Archive for October, 2016

-

Biotech Stocks Slide

Eddy Elfenbein, October 21st, 2016 at 3:53 pm -

MSFT ATH

Eddy Elfenbein, October 21st, 2016 at 12:24 pmThanks to yesterday’s earnings report, shares of Microsoft (MSFT) have finally broken out to a new all-time high.

-

CWS Market Review – October 21, 2016

Eddy Elfenbein, October 21st, 2016 at 7:08 am“There is a danger of expecting the results of the future to be predicted from the past.” – John Maynard Keynes

Before I get to today’s newsletter, I have an exciting announcement. Our Buy List ETF is now alive and trading! The official name of the ETF is the AdvisorShares Focused Equity ETF. The ticker symbol is CWS, for Crossing Wall Street! Thanks to everyone for your support. You can see more details in this video.

Now let’s get to this week’s market, which has been all about earnings. So far, we’ve had five Buy List stocks report earnings, and all five have beaten Wall Street’s estimates—some by quite a bit. On Thursday, shares of Snap-on jumped more than 6.6%. After the bell, Microsoft broke out to an all-time high, and Alliance Data Systems finally joined the Dividend Payers Club. ADS initiated a 52-cent quarterly dividend. In this week’s CWS Market Review, I’ll go over our Buy List earnings reports. I’ll also preview the nine (!) Buy List earnings reports we have next week.

79 Straight Days Near an All-Time High

Ryan Detrick highlighted a remarkable stat: The S&P 500 has now gone 79 days in a row of closing within 3% of its all-time high close. That’s amazing. For nearly four months, we’ve always been at or near a new all-time high. Yet, despite being so close to a new record, the index has only made it 10 times. In fact, the S&P 500 has now gone 46 days without making a new high. It’s as if the market is closely stalking its prey but always holding back before it strikes.

We’re still early in the earnings season, but it looks like the S&P 500 will show very slight earnings growth for Q3. Until recently, analysts had been forecasting yet another decline. This means the earnings recession is officially behind us. We’re on track for our first quarterly increase in sales and earnings since Q4 2014. Interestingly, trading volume has been quite low. The WSJ notes that “the past eight trading sessions have included the third and fourth lowest-volume days.”

Last Friday, Wells Fargo (WFC), our problem child, was the first Buy List stock to report Q3 earnings. This is such a frustrating story because the bank had been doing so well, and now we see how much bad behavior was going on behind the scenes.

I’m glad to see Tim Sloan take over as the new CEO, but he needs to do a lot of work to repair WFC’s reputation. At least the bank is still making a nice profit. On Friday, Wells reported earnings of $1.03 per share which was two cents more than estimates. On the earnings call, Sloan didn’t exactly impress analysts as he dodged important questions.

For Q3, total revenue came in at $22.328 billion, which was slightly higher than the expectations of $22.21 billion. Total average loans were up 7% to $957.5 billion. Total average deposits were up 5% to $1.3 trillion. In other words, Wells is a very, very big place.

For now, shares of WFC seem to have stabilized. I’m so frustrated with this bank. This week, I’m lowering my Buy Below on Wells Fargo to $47 per share.

Four Buy List Reports on Thursday

We had four more Buy List earnings reports on Thursday. Before the opening bell,

Alliance Data Systems (ADS) reported Q3 earnings of $4.74 per share which easily beat the company’s forecast of $4.42 per share. Wall Street had been expecting $4.44 per share. ADS’s quarterly revenue rose 19% to $1.9 billion.For the rest of 2016, ADS sees revenue of $7.2 billion and core EPS of $16.90 per share. That translates to Q4 guidance of $1.9 billion in revenue and core EPS of $4.64. Wall Street had been expecting $4.93 per share.

Ed Heffernan, president and chief executive officer of Alliance Data, commented, “It was the largest quarter in our history, with $1.9 billion in revenue and $4.74 in core EPS. The over-performance to guidance was significant and was driven by both underlying strength in the business, which we have passed through to annual guidance, as well as timing, which will reverse in the fourth quarter.

The initial guidance for 2017 is for 10% growth in revenue and core EPS. ADS also initiated a dividend of 52 cents per share. That comes to a yield of about 1%. The disappointing guidance helped knock the shares down 4.7% in Thursday’s trading.

ADS has been a rough stock for us this year, but I still like what I see. This was a good earnings report even though traders sold the stock. I’m lowering my Buy Below on ADS to $214 per share.

In last week’s issue, I said that Signature Bank (SBNY) was going to report on Tuesday. That was incorrect. My apologies. SBNY released its earnings report on Thursday morning. For Q3, the bank reported earnings of $2.11 per share. That beat Wall Street’s estimate of $2.04 per share. SBNY’s net interest margin was 3.14%, which is down eight basis points from last year.

Signature had good news about its suffering medallion business:

“This quarter, Signature Bank effectively put the Chicago taxi medallion portfolio issues behind us, while growing deposits in excess of $1.8 billion. As we grow, we continue to expand our geographic outreach for securing deposits on a national basis across a number of industries. Our capabilities, service and trusted reputation for safety have always enabled the Bank to compete with major financial institutions throughout the New York metropolitan area. Now, these attributes afford us the opportunity to garner deposits in other regions of the country as well,” stated Joseph J. DePaolo, President and Chief Executive Officer.

Signature’s deposits rose 6.1% last quarter to $31.4 billion. Shares of SBNY fell 2.5% on Thursday. This one is starting to look cheap. I’m lowering my Buy Below price on Signature Bank to $125 per share.

Snap-on (SNA) made its bid to be the star of this earnings season. For Q3, the company said it made $2.22 per share. That beat expectations by seven cents per share. Quarterly revenue rose 1.5% to $834.1 million, which was below expectations. The stock gapped up over 6.6% on Thursday.

For their outlook, Snap-on said:

Snap-on expects to make continued progress during the balance of 2016 along its defined runways for coherent growth, leveraging capabilities already demonstrated in the automotive-repair arena and developing and expanding its professional customer base, not only in automotive repair, but also in adjacent markets, additional geographies and other areas, including in critical industries, where the cost and penalties for failure can be high. In pursuit of these initiatives, Snap-on now anticipates that capital expenditures in 2016 will approximate $80 million, of which $56.6 million was incurred through the end of the third quarter. Snap-on presently expects that its full-year 2016 effective income tax rate will be slightly below its full-year 2015 rate.

This was a good report. Snap-on remains a buy up to $166 per share.

After the bell on Thursday, Microsoft (MSFT) reported fiscal Q1 earnings of 76 cents per share. That beat estimates by eight cents per share. In after-hours trading, MSFT jumped to $60.68 per share. If that holds up in Friday’s trading, that will mark Microsoft’s first all-time high since December 30, 1999.

This was a very good quarter for Microsoft. Quarterly revenue rose 5% to $22.33 billion, which topped expectations of $21.7 billion. The bright spot for Microsoft continues to be its cloud business. Adjusted revenue rose by 10% for that sector, while revenue for Microsoft Office was up by 8%. Revenue growth for Windows was flat, while Microsoft’s gaming division saw its revenue drop by 5%.

CEO Satya Nadella said that Microsoft’s cloud business is on pace to generate annual sales of $13 billion, and to hit $20 billion for the next fiscal year. I’m lifting my Buy Below on Microsoft to $63 per share.

Nine Buy List Earnings Reports Next Week

Next week is a very big week for earnings. Three Buy List stocks report on Tuesday, followed by two more on Wednesday and another four on Thursday.

On Tuesday, CR Bard, Wabtec and Express Scripts are due to report. (In last week’s issue, I incorrectly said that WAB was going to report this week.) CR Bard (BCR) has had a very good year for us, although the shares are still below their July high. For Q3, Bard said they see earnings ranging between $2.51 and $2.55 per share. Bard sees full-year earnings coming in between $10.10 and $10.20 per share. Those are good numbers. Wall Street expects $2.56 per share.

Wabtec (WAB) has been having a difficult year, but I still like the company. The problem is its freight business which has been under pressure. WAB lowered its full-year earnings to a range of $4 to $4.20 per share. The previous range was $4.30 to $4.50 per share.

In July, Express Scripts (ESRX) told us they see Q3 earnings ranging between $1.72 and $1.76 per share. They also bumped up the low end of their full-year forecast by two pennies. The pharmacy-benefits manager now expects 2016 earnings to range between $6.33 and $6.43 per share. That means the stock is going for about 11 times this year’s earnings.

On Wednesday, Fiserv and Biogen are due to report. In August, Fiserv (FISV) raised its full-year range to $4.38 to $4.45 per share. For context, Fiserv earned $3.87 per share last year, which means that this should be Fiserv’s 30th straight year of double-digit earnings growth. For Q3, Wall Street expects $1.13 per share.

Three months ago, Biogen (BIIB) had a blow-out earnings report, and the stock soared. The biotech firm also offered optimistic guidance for the rest of this year. Biogen sees 2016 earnings ranging between $19.70 and $20 per share, which is more than Wall Street had been expecting.

On Thursday, AFLAC, Ford Motor, Stericycle and Stryker will report.

Three months ago, AFLAC (AFL) gave us a range for Q3 of $1.58 to $1.86 per share. That’s a huge range. Maybe they’re as confused by the currency market as everyone else. Still, it’s nice to have forex helping AFLAC’s bottom line.

Ford Motor (F) said it will be halting production of its F-150 for a week. That’s not highly unusual but it may suggest that demand isn’t as strong as they expected. Q3 was probably a slow one for Ford. Wall Street expects only 22 cents per share. The company has maintained an optimistic forecast.

Stericycle (SRCL) has been our worst performer this year. It’s down 38% YTD. I’m concerned that Stericycle’s management has grown overly reliant on smaller mergers and “rollups” in an attempt to mask slowing organic sales. As a result, the earnings quality has gradually deteriorated. Stericycle said that this year’s earnings will range between $4.68 and $4.75 per share. For Q3, Wall Street expects $1.17 per share.

In July, Stryker (SYK) said it expects Q3 earnings to range between $1.33 and $1.38 per share. That’s less than I was expecting. For all of 2016, Stryker expects earnings to range between $5.70 and $5.80 per share. The previous range had been $5.65 to $5.80 per share. Stryker is doing well, but I’m afraid the dollar will be a headwind for the next few quarters.

That’s all for now. Next week will be dominated by earnings reports. On Tuesday, we’ll get an update on consumer confidence. The last report was quite strong. On Thursday, we’ll get the durable-goods report for September. On Friday, the government will release its initial report on Q3 GDP. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: October 21, 2016

Eddy Elfenbein, October 21st, 2016 at 7:03 amHedge Funds Hurt as Investors Remove $28 Billion in 3 Months

Is Oil Production Still Headed For A Cliff?

British America Tobacco Offers to Buy Reynolds American

Ericsson Is Suffering in North America

Indian Bank Authorities Say 3.2 Million Debit Cards Hacked

Bombardier to Scrap 7,500 More Jobs as CEO Deepens Cost Cuts

That Fine-Looking Mercedes Isn’t for Everyone

GE Beats on Profit But Cuts Revenue Target on Oil, Gas Weakness

AT&T Has 120 Billion Reasons to Approach Time Warner Cautiously

Venmo Is On Track to Process $20 Billion in Payments Per Year

Didi, a Key Player In Asia’s Ride-Hailing Market, Says It’s ‘Definitely Going Global’

Baby Boomers Are Getting Too Old for Sports Cars

‘Jac the Knife’ Nasser Is Stepping Down as BHP Billiton Chairman

Cullen Roche: The Biggest Risk of a Clinton Presidency

Be sure to follow me on Twitter.

-

Three Buy List Earnings Reports This Morning

Eddy Elfenbein, October 20th, 2016 at 10:33 amThis morning, Alliance Data Systems (ADS) reported Q3 earnings of $4.74 per share which easily beat the company’s expectation of $4.42 per share. Wall Street had been expecting $4.44 per share. Quarterly revenue rose 19% to $1.9 billion.

For the rest of the year, the company sees revenue of $7.2 billion and core EPS of $16.90 per share. That translates to Q4 guidance of $1.9 billion in revenue and core EPS of $4.64. Wall Street had been expecting $4.93 per share.

The initial guidance for 2017 is for 10% growth in revenue and core EPS. ADS also initiated a dividend of 52 cents per share. That comes to a yield of about 1%. The shares are currently down about 2%.

Signature Bank (SBNY) reported Q3 earnings of $2.11 per share. That beat Wall Street’s estimate of $2.04 per share. The bank’s net interest margin was 3.14% which is down eight basis points from last year.

SBNY said they took “significant measures” to put the Chicago medallion loans behind them. Deposits for the quarter rose 6.1% to $31.4 billion. The shares are currently down about 4% in today’s trading.

Snap-on (SNA) is making its bid to be the star of this earnings season. For Q3, the company said it made $2.22 per share. That beat expectations by seven cents per share. Quarterly revenue rose 1.5% to $834.1 million which was below expectations.

For their outlook, Snap-on said:

Snap-on expects to make continued progress during the balance of 2016 along its defined runways for coherent growth, leveraging capabilities already demonstrated in the automotive repair arena and developing and expanding its professional customer base, not only in automotive repair, but also in adjacent markets, additional geographies and other areas, including in critical industries, where the cost and penalties for failure can be high. In pursuit of these initiatives, Snap-on now anticipates that capital expenditures in 2016 will approximate $80 million, of which $56.6 million was incurred through the end of the third quarter. Snap-on presently expects that its full year 2016 effective income tax rate will be slightly below its full year 2015 rate.

The stock has been up as much as 9.1% today.

-

Morning News: October 20, 2016

Eddy Elfenbein, October 20th, 2016 at 7:16 amChina PPI To Stay Positive In Coming Months: Statistics Bureau

EU Court Adviser Backs Intel Appeal Over $1.17 Billion Fine

World Wine Production Slips Amid Rough Weather; Italy On Top

One of the Fed’s Most Influential Officials Expects a Fed Rate Hike This Year

How Silicon Valley Treats a Trump Backer: Peter Thiel

Catwalks and Katy Perry: Alibaba Starts Countdown to Singles’ Day

Vanguard Sways Financial Advisers to Bring $1 Trillion on Board

Nestle Is the Latest Food Manufacturer to Be Hit By a Global Slowdown

Glencore Sells Coal Rail Unit for $873 Million to Cut Debt

Roche Sales Lifted by Cancer Drugs

Nissan-Renault CEO Ghosn to Chair Troubled Mitsubishi Motors

Dunkin’ Brands Revenue Misses On Fewer Restaurant Openings

Tesla Will Make Its Cars Fully Self-Driving, But Not Turn the System On Yet

Josh Brown: RIAs Smile More Than Brokers

Jeff Miller: What is Your Confirmation Bias Quotient?

Be sure to follow me on Twitter.

-

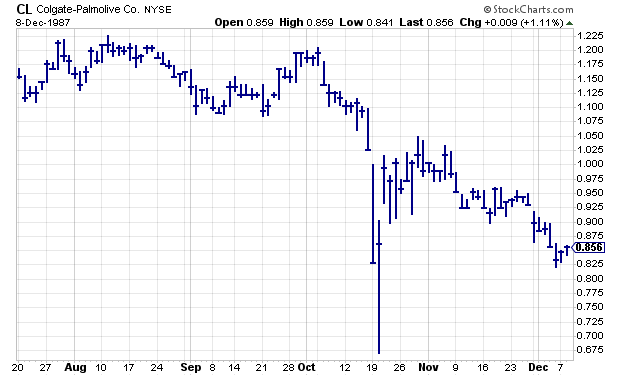

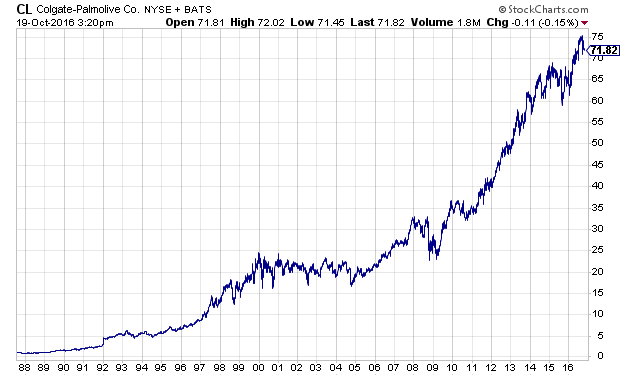

Focus on the Long-Term

Eddy Elfenbein, October 19th, 2016 at 3:21 pmI’m sure glad I didn’t own Colgate-Palmolive 29 years ago!

Wait. Maybe I’m not glad.

-

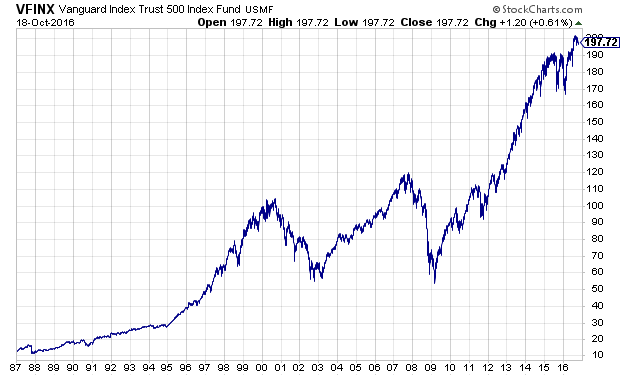

The Market Crash 29 Years On

Eddy Elfenbein, October 19th, 2016 at 9:39 am"I'm predicting another 1987-style market!!!"

"So you mean the market will rise 14-fold in the next 29 years?"— Eddy Elfenbein (@EddyElfenbein) October 12, 2016

I tweeted that out the other day. I was guessing at the 14-fold, but I was pretty close. I don’t have the daily return data for the S&P 500 going back that far, so I’m going to use the Vanguard S&P 500 Index Fund (VFINX) as a proxy (chart below).

If you had been unlucky enough to buy at the exact market peak in 1987, you’d be up 11.5 fold now. That’s an annualized gain of 8.8%.

In retrospect, the greatest one-day crash in Wall Street history looks to be a mere speck.

-

Morning News: October 19, 2016

Eddy Elfenbein, October 19th, 2016 at 7:07 amPositive China Data Leaves Uneven Impact on Asian Markets

Saudi Arabia Says Many Nations Will Join OPEC Output Cuts

Social Security Taxes to Rise for Higher-Income Americans

Yahoo Looks to Bright Side After Breach

Starbucks Names Its First China CEO

Family Behind Korean Conglomerate Lotte is Indicted in Corruption Case

BHP Just Gave Its Most Positive Assessment in 5 Years

Wells Fargo Faces Angry Questions About Profiling Latinos

Yahoo Says Traffic Rose Despite Hacking That Could Alter Verizon Deal

Morgan Stanley Profit Jumps 61.7% on Trading Comeback

Netflix Is Taking Over Hollywood, and Hollywood Isn’t Thrilled

New Rules Would Require Airlines To Refund Baggage Fees For Delayed Luggage

This Tool Tells You if You’re Making What You’re Worth

Jeff Carter: The Backbone of Finance is Going To Change

Roger Nusbaum: Hang In There, The Election Will Be Over Soon

Be sure to follow me on Twitter.

-

Consumers Are Rebounding

Eddy Elfenbein, October 18th, 2016 at 12:45 pmIn US News and World Report, Simon Constable lists five reasons to bet on a consumer rebound: tepid spending (so far), improving consumer confidence, improving consumer confidence, warmer housing market and the wealth effect.

Warmer housing market. The other thing associated with rising consumer spending is home prices, says Eddy Elfenbein, author of the Crossing Wall Street blog.

That too has been doing well. The S&P CoreLogic Case-Shiller 20-City Composite Home Price index has been steadily rising since March 2012. It measures prices changes for residential real estate across major U.S. cities.

I’d also add the decent retail sales report from last week.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His