CWS Market Review – May 8, 2015

“The stock market is going to fluctuate. Sometimes it will

fluc down; other times it will fluc up.” – Louis Rukeyser

This week, Fed Chairwoman Janet Yellen spooked Wall Street when she said, “I would highlight that equity market valuations at this point generally are quite high.”

Uh-oh. Look, I’ve got nothing against Dr. Yellen. She’s a first-rate economist. But I’ll point out that Fed Chairs don’t exactly have a sterling record with their market calls. Remember when Alan Greenspan famously warned of the market’s “irrational exuberance” in 1996? The market doubled over the next three years. Just last summer, Yellen warned us that valuations for social media and biotech stocks were “substantially stretched.” The Nasdaq Biotech ETF (IBB) is up a cool 33% since then. I won’t even go into their dismal economic projections.

In one sense, Yellen is correct that valuations are high, if we assume that the strong dollar’s hit to earnings is going to last. But if the strong greenback’s damage is temporary, which the market’s betting on, then I don’t think we have anything to worry about.

With high valuations, the question that must always be asked is, compared to what? With bond yields so low, stocks need to be higher to compete for investors’ money. The difference now is that the bond market has recently started to turn south.

In this week’s CWS Market Review, we’ll take a closer look at the bond market’s recent grumpiness. I’ll also cover our recent Buy List earnings reports. Moog (MOG-A) pulled back on poor guidance, but both Cognizant (CTSH) and Fiserv (FISV) jumped higher on their strong earnings reports. I’ll have details in a bit. But first, let’s look at what’s got the bond market so annoyed.

Whither the Bond Market?

Suddenly, everyone’s worried about the bond market. The yield on the 10-year Treasury rose seven times in eight days. On Wednesday and Thursday, the yield got to 2.25%, which is the highest in two months.

Of course, some of this needs to be put in context. Bond yields are hardly high; they’re just higher than where they were a few weeks ago, and that was pretty darn low. The 10-year yielded 3% in early 2014, and we’re still well below that.

The 10-year yield gained 31 basis points in eight sessions. That’s enough to get people’s attention. This may sound like blasphemy, but I think some of the strength in bonds is due to a stronger economy. The evidence isn’t in just yet, but I suspect the bond market is already placing its bets.

GDP for Q1 was bad. This week’s trade data indicates that the revisions will be even worse. In fact, it’s very likely that Q1 was negative. But that data is already somewhat aged. The first quarter ended more than five weeks ago. The recent initial jobless claims have been quite strong. These are some of the lowest numbers we’ve seen in decades.

We’re also seeing that commodity prices are on the rise. Oil, in fact, has been hot. On Wednesday, West Texas Intermediate got as high as $62.58 per barrel. That’s up $20 per barrel from the March low. (Anyone else remember in February when Citigroup said oil could fall to $20 per barrel? Yeah, me neither.)

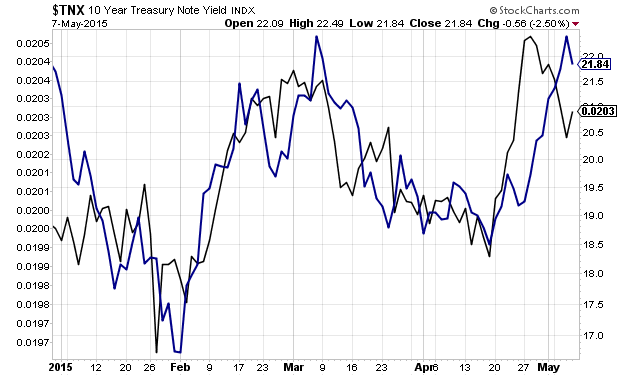

The sour mood for bonds has been mirrored in the stock market by an increase in cyclical stocks. The chart below shows how the relative strength of Tech Stocks (XLK, black line) has closely followed the path of the 10-year Treasury yield (blue line). You can see it’s a pretty close fit.

I think this suggests some hidden strengths in the economy. Or at least, that it`s stronger than people currently expect. It also means that investors are willing to leave safe havens behind and dip their toes in riskier areas of the market. It’s interesting to see that the safe and secure Utility Sector (XLU) has lagged of late.

I doubt the change in risk perception has much, if anything, to do with the Fed and the endless guessing about interest rates. The dollar’s been trending down, and gold hasn’t done much.

My advice is to ignore the bond worries. That could be an issue at some point, but we’re still a long way away. A red flag is when the 2-year yield exceeds the 10-year. The 10-year still beats the 2-year by more than 150 basis points. The smart companies are taking advantage of low yields. Just this week, Oracle (ORCL) floated $1.25 billion in 40-year bonds. Microsoft (MSFT) floated $2.25 billion of 40-year paper in February.

Investors should continue to focus on high-quality stocks like you’ll find on our Buy List. I think growth stocks will be more in favor over the next few months. Some names I especially like right now are Ford Motor (F), Ross Stores (ROST) and Wells Fargo (WFC).

Moog Beats Earnings but Lowers Guidance Again

Last Friday, Moog (MOG-A) reported fiscal-Q2 earnings of 96 cents per share. That was five cents more than estimates. Revenue came in at $637 million, which was down 2% from last year’s Q2.

Frankly, this wasn’t a good quarter. As in Q1, Moog was hurt by currency. In particular, sales dropped 15% at their Industrial Systems segment. Moog’s CEO, John Scannell, noted that the company had some unusual charges last quarter: “Excluding these charges, our underlying business performed well in the face of an adverse shift in our aircraft sales and on-going macroeconomic headwinds. As we navigate through these challenges, we continue to focus on operational improvements, strong cash flow and allocating capital to create value for our shareholders.”

In January, Moog lowered its full-year guidance from $4.25 to $3.85 per share, but that`s potentially $3.95 with share buybacks. They just lowered it again. Moog now sees full-year earnings of $3.55 per share. That includes 24 cents in special adjustments.

The market didn’t like this news at all. The shares were over $72 last week. This week, they dropped under $66. I’m not pleased with Moog’s performance this year. I’m lowering my Buy Below to $72 per share.

Cognizant Technology Solutions Earned 71 Cents per Share

On Monday, Cognizant Technology Solutions (CTSH) released a very good earnings report. The IT outsourcer earned 71 cents per share last quarter, one penny more than estimates. Their guidance had been for EPS of at least 69 cents. (CTSH is a fan of using “at least” in their forecasts.) Revenue rose 20.2% to $2.91 billion. Guidance had been for at least $2.88 billion.

For Q2, Cognizant forecasts earnings of at least 72 cents per share on revenue of at least $3.01 billion. For the whole year, they see earnings of at least $2.93 per share. That’s an increase of two cents per share from their earlier guidance. They also increased their revenue guidance from at least $12.21 billion to at least $12.24 billion.

The stock reacted very well to the earnings report. Bear in mind that CTSH had been weak going into the earnings, despite a strong year overall. I think some traders were worried that CTSH was about to drop an earnings dud. They were wrong. The stock gapped as much as 11% higher on Monday and reached a new 52-week high. The stock pulled back later in the week but finished the day on Thursday at $61.31 per share. It’s our top performer this year, with a gain of 16.43%. Not bad for early May! Cognizant remains a strong buy up to $66 per share.

Fiserv: 30 Straight Years of Double-Digit Earnings Growth

After the closing bell on Tuesday, Fiserv (FISV) reported Q1 earnings of 89 cents per share. That’s a very good number. That’s a 9% increase over last year’s Q1, and it’s three cents better than expectations. Adjusted revenue grew by 4% to $1.19 billion.

“We are pleased with our strong start to the year,“ said Jeffery Yabuki, President and Chief Executive Officer of Fiserv. “Results for the quarter were consistent with our full-year expectations, highlighted by strong operating performance and excellent growth in free cash flow.”

Fiserv reiterated their revenue and earnings forecasts for this year. They expect internal revenue to grow by 5% to 6% and EPS to range between $3.73 and $3.83. Since Fiserv made $3.37 per share last year, this year’s guidance works out to an earnings-growth rate of 11% to 14%. If that’s right, this will be Fiserv’s 30th-straight year of double-digit earnings growth. That’s simply amazing.

The shares gapped up in early trading on Wednesday. At one point, FISV hit $80.79 per share, which is just shy of a new 52-week high. I like this stock a lot, but I urge investors not to chase Fiserv. Be patient and let good stocks come to you. Fiserv is an excellent buy up to $80 per share.

Buy List Notes

That’s the end of earnings season for our 16 Buy List stocks that have quarters ending in March. We have two Buy List stocks, Hormel Foods (HRL) and Ross Stores (ROST), which ended their quarters in April. Hormel will report Q2 earnings on Wednesday, May 20th, and Ross Stores follows the next day. I’ll have more details in next week’s issue.

I also wanted to comment on last Friday’s big spike in Wabtec (WAB). The shares jumped more than 6.1%. The reason for the rally was new rules out of Washington. As it turns out, Wabtec is one of only two companies that make electronically controlled pneumatic (ECP) brakes for trains. The Department of Transportation said that trains with more than 70 tank cars will have to have ECP. If not, they can’t go more than 30 mph.

The back story is that shipping oil by rail has skyrocketed in recent years. This year, it’s projected that 374 million barrels of oil will be shipped by rail. That’s up from 30 million in 2010. More shipments means more accidents, so the Feds are trying to improve safety—and that means ECP. Wabtec is a good buy up to $103 per share.

That’s all for now. Earnings season winds down next week. There will be a few key economic reports coming our way. The retail sales report is on Wednesday. Wholesale inflation follows on Thursday, and industrial production is on Friday. Industrial production has been in a troubling downward trend since November. The March report was especially poor. I’m curious to see if this continues. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on May 8th, 2015 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His