Archive for May, 2019

-

Highlights from Today’s Fed Minutes

Eddy Elfenbein, May 22nd, 2019 at 2:15 pmThe Fed just released the minutes of their last FOMC meeting. It appears the central bank is in no hurry to raise or lower interest rates.

Here’s the part of the discussion dealing with the Fed’s outlook for the economy:

Staff Economic Outlook

The projection for U.S. economic activity prepared by the staff for the April–May FOMC meeting was revised up on net. Real GDP growth was forecast to slow in the near term from its solid first-quarter pace, as sizable contributions from inventory investment and net exports were not expected to persist. The projection for real GDP growth over the medium term was revised up, primarily reflecting a lower assumed path for interest rates, a slightly higher trajectory for equity prices, and somewhat less appreciation of the broad real dollar. The staff’s lower path for interest rates reflected a methodological change in how the staff sets its assumptions about the future path for the federal funds rate in its forecast. Real GDP was forecast to expand at a rate above the staff’s estimate of potential output growth in 2019 and 2020 and then slow to a pace below potential output growth in 2021. The unemployment rate was projected to decline a little further below the staff’s estimate of its longer-run natural rate and to bottom out in late 2020. With labor market conditions still judged to be tight, the staff continued to assume that projected employment gains would manifest in smaller-than-usual downward pressure on the unemployment rate and in larger-than-usual upward pressure on the labor force participation rate.

The staff’s forecast for inflation was revised down slightly, reflecting some recent softer-than-expected readings on consumer price inflation that were not expected to persist along with the staff’s assessment that the level to which inflation would tend to move in the absence of resource slack or supply shocks was a bit lower in the medium term than previously assumed. As a result, core PCE price inflation was expected to move up in the near term but nevertheless to run just below 2 percent over the medium term. Total PCE price inflation was forecast to run a bit below core inflation in 2020 and 2021, reflecting projected declines in energy prices.

The staff viewed the uncertainty around its projections for real GDP growth, the unemployment rate, and inflation as generally similar to the average of the past 20 years. The staff also saw the risks to the forecasts for real GDP growth and the unemployment rate as roughly balanced. On the upside, household spending and business investment could expand faster than the staff projected, supported by the tax cuts enacted at the end of 2017, still strong overall labor market conditions, favorable financial conditions, and upbeat consumer sentiment. On the downside, the softening in some economic indicators since late last year could be the leading edge of a significant slowing in the pace of economic growth. Moreover, trade policies and foreign economic developments could move in directions that have significant negative effects on U.S. economic growth. Risks to the inflation projection also were seen as balanced. The upside risk that inflation could increase more than expected in an economy that was still projected to be operating notably above potential for an extended period was counterbalanced by the downside risks that recent soft data on consumer prices could persist and that longer-term inflation expectations may be lower than was assumed in the staff forecast, as well as the possibility that the dollar could appreciate if foreign economic conditions deteriorated.

Participants’ Views on Current Conditions and the Economic Outlook

Participants agreed that labor markets had remained strong over the intermeeting period and that economic activity had risen at a solid rate. Job gains had been solid, on average, in recent months, and the unemployment rate had stayed low. Participants also observed that growth in household spending and business fixed investment had slowed in the first quarter. Overall inflation and inflation for items other than food and energy, both measured on a 12-month basis, had declined and were running below 2 percent. On balance, market-based measures of inflation compensation had remained low in recent months, and survey-based measures of longer-term inflation expectations were little changed.

Participants continued to view sustained expansion of economic activity, with strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective as the most likely outcomes. Participants noted the unexpected strength in first-quarter GDP growth, but some observed that the composition of growth, with large contributions from inventories and net exports and more modest contributions from consumption and investment, suggested that GDP growth in the near term would likely moderate from its strong pace of last year. For this year as a whole, a number of participants mentioned that they had marked up their projections for real GDP growth, reflecting, in part, the strong first-quarter reading. Participants cited continuing strength in labor market conditions, improvements in consumer confidence and in financial conditions, or diminished downside risks both domestically and abroad, as factors likely to support solid growth over the remainder of the year. Some participants observed that, in part because of the waning impetus from fiscal policy and past removal of monetary policy accommodation, they expected real GDP growth to slow over the medium term, moving back toward their estimates of trend output growth.

In their discussion of the household sector, participants discussed recent indicators, including retail sales and light motor vehicle sales for March, which rose from relatively weak readings in some previous months. Taken together, these developments suggested that the first-quarter softness in household spending was likely to prove temporary. With the strong jobs market, rising incomes, and upbeat consumer sentiment, growth in PCE in coming months was expected to be solid. Several participants also noted that while the housing sector had been a drag on GDP growth for some time, recent data pointed to some signs of stabilization. With mortgage rates at their lowest levels in more than a year, a few participants thought that residential construction could begin to make positive contributions to GDP growth in the near term; a few others were less optimistic.

Participants noted that growth of business fixed investment had moderated in the first quarter relative to the average pace recorded last year and discussed whether this more moderate growth was likely to persist. A number of participants expressed optimism that there would be continued growth in capital expenditures this year, albeit probably at a slower pace than in 2018. Several participants observed that financial conditions and business sentiment had continued to improve, consistent with reports from business contacts in a number of Districts; however, a few others reported less buoyant business sentiment Many participants suggested that their own concerns from earlier in the year about downside risks from slowing global economic growth and the deterioration in financial conditions or similar concerns expressed by their business contacts had abated to some extent. However, a few participants noted that ongoing challenges in the agricultural sector, including those associated with trade uncertainty and low prices, had been exacerbated by severe flooding in recent weeks.

Participants observed that inflation pressures remained muted and that the most recent data on overall inflation, and inflation for items other than food and energy, had come in lower than expected. At least part of the recent softness in inflation could be attributed to idiosyncratic factors that seemed likely to have only transitory effects on inflation, including unusually sharp declines in the prices of apparel and of portfolio management services. Some research suggests that idiosyncratic factors that largely affected acylical sectors in the economy had accounted for a substantial portion of the fluctuations in inflation over the past couple of years. Consistent with the view that recent lower inflation readings could be temporary, a number of participants mentioned the trimmed mean measure of PCE price inflation, produced by the Federal Reserve Bank of Dallas, which removes the influence of unusually large changes in the prices of individual items in either direction; these participants observed that the trimmed mean measure had been stable at or close to 2 percent over recent months. Participants continued to view inflation near the Committee’s symmetric 2 percent objective as the most likely outcome, but, in light of recent, softer inflation readings, some viewed the downside risks to inflation as having increased. Some participants also expressed concerns that long-term inflation expectations could be below levels consistent with the Committee’s 2 percent target or at risk of falling below that level.

Participants agreed that labor market conditions remained strong. Job gains in the March employment report were solid, the unemployment rate remained low, and, while the labor force participation rate moved down a touch, it remained high relative to estimates of its underlying demographically driven, downward trend. Contacts in a number of Districts continued to report shortages of qualified workers, in some cases inducing businesses to find novel ways to attract new workers. A few participants commented that labor market conditions in their Districts were putting upward pressure on compensation levels for lower-wage jobs, although there were few reports of a broad-based pickup in wage growth. Several participants noted that business contacts expressed optimism that despite tight labor markets they would be able to find workers or would find technological solutions for labor shortage problems.

Participants commented on risks associated with their outlook for economic activity over the medium term. Some participants viewed risks to the downside for real GDP growth as having decreased, partly because prospects for a sharp slowdown in global economic growth, particularly in China and Europe, had diminished. These improvements notwithstanding, most participants observed that downside risks to the outlook for growth remain.

In discussing developments in financial markets, a number of participants noted that financial market conditions had improved following the period of stress observed over the fourth quarter of last year and that the volatility in prices and financial conditions had subsided. These factors were thought to have helped buoy consumer and business confidence or to have mitigated short-term downside risks to the real economy. More generally, the improvement in financial conditions was regarded by many participants as providing support for the outlook for economic growth and employment.

Among those participants who commented on financial stability, most highlighted recent developments related to leveraged loans and corporate bonds as well as the current high level of nonfinancial corporate indebtedness. A few participants suggested that heightened leverage and associated debt burdens could render the business sector more sensitive to economic downturns than would otherwise be the case. A couple of participants suggested that increases in bank capital in current circumstances with solid economic growth and strong profits could help support financial and macroeconomic stability over the longer run. A couple of participants observed that asset valuations in some markets appeared high, relative to fundamentals. A few participants commented on the positive role that the Board’s semi-annual Financial Stability Report could play in facilitating public discussion of risks that could be present in some segments of the financial system.

In their discussion of monetary policy, participants agreed that it would be appropriate to maintain the current target range for the federal funds rate at 2-1/4 to 2-1/2 percent. Participants judged that the labor market remained strong, and that information received over the intermeeting period showed that economic activity grew at a solid rate. However, both overall inflation and inflation for items other than food and energy had declined and were running below the Committee’s 2 percent objective. A number of participants observed that some of the risks and uncertainties that had surrounded their outlooks earlier in the year had moderated, including those related to the global economic outlook, Brexit, and trade negotiations. That said, these and other sources of uncertainty remained. In light of global economic and financial developments as well as muted inflation pressures, participants generally agreed that a patient approach to determining future adjustments to the target range for the federal funds rate remained appropriate. Participants noted that even if global economic and financial conditions continued to improve, a patient approach would likely remain warranted, especially in an environment of continued moderate economic growth and muted inflation pressures.

Participants discussed the potential policy implications of continued low inflation readings. Many participants viewed the recent dip in PCE inflation as likely to be transitory, and participants generally anticipated that a patient approach to policy adjustments was likely to be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective. Several participants also judged that patience in adjusting policy was consistent with the Committee’s balanced approach to achieving its objectives in current circumstances in which resource utilization appeared to be high while inflation continued to run below the Committee’s symmetric 2 percent objective. However, a few participants noted that if the economy evolved as they expected, the Committee would likely need to firm the stance of monetary policy to sustain the economic expansion and keep inflation at levels consistent with the Committee’s objective, or that the Committee would need to be attentive to the possibility that inflation pressures could build quickly in an environment of tight resource utilization. In contrast, a few other participants observed that subdued inflation coupled with real wage gains roughly in line with productivity growth might indicate that resource utilization was not as high as the recent low readings of the unemployment rate by themselves would suggest. Several participants commented that if inflation did not show signs of moving up over coming quarters, there was a risk that inflation expectations could become anchored at levels below those consistent with the Committee’s symmetric 2 percent objective—a development that could make it more difficult to achieve the 2 percent inflation objective on a sustainable basis over the longer run. Participants emphasized that their monetary policy decisions would continue to depend on their assessments of the economic outlook and risks to the outlook, as informed by a wide range of data.

-

Free Webinar Today

Eddy Elfenbein, May 22nd, 2019 at 10:01 amJoin me at 4 pm ET for a free webinar. I’ll be joined by John Schindler, a national security expert. It should be a great discussion. You can register here.

-

Morning News: May 22, 2019

Eddy Elfenbein, May 22nd, 2019 at 7:06 amU.S. Weighs Blacklisting Up to Five Chinese Surveillance Firms

The Economy Is Strong and Inflation Is Low. That’s What Worries the Fed.

U.S. Existing-Home Sales Continued to Falter in April

Apple’s China Business Faces Another Blow From Trump’s Huawei Ban

The Trump Administration Is Selling Out Hundreds of Millions of Cell-Phone Users

U.S. Judge Rules Qualcomm Practices Violate Antitrust Law

Walmart to Make First Direct Pitch to Big Corporate Ad Buyers at New York Event

Huawei Unwanted: Asian Shops Shun Phone Trade-Ins on Google Suspension Worries

Wow Air Collapse Decimates Iceland’s Economy

TransferWise is Now Europe’s Most Valuable Fintech Start-Up, With a $3.5 Billion Valuation

New Coke Was a Debacle. It’s Coming Back. Blame ‘Stranger Things.’

Belgian Monastery Will Brew Beer Again, After A 220-Year Pause

Nick Maggiulli: Stop the Financial Pornography!

Joshua Brown: The Only Two Scarce Resources Left on Wall Street

Howard Lindzon: Lindzanity – Doug Horlick Worked At Goldman Sachs and I Like Him

Be sure to follow me on Twitter.

-

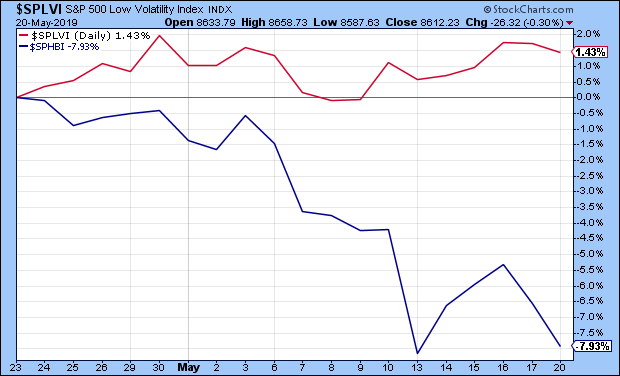

The Growing Divergence

Eddy Elfenbein, May 21st, 2019 at 7:56 amOver the last month, there’s been a growing divergence in the stock market. The more volatile stocks of the High Beta sector have done poorly whereas the conservative stocks of the Low Vol group have barely budged. In fact, they’re up some.

Check out this chart of High Beta (in blue) versus Low Vol (in red) over the last month.

Typically, this represents a market that’s become nervous. When in doubt, investors flock toward safety. At least, perceived safety.

-

Consider this Hypothetical…

Eddy Elfenbein, May 21st, 2019 at 7:46 amI want you to consider a hypothetical scenario. Let’s say you’re given two bits of information on a company from the future.

First, you’re told that the company is about to release a product that will become a big hit. The technology is superior to what’s out there and the price is much cheaper. The public will love it.

Secondly, the company operates in a country whose currency is about to appreciate against the US dollar.

My question is, knowing just those two bits of information, is the stock a buy? (Bear in mind, this is just a thought exercise.)

In my mind, the answer is yes, and obviously so. Yet, for many people, they don’t see it that way. They would shy away from the investment due to currency concerns.

The reason I bring this up is that this thought exercise spotlights the mistake many investors make when it comes to analyzing the stock market. They get wrapped up in the mechanics of the market and don’t pay enough attention to what the market is actually trying to do.

The products are the end result of the market. But you’ll notice that much debate is about the details of the market. What do I mean by this? You’ll hear constant jabber about the Federal Reserve, the impact of buy backs, valuations, politics, currencies, inflation, the CAPE Ratio and on and on.

While these have a role to play, they’re dwarfed by the most important factor and that’s serving the public with better goods and services. If you’re doing that, you’ll override the mechanics of the market, and if you can’t, you won’t. It’s that simple.

I remember Peter Lynch saying that if you’re looking to buy a car company, you should be reading Road and Track, not the Wall Street Journal.

This is a generality, but a poor balance sheet typically isn’t the ruin of a bad company. Rather, it’s poor performance in the marketplace that begins the wreckage of the balance sheet. The company may use bad finances to mask the damage, but the starting point is that the company’s products could not compete.

When looking a potential investment, don’t overthink this crucial factor. The company must be a winner in its marketplace in order to thrive.

-

Morning News: May 21, 2019

Eddy Elfenbein, May 21st, 2019 at 7:14 amThe Tech Cold War Begins: How Big Tech is Affected

As Huawei Loses Google, the U.S.-China Tech Cold War Gets Its Iron Curtain

Trump’s Huawei Attack Is a Serious Mistake

QE May Be Over, But the Fed’s U.S. Debt Hoard Is About to Soar

2-Tiered Wages Under Fire: Workers Challenge Unequal Pay For Equal Work

A Delicate Balance – Toyota Took Care to Make Offering to U.S. Before China Deals

Home Depot Earnings Beat Despite Wet Start to Spring

U.S. Postal Service Starts Testing Self-Driving Trucks

Morgan Stanley Slashes Worst-Case Price for Tesla to $10

Silicon Valley’s Shame: Living in a Van in Google’s Backyard

Top Reason For CEO Departures Among Largest Companies Is Now Misconduct, Study Finds

Animal Spirits: The Absence of Stuff

Ben Carlson: The Difference & Talk Your Book: Jeremy Schwartz of WisdomTree

Jeff Carter: Banking With Pipit Global & Dark Patterns Are Insidious Or Are They Harmless?

Be sure to follow me on Twitter.

-

Dividends Are Rising Around the World

Eddy Elfenbein, May 20th, 2019 at 9:51 amFrom CNBC:

Global dividends reached a first-quarter record of $263.3 billion, rising 7.8% despite concerns about the world economy, according to new research Monday.

The Janus Henderson Global Dividend Index said that U.S. dividends totaled a record $122.5 billion during the period, up 8.3%. Underlying U.S. growth, where it is adjusted for special dividends and changes in currency, saw a climb of 9.6%. Almost 90% of American companies featured in the index raised dividends, the highest increases coming from the banking sector.

Janus Henderson expects a record $1.43 trillion in dividend payments this year, up 4.2% in headline terms, led by North America, where growth is the fastest worldwide on an underlying basis.

-

The Taxi Medallion Bubble

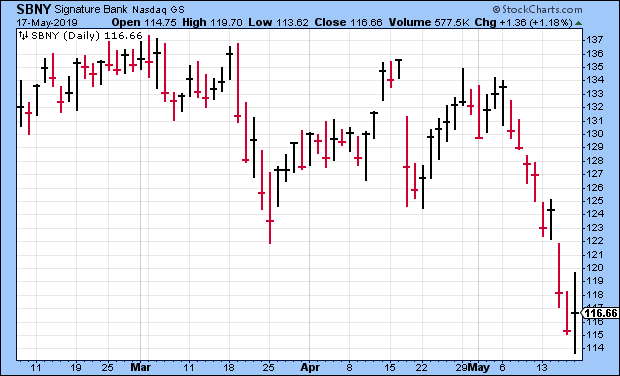

Eddy Elfenbein, May 20th, 2019 at 8:44 amThe New York Times has a long, detailed and very sad look at the implosion of the taxi medallion business. A lot of cab drivers, many of who are immigrants, were ruined. There’s been a spate of suicides as well.

One of our stocks, Signature Bank (SBNY), played a big role in this market. However, I think the bank behaved responsibly, for the most part. You can’t easily blame a bubble on the banks. The rise of ride-sharing apps played a role as well.

Here’s a quote from a Signature executive:

Walter Rabin, who led Capital One’s medallion lending division between 2007 and 2012 and has led Signature Bank’s medallion lending division since, said he was one of the industry’s most conservative lenders. He said he could not speak for the brokers and fleet owners with whom he worked.

Mr. Rabin and other Signature executives denied fault for the market collapse and blamed the city for allowing ride-hail companies to enter with little regulation. “It’s the City of New York that took the biggest advantage of the drivers,” said Joseph J. DePaolo, the president and chief executive of Signature. “It’s not the banks.”

That’s correct. The city deserves a lot of blame.

Some lenders, especially Signature Bank, have let borrowers out of their loans for one-time payments of about $250,000. But to get that money, drivers have had to find new loans. Mr. Greenbaum, a fleet owner, has provided many of those loans, sometimes at interest rates of up to 15 percent, loan documents and interviews showed.

The stock had been sinking over the past two weeks, perhaps in anticipation of a hit job. I think SBNY came out well.

-

Morning News: May 20, 2019

Eddy Elfenbein, May 20th, 2019 at 7:10 amIn a Surprise, Japan’s Economy Grew in the First Quarter, Despite a Slowdown in China

U.S., China Bicker Over ‘Extravagant Expectations’ on Trade Deal

Trade Uncertainty Darkens U.S. Small Caps Outlook

Top U.S. Tech Companies Begin to Cut Off Vital Huawei Supplies

T-Mobile and Sprint Plan Concessions to Get Their $26.5 Billion Merger Cleared

Tesla Falls as Analyst Says Its Profit Goal Is a ‘Kilimanjaro-Like’ Climb

Amazon Faces Investor Pressure Over Facial Recognition

Morgan Stanley’s Teflon Banker Chases Next Deal After Uber Flops

Where to Live If You Want the Highest Salary and Disposable Income

US Breaks Record for Dividends as Investor Payouts Surge Around the World

Who Is Robert F. Smith, the Man Paying Off Morehouse Graduates’ Loans?

‘They Were Conned’: How Reckless Loans Devastated a Generation of Taxi Drivers

A Convicted Felon Explains How He Pulled Off An Infamous Accounting Fraud

Cullen Roche: Three Things I Think I Think – It’s Rubio!

Roger Nusbaum: Don’t Make This Mistake With Factor Investing

Jeff Miller: What Determines the Agenda for Investment News?

Be sure to follow me on Twitter.

-

FactSet Raises Dividend 12.5%

Eddy Elfenbein, May 17th, 2019 at 12:05 pmFactSet (FDS) raised its dividend by 12.5%. The payout will rise from 64 cents to 72 cents per share. This is the 14th annual dividend increase in a row.

FactSet, a global provider of integrated financial information, analytical applications, and industry-leading services, today announced that its Board of Directors approved a 12.5% increase in the regular quarterly cash dividend from $0.64 per share to $0.72 per share.

The $0.08 per share increase marks the fourteenth consecutive year the Company has increased dividends, demonstrating its continued commitment to return value to shareholders. The cash dividend will be paid on June 18, 2019 to holders of record of FactSet’s common stock at the close of business on May 31, 2019.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His