CWS Market Review – April 17, 2020

“The economy is clearly in ruins here.” – Chris Rupkey, chief financial economist at MUFG Union Bank

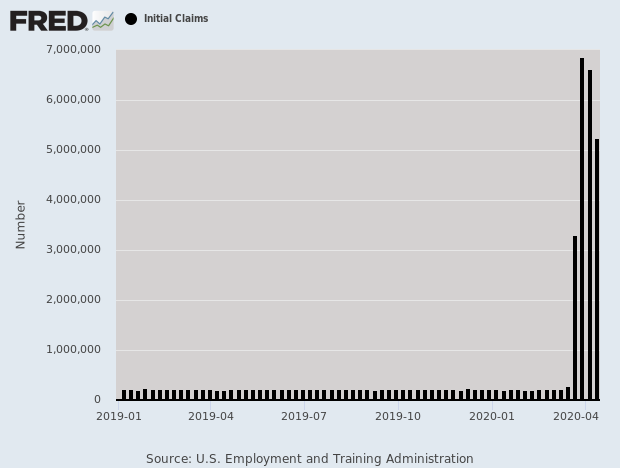

On Thursday, we got another jobless-claims report and it was more bad news. For the week, 5.245 million Americans filed for first-time jobless claims. We’re assuming that number is accurate, but I’m not sure if the system can handle 20 times the normal volume. I’m hearing stories of lots of delays.

Over the past four weeks, 22 million Americans have filed first-time claims. That’s more than all the jobs lost in 2008. We seem to be in a race to flatten the curve before the curve flattens us.

Despite the dire economic news, the stock market has held up fairly well. Will it last? That may depend on Q1 earnings season, which just began. In this week’s issue, we’ll take a closer look at our upcoming Buy List earnings reports. I have a complete earnings calendar for you with all our earnings dates and Wall Street’s consensus.

But first, let’s take a closer look at where the market stands and why we’re rallying in the face of such lousy news.

The Market Rallies on Terrible News

Since March 23, the stock market has had a very impressive run. Based on closing prices, the S&P 500 has gained more than 25% in 17 trading sessions. Of course, that’s following a very nasty spill. Still, it’s one of the biggest bounces in years.

The stock market is, by nature, forward-looking, so it tends to move first. Economic reports, however, are by nature backward-looking. That’s why it’s only now that we’re learning how bad things truly are. The mismatch between the focus of the market and that of the economic reports also explains why the market is rallying amid such ugly news.

Last week was the second-best week for the Dow in 80 years, while the best week came two weeks before. We’re even seeing some big-name stocks like Walmart, Amazon and Netflix make new highs. All of those are helping people cope during the shut-in. On our Buy List, Silgan Holdings (SLGN) just touched a new 52-week high.

I want to reiterate my position that I won’t predict a testing of the recent low, but it’s safe to act like that will happen. We can only go by history which suggests that it’s too early to sound the all-clear. Bear-market rallies are tempting, but they can end badly.

The market continues to be very volatile. I’ll give you an example. The S&P 500 had already had 24 daily moves this year of more than 3%. There was only one 3% day all of last year. Going back a little, there were no 3% days in 2012, 2013 and 2014.

I want to cover some of the recent economic news in more detail because it gives us a picture of just how severe the recession is. The retail-sales report for March showed a decline of 8.7%. That’s more than twice the previous record decline. This report is often a good indicator of consumer spending. The consumer is 70% of the economy.

The industrial-production report for March fell by 5.4%. Capacity utilization fell 4.3% to 72.7%. That’s 7.1% below the long-run average.

Homebuilder confidence was a doozy. It fell from 72 to 30. There’s never been a decline anywhere close to that. Economists had been expecting 55.

Earlier this week, the price for oil dropped below $20 per barrel and hit an 18-year low. OPEC wants to cut production, but that isn’t the issue. The obvious problem is demand.

The New York Fed puts out the Empire State Manufacturing Survey. (I read it so you don’t have to.) I have to confess that it normally makes for pretty dry reading. Not this month. Check out the opening paragraph.

Business activity plunged in New York State, according to firms responding to the April 2020 Empire State Manufacturing Survey. The headline general business conditions index plummeted fifty-seven points to -78.2, its lowest level in the history of the survey—by a wide margin. New orders and shipments declined at a record pace. Delivery times lengthened, and inventories fell. Employment levels and the average workweek both contracted at a record pace. Input price increases slowed considerably, while selling prices declined modestly. Though current conditions were extremely weak, firms expected conditions to be slightly better six months from now.

Trust me. For economists, that’s freaking out.

The main issue is still the virus. We’ve certainly made progress, and the number of new cases appears to have peaked, but there’s still a long way to go. Many states are closed until mid-May, and that’s at the earliest. I can already see grumblings from voters, and that could grow.

The equation isn’t hard. Once things are better, the economy can reopen. I assume it will happen in stages. Once businesses can get back to a full footing, employment and profits will grow.

First-quarter earnings season has begun, and we’re seeing how much damage has happened to corporate profits. At the start of the year, Wall Street had expected the S&P 500 to report Q1 earnings of $40.29 per share. (That’s the index-adjusted figure. Each point is about $8.3 billion.) That’s been revised down to $34.71 per share.

If that’s correct, then it would be a decline of 8.6% from last year’s Q1. Bear in mind that the first half of Q1 was largely unaffected by Covid-19. For Q2, Wall Street expects an earnings decline of 18.4%.

Q1 Earnings Calendar

Our Buy List is close to a five-week high. Thanks to the market’s rally, we now have six stocks that are up for the year, and 15 of the 25 are beating the market this year.

Here’s a look at our Q1 Earnings Calendar. Over the next few weeks, 21 of our 25 Buy List stocks will report their earnings. I’ve listed each stock’s name, ticker symbol, earnings date and Wall Street’s consensus. I don’t have all the reporting dates just yet. (Some companies are quite good at corporate communications. Others are somewhat less so.)

| Company | Ticker | Date | Estimate |

| Stepan | SCL | 21-Apr | $0.78 |

| Silgan Holdings | SLGN | 22-Apr | $0.50 |

| Globe Life | GL | 22-Apr | $1.72 | Eagle Bancorp | EGBN | 23-Apr | $0.97 |

| Hershey | HSY | 23-Apr | $1.70 |

| Check Point Software | CHKP | 27-Apr | $1.38 |

| Cerner | CERN | 28-Apr | $0.70 |

| Sherwin-Williams | SHW | 29-Apr | $3.94 |

| AFLAC | AFL | 29-Apr | $1.11 |

| Church & Dwight | CHD | 30-Apr | $0.77 |

| Intercontinental Exchange | ICE | 30-Apr | $1.23 |

| Stryker | SYK | 30-Apr | $1.88 |

| Moody’s | MCO | 30-Apr | $2.19 |

| Trex | TREX | 4-May | $0.61 |

| ANSYS | ANSS | 6-May | $0.80 |

| Becton Dickinson | BDX | 7-May | $2.40 |

| Danaher | DHR | 7-May | $1.02 |

| Fiserv | FISV | 7-May | $1.03 |

| Broadridge Financial Solutions | BR | TBA | $1.74 |

| Disney | DIS | TBA | $0.88 |

| Middleby | MIDD | TBA | $1.36 |

We have five earnings reports due next week.

Stepan (SCL) will be our first Buy List stock to report this earning season. The results are due out on Tuesday morning, April 21. In February, Stepan said it made $1.10 per share for its fourth quarter. Technically, analysts had been expecting 88 cents per share, but that’s a consensus of just two analysts. One expected 86 cents, and the other 90 cents. For the year, SCL made $5.12 per share.

Stepan is one of our new stocks this year. The company is a major manufacturer of specialty and intermediate chemicals. It’s pretty boring but quite profitable. Stepan has increased its dividend for 52 years in a row.

Stepan’s CEO said, “Despite significant challenges during the year, driven by the equipment failure in Ecatepec, the wet weather in the U.S. farm belt, the sulfonation exit in Germany and FX headwinds, the Company exceeded its 2018 record full-year adjusted net income and grew adjusted EPS 7%.”

For Q1, the three analysts expect earnings of 78 cents per share. That’s down from $1.31 per share last year. My Buy Below on Stepan is currently at $110 per share, but I’ll probably lower it next week after I get a chance to see the earnings report.

Silgan Holdings (SLGN) is our second-best performing stock this year. Through Thursday, SLGN is up 7.46%. The stock made a new 52-week high on Thursday.

The company is due to report earnings on Wednesday, April 22. Three months ago, Silgan reported Q4 earnings of 38 cents per share. That pinged Wall Street’s forecast on the nose. Silgan had said they expected earnings between 34 to 39 cents per share, which seems like a wide range.

Frankly, Silgan did not have a great 2019, but I see a lot of promise for them going forward. The company is one of the leading makers of metal containers in the world. In North America, Silgan holds the #1 position in metal food containers. Silgan’s containers are used by folks like Campbell’s Soup, Del Monte and Nestlé.

For 2020, Silgan sees earnings ranging between $2.28 and $2.38 per share. I expect to see that lowered. Silgan recently raised its quarterly dividend by 9% to 12 cents per share. This was their 16th consecutive annual dividend increase. For Q1, Wall Street expects earnings of 50 cents per share.

Globe Life (GL) is also scheduled to report on Wednesday. The insurance stock has been hit hard this year. In February, GL reported Q4 operating income of $1.70 per share. That was two cents below estimates. For 2020, GL expects operating earnings of $7.03 to $7.23 per share. For Q1, Wall Street expects $1.72 per share.

Eagle Bancorp (EGBN) will report earnings on Thursday, April 23. This bank has been our problem child this year. It’s our second-worst performer, trailing only Middleby (MIDD). The bank was hit especially hard by the corona-induced bear. In 16 sessions, EGBN fell 43%.

Still, the actual results haven’t been that bad. For Q4, Eagle earned $1.06 per share. That was one penny below estimates. For all of 2019, Eagle made $4.18 per share. That’s down from $4.44 per year in 2018.

The big issue for Eagle is their legal fees. For Q4, the bank’s legal, accounting and professional fees and expenses rose 68% to $4.1 million. That’s about 12 cents per share.

Looking past these expenses, the bank’s doing just fine. For Q4, Eagle had a return-on-equity of 11.78%. The bank’s efficiency ratio was 39.7% for Q4 and 40% for the entire year. The legal expenses aren’t pleasant, but it’s a manageable problem.

For Q1, Wall Street expects 97 cents per share. At the current price, the dividend yields 3.1%. I’ll probably lower the $48 Buy Below price, but I want to see the earnings first.

Hershey (HSY) will also report on Thursday. HSY is another of our better-performing stocks this year. Hershey is a classic defensive stock, which means it hasn’t been as severely impacted by the bear market. In January, the chocolatier reported Q4 earnings of $1.28 per share. That was four cents better than estimates. The company had been expecting $1.18 to $1.24 per share. For the year, Hershey made $5.78 per share. Last year was a good year for them.

For 2020, Hershey sees earnings between $6.13 and $6.24 per share. For Q1, Wall Street expects earnings of $1.70 per share.

That’s all for now. There are a few key economic reports due out next week. We’ll get the existing-home sales report on Tuesday. The next jobless-claims report is due out on Thursday. This report has become the most-watched economic report on Wall Street. The new-homes sales report will also be out on Thursday. Then on Friday, the durable-goods report is due out. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on April 17th, 2020 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His