Archive for May, 2009

-

Very Cool Interactive Map of GM Fallout

Eddy Elfenbein, May 31st, 2009 at 11:54 pmCheck it out.

(HT: ZH) -

GQ quotes Nassim Nicholas Taleb as saying that in the falling market he “made $20 billion for our clients, half a billion for the Black Swan fund.” Yeah…about that.

Eddy Elfenbein, May 31st, 2009 at 10:45 pmJanet Tavakoli does some great legwork:

A recent GQ article quoted Nassim Nicholas Taleb as saying that in the falling market he “made $20 billion for our clients, half a billion for the Black Swan fund.”

I checked with Nassim Taleb regarding the $20 billion in gains and asked if he were misquoted. He responded via email: “The quote is inaccurate. THe [sic] 20 billion might correspond to the face value of positions.” This response is both vague and different in character from the mythical $20 billion in gains inaccurately quoted in GQ’s article. The total gains could be a tiny fraction of what Taleb loosely describes as “face value.”

Why is GQ’s mistake important? In my opinion, public claims of enormous private hedge fund gains require credible back up, and one would think that GQ would have known that before it inaccurately quoted Taleb as having made a bell ringing gain of $20 billion for clients. Presumably, the error referred to outside clients, not the black swan fund itself, but it could have the side effect of attracting investors to the black swan fund, similar to advertising or salesmanship.

The black swan fund’s strategy is purportedly to buy out-of-the-money put options on stocks and broad market indices and hedge tail risk for clients. The strategy may produce long periods of mediocre—or even negative—returns followed by a large gain and vice versa. No one can tell you for certain exactly when (or for how long) large gains are possible. Initial success in a newly created fund may not be replicated in the future, and there is always the problem of scaling. Scaling refers to the fact that an individual fund may make a high return on an initial investment, say 100% on $100 million, but lose 10% on $1 billion.Read the whole thing.

-

Jack Welch’s Challenge

Eddy Elfenbein, May 31st, 2009 at 12:23 pmIt was Jack Welch’s night to reign supreme once more.

That’s the assessment of Vanity Fair magazine, which along with Bloomberg News staged a panel discussion in Manhattan on Thursday evening on how the economy got into its current mess and how to get out of it. Vanity Fair said Mr. Welch, the former longtime chief executive of General Electric, was the audience favorite as he gave what it called “an unapologetic defense of old-school capitalism in a room teeming with past and future Masters of the Universe.”

Mr. Welch went head to head with the other panelists and the moderator, DealBook’s Andrew Ross Sorkin. At one point, he challenged the Nobel Prize-winning economist Joseph Stiglitz on the role of unions, saying, “Give me a highly successful, unionized American industry.”Hollywood.

Want another? Pro Sports. -

Corporate Dividends Are Drying Up According to Bankrupt Newspaper

Eddy Elfenbein, May 31st, 2009 at 12:13 pmThe Minneapolis Star Tribune reports:

In February, General Electric Co. — the classic widows-and-orphans stock — cut its dividend for the first time since 1938, a move that will save the company about $9 billion a year.

The January to March period marked the first quarter since Standard & Poor’s started recording dividend data in 1955 that the number of dividend cuts was greater than the number of dividend increases. A record low 283 companies announced dividend increases in the first quarter of 2009.

“While the number of dividend decreases is at a record high, the number of increases has set a new record low,” said S&P senior index analyst Howard Silverblatt in April. “Since 1955, the average has been 15 increases for every decrease. Now its three increases for every four decreases.” -

Barron’s Punches Hole in Green Mountain Coffee (GMCR)

Eddy Elfenbein, May 30th, 2009 at 3:30 pmBill Alpert looks at one of the hottest stocks around, Green Mountain Coffee Roasters (GMCR), and isn’t impressed:

At almost 60-times the earnings forecast for the current fiscal year ending Sept. 2009, Green Mountain’s valuation warrants a closer examination of the business. That’s more than it seems to have gotten from sell-side bulls — none of whom said much about why March earnings beat analysts’ forecasts by 40% when sales beat forecasts by only 8%. Powering those earnings was an 85% jump in the royalties Green Mountain gets from other companies selling coffee in its K-Cup single-serve pods. As it turns out, a significant portion of those royalty generating sales were to Green Mountain itself, which sells both its own coffee pods, and those of other brands. By boosting its wholesale purchases from K-Cup licensees, Green Mountain can trigger royalty payments that directly boost its profits. Indeed, Green Mountain nearly tripled its March-quarter purchases from one licensee — the publicly-held Diedrich Coffee (DDRX) — thereby generating royalties that we estimate were almost 10% of the $21 million in pre-tax profits that Green Mountain reported in the quarter. As the bottom-right chart shows, Green Mountain has benefited from these transactions for many quarters; Diedrich is just one of a number of K-Cup licensees from whom it has made royalty-triggering purchases. In March, Green Mountain bought the wholesale business of a struggling licensee — the Tully’s unit of TC Global — whose sales to Green Mountain had been rising like Diedrich’s.

-

Western Civilization Peaks

Eddy Elfenbein, May 30th, 2009 at 3:04 pm -

First Sanjaya, Now This

Eddy Elfenbein, May 30th, 2009 at 2:31 pmHere are seven portfolios larger than yours. Oh, did I mention they’re cats and dogs.

I’m serious.1. Gunther IV, the German Shepherd: This dog actually received his inheritance from his father, Gunther III, a German Shepherd who received an inheritance from Karlotta Liebenstein, a German countess. Gunther IV has bought a Miami villa from Madonna and won a rare white truffle in an auction. Learn more about Gunther IV on a Web site devoted to him and those he hangs out with. He’s worth about $372 million right now, thanks to his growing trust fund.

2. Oprah’s dogs: Oprah Winfrey has several animals, including some dogs. She wants to make sure that her dogs are cared for when she is gone. Her will specifies that that her dogs receive $30 million for their care. (Just a drop in the bucket when you look at the billions Oprah is worth.) True, that money will be split amongst all dogs that she has, but even so, each and every one is probably richer than you are. They’re definitely richer than I am.Read the rest here.

-

Harvard MBAs Promise to Be Ethical

Eddy Elfenbein, May 30th, 2009 at 12:11 amThe New York Times reports that 20% of the graduating MBA class at Harvard has signed a pledge to be ethical. Oh boy. Have far have we fallen that you sign a pledge to be a decent human being?

Here’s the MBA Oath (the short version).As a manager, my purpose is to serve the greater good by bringing people and resources together to create value that no single individual can create alone. Therefore I will seek a course that enhances the value my enterprise can create for society over the long term. I recognize my decisions can have far-reaching consequences that affect the well-being of individuals inside and outside my enterprise, today and in the future. As I reconcile the interests of different constituencies, I will face choices that are not easy for me and others.

Therefore I promise:

* I will act with utmost integrity and pursue my work in an ethical manner.

* I will safeguard the interests of my shareholders, co-workers, customers and the society in which we operate.

* I will manage my enterprise in good faith, guarding against decisions and behavior that advance my own narrow ambitions but harm the enterprise and the societies it serves.

* I will understand and uphold, both in letter and in spirit, the laws and contracts governing my own conduct and that of my enterprise.

* I will take responsibility for my actions, and I will represent the performance and risks of my enterprise accurately and honestly.

* I will develop both myself and other managers under my supervision so that the profession continues to grow and contribute to the well-being of society.

* I will strive to create sustainable economic, social, and environmental prosperity worldwide.

* I will be accountable to my peers and they will be accountable to me for living by this oath.

This oath I make freely, and upon my honor.Two quick points:

When reading an ethical oath, should it be perfectly obvious how the authors voted?

Isn’t pride also a sin? -

Right-Wing Comment of the Day

Eddy Elfenbein, May 29th, 2009 at 7:24 pmGuess who spouted this?

It must be said, that like the breaking of a great dam, the American decent into Marxism is happening with breath taking speed, against the back drop of a passive, hapless sheeple, excuse me dear reader, I meant people.

Give up? Here’s you answer:

-

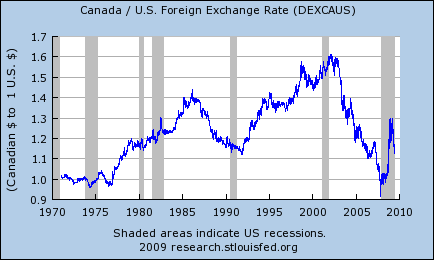

Canadian Euro Has Best Month in 60 Years

Eddy Elfenbein, May 29th, 2009 at 4:28 pmThe loonie is making us look like a bunch of hosers:

Canada’s currency headed for the biggest monthly gain since the Korean War as commodities surged, global stocks rallied and the U.S. dollar tumbled.

The Canadian dollar rose 9.2 percent since April 30, the most since at least October 1950, according to data from the Bank of Canada and Bloomberg.

“This does seem like a historic move,” said David Watt, a senior currency strategist in Toronto at RBC Capital Markets. “The biggest driver has been the decline in general fear, compounded by an increase in specific fear for the U.S. dollar, which might or might not be appropriate.”

The Canadian currency appreciated as much as 2.1 percent to C$1.0898 per U.S. dollar, the strongest level since Oct. 6, and traded at C$1.0908 at 2:15 p.m. in Toronto, from C$1.1133 yesterday. One Canadian dollar buys 91.68 U.S. cents.

The Onion notes: U.S. Dollar Slips Against Canadian Acorn

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His