Archive for April, 2017

-

Morning News: April 24, 2017

Eddy Elfenbein, April 24th, 2017 at 7:13 amFrance Delivers Euro’s Latest Existential Question

German Business Confidence Climbs to Highest Since July 2011

Trump’s America to Win as China Stumbles, Steel Veteran Says

U.S. Chamber of Commerce Chief Expects Basic NAFTA Deal By Mid-2018

Becton to Buy C.R. Bard in $24 Billion Medical Supply Deal

Syngenta Defends GMO Corn as Merger Shifts Blame to China’s Door

LafargeHolcim CEO’s Resignation on Syria Creates Power Vacuum

No Longer A Dream: Silicon Valley Takes On The Flying Car

The Electric Car Revolution Now Faces Its Biggest Test

Tesla’s Big Model 3 Bet Rides on Risky Assembly Line Strategy

JAB Puts Jimmy Choo, Bally Up for Sale to Focus on Coffee

Malaysia to Pay $1.2 Billion to Abu Dhabi Fund Over 1MDB Scandal

Josh Brown: Cheap. Capital. Is. Awesome.

Jeff Miller: Time To Rebuild the Wall of Worry?

Be sure to follow me on Twitter.

-

CR Bard’s Earnings Report

Eddy Elfenbein, April 23rd, 2017 at 6:39 pmNot that it matters much now, but CR Bard (BCR) just released their Q1 earnings report which was scheduled for later this week.

Bard had previously said they expected Q1 EPS between $2.60 and $2.66, and full-year EPS between $11.45 and $11.75. It turns out for Q1, they made $2.87 per share. They now expect full-year EPS between $11.65 and $11.90. For Q2, they’re expecting $2.75 to $2.85 per share. Wall Street had been expecting $2.87.

I’ve lifted our Buy Below on BCR to $330 per share.

First quarter 2017 net sales were $938.8 million, an increase of 7 percent on an as-reported basis over the prior-year period. Excluding the impact of foreign exchange, first quarter 2017 net sales increased 8 percent over the prior-year period. Divested products and acquisitions in the last twelve months favorably impacted net sales growth by approximately 70 basis points.

For the first quarter 2017, net sales in the U.S. were $657.2 million and net sales outside the U.S. were $281.6 million, an increase of 5 percent and 14 percent, respectively, over the prior-year period. Excluding the impact of foreign exchange, first quarter 2017 net sales outside the U.S. increased 17 percent over the prior-year period.

For the first quarter 2017, net income was $178.1 million and diluted earnings per share were $2.37, an increase of 53 percent and 54 percent, respectively, as compared to first quarter 2016 results. Adjusting for amortization of intangibles and certain items that affect comparability between periods as detailed in the tables below, first quarter 2017 net income was $215.4 million and diluted earnings per share were $2.87, an increase of 22 percent and 23 percent, respectively, as compared to first quarter 2016 results.

In conjunction with the first quarter results, the company is also updating financial guidance for the full year and providing financial guidance for the second quarter of 2017. For the full year 2017, net sales are now forecasted to increase between 5 percent and 6 percent on an as-reported basis. Excluding the impact of foreign exchange, full year 2017 net sales are forecasted to increase between 6 percent and 7 percent over 2016. Full year 2017 diluted earnings per share, after adjusting for amortization of intangibles and certain items that affect comparability between periods, are projected to be between $11.65 and $11.90, representing growth between 13 percent and 16 percent compared to full year 2016 results.

For the second quarter 2017, net sales are forecasted to increase between 4 percent and 5 percent on an as-reported basis. Excluding the impact of foreign exchange, second quarter 2017 net sales are forecasted to increase between 6 percent and 7 percent over second quarter 2016. Second quarter 2017 diluted earnings per share, after adjusting for amortization of intangibles and certain items that affect comparability between periods, are projected to be between $2.75 and $2.85, representing growth between 8 percent and 12 percent compared to second quarter 2016 results.

-

The BCR/BDX Press Release

Eddy Elfenbein, April 23rd, 2017 at 6:32 pmHere’s the press release:

FRANKLIN LAKES, N.J. and MURRAY HILL, N.J., April 23, 2017 /PRNewswire/ — BD (Becton, Dickinson and Company) (NYSE: BDX), a leading global medical technology company, and C. R. Bard, Inc. (NYSE: BCR), a medical technology leader in the fields of vascular, urology, oncology and surgical specialty products, announced today a definitive agreement under which BD will acquire Bard for $317.00 per Bard common share in cash and stock, for a total consideration of $24 billion. The agreement has been unanimously approved by the Boards of Directors of both companies.

The combination will create a highly differentiated medical technology company uniquely positioned to improve both the process of care and the treatment of disease for patients and healthcare providers. The transaction will build on BD’s leadership position in medication management and infection prevention with an expanded offering of solutions across the care continuum. Additionally, Bard’s strong product portfolio and innovation pipeline will increase BD’s opportunities in fast-growing clinical areas, and the combination will enhance growth opportunities for the combined company in non-U.S. markets.

This financially compelling transaction will be immediately accretive and is expected to generate high-single digit accretion to adjusted earnings per share (EPS) in fiscal year 2019. Approximately $300 million of estimated annual, pre-tax, run-rate cost synergies are expected by fiscal year 2020. Separately, BD also expects to benefit from revenue synergies beginning in fiscal year 2019. The transaction is expected to improve BD’s gross margins by approximately 300 basis points in fiscal year 2018, increase BD’s earnings per share growth trajectory to the mid-teens, and generate strong cash flow.

Vince Forlenza, BD’s chairman and chief executive officer, said, “Combining with Bard will accelerate our ability to offer more comprehensive, clinically relevant solutions to customers and patients around the globe, creating a strong partner for healthcare providers who are increasingly focused on delivering better outcomes at a lower total cost. Our two purpose-driven organizations are well-aligned strategically, sharing a strong track record of performance and a deep commitment to addressing unmet needs in today’s challenging healthcare environment. We expect the transaction to contribute meaningfully to BD’s plans for revenue growth and margin expansion, and generate outstanding value both near- and long-term for shareholders. I am excited to welcome Bard’s talented employees to our strong and dedicated team as we bring together two companies with such complementary capabilities, values and strong reputations for delivering superior results.”

Tim Ring, Bard’s chairman and chief executive officer, said, “We are confident that this combination will deliver meaningful benefits for customers and patients as we see opportunities to leverage BD’s leadership, especially in medication management and infection prevention. We also believe that we can expand our access to customers and patients through BD’s strategic selling capabilities, and that our fast-growing portfolio in emerging markets can significantly benefit from their well-established international commercial infrastructure. Our two companies share the conviction that a product leadership strategy focused on unmet needs and improved outcomes that provide economic value to the global healthcare system will provide long-term shareholder returns.”

John Weiland, Bard’s vice-chairman, president and chief operating officer, added, “BD and Bard share a common purpose with highly compatible organizations. We are very proud of the business and culture we have built over 110 years, focused on quality, integrity, innovation and service. We have long had great respect for BD and find in them a similarly strong, results-oriented culture that prioritizes execution and long-term value creation. In addition to significant benefits for our customers, patients, and shareholders, we believe this combination will provide our employees with new and exciting opportunities as part of a highly competent, dynamic global organization. We look forward to this next chapter in our company’s great history.”

Strategic Highlights

Will create new opportunities to build on BD’s leadership position in medication management and infection prevention with an expanded offering of solutions across the care continuum.

Will bring together highly complementary product sets to create unmatched solutions for customers, enhancing growth opportunities for the combined company.

By combining Bard’s strong leadership position and innovation pipeline in fast-growing vascular access segments – PICCs (peripherally inserted central catheters), midlines and drug delivery ports – with BD’s leadership and innovation in IV drug preparation, dispensing, delivery and administration, the new company will be better positioned to provide end-to-end medication management solutions across the care continuum.

Will further expand BD’s leadership in infection prevention, with offerings positioned to address 75 percent of the most costly and frequent healthcare associated infections (HAIs). Through the combined solutions set, the new company will have a more comprehensive, clinically relevant offering to address Surgical Site Infections (SSIs) and Catheter-Related Blood Stream Infections (CRBSIs).

Bard’s strong product portfolio and innovation pipeline will increase BD’s opportunities in fast growing clinical areas, including peripheral vascular therapy, oncology and bio-surgery.Bard’s clinically differentiated offerings create more meaningful scale and relevance for BD in high-growth categories of oncology and surgery.

Bard will expand BD’s focus on the treatment of disease states beyond diabetes to include peripheral vascular disease, urology, hernia and cancer.

BD’s leading global capabilities and infrastructure will further accelerate the combined company’s growth outside of the U.S., creating more opportunities for patients and clinicians around the world to benefit from BD’s and Bard’s product technology.Together, BD and Bard will bring to market an expanded portfolio of clinically relevant products, with opportunities to drive near-term revenue synergies outside of the U.S.

Bard, which registered approximately 500 products internationally in 2016, has made significant progress expanding outside of the U.S. in recent years, particularly in emerging markets, where Bard is among the fastest growing medical technology companies.

Bard’s strong presence in vascular access and surgery will also help drive sales of the highly complementary CareFusion portfolio outside of the U.S.

The combined company will have a large and growing presence in emerging markets, including $1 billion in annual revenue in China.

Transaction HighlightsUnder the terms of the transaction, Bard common shareholders will be entitled to receive approximately $222.93 in cash and 0.5077 shares of BD stock per Bard share, or a total of value of $317.00 per Bard common share based on BD’s closing price on April 21, 2017. At closing, Bard shareholders will own approximately 15 percent of the combined company.

BD expects to contribute approximately $1.7 billion of available cash to fund the transaction, along with, subject to market conditions, approximately $10 billion of new debt and approximately $4.5 billion of equity and equity linked securities issued to the market. Bard shareholders will also receive $8 billion of BD common stock. BD has also obtained fully committed bridge financing. At closing, BD estimates the combined company will have pro forma leverage of approximately 4.7x and is committed to deleveraging to below 3.0x leverage within three years of closing. BD expects to continue the suspension of its share repurchase program. BD is also committed to annual dividend increases while reinvesting in the business to continue to drive long-term growth.

The transaction is subject to regulatory and Bard shareholder approvals and customary closing conditions, and is expected to close in the fall of 2017.

Integration Plans

BD has a successful integration track record, as demonstrated by its 2015 acquisition and integration of CareFusion. BD has put in place a plan to ensure a seamless integration with Bard. A designated integration team, comprised of senior members of both organizations, will be led by Bill Tozzi, a seasoned BD executive who most recently served as worldwide president of the Medication and Procedural Solutions business and earlier was corporate controller for BD. At the closing of the transaction, Tim Ring, chairman and chief executive of Bard, and an additional Bard director, are expected to join the BD Board of Directors, which will be expanded by two directors. BD is confident in its ability to achieve synergies as it brings together two world class companies and expects to offer opportunities for talented employees to become part of an even more dynamic global leader.

BD Organizational Update

BD expects to create a third segment within the company – BD Interventional — where the Bard businesses will report both operationally and financially. BD is separately announcing today the appointment of Tom Polen, 43, currently executive vice president and president of the BD Medical Segment, as president of BD, effective immediately. In his new role, Mr. Polen will oversee BD’s Medical and Life Sciences segments, as well as the new Interventional segment.

Transaction Conference Call and Webcast Information

BD and Bard will conduct a live conference call and webcast on April 24, 2017 at 8:00 a.m. (ET). The webcast of the conference call, along with related slides, will be accessible through BD’s and Bard’s websites. The conference call will also be available for replay through BD’s and Bard’s websites, or at (800) 585-8367 (domestic) and (404) 537-3406 (international) through the close of business on May 1, 2017, confirmation number 13011331.

BD Earnings Update

BD’s earnings conference call, previously scheduled for Thursday, May 4, 2017, has been rescheduled for Tuesday, May 2, 2017, at 8:00 a.m. (ET). BD will issue a press release detailing the quarter’s earnings earlier that morning. The webcast of the conference call, along with related slides, will be accessible through BD’s website at www.BD.com/investors and will be available for replay through Thursday, May 9, 2017.

Bard Earnings Update

Bard separately today announced first quarter 2017 financial results, which are available on Bard’s corporate website, and is canceling the previously scheduled earnings conference call on April 26, 2017.

Advisors

Perella Weinberg Partners LP is acting as lead financial advisor to BD. Citi is also serving as a financial advisor to BD and will be providing fully committed financing. Skadden, Arps, Slate, Meagher & Flom LLP provided legal counsel to BD. Goldman, Sachs & Co. served as financial advisor to Bard. Wachtell, Lipton, Rosen & Katz served as legal advisor to Bard.

-

CWS Market Review – April 23, 2017

Eddy Elfenbein, April 23rd, 2017 at 6:09 pmGreat news broke on Sunday. Becton, Dickinson (BDX) said they’re buying CR Bard (BCR) for $24 billion, or $317 per share. That’s a 25.3% premium to Friday’s closing price!

This is terrific news and it’s great seeing a long position get rewarded so handsomely.

Here’s how the deal work. BCR shareholders will get $222.93 per share in cash plus 0.5077 shares of BDX. That works out to $317 based on Friday’s close.

Here’s the press release.

Don’t worry. There’s nothing you have to do right now. The deal is expected to close this fall. I’ll have more details in upcoming issues of CWS Market Review. But first, I wanted to let you know about this news as soon as possible.

– Eddy

P.S. Hooray!!!!

-

CWS Market Review – April 21, 2017

Eddy Elfenbein, April 21st, 2017 at 7:08 am“The market owes you nothing. Take full responsibility for everything that happens and your results will improve.” – Dan Zanger

We’re now in the high tide of earnings season. So far, 82 companies in the S&P 500 have reported earnings. Of those, 75% have beaten Wall Street’s expectations. Bear in mind that expectations are expected to be beaten. If you don’t beat expectations…well, that’s simply not expected. In recent years, the expectations’ “beat rate” has averaged 71%.

Our earnings have been very strong so far. We had five Buy List earnings reports this week, and all five topped expectations. After its earnings report, Snap-on jumped more than 5.7%, but Alliance Data Systems was our big winner. After its report, ADS rallied 8.3%. (Yes, this is the same stock recently rated “underperform” by Oppenheimer.)

We have nine more Buy List earnings reports due next week. This week’s issue will be all about earnings. I’ll run down the five reports from this week, and I’ll preview the coming batch for next week. By the way, you can always check out our complete Earnings Calendar. Now, let’s get to this week’s reports!

Five Buy List Earnings This Week

On Wednesday, Signature Bank (SBNY) led off our earnings parade by reporting very strong Q1 earnings of $2.15 per share. That’s 10 cents more than estimates, and it compares with $1.97 per share for last year’s Q1. On a technical note, the Q1 figure doesn’t include a tax benefit of $14.4 million.

Digging into the details, Signature’s numbers were strong. Net interest income rose 8.4%. Total assets increased 15.4% to $40.27 billion. In the last year, total deposits are up 17.2%. The key figure for any bank is net interest margin. For Q1, that was 3.14% for Signature. The medallion loans are still a headache, but it’s a manageable problem.

Signature’s stock has been sliding back for the last few weeks. On Monday, shares of SBNY slipped below $136. After the earnings report, the stock gapped up, then shot back down. Traders finally decided (correctly) that it was a decent report, and SBNY closed Thursday at $139.95 per share. Don’t let the volatility scare you. This week, I’m dropping our Buy Below down to $152 per share.

Thursday morning was very busy for us with four earnings reports. Let’s start with Alliance Data Systems (ADS), which was the big star. ADS reported “core” EPS of $3.91 per share which beat estimates by five cents per share. Quarterly revenue rose 12.1% to $1.88 billion. That topped estimates by $70 million.

This was a very good quarter for ADS. They’re standing by their full-year EPS guidance of $18.50. CEO Ed Heffernan said, “Overall, our outlook for full-year 2017 results remains consistent, and all indications continue to support our belief that a significant acceleration (or what I refer to as a ‘slingshot’) will occur in our core EPS growth rate as we move into the back half of 2017, and throughout 2018.”

On Wednesday, the shares gained $19.99 to close at $260.63. That’s a gain of 8.71%. (Last week, you may recall, Oppenheimer initiated coverage on ADS with an “underperform” rating. Nice timing, there!) This week, I’m raising our Buy Below price on Alliance Data Systems to $266 per share.

Moving on to Danaher (DHR), the company reported Q1 earnings of 85 cents per share. That beat estimates by a penny. Previously, the company said they expected Q1 earnings to range between 82 and 85 cents per share. Quarterly revenues rose 7% to $4.2 billion, and core revenue grew by 2.5%.

Danaher said they expect Q2 earnings between 95 and 98 cents per share. Wall Street had been expecting 99 cents. The company reiterated their full-year guidance of $3.85 to $3.95 per share.

As I look at Danaher’s report, there’s literally not one figure that should surprise anyone. This is what I expected. CEO Thomas Joyce said, “We are off to a good start in 2017.” Still, the shares dropped 4.1% after the earnings report. Danaher remains a buy up to $90 per share.

Sherwin-Williams (SHW) also had a very strong quarter. The paint people earned $2.27 per share for Q1. That was well ahead of Wall Street’s estimates of $2.05 per share. Previously, the company told us to expect a range between $2.03 and $2.12 per share. Sherwin saw particular strength in their Paint Stores Group.

For Q2, Sherwin expects earnings to range between $4.40 and $4.60 per share (that doesn’t include an adjustment of 25 cents per share for acquisition costs). Wall Street had been expecting $4.43 per share. For the whole year, the company now expects $14.05 to $14.25 per share (40 cents for acquisition costs). Wall Street had been expecting $13.71 per share. Sherwin’s previous range was $13.60 to $13.80 per share. This is very good news.

SHW jumped 4% on Thursday. It’s now one of our three 20% winners on the year. This week, I’m lifting my Buy Below on Sherwin-Williams to $331 per share.

Last is Snap-on (SNA) which had a visit from President Trump earlier this week. The president spoke in front of an American flag made of Snap-on wrenches.

For Q1, Snap-on reported earnings of $2.39 per share. That was three cents better than estimates, and it compares with $2.16 per share one year ago. Quarterly revenue grew 6.3% to $887.1 million which beat estimates of $876.9 million.

The stock jumped 5.7% in Thursday’s trading. That’s a nice change from three months ago when SNA dropped sharply after its earnings report. Snap-on remains a solid buy up to $161 per share.

Nine Earnings Reports Coming Next Week

Next week will be a very busy one for us with nine Buy List earnings reports. Express Scripts (ESRX) leads off on Monday. The stock has gotten a lot of political attention recently as some people like to blame them for high drug prices. More specifically, drug companies like to blame them for high drug prices. Shares of ESRX recently dropped to a three-year low.

For Q1, Express said it expects earnings between $1.30 and $1.34 per share. Wall Street chose the middle and expects $1.32 per share. For the whole year, Express sees EPS ranging between $6.82 and $7.02 per share. Right now, Express is a good value.

On Tuesday, Stryker (SYK) and Wabtec (WAB) are scheduled to report. For Q1, Stryker expects earnings to range between $1.40 and $1.45 per share. For all of 2017, they see earnings between $6.35 and $6.45 per share. For Q1, Wall Street expects $1.43 per share. SYK came very close to a new all-time high this week.

Wabtec had a terrible Q4 earnings report. From February 15 to March 27, the stock dropped 15%. It’s come back a little since then. Wabtec expects full-year 2017 earnings to range between $3.95 and $4.15 per share. For Q1, Wall Street is looking for 82 cents per share. Don’t bail on WAB just yet!

On Wednesday, Axalta Coating Systems (AXTA), CR Bard (BCR) and Fiserv (FISV) are up. Axalta has been a strong performer for us this year. They just bought Valspar’s Industrial Wood Coatings unit for $420 million. Wall Street is looking for earnings of 24 cents per share. They should beat that.

CR Bard continues to be a home run stock for us. We added BCR to our Buy List in 2012 at $85.50. The stock closed Thursday at $254.77 per share. (Quick lesson for investors: Many of our biggest home runs didn’t become massive winners until three or four years in.) For Q1, Bard expects EPS between $2.60 and $2.66, and between $11.45 and $11.75 for the whole year.

Fiserv is one of those companies like Danaher. I’m not terribly concerned with their quarterly earnings. They may beat or miss by a penny or two, but the larger trend is more important. Fiserv is a very solid company. Wall Street is looking for earnings of $1.19 per share.

Then on Thursday, it’s time for AFLAC (AFL), Cerner (CERN) and Microsoft (MSFT). Shares of AFLAC have come to life recently. On Thursday, the duck stock came within a penny per share of its all-time high. AFLAC has said that if the yen stays at ¥108.70 to the dollar, then they expect to make between $6.40 and $6.65 per share this year. For Q1, Wall Street expects $1.62 per share.

Cerner is our best-performing stock this year. Last year, it was one of our worst. The company said they expect Q1 earnings between 57 and 59 cents per share. Frankly, that’s lower than I hoped for. Wall Street is also subdued on Cerner. The consensus is for 57 cents per share. For the year, Cerner expects earnings between $2.44 and $2.56 per share. I’m a little cautious on Cerner right now.

Microsoft has been making so many good moves lately. The earnings have been very strong for the last few quarters and I’m expecting more of the same. Wall Street expects quarterly earnings of 70 cents per share.

HEICO Splits 5-for-4

This week, shares of HEICO (HEI) split 5-for-4. This means that shareholders now have 25% more shares. Our Buy Below price dropped from $90 to $72 per share.

For track record purposes, I assume the Buy List starts the year as a $1 million portfolio that’s equally divided among the 25 stocks. For HEICO, that meant a position of 518.4705 shares at a starting price of $77.15 per share. With the split, that becomes 648.0881 shares starting at $61.72 per share. HEICO won’t report earnings for another month.

That’s all for now. Next week will be jam-packed with earnings reports. The big economic news next week will come on Friday when the government releases its first estimate for Q1 GDP. It probably won’t be good. The Atlanta Fed’s GDPNow currently predicts Q1 growth of 0.5%. That may put off any rate hike plans for the Federal Reserve. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: April 21, 2017

Eddy Elfenbein, April 21st, 2017 at 6:33 amU.S. and Indonesia Seek to Cut Trade and Investment Barriers

Trump Targets Steel Trade, But China Will Be Tough To Contain

Trump to Sign Actions on Taxes, Wall Street Regulation

FCC Clears Way For Big TV Mergers, Eases Broadband Price Limits

Elon Musk Outlines His Mission to Link Human Brains With Computers in 4 Years

Why Verizon Is Putting Actual Employees in Its New TV Ads

Visa’s Profit Boosted By Europe Unit, Big Card Portfolio Wins

Virtual Reality Companies Navigate ‘The Trough of Disillusionment’

High-Stakes Vote on Wells Fargo Board Also Tests Proxy Adviser ISS

A New Era After Bill O’Reilly? Women Aren’t Convinced

Desperate Malls Turn to Concerts and Food Trucks

Subprime Mortgage Giant Ocwen Rocked by U.S. Suit Claiming Abuse

Ben Carlson: Urgent vs. Important & the Power of Small Wins

Michael Batnick: The Other Side

Be sure to follow me on Twitter.

-

Update on Our Earnings Stocks

Eddy Elfenbein, April 20th, 2017 at 12:37 pmAlliance Data Systems (ADS) +7.71%

Snap-on (SNA) +5.55%

Sherwin-Williams (SHW) +3.72%

Danaher (DHR) -2.90%as of 12:37

-

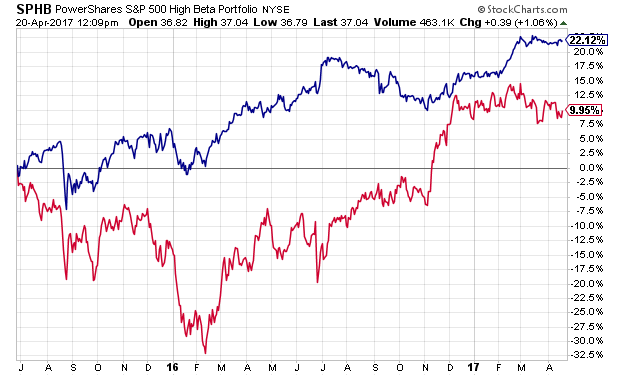

There’s Never Just One Stock Market

Eddy Elfenbein, April 20th, 2017 at 12:18 pmCheck out Josh Brown’s post from earlier today on the stealth bear market that hit Wall Street in 2015-16. He quotes Andrew Adams as saying that if you had invested in the 10 largest stocks in 2015, you would have been up 20% on the year, yet the other 490 stocks were down 3%.

The point is that we often talk about the S&P 500 as if it’s one giant stock. In reality, there are many currents and cross-currents running just below the surface. The index only tells us an average, and it’s a size-weighted average at that.

One good way to divide the market is by looking at high beta stocks compared with low vol stocks. Look at this chart from the last 20 months:

I’ll tell you that Low Vol is the blue line, which seems obvious since it’s so much less volatile. The red line is High Beta. Back to Josh’s point, we already had a nasty bear market. Sure, not everybody experienced it, but for those who did, it was rather unpleasant.

The Trump Rally was all about the red line, but the blue line started to perk up in February.

-

Four Buy List Earnings Reports this Morning

Eddy Elfenbein, April 20th, 2017 at 9:24 amThis was a busy morning for Buy List earnings reports. We had four before the opening bell. Let me go through each one.

Let’s start with Alliance Data Systems (ADS). The company reported “core” EPS of $3.91 per share which beat estimates by five cents per share. Quarterly revenue rose 12.1% to 1.88 billion. That topped estimates by $70 million.

This was a good quarter for ADS. They’re standing by their full-year EPS guidance of $18.50. The CEO said he expects significant acceleration in the back half of the year.

Moving on to Danaher (DHR). The company reported Q1 earnings of 85 cents per share. That beat estimates by a penny. Previously, the company said they expected Q1 earnings to range between 82 and 85 cents per share.

Danaher said they expect Q2 earnings between 95 and 98 cents per share. Wall Street had been expecting 99 cents. The company also reiterated their full-year guidance of $3.85 to $3.95 per share.

Sherwin-Williams (SHW) had a very strong quarter. The company earned $2.53 per share, but that included 34 cents from lower income, and an eight-cent charge for acquisition costs. That works out to $2.27 per share. The company had told us to expect a range between $2.03 and $2.12 per share, while Wall Street had been expecting $2.05 per share.

For Q2, Sherwin expects earnings to range between $4.40 and $4.60 per share (not including 25 cents per share in acquisition costs). Wall Street had been expecting $4.43 per share. For the whole year, the company now expects $14.05 to $14.25 per share (40 cents for acquisition costs). Wall Street had been expecting $13.71 per share. Sherwin’s previous range was $13.60 to $13.80 per share.

Last is Snap-on (SNA), which had a visit from President Trump earlier this week. The company earned $2.39 per share for Q1. That’s three cents better than estimates. Snap-on had quarterly revenues of $887.1 million which beat estimates of $876.9 million.

-

Morning News: April 20, 2017

Eddy Elfenbein, April 20th, 2017 at 6:55 amReconciling the IMF’s 3 Growth Messages

Japanese Exports Surge to End First Quarter on Strong Note

Brent Oil Rebounds as Saudis Signal Potential OPEC Cut Extension

General Motors Says Venezuela Illegally Seizes Auto Plant

Exxon Seeks U.S. Waiver to Resume Russia Oil Venture

ConocoPhillips Takes Slow, Steady Route in Race For Oil Profits

Bill O’Reilly Is Forced Out at Fox News

Morgan Stanley Bond Traders Top Goldman for First Time Since 2011

Wells Fargo’s Regulator Admits It Missed Red Flags

Why The Best Is Yet To Come For Netflix

Qualcomm’s Chip Expansion Helps Deflect Lawsuit Concerns

Why IBM Stock Is Likely to Keep Singing the Blues

Theranos Investors Say They Were Pressured to Abandon Lawsuit

Jeff Carter: Change Is Not Easy

Josh Brown: ESG Links: Allocating With Purpose

Be sure to follow me on Twitter.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His