Archive for December, 2013

-

Dow Closes At All-Time Inflation-Adjusted High

Eddy Elfenbein, December 20th, 2013 at 4:37 pmAfter 14 years, the Dow Jones finally took out its inflation-adjusted all-time high.

I can’t be 100% certain since we don’t have the December CPI numbers, but I will say that’s very likely.

On January 14, 2000, the Dow closed at 11,722.98. Today it closed at 16,221.14 for a gain of 38.4%. This, I should add, doesn’t include dividends.

Now for some math: The high from 2000 was 69.562 times the CPI. To match that today, and then smooth out the trend to the end of the month, the CPI would have to rise by 0.08% in December. Anything less than that, and we’re at a new high.

But that 0.08% is the non-seasonally adjusted number. Assuming I have my numbers right, the not-seasonally adjusted CPI would need to rise by no more than 0.4% this month. (Apparently, December is the month with greatest seasonal impact.)

We’ll get the CPI report in a few weeks, but I’m confident in calling this the new high.

-

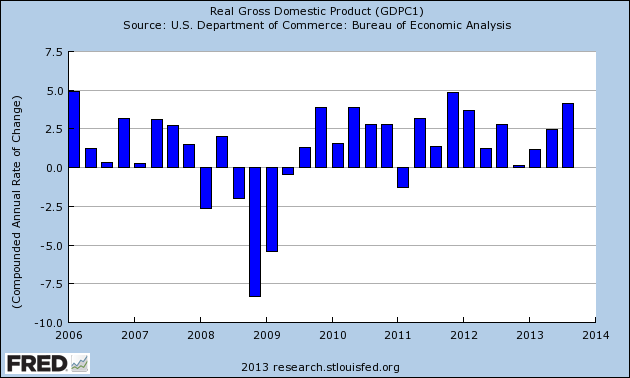

Q3 GDP +4.1%

Eddy Elfenbein, December 20th, 2013 at 9:03 amThis morning, the government revised third-quarter GDP growth up to 4.1%. That’s a surprisingly strong number — the second-best growth rate in the last 30 quarters.

This report puts the Fed’s tapering decision in more context. The economy is clearly doing somewhat better. As I’ve said, things like the 2-10 spread, the ISM report and the behavior of cyclical stocks, have all been pointing in the direction of stronger growth.

I should caution investors that this is just one data point (albeit a biggie). The third quarter began nearly six months ago, and ended three months ago. I wouldn’t be surprised to see the 10-year Treasury crack 3% very soon.

-

CWS Market Review – December 20, 2013

Eddy Elfenbein, December 20th, 2013 at 7:05 amLadies and gentlemen, here’s the 2014 Crossing Wall Street Buy List.

AFLAC ($AFL)

Bed Bath & Beyond ($BBBY)

CA Technologies ($CA)

Cognizant Technology Solutions ($CTSH)

CR Bard ($BCR)

DirecTV ($DTV)

eBay ($EBAY)

Express Scripts ($ESRX)

Fiserv ($FISV)

Ford ($F)

IBM ($IBM)

McDonald’s ($MCD)

Medtronic ($MDT)

Microsoft ($MSFT)

Moog ($MOG-A)

Oracle ($ORCL)

Qualcomm ($QCOM)

Ross Stores ($ROST)

Stryker ($SYK)

Wells Fargo ($WFC)

The five new stocks are eBay ($EBAY), Express Scripts ($ESRX), IBM ($IBM), McDonald’s ($MCD) and Qualcomm ($QCOM).

The five deletions are FactSet Research Systems ($FDS), Harris ($HRS), JPMorgan Chase ($JPM), Nicholas Financial ($NICK) and WEX Inc. ($WEX). I’ll have more to say about the Buy List changes and the new stocks next week.

To recap, I assume the Buy List is equally weighted among the 20 stocks. The “buy price” for each stock will be the closing price as of December 31, 2013. The new Buy List goes into effect on January 2, 2014, the first day of trading of the new year.

The Buy List is now locked and sealed, and I won’t be able to make any changes for the entire year. I’ll have a complete recap of 2013 at the end of the year. I’ll also have more to say about our new buys, plus I’ll give you new Buy Below prices.

Our low-turnover, long-term strategy has beaten the market for seven years in a row. I’m very excited for 2014 and I am confident we’ll extend our streak. Now let’s look at what happened to our Buy List stocks this week.

Nicholas Financial to Be Bought Out for $16 per Share

The big news for our Buy List this week, and which figured into the finalization of the Buy List for 2014, was that Nicholas Financial ($NICK) agreed to be bought out by Prospect Capital ($PSEC) for $16 per share. I’m not at all happy with this deal.

We knew there were parties interested in buying NICK, but I find this deal baffling because it’s a very low price for a buyout. The day before the buyout news came out, NICK had closed at $15.28, so it’s a premium of less than 5%. That’s tiny. Moreover, NICK had traded as high as $17.20 just two months ago. The $16-per-share offer is about 10 times trailing earnings, and it gives the dividend a 3% yield. I see no benefit in selling out at $16 per share.

A number of law firms have already announced legal threats against the deal, but this happens quite often. This time, however, I truly believe it’s a terrible price. In my view, $18 per share would be low but acceptable. If it goes forward, the deal is expected to close in April, and NICK shareholders will get $16 worth of shares in PSEC. It’s a tax-free deal, so if you plan to hold on, you’ll simply become a PSEC shareholder.

I don’t know much about PSEC. It’s a closed-end fund that specializes in targeting cheap deals. (Well, they certainly got one in NICK!) PSEC currently pays a monthly dividend of 11 cents per share, which gives the stock a rich yield, but I can’t say how sustainable it is.

Ideally, the current deal will be reviewed as it gets more scrutiny. Or possibly, someone else will make a counteroffer. Either way, NICK will not be on next year’s Buy List. For long-term shareholders, there’s no reason to sell. In fact, there is one small benefit in holding on, in that your position in PSEC will be much more liquid than it was in NICK. I’m not happy with this deal, but it looks like we’re stuck with it. At least we can say we made a very good profit with NICK. I wish them the best.

The Fed Tapers!

This week’s big economic news came on Wednesday, when the Federal Reserve announced that it would start tapering its bond purchases. Frankly, this caught me off guard. I wasn’t expecting a tapering announcement until next year. But starting next month, the Fed will reduce its bond purchases from $85 billion per month to a measly $75 billion (that’s $40 billion in Treasuries and $35 billion in mortgages).

Bear in mind, of course, that the bond buying isn’t ending. Far from it. The Fed is merely cutting back on the amount of purchases. In fact, the Fed indicated that it intends to be more accommodative going forward.

Let me explain that: The Fed reiterated its view that it expects to keep interest rates near 0% as long as the unemployment rate is above 6.5%. (It’s currently at 7.0%.) But they added a new wrinkle in their post-meeting statement. The Fed said that “it likely will be appropriate to maintain the current target range for the federal funds rate well past the time that the unemployment rate declines below 6-1/2 percent, especially if projected inflation continues to run below the Committee’s 2 percent longer-run goal.”

That “well past” bit is new, and it signals to investors that despite the taper of bond purchases, low rates will be around for a long time to come. That’s what most certainly caused the stock market to rally on Wednesday. The S&P 500 added nearly 30 points to close at a new all-time high. The Fed also raised its growth estimates a bit for 2014.

What does taper mean for us? Honestly, not much. The most important point is that the Fed is still on the side of investors. We all knew this day was coming, but no one was sure when. Like I said, I didn’t see this coming for at least a few more months. As I’ve discussed before, we’ve gotten some better economic news lately, so the Fed feels it doesn’t need to push the economy quite as hard as it did before. Now let’s look at some of our earnings reports.

FactSet Research Earns $1.22 per Share

I’ve decided to remove FactSet Research Systems ($FDS) from next year’s Buy List. This was a tough call, because FDS is a very good company. I’m afraid the current price is just too high (more than 22 times this year’s earnings estimate). I’m very firm about valuations, and I refuse to stick with a stock that’s just too darn expensive.

I know I’ve been singing the stock’s praises until recently, but as I prepared this year’s Buy List, the math on FDS simply didn’t work. Earlier this week, the company reported fiscal Q1 earnings of $1.22 per share. That was two cents below the Street’s forecast, and the stock got dinged for a 6.4% loss.

For Q2, FactSet sees revenue ranging between $225 million and $228 million, and they see earnings coming in between $1.20 and $1.23. FactSet added that the ending of a tax credit for R&D should take a three-cent bite out of earnings. Wall Street’s consensus was for $1.25 per share.

I’m going to put FactSet back on my Watch List. I hope to add it again in years to come, but it will have to be at a better valuation.

Oracle Earns 69 Cents per Share

After the bell on Wednesday, Oracle ($ORCL) reported fiscal Q2 earnings of 69 cents per share which was two cents better than expectations. The stock jumped 5.8% on Thursday and touched a 13-year high.

Without a doubt, Oracle faces some problems. Plus, spending on IT around the world has been tepid. Still, I like Oracle a lot. The big concern isn’t hard to spot: weak sales growth. For the last three quarters, Oracle has missed Wall Street’s sales forecasts. Fortunately, that streak just came to an end. For Q2, Oracle’s revenue rose 2% to $9.28 billion, which was $100 million more than the forecast. Taking a closer look at the revenue side, we see that new software sales fell 1% last quarter. These sales are important, because they’re often recurring revenue. Oracle had given us a wide range for quarterly software sales: between -4% and +6%.

On the hardware side, sales fell 3% to $714 million. These are low-margin sales, and Oracle is working to phase out these systems in favor of their premium hardware. Free cash flow rose 14% to $14.6 billion. On the conference call, Oracle said their free cash flow now exceeds that of new Buy List member IBM ($IBM).

For Q3, Oracle said they project earnings to range between 68 and 72 cents per share. The Street had been looking for 70 cents per share. The company also said it sees revenue for this quarter rising by 2% to 6%. The Street was at 4%. Importantly, Oracle projects new software sales to rise between 1% and 11% this quarter. It’s taken Oracle a while to implement its strategy, but it appears to be paying off. I’m raising my Buy Below on Oracle to $39 per share.

Ford Drops on Lower Outlook

Shares of Ford Motor ($F) got nailed on Wednesday after the automaker lowered its earnings forecast for next year. The company said it will earn between $7 billion and $8 billion next year (pre-tax), which is down from probably about $8.5 billion this year. Ford also said that its profit margins and cash flow will fall next year. The stock lost 6.3% on Wednesday, which was the biggest drop since 2011. Ford fell another 2.2% on Thursday.

While this announcement is disappointing, I still like Ford for the long term. The reason is that Ford’s problems largely revolve around dealing with its growth. The company is introducing 23 new models next year including 16 in North America. Product launches are very expensive, and they turned out to be pricier than Ford expected. They’ve also been hiring a lot more folks. That’s quite different from suffering due to a lack of sales.

Keep in mind how the auto biz works. You need to make large up-front investments in people, plants and factories for new launches, and the payoff may be years down the road. The number of launches next year is more than double this year’s number. What Ford is doing is playing for an earnings rise in 2015 and 2016.

Looking at sales by region, Ford said that pre-tax profits will fall in North America, but will rise in Europe. The company has had a difficult time in Europe, but they seem to be turning a corner. The bottom line is that Ford has had a very good year this year, and they’re not resting on their laurels. I’ve been very bullish on Ford, and the lower price makes me like it even more. To reflect this week’s sell-off, I’m lowering my Buy Below to $17 per share. This one is for patient investors.

A few things before we go. Fiserv ($FISV) split its stock 2-for-1 earlier this week. This has been a very good stock for us this year. I’m raising the Buy Below to $58 per share. I also want to lift CA Technologies ($CA) to $34 per share. Lastly, I’m raising the Buy Below on Cognizant ($CTSH) to $101 per share.

That’s all for now. The stock market will close at 1 p.m. on Tuesday and will be closed all day on Wednesday for Christmas. Despite the shortened trading, there will be a few important economic releases next week, such as personal income, orders for durable goods, and new home sales. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review. I hope everyone has a wonderful holiday season!

– Eddy

-

Morning News: December 20, 2013

Eddy Elfenbein, December 20th, 2013 at 6:27 amStandard & Poor’s Confirms ‘AAA’ Rating for Britain

S&P Warns South Africa on Twin Deficits as It Affirms Rating

Chinese Liquidity to Remain Tight in 2014 — Bank of China

Japan Stays Aggressive on Stimulus

China Rejects U.S. Corn Imports After Finding GMO Strain in Cargoes

Lew Warns Congress Debt Limit Must Be Raised No Later than Early March

Zuckerberg to Pocket $1 Billion in Facebook Stock Sale

Red Lobster to Be Split from Darden Empire

Fury and Frustration Over Target Data Breach

Why Credit Hacks Will Keep Happening

AMC Entertainment Closes Out Big Year for IPOs

Nike Fiscal 2Q Profit Jumps 40%

Fired Microsoft Manager, Pal, Charged with Insider Trading

Using Data to Make Markets Inefficient

Roger Nusbaum: The Market is Scandalous and We Have to Deal With It

Be sure to follow me on Twitter.

-

Oracle Hits 13-Year High

Eddy Elfenbein, December 19th, 2013 at 4:01 pmThanks to yesterday’s earnings report, shares of Oracle ($ORCL) got as high as $36.96 today. That’s the highest point since October 16, 2000 (that’s even before the chart range at Big Charts).

-

Morning News: December 19, 2013

Eddy Elfenbein, December 19th, 2013 at 6:35 amEurozone Ministers Agree Banking Deal Ahead of Summit

UN Lower’s India Growth Forecast to 4.8% for 2013

How Secret Currency Traders’ Club Devised Biggest Market’s Rates

Bitcoin Tumbles After China Crackdown

In Asia, Relief at News of Fed ‘Taper’

Bernanke Drop the Mic as He Exits the Fed

Deal for IMG Shows Sports’ Draw and Potential

Bayer to Acquire Drug Maker Algeta in $2.9 Billion Deal

AstraZeneca Buys Diabetes Venture for $4.1 Billion

Ford Forecast Shows Cost of Most New Models Since 2006

Saab Shares Soar on $4.5 Billion Brazil Defence Deal

Credit Suisse Fraud Exceeded $1 Billion Loss, N.J. Official Says

Facebook, Zuckerberg, Banks Must Face IPO Lawsuit

Bernanke Goes Out Like a Wrecking Ball

The Legacy of Government Debt in Europe Bodes Ill for Growth

Be sure to follow me on Twitter.

-

Oracle Earns 69 Cents Per Share

Eddy Elfenbein, December 18th, 2013 at 4:49 pmOracle ($ORCL) just reported earnings of 69 cents per share which was two cents better than expectations.

The company reported a 1 percent decrease in new software sales and Internet-based software subscriptions for the quarter.

Oracle had forecast that new software sales and subscriptions would be between down 4 percent and up 6 percent in the second quarter, which ended in November. Investors scrutinize new software sales because they generate high-margin, long-term maintenance contracts and are an important indicator of future profit.

Revenue from Oracle’s hardware systems products, which it acquired through the $5.6 billion purchase of Sun Microsystems in 2010, fell 3 percent to $714 million in the second quarter.

Oracle’s hardware revenue has fallen since it bought Sun, with Ellison saying much of that decline is due to phasing out older low-margin systems in favor Oracle’s premium hardware.

Oracle had forecast that hardware product revenue for the November quarter would decline as much as 9 percent or grow as much as 1 percent.

The shares initially rose in the after-hours session, but then they gave back those gains. They’ll offer guidance during the conference call.

-

The Fed Tapers! $10 Billion Reduction

Eddy Elfenbein, December 18th, 2013 at 2:01 pmInformation received since the Federal Open Market Committee met in October indicates that economic activity is expanding at a moderate pace. Labor market conditions have shown further improvement; the unemployment rate has declined but remains elevated. Household spending and business fixed investment advanced, while the recovery in the housing sector slowed somewhat in recent months. Fiscal policy is restraining economic growth, although the extent of restraint may be diminishing. Inflation has been running below the Committee’s longer-run objective, but longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with appropriate policy accommodation, economic growth will pick up from its recent pace and the unemployment rate will gradually decline toward levels the Committee judges consistent with its dual mandate. The Committee sees the risks to the outlook for the economy and the labor market as having become more nearly balanced. The Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance, and it is monitoring inflation developments carefully for evidence that inflation will move back toward its objective over the medium term.

Taking into account the extent of federal fiscal retrenchment since the inception of its current asset purchase program, the Committee sees the improvement in economic activity and labor market conditions over that period as consistent with growing underlying strength in the broader economy. In light of the cumulative progress toward maximum employment and the improvement in the outlook for labor market conditions, the Committee decided to modestly reduce the pace of its asset purchases. Beginning in January, the Committee will add to its holdings of agency mortgage-backed securities at a pace of $35 billion per month rather than $40 billion per month, and will add to its holdings of longer-term Treasury securities at a pace of $40 billion per month rather than $45 billion per month. The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. The Committee’s sizable and still-increasing holdings of longer-term securities should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative, which in turn should promote a stronger economic recovery and help to ensure that inflation, over time, is at the rate most consistent with the Committee’s dual mandate.

The Committee will closely monitor incoming information on economic and financial developments in coming months and will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until the outlook for the labor market has improved substantially in a context of price stability. If incoming information broadly supports the Committee’s expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective, the Committee will likely reduce the pace of asset purchases in further measured steps at future meetings. However, asset purchases are not on a preset course, and the Committee’s decisions about their pace will remain contingent on the Committee’s outlook for the labor market and inflation as well as its assessment of the likely efficacy and costs of such purchases.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the asset purchase program ends and the economic recovery strengthens. The Committee also reaffirmed its expectation that the current exceptionally low target range for the federal funds rate of 0 to 1/4 percent will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored. In determining how long to maintain a highly accommodative stance of monetary policy, the Committee will also consider other information, including additional measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments. The Committee now anticipates, based on its assessment of these factors, that it likely will be appropriate to maintain the current target range for the federal funds rate well past the time that the unemployment rate declines below 6-1/2 percent, especially if projected inflation continues to run below the Committee’s 2 percent longer-run goal. When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; James Bullard; Charles L. Evans; Esther L. George; Jerome H. Powell; Jeremy C. Stein; Daniel K. Tarullo; and Janet L. Yellen. Voting against the action was Eric S. Rosengren, who believes that, with the unemployment rate still elevated and the inflation rate well below the federal funds rate (Note: The Fed said strike those last three words) target, changes in the purchase program are premature until incoming data more clearly indicate that economic growth is likely to be sustained above its potential rate.

-

Barry Ritholtz Chats With Morgan Housel

Eddy Elfenbein, December 18th, 2013 at 9:41 am -

Nicholas Financial To Be Bought Out!

Eddy Elfenbein, December 18th, 2013 at 7:48 amNicholas Financial, Inc. (the “Company”) (NICK) announced today that it has signed an arrangement agreement dated December 17, 2013 (the “Arrangement Agreement”) whereby the Company has agreed to sell all of its issued and outstanding Common shares to an indirect wholly-owned subsidiary of Prospect Capital Corporation (“Prospect”), pursuant to a plan of arrangement (the “Arrangement”) under the Business Corporations Act (British Columbia).

Prospect (PSEC) (www.prospectstreet.com) is a closed-end investment company that lends to and invests in private and public middle market businesses. Prospect’s investment objective is to generate both current income and long-term capital appreciation through debt and equity investments.

Prospect has elected to be treated as a business development company under the Investment Company Act of 1940 (“1940 Act”). Prospect is required to comply with a series of regulatory requirements under the 1940 Act as well as applicable NASDAQ, federal and state rules and regulations. Prospect has elected to be treated as a regulated investment company under the Internal Revenue Code of 1986. Failure to comply with any of the laws and regulations that apply to Prospect could have an adverse effect on Prospect and its shareholders.

Pursuant to the terms of the Arrangement, the Company’s shareholders are to receive (subject to applicable dissenter’s rights under the Business Corporation Act (British Columbia)), in exchange for each Common share of the Company held immediately prior to the effective time of the Arrangement, the number of shares of common stock of Prospect (or fraction thereof) determined by dividing US $16.00 by the volume-weighted average price, or VWAP, of Prospect common stock for the twenty (20) trading days prior to and ending on the trading day immediately preceding the effective time of the Arrangement. In addition, each and every option to acquire Common shares of the Company outstanding immediately prior to the effective time of the Arrangement will be cancelled or transferred by the holder thereof to the Company (subject to applicable dissenters’ rights under the Business Corporations Act (British Columbia)) in exchange for a cash amount equal to the amount by which (i) the product obtained by multiplying (x) the number of Common shares of the Company underlying each option by (y) $16.00 exceeds (ii) the aggregate exercise price payable under such option.

The transactions contemplated by the Arrangement Agreement will not be consummated unless certain conditions typical for this type of transaction are either satisfied or waived prior to closing. These conditions include, among other things, that the Arrangement Agreement and the transactions contemplated thereby are approved by the securityholders of the Company in accordance with the Business Corporations Act (British Columbia) and the Company’s Articles. An information circular providing further information regarding the Arrangement Agreement and the parties thereto will be mailed to securityholders of the Company in advance of the special meeting thereof expected to be held for the purpose of approving, among other things, the Arrangement Agreement and the Arrangement contemplated thereby.

Nicholas Financial (NICK) will be bought out by Prospect Capital (PSEC) for $16 per share. The deal is expected to close in April. Note that shareholders won’t be getting cash but whatever shares of PSEC $16 works out to. You won’t be taxed when you get the shares of PSEC.

I have to admit that I’m baffled by this. I think NICK is very much selling itself short. I can’t think of another company that sold itself for 10 times trailing earnings, and a dividend yield of 3%. Management clearly wanted out. Only two months ago, NICK traded for as much as $17.20 per share. Sixteen dollars is a premium of less than 5%.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His