CWS Market Review – February 12, 2016

“Know what you own, and know why you own it.” – Peter Lynch

This was another dramatic week on Wall Street. On Thursday, the S&P 500 first tested, and later broke below, the “Tchaikovsky Low” of 1,812. At its lowest point, the index touched 1,810 which it hasn’t seen in two years.

Financial stocks were hit particularly hard. Big banks like Citigroup are now going for around six times next year’s earnings estimate. The price of oil also fell to $27.39 per barrel which is a 12-year low.

In this week’s CWS Market Review, I’ll try to make sense of the chaos. Basically, there are several factors that are converging all at once, and some of them seem to make little sense. For example, in Japan, the central bank has cut interest rates to negative territory, yet the yen is rallying. That’s not what the textbooks said will happen, but confounding conventional wisdom has pretty much been the theme of 2016.

Later on, I’ll cover this week’s earnings report from Cognizant Technology Solutions. I’ll also preview four more earnings reports coming our way next week. But first, let’s take a step back and look at the macro picture.

The Macro View

Since this has been such an unusual time for the markets, I want to list a number of different trends that are shaping the financial world.

Negative Interest Rates. In an effort to get their economies moving again, a number of central banks have cut interest rates to less than 0%. So far, the market response has not been very positive. As I mentioned before, in Japan, the yen has actually strengthened under negative rates (which is good for AFLAC).

At the European Central Bank, Mario Draghi seems especially frustrated. On top of that, there’s an emerging banking crisis in Europe. A number of banks got burned by bad loans to the energy sector. This has particularly impacted Deutsche Bank, but they’re not alone. Shares of Credit Suisse just slid to a 27-year low. With the economy still fragile there, Draghi may have to come up with some more magic tricks.

Back in the U.S.A., Janet Yellen testified before Congress this week and was asked about the possibility of negative interest rates. She didn’t say she was for it, but she didn’t rule it out. Of course, that’s what central bankers say about most anything. Frankly, I think the negative-rates talk for the Fed is very premature. Things would have to get a lot worse before that becomes a serious possibility. There’s also the question of whether that policy is even legal or feasible, given our financial system. My view is that they could do it if they wanted to, but that possibility is a long way off.

No Fed Rate Increases. A big change this year has been the outlook for interest rates. Not that long ago, the market had been expecting three or four rate increases this year. Now, almost no one believes that will happen though the Fed has so far stuck to its forecasts. The futures market sees the Fed largely standing pat.

You can see the impact of this revised outlook on certain sectors of the stock market. For example, utility stocks have rallied this year. That makes sense if rates stay low for longer. Conversely, financial stocks have done quite poorly. Those banks would have liked higher rates.

Many big banks are down by 20% or 30% in the last few weeks. That explains a lot of the weakness we’ve seen at Wells Fargo (WFC) and Signature Bank (SBNY). Bear in mind that those two banks are much stronger than many other banks. The S&P Bank Index is currently about where it was in August 1996. That’s nearly 20 years of no gains.

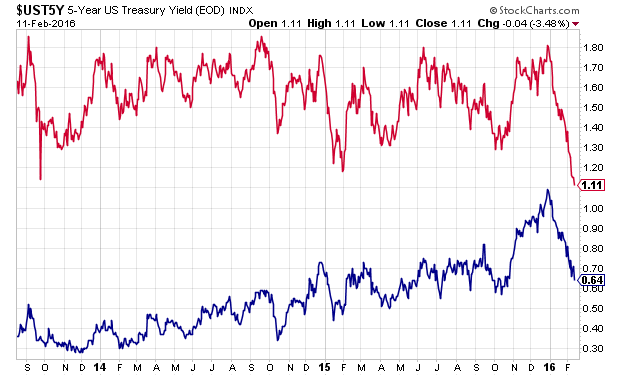

The Flattening Yield Curve. The new outlook for interest rates has also had a big impact on the yield curve. The middle part of that curve has become much flatter in recent weeks. For example, the yield on the five-year Treasury is down to 1.11%. That’s down from 1.80% on the second-to-last day of 2015. That’s a pretty stunning turnaround.

The spread between the two- and five-year Treasuries is now 47 basis points. That’s down from 70 basis points at the start of the year. Again, this reflects a belief that rates will stay low for longer. Interestingly, the spread at the longer end of the curve is largely unchanged. So I don’t think the flattening of the middle of the curve is a warning of a recession. When you see the 10-year above the 30-year, then it’s time to worry. We’re a long way from that.

Plunging Oil. The oil market continues to be in free fall. This is stunning. Every prediction of a bottom has failed. What’s interesting is that since late October, oil and the stock market have been strongly correlated. It used to be accepted wisdom that lower oil was good for our economy because it put more money in consumers’ pockets. That’s still true, but it overlooks the unpleasant side effects. For example, energy companies have cut back on hiring. Also, the junk-bond market got beaten up by some bad energy loans. In fact, that was also a factor Wells Fargo (WFC) discussed in its last earnings report. Although it’s not a major factor for Wells, it will be for other banks.

Valuation. The drop in medium-term rates has been a strong signal for prudent investors to focus on stocks with generous dividends. Let’s work some simple math. A five-year Treasury currently pays you 1.11%. That’s above half the dividend yield for the S&P 500. For the return of stocks to match the return of the five-year, stocks would have to decline by 1.11%, on average, for the next five years (this assumes dividends remain the same). That would bring the S&P 500 about 100 points lower by February 2021.

Obviously, this is a very basic analysis, but my point is to highlight the gap between the stock and bond market. The yield curve is demanding that investors buy dividend-friendly stocks. Microsoft, for example, currently yields 2.9%. They’re in little danger of cutting their dividend. The software giant generates $2 billion every month of cash flow. Wells Fargo yields 3.3%, and they’re in far better shape than they were a few years ago. In fact, it’s possible Wells will increase their dividend payout in April.

The Carry Trade. With negative interest rates, investors have crowded into the carry trade. This involves borrowing money in a currency with a low rate and investing in a currency with a high rate. You “carry” the investment across the border. This trade works up to the point where it stops working, and that’s what happened recently. A lot of traders got squeezed on their shorts of the Japanese yen, so they had to cover their trades, which pushed the yen even higher.

The Gold Rally. One surprise this year has been the strength in gold. Late last year, the yellow metal fell to around $1,050 per ounce and seemed to stay there. Lately, however, it’s caught fire. On Thursday, gold closed at $1,247 per ounce, which is an 18% gain the year. So is this a turn for gold? Possibly, but I’m a doubter. Lower real rates are good for gold, but the trade is also impacted by geopolitical events. Several tension spots around the world have flared up recently. Russia and Turkey are exchanging unpleasant looks, and North Korea is up to its usual antics. Gold tends to be the opposite of the stock market—it moves up very quickly, and slides downward very slowly.

Emerging Markets. A lot of emerging stock markets have not done well lately. This is really the effect of the U.S. dollar. This is an important point investors should understand. Since emerging markets are considered riskier, they have to offer more to draw overseas capital. When the dollar rallies, that pulls the rug out from the emerging markets. Furthermore, the money doesn’t leave slowly. It leaves very suddenly. The Emerging Markets ETF (EEM) has been battered for the last year.

Cognizant Technology Solutions Earned 80 Cents per Share

On Monday, Cognizant Technology Solutions (CTSH) reported Q4 earnings of 80 cents per share, which was two cents more than expectations. That’s a pretty good number. The company had previously said it expected earnings of at least 77 cents per share. Quarterly revenue rose 17.9% to $3.23 billion.

“We are pleased with our strong performance in 2015,” said Francisco D’Souza, CEO. “At a time when major technology shifts are disrupting all industries, clients are looking to a partner like Cognizant to work with them to create the winning business models of tomorrow at the intersection of the physical and digital worlds. Our investments in disruptive technologies, new business models and best-in-class delivery uniquely position us to enable clients to drive digital transformation at enterprise scale.”

For the year, Cognizant made $3.07 per share. Revenue rose 21.0% to $12.42 billion. Let me add some context. A year ago, their initial guidance for 2015 was for earnings of at least $2.91 per share and revenue of at least $12.21 billion. In other words, they outperformed their expectations.

Now for guidance. Cognizant sees Q1 earnings between 78 and 80 cents per share. In last week’s issue, I said I was expecting full-year guidance around $3.45 per share. The company, however, was more conservative. Cognizant expects 2016 earnings to range between $3.32 and $3.44 per share.

Wall Street did not like that. Shares of CTSH fell 7.7% on Monday. There’s no need to panic. I think the company is low-balling expectations so they can raise them later on. For now, I’m lowering my Buy Below on Cognizant to $58 per share.

Four Buy List Earnings Reports Next Week

Next week, three of our Buy List stocks will report Q4 earnings. We also have one stock, Hormel Foods (HRL), which is due to report, but they’re actually an early bird from the next cycle, as their fiscal quarter ended at the end of January.

On February 16, Cerner, Express Scripts and Hormel are due to report. Shares of Cerner (CERN) are still hurting from the unexpectedly weak outlook they gave late last year. But I think the selling is overdone. Wall Street expects Q4 earnings of 57 cents per share, which is a healthy increase over the 47 cents per share they made in Q4 of 2014.

In October, Express Scripts (ESRX) said they expect full-year 2015 earnings of $5.51 to $5.55 per share. That implies Q4 earnings of $1.54 to $1.58 per share. The shares dropped sharply last month after the company got into a public spat with Anthem (ANTM). I think these companies can work out their differences.

Not only was Hormel our best stock in 2015, but it’s also been our best stock so far in 2016. Through Thursday, the Spam stock is up 5.44% YTD. Wall Street expects fiscal Q1 earnings of 73 cents per share. That sounds about right.

Hormel also split 2-for-1 this week. That means shareholders now have twice as many shares. For track-record purposes, I assume the Buy List is a $1 million portfolio that starts the year with $50,000 in each stock. For Hormel, that was 632.2711 shares bought at $79.08. With the split, that’s now 1,264.5422 shares at $39.54. Hormel’s new Buy Below is $41 per share.

Lastly, Wabtec will report earnings on February 18. Their Q3 report was not good, and the shares have been punished ever since. The company sees Q4 earnings of $1.05. On Wednesday, the shares got a nice bounce after the board authorized a new $350 million share-buyback plan.

That’s all for now. The stock market will be closed on Monday in honor of George Washington’s birthday. (The NYSE, rightly, does not call it President’s Day.) In addition to the earnings reports, we can look forward to the industrial-production report on Wednesday. The latest Fed minutes will come out Wednesday afternoon. Then the CPI report comes out on Friday. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on February 12th, 2016 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His