CWS Market Review – April 5, 2013

“There is only one side of the market, and it is not the bull

side or the bear side, but the right side.” – Jesse Livermore

Let me give you the briefest summation of Wall Street over the last six months: Investors worry about something that’s unlikely to happen, the financial media amplifies said worry, calming voices are ignored, the markets trends downward, the financial media then calls for civility and public-spiritedness to address the needless worry they just promoted, incredibly the world doesn’t end, the worries fade away, volatility falls and the market quietly rallies.

We’ve repeated this dance so many times I’m beginning to lose count. There was the Fiscal Cliff, the debt ceiling (remember the $1-trillion coin), the elections in Italy, the fiasco in Cyprus and the Great Rotation out of bonds. The latest worry is war rumblings from North Korea. While the rhetoric is disturbing, the reality is that Pyongyang’s bark is far worse than its bite.

What’s interesting is that the market has so far ignored the threats from North Korea. I suspect that we’re going through Apocalypse Fatigue. Michael Gayed has suggested we’re in a Honey Badger market: Whatever latest worry comes our way, stock market don’t care. I suspect he’s on to something.

There are, however, stealth movements occurring within the market that we need to pay attention to. Since the middle of March, the market has become more defensive. A lot more defensive. The more-conservative sectors have led the more-aggressive sectors. In a few cases, the divergence has been rather stunning. The Healthcare ETF ($XLV), for example, has beaten the S&P 500 for the last 12 days in a row. Both Utilities ($XLU) and Consumer Staples ($XLP) have been recent leaders as well.

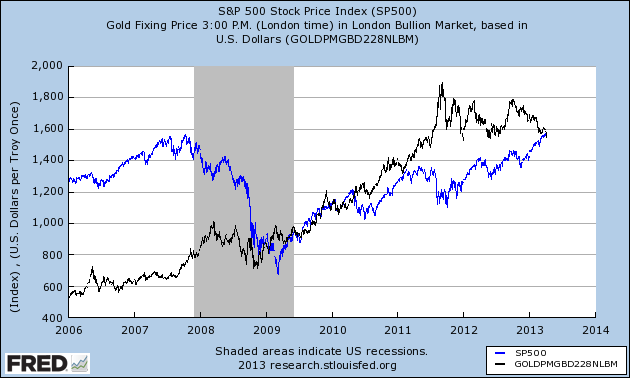

The move towards defensive stocks is telling us something. Coupled with the recent drop in gold, this suggests that investors are finally shying away from risk. The price of gold actually fell below the S&P 500 for the first time since May 4, 2010 (see chart above). I won’t go so far as to say this portends a bear market, but it may spell an end to the market’s appetite for risk.

What to do now: Investors should remain calm and make sure they own high-quality stocks such as the ones on our Buy List. Dividends are especially important right now. A 3% yield might not seem like a lot, but traders will swim to those lifeboats if things get rough. Earnings season starts next week, and I expect that the gap between winners are losers will grow even wider. Patience and discipline are our keys.

Updates on Every Buy List Stock

This week, I want to do something a little different. Since there hasn’t been much news lately, and since earnings season is about to begin, I thought I’d offer a brief update for every stock on the Buy List.

AFLAC ($AFL) broke above $53 earlier this week before pulling back. Later this month, we’ll find out how much the weaker yen has been biting away at AFL’s bottom line. After showing a little strength recently, the yen plunged again on Thursday. Yen or not, I still like AFLAC’s market position. The shares are a buy up to $54.

Bed Bath & Beyond ($BBBY) will report fiscal Q4 earnings on April 10th. On the last earnings call, BBBY said to expect Q4 earnings to range between $1.60 and $1.67 per share. The Street had been expecting $1.75, so the stock got spanked. The good news was that the stock became a very good bargain, and I sounded the alarm in mid-February. The stock has rallied very nicely since then. I’m going to keep our Buy Below at $65. I suspect BBBY will earn about $1.70 per share, give or take, but I’m more interested in hearing their outlook for the rest of 2013. Stay tuned.

CA Technologies ($CA) got off to a great start this year but has pretty much stagnated ever since. In January, I predicted the company would beat earnings, and that’s exactly what happened. On the surface, CA appears to be a dull company, but don’t let that fool you. The stock currently yields just over 4%. CA is a good buy up to $27.

Cognizant Technology Solutions ($CTSH) has drifted lower in recent weeks. If you don’t own CTSH, this is a good opportunity. The IT outsourcer soundly beat earnings in January and guided higher for Q1 and the entire year. CTSH said it sees full-year 2013 earnings of at least $4.31, which means the stock is going for 17.3 times earnings. Buy up to $82.

CR Bard ($BCR) has been rather sluggish this year. In January, the company warned that this year will be rough, but 2014 should be very good. The stock isn’t in my doghouse just yet, but I want to hear better things from them before I’m willing to raise my Buy Below price. For now, Bard is a buy up to $102.

DirecTV ($DTV) has been one of our best performers of late. Last week, I raised DTV’s Buy Below to $59 after it beat earnings by 42 cents per share. This is an excellent stock, but I think the shares may take a breather for a bit around $55 since it’s run up so quickly.

FactSet Research Systems ($FDS) has found a base around $90 per share. If you recall, the stock took a beating after reporting decent earnings. At least, I thought they were decent. Traders, however, seemed to disagree. Don’t let the sell-off scare you: FactSet is a very good company. FDS remains a buy below $95.

Fiserv ($FISV) made a new 52-week high on Monday. Fiserv is as solid as they come. Q1 earnings are due out on April 29th. Fiserv is a buy up to $88.

Ford Motor ($F) had a good sales report for March. Earnings should be out around the middle of the month. The Street currently expects 39 cents per share, which is flat from a year ago. Ford is doing well, but Europe may still be an anchor. Ford is a buy up to $15 per share.

Harris Corp. ($HRS) may be the single-best value on our Buy List right now. The stock took another hit after Oppenheimer said that Harris is running below its full-year revenue forecast. For now, I trust Harris’s record more than Oppenheimer’s. Earnings are due out at the end of the month. Harris is a buy up to $53 per share.

JPMorgan Chase ($JPM) will report Q1 earnings on Thursday, April 11th. Wall Street expects $1.38 per share. Hopefully, Jamie Dimon won’t shoot his mouth off on the earnings call. JPM has pulled back over the past few weeks. Don’t let that rattle you. JPM remains a solid buy up to $52.

Medtronic ($MDT) is another good example of a stock that fell after its earnings report but has since gained back everything it lost. Like Stryker, Medtronic has ridden the healthcare rally this year. Look for good earnings next month and another dividend increase in June. Buy below $48.

Microsoft ($MSFT) is due to report earnings on April 17th. Wall Street’s consensus is for 77 cents per share. The last earnings report was pretty good. On Wednesday, the shares hit a five-month high. If volatility makes you nervous, this is an excellent low-vol stock. Microsoft is a buy up to $30.

Moog ($MOG-A) lowered the upper end of their full-year guidance by 10 cents per share in January. The CEO said they’re off to a slow start this year. After a strong rally in December in January, the shares have pulled back recently. Moog is a buy up to $50.

Nicholas Financial ($NICK) still yields a rich 3.23% even after its recent price surge. I haven’t heard any news about the buyout offer, but I wouldn’t be surprised if others are interested in NICK. The fact is that with rates so low, big investors are looking at non-traditional places to get yield like used car loans. NICK is a good buy up to $16.

Oracle ($ORCL) got hit after a lousy earnings report. I have to apologize for this one. I thought Oracle would do much better. But never count Oracle out. I’m going to drop my Buy Below down to $35.

Ross Stores ($ROST) had a good earnings report two weeks ago and the shares have rallied. ROST is a solid buy up to $62.

Stryker ($SYK) is our second-best performer this year. But don’t chase it. Earnings are due out on April 23rd. They didn’t give a Q1 forecast, but said to expect $4.25 to $4.40 per share for all of 2013. That’s probably too low. Buy SYK anytime you see it below $66.

Wells Fargo ($WFC) remains a solid buy up to $40. Look for a strong earnings report around the middle of the month.

WEX Inc. ($WXS) announced that on April 15th, they’re changing their ticker symbol to WEX. Frankly, I like this move. I hate it when ticker symbols don’t match the name. Let me add that I kept the Buy Below on WEX at $75 despite the market price being above $75. I did this because I don’t want investors to chase this one. As disciplined investors, we wait for good stocks to come to us. Well, on Wednesday and Thursday, the stock fell below $75 during the day. WEX remains a buy up to $75 per share.

That’s all for now. Earnings season kicks off next week. Remember: We’ll see earnings reports next week from JPMorgan Chase and Bed Bath & Beyond. On Wednesday, the Fed will release the minutes from their March 29-30 meeting. This might actually be newsworthy, depending on how much they talked about ending their bond purchases. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on April 5th, 2013 at 7:20 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His