Kling argues that what really need right now is profits:

A stimulus will work if and when it serves to increase profits, because profits are at the core of a free market system. The economy will recover if and when profits recover.

Wages and salaries rose by 3%, while corporate profits fell by 9%, from the third quarter of 2007 through the third quarter of 2008, according to Commerce Department data. Fourth-quarter figures, which will be available in late February, are expected to show weakening in both types of income, with wages and salaries showing almost no increase, and profits falling by more than 15% relative to last year’s fourth quarter.

The economy is in trouble today because of, pardon the pun, false profits. The financial sector reported as much as 40% of all profits in recent years. However, the reported profits on instruments such as mortgage-backed securities and the sale of credit default swaps did not reflect the long-term risks of those instruments. That is, the return on capital in the financial sector was artificially high because the amount of capital used to protect against risk was artificially low. Losses at many financial firms are inevitable. It is the market’s way of telling the bloated industry to contract, releasing capital and talent for use elsewhere in the economy. -

Nicholas Financial’s Q3 Earnings

Eddy Elfenbein, January 29th, 2009 at 3:20 pmNICK just came out with its third-quarter earnings and I thought they were pretty good. Or rather, not nearly as horrible as they could have been. For the last three months of 2008, NICK earned $1,266,809 or 12 cents a share. That’s way down from the 22 cents they made a year ago, but it’s an increase from the 8 cents it made in the second quarter. Bottom line, you’re not going out of business when you’re making money.

There are a few items to highlight. First, the company changed its financing option which altered how they account for their use of interest rate swaps. This means that that swaps are now recorded on the income statement. For the third quarter, that’s about $1 million or 10 cents a share. As I see, this is merely an accounting issue and it doesn’t impact the company’s business.

Well, there is one important impact on NICK’s business and that is they were able to cut their financing expenses in the third quarter. Interest expense dropped to $1.27 million from $1.43 million in the second quarter. Under the company’s line for “Average Cost of Borrowed Funds,” the decrease is from 5.45% to 4.87%. That’s good to see. Personally, I hate dealing in GAAP/non-GAAP jazz, but I’ll do it if there’s a real benefit.According to Peter L. Vosotas, Chairman and CEO, “the business climate remains challenging, auto sales are still well below historical levels and the employment outlook continues to weaken. We expect to see some seasonal improvement in our business during the fourth quarter but remain very cautious about the coming year, as we believe the recessionary pressures embedded in the economy will not subside in the near-term. During the last two quarters we have been tightening our credit underwriting guidelines in response to market conditions. We continue to evaluate markets in which we operate in and we do not anticipate any significant change from our branch-based methodology. Due to a combination of tighter underwriting guidelines and a significant slow down in auto sales during the three months ended December 31, 2008, we have reduced the size of our loan portfolio by approximately $2.6 million and also decreased our credit line outstanding by approximately $4.6 million.”

The key line to watch is provision for credit losses. That dropped from $5.1 million last quarter to 4.6 million this quarter. That’s high but moving in the right direction. As a percentage of “average finance receivables, net of unearned interest” credit losses dropped from 9.66% last quarter to 8.77% in the third quarter.

This was a decent quarter and if NICK keeps it up, they could be in great shape by next year. -

The Stimulus Bill Clears the House

Eddy Elfenbein, January 28th, 2009 at 6:43 pmThe vote was 244 to 188. Eleven Democrats crossed the aisle. No Republicans crossed.

So much for the president’s urge for bi-partisan support.

The Democrats voted 244 to 11. The GOP voted 0 to 177. One GOP member didn’t vote.

The “nay” Democrats were:

Bright (AL)

Griffith (AL)

Taylor (MS)

Shuler (NC)

Cooper (TN)

Boyd (FL)

Ellsworth (IN)

Kanjorski (PA)

Kratovil (MD)

Minnick (ID)

Peterson (MN)

Now…it’s off to the Senate. (Here’s some help if you need a reminder of how the system works).

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His