CWS Market Review – June 16, 2017

“If you’ve followed my forecasts, you’ve probably lost a lot of money.”

– St. Louis Fed President James Bullard

Well…it happened. As expected, the Federal Reserve raised interest rates again this week. I don’t like it, but we can’t always choose the ideal environment to invest in. If you wait for things to be perfect, then you’d never be in the market.

This was an important meeting for the Fed because they also explained what they intend to do with their enormous balance sheet. This has been a big concern on Wall Street. I’ll explain what it all means. Additionally, the central bankers updated their economic projections. I should explain that the Fed has a pretty dismal track record of predicting where things will go, but it’s still useful to look at their outlook for the economy.

Fortunately, the stock market continues to hold up well. The S&P 500 closed at another all-time high on Tuesday. However, there’s been a significant weak link in the market recently, and that’s big-cap tech stocks. Don’t feel too bad for these guys. They’ve been running up the score lately, so I can’t say it’s not wholly surprising to see them face a little pain. Outside of Microsoft, this recent trend hasn’t had a big impact on our Buy List. In fact, our Buy List has been doing quite well of late. Before I get to all that, let’s look at what the Fed did this week.

The Federal Reserve Raises Interest Rates

On Wednesday afternoon, the Federal Reserve released its latest policy statement. The central bank said they raised their range for the Fed funds rate to between 1% and 1.25%. That’s an increase of 0.25%. This was the second rate hike this year, and the fourth of this cycle.

As I’ve said before, I think this move is a mistake, and I won’t belabor the arguments against the increase. It happened, and we have to move on. I’ll note that there was one dissenting voice, Neel Kashkari of the Minneapolis Fed, who agrees with me.

On Wednesday morning, just hours before the Fed’s statement, the government released the inflation report for May. The report again showed that there’s absolutely no threat of inflation on the horizon. If anything, the rate of inflation has fallen off sharply over the last three months. It’s hard to justify rate increases to fight off an inflation threat that doesn’t exist.

During May, the headline rate of inflation fell by 0.1%. Economists had been expecting no change. Some of that was due to falling prices for gasoline. That’s why we also want to look at the “core rate,” which excludes volatile food and energy prices. But the core rate for May only rose by 0.1%. There’s simply not much inflation out there.

You may recall that March was the weakest month for core inflation in over 30 years. As with all stats, we don’t want to be fooled by one-point trends. There are always outliers, so we want to see more evidence. Indeed, that evidence came in the last two months. Core inflation for April and May were the second- and third-weakest of the last three years, trailing only March. So it’s not only that inflation is low: it’s actually going lower.

More troubling is that we’ve seen a swift reaction in the bond market. On Tuesday, the yield on the 10-year Treasury dropped to 2.1%. That’s the lowest point all year. After the election last year, Treasury yields soared on economic optimism, but that’s largely faded in recent weeks. The spread between the two-year and ten-year Treasuries is now less than 80 basis points.

In the Fed’s policy, they acknowledge the recent weakness in the economy, but they seem to feel that it will soon pass. I hope they’re right, but I just don’t see the evidence just yet. In fact, this week’s retail-sales report was another dud. Economists had been expecting a gain of 0.1%. Instead, retail sales fell 0.3% in May. This was the biggest drop in 16 months.

But the Fed thinks they’ve only started raising rates. According to the latest Fed projections, they expect to raise rates one more time this year. After that, the outlook becomes a lot less clear (the blue dots get much more dispersed). The Fed sees three more hikes in 2018, and possibly three more in 2019. That means it’s possible that the 2/10 spread could be negative as early as next year. Still, I don’t want to be too alarmist. By the Fed’s own projections, they see real interest rates staying negative for another 18 months. My point is that we’re not in the danger zone just yet, but we can see it on the horizon.

The Fed also unveiled its plans for what they intend to do with their $4.2 trillion balance sheet, or as the Fed calls it, their “normalization plans.” The Fed said they plan to stop reinvesting the proceeds of their bonds in gradually increasing increments. It will be a long, long time before the balance sheet gets back to normal. But the key point is that the Fed intends to raise rates at the same time they address their balance sheet. That point wasn’t always so clear.

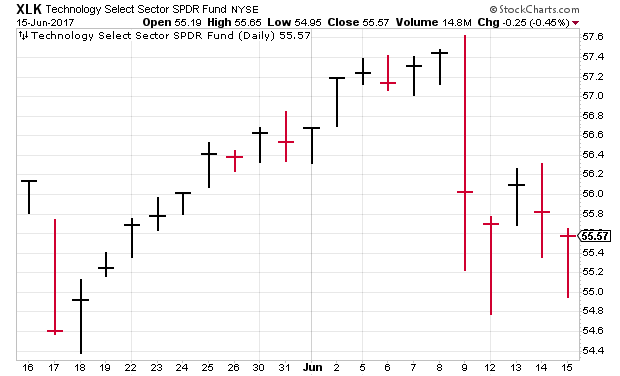

The Great Tech Stock “Crash” of 2017

What’s happening with tech stocks? The tech sector has fallen four times in the last five sessions, and some of those drops have been pretty sharp. The stock market had been so placid for so long that a fairly minor bump in the road for large-cap tech stocks has rattled a lot of investors.

Let’s add some context here: tech stocks had been leading an already powerful rally. In fact, the rally hasn’t even affected the whole sector. A huge part of the gains have fallen on just five major stocks; Facebook, Apple, Amazon, Microsoft and Google. That’s right: the latest acronym hitting Wall Street is FAAMG.

At one point, Facebook, Amazon and Apple were all up over 30% for the year. That was more than three times the rest of the market. Not anymore! In the last week, the Tech Sector ETF (XLK) has dropped from $57.44 to $55.57.

I want to stress that the damage we’re seeing in tech is hardly unprecedented. What’s been unusual is the exceedingly low volatility visible until now. It’s the change from very, very low volatility to normal behavior that’s jarred Wall Street. Frankly, the current losses are very normal.

Our Buy List has largely side-stepped the FAAMG phenomenon, with the exception of Microsoft (MSFT). Shares of MSFT just pulled back below our $70 Buy Below price. Again, that’s following an impressive run-up. Of all the FAAMG stocks, Microsoft is the one I’m least worried about. The last few earnings reports have been quite good. Also, I’m expecting another dividend hike in September. For now, I’m not worried about Microsoft, but I think we’ll see more losses in the tech sector for a few more weeks. Now let’s look at some of our Buy List stocks.

Buy List Updates

There hasn’t been a lot of news impacting our Buy List stocks this week. The good news is that our performance versus the rest of the market continues to be strong.

This week, I want to make a few adjustments to some of our Buy Below prices. As always, please bear in mind that these are not price targets. Instead, they’re guidance for current entry into a stock.

First up is AFLAC (AFL). I’m lifting my Buy Below on the duck stock to $80 per share. AFL has gapped up recently. Paul Amos, the current president and CEO’s son, said he’ll be leaving the company. That probably takes him out of the running to be the next CEO.

I’m also raising our Buy Below on Fiserv (FISV) to $131 per share. This stock is as strong and steady as it’s ever been. I’m looking forward to another good earnings report next month.

I’m dropping my Buy Below on Ross Stores (ROST) to $66 per share. I still like Ross a lot, but the stock has been caught up in a poor environment for retail. I’m not worried about Ross. This will be a real bargain if you can get Ross below $60 per share.

Finally, I’m lowering my Buy Below on Snap-on (SNA) to $168 per share. This is another good stock caught in a downtrend.

That’s all for now. There’s not much in the way of economic news next week. On Wednesday, we’ll get the existing-home sales report for May. Then on Friday will be the new-home sales report. For now, the housing sector is a bright spot in the economy, while consumer spending looks tired. We’ll see how long this can last. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on June 16th, 2017 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His