Archive for June, 2016

-

Digesting Tesla’s SolarCity Bid

Eddy Elfenbein, June 22nd, 2016 at 3:49 pm -

Buy List ETF Update

Eddy Elfenbein, June 22nd, 2016 at 9:48 amI wanted to let everyone know that we have BIG NEWS coming soon.

I’m currently in a legal “blackout” period so I’m limited in what I can say to you.

But I can say that something is definitely coming.

Stay tuned!

-

Morning News: June 22, 2016

Eddy Elfenbein, June 22nd, 2016 at 7:21 amBrexit Polls and Markets Disagree in Campaign’s Final Hours

In SolarCity Bid, Tesla’s Musk Targets Customers Wanting All

Close a Nuclear Plant, Save Money and Carbon, Improve the Grid, Says PG&E

Apple Pays Back E-Book Buyers Following Settlement

Hyperloop One Explores Building High-Speed Transport System in Moscow

FedEx Posts $70 Million Loss, Gives Cautious Outlook

Teva and Allergan Sell Generic Drugs to Impax In Latest Divestiture

Former Bangladesh Bank Chief Blames Global System for Theft

Volkswagen Leaders Struggle to Appease Shareholders at Meeting

Mitsubishi Motors Expects to Swing to $1.38 Billion Net Loss

A $541 Million Loss Haunts Deutsche Bank And Former Trader Dixon

United: Catching Up From a Long Delay

Ex-Jet QB Sanchez Among Athletes Cheated in Investment Fraud

Josh Brown: Five-Word Financial Advice For New Graduates

Be sure to follow me on Twitter.

-

Yellen Warns

Eddy Elfenbein, June 21st, 2016 at 12:50 pmStocks Fluctuate as Yellen Warns of ‘Brexit’ Consequences

Fed Chair Janet Yellen Warns That U.S. Economy Faces ‘Considerable Uncertainty’

Yellen Warns Global Turbulence Could Hit Growth

Janet Yellen Warns of Domestic, Global Risks to US Economy

Yellen Warns of ‘Considerable Uncertainty’

Yellen Warns Against Fed Reforms

Yellen Warns on Waiting Too Long to Hike

-

Janet Yellen’s Testimony

Eddy Elfenbein, June 21st, 2016 at 10:03 amHere’s what Janet Yellen will be saying to the Senate Banking Committee today:

Chairman Shelby, Ranking Member Brown, and other members of the Committee, I am pleased to present the Federal Reserve’s semiannual Monetary Policy Report to the Congress. In my remarks today, I will briefly discuss the current economic situation and outlook before turning to monetary policy.

Current Economic Situation and Outlook

Since my last appearance before this Committee in February, the economy has made further progress toward the Federal Reserve’s objective of maximum employment. And while inflation has continued to run below our 2 percent objective, the Federal Open Market Committee (FOMC) expects inflation to rise to that level over the medium term. However, the pace of improvement in the labor market appears to have slowed more recently, suggesting that our cautious approach to adjusting monetary policy remains appropriate.

In the labor market, the cumulative increase in jobs since its trough in early 2010 has now topped 14 million, while the unemployment rate has fallen more than 5 percentage points from its peak. In addition, as we detail in the Monetary Policy Report, jobless rates have declined for all major demographic groups, including for African Americans and Hispanics. Despite these declines, however, it is troubling that unemployment rates for these minority groups remain higher than for the nation overall, and that the annual income of the median African American household is still well below the median income of other U.S. households.

During the first quarter of this year, job gains averaged 200,000 per month, just a bit slower than last year’s pace. And while the unemployment rate held steady at 5 percent over this period, the labor force participation rate moved up noticeably. In April and May, however, the average pace of job gains slowed to only 80,000 per month or about 100,000 per month after adjustment for the effects of a strike. The unemployment rate fell to 4.7 percent in May, but that decline mainly occurred because fewer people reported that they were actively seeking work. A broader measure of labor market slack that includes workers marginally attached to the workforce and those working part-time who would prefer full-time work was unchanged in May and remains above its level prior to the recession. Of course, it is important not to overreact to one or two reports, and several other timely indicators of labor market conditions still look favorable. One notable development is that there are some tentative signs that wage growth may finally be picking up. That said, we will be watching the job market carefully to see whether the recent slowing in employment growth is transitory, as we believe it is.

Economic growth has been uneven over recent quarters. U.S. inflation-adjusted gross domestic product (GDP) is currently estimated to have increased at an annual rate of only 3/4 percent in the first quarter of this year. Subdued foreign growth and the appreciation of the dollar weighed on exports, while the energy sector was hard hit by the steep drop in oil prices since mid-2014; in addition, business investment outside of the energy sector was surprisingly weak. However, the available indicators point to a noticeable step-up in GDP growth in the second quarter. In particular, consumer spending has picked up smartly in recent months, supported by solid growth in real disposable income and the ongoing effects of the increases in household wealth. And housing has continued to recover gradually, aided by income gains and the very low level of mortgage rates.

The recent pickup in household spending, together with underlying conditions that are favorable for growth, lead me to be optimistic that we will see further improvements in the labor market and the economy more broadly over the next few years. Monetary policy remains accommodative; low oil prices and ongoing job gains should continue to support the growth of incomes and therefore consumer spending; fiscal policy is now a small positive for growth; and global economic growth should pick up over time, supported by accommodative monetary policies abroad. As a result, the FOMC expects that with gradual increases in the federal funds rate, economic activity will continue to expand at a moderate pace and labor market indicators will strengthen further.

Turning to inflation, overall consumer prices, as measured by the price index for personal consumption expenditures, increased just 1 percent over the 12 months ending in April, up noticeably from its pace through much of last year but still well short of the Committee’s 2 percent objective. Much of this shortfall continues to reflect earlier declines in energy prices and lower prices for imports. Core inflation, which excludes energy and food prices, has been running close to 1-1/2 percent. As the transitory influences holding down inflation fade and the labor market strengthens further, the Committee expects inflation to rise to 2 percent over the medium term. Nonetheless, in considering future policy decisions, we will continue to carefully monitor actual and expected progress toward our inflation goal.

Of course, considerable uncertainty about the economic outlook remains. The latest readings on the labor market and the weak pace of investment illustrate one downside risk–that domestic demand might falter. In addition, although I am optimistic about the longer-run prospects for the U.S. economy, we cannot rule out the possibility expressed by some prominent economists that the slow productivity growth seen in recent years will continue into the future. Vulnerabilities in the global economy also remain. Although concerns about slowing growth in China and falling commodity prices appear to have eased from earlier this year, China continues to face considerable challenges as it rebalances its economy toward domestic demand and consumption and away from export-led growth. More generally, in the current environment of sluggish growth, low inflation, and already very accommodative monetary policy in many advanced economies, investor perceptions of and appetite for risk can change abruptly. One development that could shift investor sentiment is the upcoming referendum in the United Kingdom. A U.K. vote to exit the European Union could have significant economic repercussions. For all of these reasons, the Committee is closely monitoring global economic and financial developments and their implications for domestic economic activity, labor markets, and inflation.

Monetary Policy

I will turn next to monetary policy. The FOMC seeks to promote maximum employment and price stability, as mandated by the Congress. Given the economic situation I just described, monetary policy has remained accommodative over the first half of this year to support further improvement in the labor market and a return of inflation to our 2 percent objective. Specifically, the FOMC has maintained the target range for the federal funds rate at 1/4 to 1/2 percent and has kept the Federal Reserve’s holdings of longer-term securities at an elevated level.

The Committee’s actions reflect a careful assessment of the appropriate setting for monetary policy, taking into account continuing below-target inflation and the mixed readings on the labor market and economic growth seen this year. Proceeding cautiously in raising the federal funds rate will allow us to keep the monetary support to economic growth in place while we assess whether growth is returning to a moderate pace, whether the labor market will strengthen further, and whether inflation will continue to make progress toward our 2 percent objective. Another factor that supports taking a cautious approach in raising the federal funds rate is that the federal funds rate is still near its effective lower bound. If inflation were to remain persistently low or the labor market were to weaken, the Committee would have only limited room to reduce the target range for the federal funds rate. However, if the economy were to overheat and inflation seemed likely to move significantly or persistently above 2 percent, the FOMC could readily increase the target range for the federal funds rate.

The FOMC continues to anticipate that economic conditions will improve further and that the economy will evolve in a manner that will warrant only gradual increases in the federal funds rate. In addition, the Committee expects that the federal funds rate is likely to remain, for some time, below the levels that are expected to prevail in the longer run because headwinds–which include restraint on U.S. economic activity from economic and financial developments abroad, subdued household formation, and meager productivity growth–mean that the interest rate needed to keep the economy operating near its potential is low by historical standards (This is the Wicksell natural rate stuff – Eddy). If these headwinds slowly fade over time, as the Committee expects, then gradual increases in the federal funds rate are likely to be needed. In line with that view, most FOMC participants, based on their projections prepared for the June meeting, anticipate that values for the federal funds rate of less than 1 percent at the end of this year and less than 2 percent at the end of next year will be consistent with their assessment of appropriate monetary policy.

Of course, the economic outlook is uncertain, so monetary policy is by no means on a preset course and FOMC participants’ projections for the federal funds rate are not a predetermined plan for future policy. The actual path of the federal funds rate will depend on economic and financial developments and their implications for the outlook and associated risks. Stronger growth or a more rapid increase in inflation than the Committee currently anticipates would likely make it appropriate to raise the federal funds rate more quickly. Conversely, if the economy were to disappoint, a lower path of the federal funds rate would be appropriate. We are committed to our dual objectives, and we will adjust policy as appropriate to foster financial conditions consistent with their attainment over time.

The Committee is continuing its policy of reinvesting proceeds from maturing Treasury securities and principal payments from agency debt and mortgage-backed securities. As highlighted in the statement released after the June FOMC meeting, we anticipate continuing this policy until normalization of the level of the federal funds rate is well under way. Maintaining our sizable holdings of longer-term securities should help maintain accommodative financial conditions and should reduce the risk that we might have to lower the federal funds rate to the effective lower bound in the event of a future large adverse shock.

Thank you. I would be pleased to take your questions.

-

Morning News: June 21, 2016

Eddy Elfenbein, June 21st, 2016 at 7:23 amWith Two Days To Go, Britain’s EU Referendum on a Knife-Edge

Brexit Vote in Balance in Polls as Soros Warns of Pound Plunge

German Market Sentiment Unexpectedly Rises Before U.K. Vote

The Fed Gets an Attitude Adjustment

Supreme Court Sides With R.J. Reynolds in RICO Case

SoftBank President Nikesh Arora to Step Down

Tencent Seals Deal to Buy ‘Clash of Clans’ Developer Supercell for $8.6 Billion

Boeing Signs Deal to Sell Jets to Iran’s State Airline

United Continental Targets $3.1 Billion in Revenue, Efficiency Gains

Credit Suisse Chief Contends With Rising Tensions, and a Sinking Stock

A Desperate Search for Gold After Brazil’s Worst Mining Disaster Ever

Carl Icahn Bid Pushes Shares of Federal-Mogul Up

Here Are The Tech Companies People Are Dying to Work For, According to LinkedIn

Cullen Roche: The Three Types of Financial Forecasters

Jeff Carter: Heuristics. Sometimes They Lead to Bad Decisions

Be sure to follow me on Twitter.

-

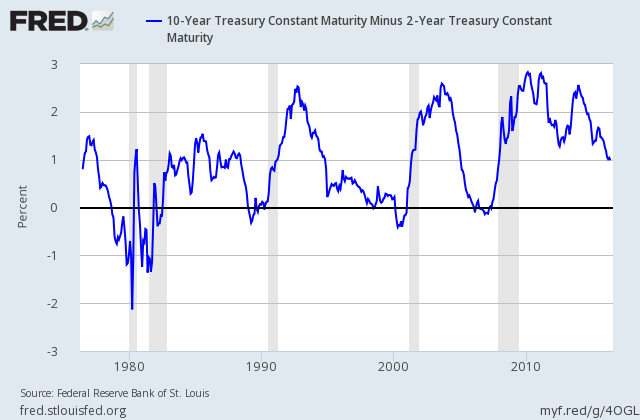

The 2/10’s Track Record

Eddy Elfenbein, June 20th, 2016 at 10:06 pmThere are lots of good metrics that tell you how well the economy did. There are very few that tell you how well the economy is doing. But there are almost none that tell you how well the economy is about to do.

One example of the last one is the spread between the 2- and 10-year Treasury yields. When the spread has turned negative, it’s been a fairly good indicator that a recession is close by.

Check out this chart showing the 2/10 spread along with the recession periods (the gray shaded areas).

That’s not bad. Compared with the Fed or Wall Street, it’s outstanding.

I wanted to run the numbers and see how well the 2/10 spread did. Here’s the 2/10 spread versus the number of times the economy was in recession 12 months in the future.

Lower Upper Recession Months Total Months Under -0.50 13 24 -0.49 -0.01 22 49 0.00 0.25 8 47 0.26 0.50 1 46 0.51 0.75 4 39 0.76 1.00 2 39 1.01 1.50 3 85 1.51 2.00 3 56 2.01 Over 0 83 If the chart doesn’t make sense, here’s what I did: I sorted each month by its 2/10 spread and then I sorted the months into nine different buckets. (I’ve listed the upper and lower bounds on the table.) Next I looked exactly 12 months into the future and counted the total number of months and the number of months the economy was officially in recession.

In short, the lower the spread, the greater the odds of a recession. The tipping point is about 0.12%. Right now, the spread is at 0.92.

Exxon Surges Back

Eddy Elfenbein, June 20th, 2016 at 12:20 pmExxon Mobil (XOM) obviously follows the course of world oil markets. The stock plunged from an intra-day high of $104.76 on July 29, 2014 to an intra-day low of $66.55 on August 24, 2015. That’s a brutal loss of 36% in a little over a year.

But now XOM is hot again. The shares touched $91.59 today. That ties a 16-month high. The stock has made back roughly two-thirds of what it lost.

The market gods are capricious and rarely boring.

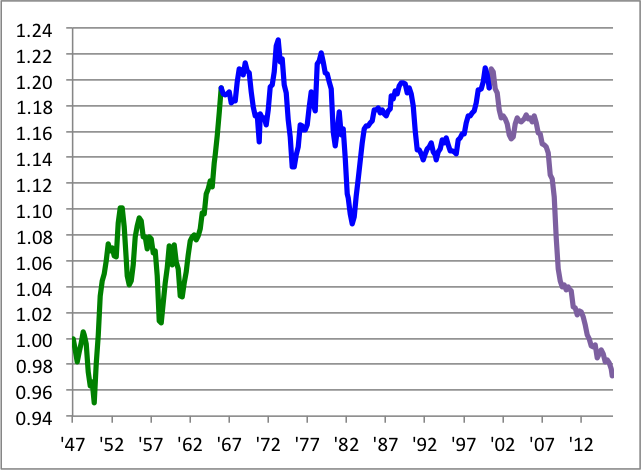

The Three Stages of the Post-War Economy

Eddy Elfenbein, June 20th, 2016 at 12:02 pmHere’s a look at the growth of the U.S. GDP in real terms since 1947, but I’ve made one major change: I’ve divided the data series by a trend line growing at 3.2% per year.

Doing this shows the post-war economy in three distinct stages. In the early post-war period, from 1947 to 1966 (in green), the economy grew faster than 3.2% per year. Then, from 1966 to 2000 (in blue), the economy mostly kept pace with the 3.2% trend line. The final portion is since 2000 (in purple) as the economy has markedly lagged the 3.2% trend line.

Let me make it clear that I’m adding an artificial framework to this data. That criticism is accurate. Still, I believe I’m doing this in a fair way, and seen my way, the economy clearly outlines three different periods.

You can surely quibble with the precise turning points. I think some people may claim that the post-war extended until 1973. Either way, I don’t think these shifts are truly quite so abrupt, but the larger trend is obvious.

Why is this so?

I’ve left out an important variable, which is population growth. After WW2, the United States had a famous Baby Boom. In recent years, fertility rates have dropped although immigration has increased.

Adjusting for population, I wonder if we’ve seen a large drop-off at all.

But if we look at GDP growth per capita, I’m curious which age cohort ought to be used. Should we use the entire population, or would it be more appropriate to use those in the workforce? I’m not sure of the right answer. Perhaps the aging population doesn’t make our recent economic growth seem so poor.

Are we truly worse off, or are we just getting older? I don’t know the answer.

Market Set to Rally as “Remain” Gains

Eddy Elfenbein, June 20th, 2016 at 7:20 amRemain isn’t going away!

The stock market looks to open very strong today. The S&P 500 futures are currently pointing to a gain of 27 points.

The latest polls are showing a gain for the “Remain” camp in this week’s Brexit vote. The British pound is close to making its biggest gain in eight years. The murder of MP Jo Cox may have influenced the latest results.

Janet Yellen plans to speak before Congress this week. She mentioned that Brexit is an issue facing the Fed.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His