Archive for November, 2013

-

Morning News: November 25, 2013

Eddy Elfenbein, November 25th, 2013 at 6:41 amOil Prices Plunge After Iran Nuclear Deal

Europe Twin Woes Fester in ECB’s Job-to-Inflation Fight

ECB’s Hansson Says Rate Cut Options Not Fully Exhausted

Swiss Voters Reject Strictest Executive Pay Limits in Ballot

France Seeks Grandeur Abroad As Pessimism Grows At Home

Japan Is Cool Again, According To Japan’s New ‘Cool Japan Fund’

Marathon WTO Talks Likely To Leave Questions Open For Ministers

Apple Agrees to $350 Million Deal for Israel’s PrimeSense

Peugeot Set to Benefit Most in Europe From Iran Accord

Chrysler Presses Ahead With IPO Plan

Cairn India to Spend $1 Billion on Buyback

In BItcoin’s Orbit: Rival Virtual Currencies Vie for Acceptance

Jeff Miller: Weighing the Week Ahead: Will Consumers Open Their Wallets?

Be sure to follow me on Twitter.

-

ABBA 1975

Eddy Elfenbein, November 22nd, 2013 at 4:11 pm -

CWS Market Review – November 22, 2013

Eddy Elfenbein, November 22nd, 2013 at 7:11 am“It is not the employer who pays the wages; he only handles the

money. It is the product that pays the wages.” – Henry FordSo the bubble that everyone’s predicting still hasn’t arrived. For those of us who eschew market timing, this is almost like poor Linus sitting in the Pumpkin Patch waiting for the Great Pumpkin to arrive.

And stocks keep going up. The Dow Jones closed Thursday above 16,000 for the first time in its 117-year history. The index now stands at 16,009.99. We’ve gained nearly 9,500 points since the low from March 2009. This was a fairly quiet week, but we got a boost from our friends at the Fed, who signaled that the easy-money party will very likely continue.

Our Buy List is now up 34.24% for the year, which is another year-to-date record, and we again have our widest lead over the market this year (8.32%). Put it this way: one of our Buy List stocks could go completely bust sometime in the next six weeks, and we’d still be beating the S&P 500.

Next week is a holiday-shortened trading week. The stock market is closed all day on Thursday for Thanksgiving and will close at 1 p.m. on Friday. Trading volume is traditionally very low during Thanksgiving week. I’m taking some time off as well, so there won’t be an issue next week. I will, however, continue to update the blog if any big news hits.

I’ve been busily working on next year’s Buy List. I’ve had a lot of questions from readers, but no, I’m not going to reveal any changes just yet. As usual, fifteen of our stocks will stay, and we’ll have just five new additions and five deletions. I’ll announce the new Buy List, and CWS Market Review subscribers will be the first to know. Stay tuned in the next few weeks for more details.

In this week’s CWS Market Review, I’ll discuss our two recent earnings reports. Frankly, they were slightly on the disappointing side. Ross Stores, in particular, gave out weak guidance for Q4. The stock took a hit in the after-hours market, but it’s been a very big winner for us this year. We also had a stock split announcement from Fiserv. Later on, I’ll update the Buy Belows on several of our stocks. But first, let’s look at our recent earnings news.

Medtronic Earned 91 Cents per Share

On Tuesday, Medtronic ($MDT) reported fiscal Q2 earnings of 91 cents per share, which beat estimates by one penny per share. This was a solid quarter for MDT. Quarterly revenue rose 2.4% to $4.19 billion. Medtronic’s CEO Omar Ishrak said, “Our second-quarter revenue growth was in line with our outlook for the year, and we are performing at or better than the market in almost every one of our business lines.” That’s something nice to hear from your CEO.

I felt the company’s margins were a bit soft last quarter, but nothing dire. Not including the effects of currency, sales for Medtronic’s cardiac-rhythm disease-management segment rose by 5% to $1.27 billion. On the conference call, MDT said that gross margins will be slightly below the Street’s outlook. One weak spot was their spinal-products unit.

Most importantly, Medtronic reaffirmed their full-year guidance of $3.80 to $3.85 per share. They see revenue rising by 3% to 4%. Note that MDT’s fiscal year ends in April. The shares are close to the 52-week high from last week, which was the highest price in nearly eight years. The all-time high was $62 per share from December 2000. Medtronic remains a good buy up to $61 per share.

Ross Stores Disappoints

After the close on Thursday, Ross Stores ($ROST) reported Q3 earnings of 80 cents per share. This matched the Street’s expectation, but honestly, I had been expecting more. For comparison, the discount retailer earned 72 cents per share in last year’s Q3. So they’re still growing well, but perhaps there are still pockets of weakness among lower-end consumers.

In August, Ross said earnings would range between 75 and 78 cents per share, which I knew was a very conservative forecast. Sales for Q3 rose by 6% to $2.398 billion. The big number, however, is comparable-store sales, and that rose by 2% for the quarter. Again, that’s good but I was expecting a little more from Ross.

CEO Michael Balmuth said, “Third-quarter sales were in line with our guidance, while earnings were better than expected mainly due to above-plan merchandise gross margin. Operating margin of 11.3% was relatively flat to last year. As a percent of sales, an improvement in cost of goods sold was offset by an increase in selling, general and administrative expenses.”

Balmuth said Ross has adopted a “cautious outlook” for Q4. They see earnings for Q4, which is the all-important holiday shopping quarter, as ranging between 97 cents and $1.01 per share. The consensus on Wall Street was for $1.09 per share. That’s a pretty big miss. For the full year, Ross sees earnings coming in between $3.83 and $3.87 per share. That’s up from $3.53 per share last year, which included an extra week of business (or 10 cents per share for the bottom line).

Ross is still doing well, but I think the retail environment may not be as strong as I thought. Both Target ($TGT) and Walmart ($WMT) dropped recently on weak guidance. Ross is still a very sound stock, but I’m lowering my Buy Below to $79 per share.

Fiserv to Split 2-for-1

Fiserv ($FISV) announced this week that it will be splitting its stock 2-for-1. That means that shareholders will get twice the number of shares, and the stock will be cut in half.

There’s no change to your actual investment, but the increase in shares will help FISV’s liquidity. The split will come on December 16, so don’t be shocked when you see the lower share price. Fiserv hasn’t declared a split since 2001, but it announced six splits between 1991 and 2001 (all 3-for-2).

Last month, Fiserv released a very good earnings report for Q3. The company topped expectations by five cents per share. Plus, FISV is on its way to hitting its full-year forecast of $5.94 to $6.02 per share. I’ve been impressed that their operating margins are improving, and cash flow has been strong. This week, I’m raising my Buy Below to $112 per share. Naturally, the Buy Below will split next month along with FISV.

Several New Buy Below Prices

I also want to adjust a few of our Buy Below prices. Thanks to the recent rally, several of our stocks have run past my Buy Below prices. I want to make sure you always know what’s a good entry point for our stocks. I also want to stress that these Buy Below prices are not price targets. Many investors assume that the biggest gap between the current price and my Buy Below implies what I think the best value is. Not at all. If a stock is below the Buy Below, then it’s a Buy. Around here, we keep our system simple.

The Buy Below prices serve as guidance for current entry into a stock. I also factor in each stock’s volatility, so some Buy Belows will be tighter than others. That’s just how it is, and it’s not a judgment on a stock’s valuation.

In addition to the new Buy Below prices for Fiserv and Ross Stores, I’m lowering Nicholas Financial ($NICK) down to $17 per share. Again, that’s not a reflection on NICK’s outlook. I’m adjusting for the post-earnings slide. NICK is still a very good stock, and I hope to see a dividend increase soon.

This week, I’m raising CR Bard ($BCR) to $142 per share. This has been an excellent stock for us this year. The last earnings report was outstanding. In June, Bard raised its dividend for the 41st year in a row. Q4 should be another solid quarter for Bard.

I’m lifting the Buy Below on Harris ($HRS) to $67. Don’t let the tight range fool you; this is a very good stock. I don’t want anyone to chase it higher than they need to. As well as Harris has done for us this year (up 32.2%), it was dead money until April. That’s how some stocks roll, so we need to be prepared for down periods as well. Harris continues to be a very good buy.

Cognizant Technology Solutions ($CTSH) is one of the best values on our Buy List. They just beat earnings and raised guidance. I’m raising my Buy Below to $97 per share. Go CTSH!

I’m about fed up with writing about JPMorgan Chase ($JPM), and that’s probably how you feel about reading about them. While the bank continues to make a healthy profit, the management has been remarkably tone deaf regarding its public image. The latest failure was the absurd #askJPM stunt. Ugh! The bank finally reached a $13 billion settlement with the Federales. Some folks think they got off light. At least, the settlement is finally behind them, and that helped the shares. On Thursday, JPM hit a new 52-week high. I’m raising our Buy Below by $3 to $59 per share.

I have to confess that my opinion of Oracle ($ORCL) has improved recently. I had been unimpressed by the company’s recent performance, but I’ve learned not to count Larry Ellison out too quickly. Earnings are due out again just before New Year’s Day. ORCL told us to expect earnings to range between 64 and 69 cents per share. They should be able to top that. On Monday, the shares touched a six-month high. I’m raising my Buy Below on Oracle to $36 per share.

Keeping with tech, Microsoft ($MSFT) may be our biggest surprise all year. The tech giant has defied all predictions that it was hopelessly out of touch. The shares are up 42.2% this year so far. All eyes are on the Xbox One as the company’s first test of its One Microsoft strategy. I’m lifting our Buy Below to $40 per share.

Nothing seems to slow Moog ($MOG-A) down! The maker of flight-control systems has itself been a high-flier this year. The stock surged 4.1% on Thursday to reach yet another new all-time high. It’s our single biggest winner of the year, with a 58% gain. The shares have nearly doubled in the last 12 months. I’m raising our Buy Below on Moog to $68 per share.

Three more quick ones. I’m raising the Buy Below on Stryker ($SYK) by $1 to $76. I still like Wells Fargo ($WFC) a lot. I’m raising our Buy Below on WFC to $46 per share. Finally, I’m raising WEX Inc.’s ($WEX) Buy Below to $102 per share.

That’s all for now. Next week is Thanksgiving, so expect to see a very slow market. The stock market will be closed all day on Thursday, and it closes early on Friday. There won’t be an issue next week, but I’ll return for the first week of December. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review. Have a Happy Thanksgiving!

– Eddy

-

Morning News: November 22, 2013

Eddy Elfenbein, November 22nd, 2013 at 7:03 amGerman Business Morale Surges to Highest Level in 1.5 Years

German Growth Led by Domestic Economy as Investment Expands

European Banks’ Legal Tab Exceeds $77 Billion as Probes Escalate

Brent Hits One-Month High; Iran in Focus

Fannie Mae, Freddie Mac Attract Investor Groups

Yellen’s Fed Leadership is an Almost-Done Deal

U.S. to Sell Rest of GM Stake by Year-End

Apple Supplier Foxconn to Invest $40 Million in Pennsylvania

Spotify Hits a High Note: Valuation Tops $4 Billion

Telefonica Braces for More Currency Swings in Latin America

U.S. Jury Awards Apple $290 Million in Retrial Against Samsung

Roger Nusbaum: Habits of the Mentally Strong

Pragmatic Capitalism: Perhaps The Only Chart That Matters (For Now)

Be sure to follow me on Twitter.

-

Fiserv Will Split 2-for-1

Eddy Elfenbein, November 21st, 2013 at 9:42 amFiserv ($FISV) announced today that it will split its stock 2-for-1. That means that if you own it, the number of shares you have will double and the price will fall in half.

Fiserv hasn’t declared a split since 2001, but they announced six splits between 1991 and 2001 (all 3-for-2 splits). The split will happen on December 16.

-

Morning News: November 21, 2013

Eddy Elfenbein, November 21st, 2013 at 6:58 amEuro-Area Factory Production Accelerates as China Cools

BOJ Kuroda Upbeat on Global Economy

Nokia Calls on Indian Court to Unfreeze Assets

Credit Suisse to Fence Off Swiss Operations in Separate Unit

Anxiety Over Asset Bubbles From Homes to Internet Rising in Poll

US Rejects Fairholme’s Proposal to Recapitalize Fannie, Freddie

Fed QE Taper Likely in Coming Months on Data, Minutes Say

U.S. Retail Signal Rise in Demand; Inflation Tame

Goldman Sachs’ Outlook For Stocks Looks A Lot Like Jeremy Grantham’s Bubble Scenario

Google Wallet Now Comes With a Debit Card

Strong Demand for Yahoo Convertibles

Tesla Gets Top Marks in Consumer Reports Satisfaction Survey

Edward Harrison: Bullard Pushes inflation Floor Threshold, Says Tapering on Table for December

John Hempton: A Question for Tile Shop’s Institutional Shareholders

Be sure to follow me on Twitter.

-

Checking In on My 2013 Outlook

Eddy Elfenbein, November 20th, 2013 at 10:33 pmLast December, Roben Farzad asked a group of market experts to share their thoughts on the market in 2013. Here’s what I had to say.

The math is still very much in favor of stocks. Dividends are growing and bond yields are terrible. An emergent recovery in housing is helping consumers. I like Ford because it’s on the way to duplicating its U.S. turnaround in Europe. Aflac is a very well-run company that fell because the market wildly overreacted to its exposure to Europe. Moog is a classic value play. The stock has been a laggard despite giving good earnings guidance for 2013.

I think it holds up pretty well. (Please no comments on the photo.)

-

Trader Gets 30 Months for Moving Decimal Point

Eddy Elfenbein, November 20th, 2013 at 3:22 pmSmooth move, Einstein (via Fortune).

Last fall, David Miller thought he’d found a sure-fire way to dig himself out of debt.

The Rochdale Securities trader had watched Apple (AAPL) shares fall in the space of a month from above $700 to below $600. Earnings were due out Oct. 25, and Miller expected what analysts call a positive surprise.

He took a client’s order for 1,625 shares of Apple, moved the decimal point three places, and bought 1.6 million shares — a billion dollars worth — using his employer’s capital for collateral.

Unfortunately for Miller, and for Rochdale, Apple’s surprise was the other kind. Earnings missed for the second quarter in a row and gross margin guidance disappointed Wall Street. Apple went down, not up.

On paper, Miller had just lost $30 million of someone else’s money.

By the time the dust settled, Rochdale Securities had gone out of business, 40 people had lost their jobs and Miller was in federal court in Hartford, CT, pleading guilty to wire fraud charges that carried a possible sentence of 30 years in prison.

He got 30 months.

At Tuesday’s sentencing hearing, according to the Hartford Courant’s Edmund Mahoney, Miller gave a long and teary apology. “I don’t deserve to be forgiven.

-

The Fed and Communication

Eddy Elfenbein, November 20th, 2013 at 2:47 pmBen Bernanke gave an interesting speech yesterday about Federal Reserve policy and communication. You can see the complete text here. Bernanke said that one of his goals as Fed Chair was to make the Fed more transparent. I think he’s done a good job there, but the markets were surprised earlier this year when the Fed didn’t start tapering as many folks had expected. I think this episode was the impetus for Bernanke’s speech.

Let’s step back and remember that an interesting quality of monetary policy is that expectations matter. The public has to believe that you’re credible for your policy to work. If they think you’re going to stand behind your policy, then the policy will be much more effective. This is also why there’s been a growing emphasis on targeting specific economic indicators.

Bernanke that explained that in response to the crisis, the Fed had lowered interests to 0%. While they couldn’t go below 0%, the Fed could communicate their intentions to keep rates down there for a long time. At first the Fed used language to convey their intentions (“some time” or “extended period”), but the market wasn’t getting the clue. So two years ago, the Fed started using specific dates, and Wall Street finally got the idea.

The Fed kept pushing out the date, so now the market was concerned about what indicators the Fed was watching. So last December, the Fed said, “Fine, here are some numbers, but don’t freak out. These are thresholds, not triggers.”

Here’s where Bernanke explained the troubles following his June presser:

Having seen progress in the labor market since the beginning of the latest asset purchase program in September 2012, the Committee agreed in June of this year to provide more-comprehensive guidance about the criteria that would inform future decisions about the program. Consequently, in my press conference following the June FOMC meeting, I presented a framework linking the program more explicitly to the evolution of the FOMC’s economic outlook.

(…)

The framework I discussed in June implied that substantial additional asset purchases over the subsequent quarters were likely, with even more purchases possible if economic developments proved disappointing. However, following the June meeting and press conference, market yields moved sharply higher. For example, between the FOMC meetings of June and September, the 10-year Treasury yield rose about 3/4 percentage point and rates on MBS increased by a similar amount.

(…)

(M)arket participants may have taken the communication in June as indicating a general lessening of the Committee’s commitment to maintain a highly accommodative stance of policy in pursuit of its objectives. In particular, it appeared that the FOMC’s forward guidance for the federal funds rate had become less effective after June, with market participants pulling forward the time at which they expected the Committee to start raising rates, in a manner inconsistent with the guidance.

To the extent that this third factor–a perceived reduction in the Fed’s commitment to meeting its objectives–contributed to the increase in yields, it was neither welcome nor warranted, in the judgment of the FOMC. This change in expectations did not correspond to any actual lessening in the FOMC’s commitment or intention to provide the high degree of monetary accommodation needed to meet its objectives, as Committee participants emphasized in subsequent communications.

At its September 2013 meeting, the FOMC applied the framework communicated in June. The Committee’s decision at that meeting to maintain the pace of asset purchases was appropriate and fully consistent with the earlier guidance. The Committee was looking for evidence that job market gains would continue, supported by a pickup in growth. As it happened, the implications for the outlook of the evidence reviewed at the September meeting were mixed at best, while the ongoing fiscal debates posed additional risks. The Committee accordingly elected to await further evidence supporting its expectation of continued improvement in the labor market. Although the FOMC’s decision came as a surprise to some market participants, it appears to have strengthened the credibility of the Committee’s forward rate guidance; in particular, following the decision, longer-term rates fell and expectations of short-term rates derived from financial market prices showed, and continue to show, a pattern more consistent with the guidance.

-

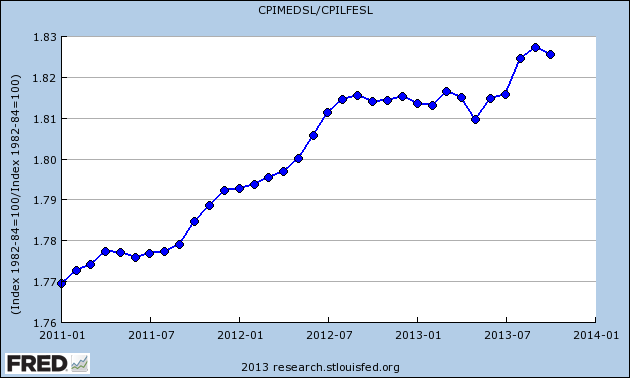

Healthcare Costs Update

Eddy Elfenbein, November 20th, 2013 at 12:02 pmThe government released the October CPI report this morning. Once again, inflation continues to be tame. Consumer prices fell 0.1% last month which was the first drop in six months. The “core rate,” which excludes food and energy, rose by 0.1%.

What I wanted to see was the trend of medical costs versus core inflation. Medical costs had been outpacing core inflation for decades, but that abruptly slowed down last year. There was, however, a recent uptick in medical costs in August, but that trend may have already faded.

Here’s the chart of medical costs divided by core inflation.

From August 2012 to July 2013, the rise in medical costs was almost the same as the rise in core prices. If this continues, that’s a game changer.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His