Posts Tagged ‘ROST’

-

CWS Market Review – November 21, 2014

Eddy Elfenbein, November 21st, 2014 at 7:08 am“Become more humble as the market goes your way.” – Bernard Baruch

Before I get into this week’s CWS Market Review, I have two announcements. The first is that there will be no newsletter next week. It’s Thanksgiving, and I’m taking a little break. The second is that I’ll be unveiling next year’s Buy List in the CWS Market Review on December 19, 2014, which is four weeks from today.

As always, I’ll be adding five stocks and deleting five stocks. The 2015 Buy List won’t take effect until the start of trading in January. I like to announce the names a few days ahead of time so no one can claim the positions are somehow manipulated. Later on in today’s newsletter, I’ll give you a list of some stocks I’m thinking about adding or deleting.

Now…about this lethargic stock market. The recent market hasn’t merely been slow; it’s been one of the sleepiest markets in history. Every day, it seems, the indexes climb higher, but only microscopically. The S&P 500 just closed out a five-day run where it didn’t close higher or lower by more than 0.1%. That hasn’t happened in 50 years.

The S&P 500 hasn’t had a meaningful down day in nearly a month. The last time the index dropped by more than 0.3% (which isn’t that much) was on October 22. The S&P 500 has closed higher 19 times in the last 26 sessions, but most of those were very small increases. The index has now closed above its five-day moving average for an amazing 25 straight days. That’s the longest streak since 1986. On Thursday, the market closed at yet another all-time high.

I’m pleased to note that our Buy List continues to do well. We had two very good earnings reports this week. Medtronic jumped nearly 5% on Tuesday after it reported good earnings. Then on Thursday, Ross Stores handily beat Wall Street’s earnings consensus, and the shares are poised to move much higher. I’ll give the details on those in just a bit, but first let’s look at some ideas I’m considering for the 2015 Crossing Wall Street Buy List.

Potential Changes for Next Year’s Buy List

According to the rules of our Buy List, I select 20 stocks each year. The portfolio is then locked and sealed, and I can’t make any changes for the next 12 months. (This set-and-forget rule has probably helped me more than I realize, since it’s prevented me from dumping good names at the first sign of trouble.) Each year, I swap out five names, which means my annual portfolio turnover is just 25%.

Right now, the five names I’m considering for deletion are CA Technologies ($CA), DirecTV ($DTV), IBM ($IBM), McDonald’s ($MCD) and Medtronic ($MDT). This is just a preliminary list: there’s no guarantee that these will be the ones to be cut when I make the big announcement next month.

Let me run through some thoughts on each of the names.

We did very well with DirecTV ($DTV), and I was happy to have it on our Buy List. But now it’s time to say goodbye. If all goes according to plan, the company will soon be bought out by AT&T. I like AT&T, but I’d rather not have it on our Buy List.

Medtronic ($MDT) is in a similar position. The medical-device stock has done very well for us, and particularly well lately (I’ll discuss this week’s earnings report in a bit). But Medtronic is about to become a very different company from the one we originally bought. The Covidien deal is a gigantic undertaking. They’re basically doubling in size, and there will need to be a lot of cost-cutting. If all goes well, Medtronic will soon take the name Medtronic PLC and will be incorporated in Ireland.

IBM ($IBM) and McDonald’s ($MCD) are also problematic. I simply made a mistake with both stocks. I thought both stocks were turning around, but the problems are more serious than I imagined. I think the prospects for McDonald’s could improve, but it’s too early to say. Their sales are flat, while competitors like Chipotle are cranking same-store-sales growth of 20%. IBM made a series of errors, and I think there need to be some changes at the top. Frankly, I think the two companies share a trait: they aren’t sure what kind of business they want to be.

CA Technologies ($CA) may be the weakest of the bunch. Their sales are in a tailspin. I should have pulled the plug a long time ago. As an investor, I always need to be frank about my mistakes, and I missed how serious the problems were at CA.

Ten Possible Additions for Next Year’s Buy List

Here are ten stocks I’m strongly considering for next year’s Buy List:

Alliance Data Systems ($ADS)

Babcock & Wilcox ($BWC)

Cardtronics ($CATM)

Colgate-Palmolive ($CL)

FactSet Research Systems ($FDS)

Howard Hughes Corporation ($HHC)

SEI Investments ($SEIC)

Signature Bank ($SBNY)

Tupperware Brands ($TUP)

Westinghouse Air Brake Technologies ($WAB)

I reserve the right to change my mind over the next four weeks, but I can say that these ten stocks are under serious consideration for next year’s Buy List. I don’t want to go into more detail, though, until I’ve made my final decision. Now let’s look at some recent earnings news.

Medtronic Is a Buy up to $76 per Share

In last week’s CWS Market Review, I said that I didn’t expect a big earnings beat from Medtronic ($MDT), and I was right. On Tuesday, the medical-device maker reported fiscal Q2 earnings of 96 cents per share. That met expectations right on the nose. For comparison, the company earned 91 cents per share for last year’s Q2.

The important news is that Medtronic continues to do well. The company also took the opportunity to reiterate that the Covidien ($COV) deal is on track. They hope to close the deal by the beginning of next year. At that time, Medtronic will reincorporate in Ireland, and its new name will be Medtronic PLC. The deal is up for a shareholder vote on January 6. I think it will pass easily.

For Q2, quarterly sales came in at $4.37 billion, which was a shade more than the consensus of $4.36 billion. Medtronic also reiterated its full-year earnings outlook of $4.00 to $4.10 per share. Their fiscal year ends in April, and Medtronic has already made $1.89 for the first two quarters of this year. That means they see earnings ranging between $2.11 and $2.21 per share for the last six months of this fiscal year. Medtronic earned $2.03 for the back-half of FY 2014.

Omar Ishrak, Medtronic’s CEO, said, “Revenue growth was at the upper end of our full-year revenue outlook and within our mid-single digit baseline goal, reflecting the strong execution of our global organization.”

The shares popped 4.7% on Tuesday and reached a new all-time high price. In the last three years, Medtronic has gained more than 116% for us, compared with 72% for the S&P 500. As I said before, there’s a good chance that Medtronic won’t be on next year’s Buy List, but that’s due to the deal, and not to any business failure. This week, I’m raising my Buy Below on Medtronic to $76 per share.

Ross Stores Beat Earnings

In last week’s CWS Market Review, I wrote, “For Q3, Ross said it expects earnings to range between 83 and 87 cents per share. Oh, please. That’s almost certainly too low.” I was right again. The deep discounter earned 93 cents per share for its fiscal third quarter.

I wish I could say this was due to my supernatural powers to divine the future. I’m sad to say that I was simply looking at the numbers, and the math said Ross is doing just fine. Quarterly sales rose 8% to $2.599 billion. Same-store sales, which is the key number for retailers, were up by 4%. Ross continues to deliver.

The CEO said, “We are pleased with the better-than-expected sales and earnings we achieved in the third quarter. These results were driven by our ongoing ability to deliver compelling bargains to our customers, which drove above-plan sales gains and strong merchandise gross margins. Operating margin for the quarter grew 55 basis points due to a 40-basis-point improvement in cost of goods sold and a 15-basis-point decline in selling, general and administrative expenses.”

Now let’s look at their guidance. For Q4, which is the all-important holiday shopping season, Ross forecasts earnings between $1.05 and $1.09 per share. Ross earned $1.02 for last year’s Q4. For the entire year, Ross sees earnings ranging between $4.28 and $4.32 per share. That’s an increase of 10% to 11% over last year.

Ross Stores is an excellent example of our style of investing. The stock had a miserable first half of 2014. By July, shares of ROST had dropped below $62. The shares were down more than 17% on the year. But the numbers still looked good, and we held on. ROST has rallied strongly ever since. The shares are now up more than 11% for the year, which is just ahead of the S&P 500.

The stock looks to open higher on Friday morning. This week, I’m raising our Buy Below on Ross Stores to $91 per share.

That’s all for now. The stock market will be closed next Thursday for Thanksgiving. The market will close at 1 pm on Friday. This is usually the slowest trading day of the year. There’s not much reason for the market to be open, but the NYSE hates to have the exchange closed four days in a row. The only interesting economic report will come on Tuesday when we get the first revision to Q3 GDP. The initial report said that the economy grew by 3.5% for Q3. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – November 14, 2014

Eddy Elfenbein, November 14th, 2014 at 7:17 am“Things are almost never clear on Wall Street, or when they

are, then it’s too late to profit from them.” – Peter LynchConsider this fact: In the last four weeks, the value of the global stock market has increased by a staggering $3.4 trillion. For some reason, we were terrible investors in September and early-October, but we’ve been brilliant investors ever since.

Or…perhaps, the mood of investors turned on a dime. It’s hard to believe that only a few days ago, investors were scared out of their wits about impeding elections, a deteriorating economy in Europe and truly scary news about the Ebola virus. How times have changed!

Investors shook these fears off and the stock market rallied to new highs again this week. Through Tuesday, the S&P 500 hit record closing highs for five straight days. The index has now made 40 record highs this year. That compares with 45 record highs last year. The S&P 500 has closed higher 16 times in the last 21 trading days, and three of those five declines were pretty measly (less than 0.2%). In the last month, we’ve experienced only one meaningful daily decline. This has been a golden time for investors, although trading volume has been very low (some chart watchers say that’s a bad sign).

In this week’s CWS Market Review, we’ll take a closer look at what’s driving this market. The simple explanation is that what’s been happening is still happening, only more so. Don’t worry; I’ll explain what it all means in a bit. I’ll also review this past earnings season. Except for a few duds, this was a solid earnings season for our Buy List. I’ll also preview two Buy List reports coming our way next week. Yes, the October reporting cycle is already upon us. We also had another good jobs report last week. But first, let’s look at what’s driving this market.

What’s Driving this Market

This has been a fascinating rally of late because we can see several factors at work. The most important factor continues to be the strength of the U.S. dollar. I’m afraid I might sound like I’m discussing the same phenomenon each week, but the dollar’s impact is crucial to what’s impacting our portfolios.

Since the economy in Europe and Japan are still quite weak, the governments there are purposely trying to weaken their currencies. It’s not so much that the dollar is truly strong; it’s that the greenback is the tallest Munchkin in Munchkin Land. Of course with forex, that’s all that matters. The yen just dropped to a seven-year low against the dollar. It looks like the government is about to call snap elections there. The British pound recently fell to a 14-month low against the dollar.

One impact of the rising dollar is that it puts the squeeze on commodity prices. The price of gold recently fell to a four-year low. Gold has been in a near non-stop plunge over the last three years. Since its 2011 peak, gold has lost close to $800 per ounce. That’s not all. Crude oil has been falling as well. On Thursday, oil fell below $75 per barrel. For the first time since 2010, prices at the pump are below $3 per gallon.

One of the reasons for the drop in oil is that Saudi Arabia has stepped up production. Normally, the Saudis would try to curtail their output in an attempt to prop up prices. This is probably evidence of OPEC’s declining influence. We can also see that Energy stocks have been quite weak (see the chart below). Many of the large oil stocks have mostly sat out this rally. The Energy Sector ETF ($XLE) is down slightly for the year, while most other sectors have done quite well. We currently don’t have any Energy stocks on the Buy List so that’s been a big help. I don’t see a broad rally for the Energy sector starting anytime soon.

Lower gas prices have been a welcome relief for many consumers. Despite the growth in payrolls, workers haven’t seen any real improvement in their wages. Since 2007, median income is down by 5%. About 10% of retail sales goes towards gasoline so lower prices at the pump frees up more money for other items. On Thursday, Walmart ($WMT) impressed Wall Street by reporting earnings that topped the consensus figure by three cents per share. The stock jumped 4.7% on the day. Business has been going well for WMT lately. Next year, Walmart has a good chance of clearing $500 billion in annual revenue.

Walmart’s strength has been good news for our favorite retailers. Shares of Bed Bath & Beyond ($BBBY) breached $71 this week. The stock hasn’t been that high since January. Our other big retailer, Ross Stores ($ROST), is due to report its fiscal Q3 earnings on Thursday, November 20. This is for the quarter that ended in October. Like BBBY, Ross has been rallying strongly lately. The shares topped $83 on Thursday for a fresh 52-week high. It was only four months ago that Ross was languishing at $62 per share.

For ROST’s last earnings report in August, the deep discounter beat estimates by six cents per share. The stock jumped more than 7% the next day, and it has continued to rally. For Q3, Ross said it expects earnings to range between 83 and 87 cents per share. Oh, please. That’s almost certainly too low. (Ross tends to be conservative with its estimates.)

For Q4 (November, December and January), Ross expects to see earnings between $1.05 and $1.09 per share. Naturally, the holiday season is very important for any retailer. For this year, Ross sees earnings coming in between $4.18 and $4.26 per share. Ross is getting pricier but it’s far from outrageous. For now, I’m keeping our Buy Below tight, at $83 per share. If the results are good, I’ll raise the Buy Below. Ross Stores continues to be a solid stock. Our patience has paid off.

Finance and Healthcare Have Been the Leaders

The two sectors of the market that have taken the lead for the Strong Dollar Trade are Healthcare and Finance, although Healthcare’s big run has preceded the emergence of the Strong Dollar Trade. The Healthcare Sector ETF ($XLV) has been a steady winner since February 2011. The recent election results also gave a boost to many Healthcare names.

The Healthcare stocks on our Buy List have also been doing quite well. Stryker ($SYK), Medtronic ($MDT) and CR Bard ($BCR) all hit new 52-week highs on Thursday. All three stocks are also handily beating the market this year. The Buy List is overweighted with Healthcare and that’s been good for us this year.

Medtronic is due to report earnings on Tuesday, November 18. This will be for their fiscal second quarter. Three months ago, the medical device stock topped earnings by a penny per share. For Q1, revenue rose 4.7% to $4.27 billion, which was $20 million better than expectations. Medtronic had its strongest growth for U.S. medical devices in five years.

The best news for Medtronic recently was the result of last week’s election. While I caution investors not to let their politics interfere with their investments, it appears that Congress will try to repeal the medical devices tax. I can’t say if this will happen, but it’s interesting to note that shares of MDT bounced nicely the day after the election.

Medtronic has stood by its intended acquisition of Covidien ($COV). The company plans to rework the specifics so it can clear any new regulations concerning tax inversions. This week, the company also offered concessions to please EU regulators. Medtronic will restructure the financing for the $43 billion deal which will allow the American company to reincorporate in Ireland and thereby lower its tax bill.

Medtronic has said they see full-year earnings (ending in April) ranging between $4.00 and $4.15 per share. Wall Street currently expects Q2 earnings of 96 cents per share. I don’t expect a big earnings beat from Medtronic. Rather, I expect to see more steady growth. This is an ideal stock for conservative investors. Medtronic is a buy up to $70 per share. Again, I’ll raise the Buy Below if earnings are strong, but I caution you not to chase it. Disciplined investors wait for good stocks to come to them.

Financial stocks have been more of a direct beneficiary of the Strong Dollar Trade. The Financial sector has led the market since August 20, although many financials got dinged hard in early October.

Our big banking stock is Wells Fargo ($WFC), and that’s ridden the recent wave quite nicely. Shares of WFC touched a new high a few days ago. The bank’s earnings have been very good lately, and they’ve navigated a difficult time for the industry. Wells is by far the best-run big bank in the country. (By the way, I’m so happy we got rid of JPMorgan this year.) Wells Fargo is a buy up to $54 per share.

Survey of Q3 Earnings Season

Earnings season is just about done, so let’s look at where we stand. Of the 445 companies in the S&P 500 that have reported so far, 332 beat expectations, 73 missed and 40 met.

For Q3, the S&P 500 is on track to report operating earnings of $29.83 per share. That’s an index-adjusted number, and it represents an increase of 10.8% over last year’s Q3. (These numbers are from S&P and they sometimes differ from other news sources.) At the start of the year, Wall Street had been expecting $30.89 for Q3. The estimates gradually fell as the year wore on. I should add that estimates generally start out too high, and it’s common to see them fall as earnings day approaches.

Over the last four quarters, the S&P 500 has earned $114.74 per share, so the index is going for 17.8 times that. Wall Street currently expects Q4 earnings to come in at $31.13 per share. That would be an increase of 10.2% over last year’s Q4. I like to see these steady 10% to 12% increases.

Interestingly, the estimates for Q4 had been fairly stable for much of the year. At the beginning of 2014, Wall Street was expecting $32.17 for Q4. On September 30, the estimate had increased by a tiny bit to $32.24. Only recently have the numbers come down.

If the current Q4 estimate is accurate, it would bring full-year earnings to $117.62. That would be an increase of 9.6% over last year. I’m fine with that. Going by Thursday’s close, the S&P 500 is now up 10.33% this year. In other words, the S&P 500 has largely kept pace with earnings this year. Despite some careless talk of bubbles, valuations haven’t changed. I should add that dividend growth has mostly tracked share prices as well.

In other words, there’s no bubble. The threat to the market isn’t excess valuations. Rather, it’s the potential for lack of growth. I don’t see difficulties in the immediate horizon, but that could change. As long as rates stay low, and the economy expands, stocks are the place to be.

Buy List Updates

This week, for the first time since September, shares of Ford ($F) topped $15 per share. The company finally started production on its aluminum-based F-150 trucks. This could be a game changer for the industry. (I hate that cliché so forgive me, but it’s true in this case.) Ford is currently going for less than 10 times next year’s earnings. The automaker just reported very good sales growth in Europe, especially in Britain and Italy. Ford remains a good buy up to $17 per share.

Earlier I mentioned that Stryker ($SYK) reached a new 52-week high. I also expect to see Stryker increase its dividend soon. Last year’s increase came on December 4. The company currently pays 30.5 cents per share. I think that will go up to 33 to 34 cents per share. Stryker is a buy up to $90 per share.

That’s all for now. Next week, we’ll get important reports on Industrial Production and Capacity Utilization. On Wednesday, the Fed will release the minutes from the last FOMC meeting. That’s when the Fed decided to end Quantitative Easing. On Thursday, we’ll get the latest report on Consumer Inflation. I expect to see more evidence that the strong dollar is holding back prices. We’ll also get earnings reports from Medtronic and Ross Stores. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – August 22, 2014

Eddy Elfenbein, August 22nd, 2014 at 7:12 am“There is a danger of expecting the results of the future

to be predicted from the past.” – John Maynard KeynesLadies and gentlemen, I have a very important announcement to make: the Summer Swoon is officially over!

Yep, it’s true. From July 24 to August 7, the S&P 500 shed 3.94%. The market’s low came right as the Dow barely touched its 200-day moving average. But since then, the market has rallied impressively. In two weeks, U.S. equities have gained more than $900 billion in value. The S&P 500 has closed higher in eight of the last ten sessions. On Thursday, the index closed at 1,992.37, which is its highest all-time close. Believe it or not, we’re now within striking distance of 2,000.

Think about this: The stock market has nearly tripled in less than five and a half years. That’s simply amazing. As long-time followers know, our Buy List has done even better.

We’ve had more good news for our Buy List this week. Ross Stores, the deep discounter, just did our favorite two-step—the beat-and-raise polka. Medtronic, the large-cap medical devices company, beat earnings as well. Finally, on Thursday, eBay broke out with a 5% gain on news that it might spin off its PayPal unit. I’ll have full details later on.

We’ve also had some more promising general economic news. The Commerce Department said that housing starts were up sharply last month, and last week’s report on Industrial Production was also quite good. Some folks at the Fed are even talking about raising rates sooner than expected (I doubt it will happen). I want to be careful to put this in proper perspective, though. There are signs that the economy is improving, but we’re still far from healthy. I’ll run down the economic outlook in just a bit, and I’ll highlight what Buy List stocks look especially good right now. But first, let’s look at two big shifts that have been quietly underway on Wall Street.

The Shift Toward Large-Caps and Growth

The Summer Swoon caught a lot of folks off guard. Investors need to understand that summertime investing can be weirdly interesting because a lot of Wall Street bigwigs head off to the Hamptons or Martha’s Vineyard. As a result, trading volume drops off, and smaller events can have an outsized impact.

To boil it down, the market was tripped up by “headline risk,” which refers to political events not related to the market. Every night we’ve seen troubling stories about conflicts in places like Ukraine, Syria and Gaza. Naturally, this has scared investors, especially since volatility had been so low during the spring. I’ve mentioned this statistic before, but it bears repeating: The S&P 500 went 62 days in a row without a single close greater or less than 1%. The market hadn’t had a streak that long in nearly 20 years.

But what’s caught my eye now is that this rally has been a party for the big boys. Large-cap stocks are outperforming, and the smaller guys are lagging behind. While the large-cap S&P 500 finally topped its high from July 3, the small-cap Russell 2000 is still lagging at 4% below its July high. In fact, the Russell 2000 reached its all-time high close on March 4. On July 3, the Russell ran up to its previous high, falling short by just 0.5 points. Technical analysts are always on the lookout for “failures” like this, as they may portend more bad news. Since March 4, the S&P 500 is up more than 6%, while the Russell is down 4%. That’s a surprisingly wide gap between the two indexes.

Large-caps aren’t the only favored sector. Growth stocks are also doing well. This is a big change from the spring. In March and early April, the stock market turned sharply against Growth stocks in favor of Value. But since April 11, the Vanguard Growth ETF ($VUG) is up by 12.5%, and the relative performance of Growth has gotten even stronger lately.

What do these two market shifts, large-cap and growth, mean for the market? It’s hard to say exactly, but I think they reflect greater confidence in the economy. When people get scared, they turn to Value, so the newfound love for Growth probably reflects investor optimism. The last GDP report was certainly encouraging, and it bolsters the view that the economy is improving. Another bit of evidence was last Friday’s Industrial Production report. In July, Industrial Production rose by 4%. That’s twice the rate that economists were expecting. Industrial Production is up 5% in the last year.

The turn to large-caps is a bit more complicated. The big difference between large- and small-cap indexes is that large-cap stocks tend to get more of their revenue from overseas. The smaller stocks are skewed towards domestic manufactures. As a result, the large-cap surge could reflect more optimism about Europe and other foreign markets. For example, Ford Motor ($F) recently turned a profit from their European operations, which was earlier than expected.

The U.S. dollar is also improving against many currencies (bond yields in Europe are crazy low). A stronger dollar is typically correlated with large-caps outperforming small-caps. This makes sense since a stronger currency has a tendency to impede smaller domestic manufacturers.

The positive economic news is clearly influencing the Federal Reserve. On Wednesday, the Fed released the minutes from their July meeting. The minutes suggested that some Fed members are beginning to think that interest rates may have to go up sooner than expected. I’m skeptical. Of course, looking at the minutes from any Fed meeting is an extended exercise in indefinite adjectives; “some” members say this, while “many” members say that. We never know exactly how many members feel a certain way on a given issue.

I suspect the majority on the FOMC is in favor of letting short-term rates ride for several more months. Earlier this week, we learned that inflation continues to be very subdued. The CPI rose by just 0.1% in July. That’s the lowest rate in five months. There are few things that scare central bankers more than inflation, so this news gives the Fed a little more breathing room to keep rates low. For its part, the bond market is still holding up. The 10-year yield recently closed at its lowest level in 15 months. Until there’s more evidence of inflation, Janet Yellen and her friends at the Fed are quite content to keep rates near the floor. This is good for the economy, the stock market and Growth-oriented stocks. Now let’s turn to some of our recent earnings reports.

Medtronic Beats by a Penny

On Tuesday, Medtronic ($MDT) reported fiscal Q1 earnings of 93 cents per share. That was one penny better than expectations. Quarterly revenues rose 4.7% to $4.27 billion, which was $20 million better than expectations. Medtronic had its strongest growth for U.S. medical devices in five years.

I was pleased to hear the company reaffirm its commitment to the Covidien deal. Medtronic also stood by its full-year earnings guidance range of $4.00 to $4.15 per share. I like this company a lot, but I’m going to keep our Buy Below at $67 per share, which is fairly tight. At the current price, MDT is going for less than 16 times this year’s estimate. Medtronic is an ideal stock for conservative investors.

Ross Stores Is a Buy up to $77 per Share

After the closing bell on Thursday, Ross Stores ($ROST) reported very good numbers for their fiscal Q2. For May, June and July, the deep discounter earned $1.14 per share. That was six cents better than Wall Street’s consensus. It was also well above Ross’s own guidance of $1.05 to $1.09 per share. I should add that Ross tends to be fairly conservative with its guidance. Quarterly revenue rose by 7%, which was also better than expectations.

The results from Ross tell us that consumers are willing to spend money if they see good deals. I was very pleased to see the company’s operating margins rise to a company record. In the earnings report, Ross gave us earnings guidance for Q3 and Q4. For the current quarter, they see earnings ranging between 83 and 87 cents per share. The Street was at 86 cents. For Q4, they project earnings between $1.05 and $1.09 per share. Wall Street was at $1.12 per share. Bear in mind that Q4 is a biggie for a retailer like Ross.

Ross’s CEO said, “Our second-quarter sales performed at the high end of our expectations as today’s value-focused consumers continued to respond to our wide assortment of competitive name-brand bargains. Merchandise gross margin was above plan, which, coupled with strong expense controls, enabled us to deliver quarterly earnings per share that were above the high end of our guidance.”

Ross raised guidance for the entire year. Previously, they said they expected earnings to range between $4.09 and $4.21 per share. Now they see earnings coming in between $4.18 and $4.26 per share. Last week, I said that I wanted to see better guidance from Ross before I would touch the Buy Below price. Well, we got our evidence and business is going well. I’m raising our Buy Below on Ross Stores to $77 per share.

Will eBay Ditch PayPal?

Shares of eBay ($EBAY) spiked upward on Thursday on rumors that the company is considering spinning off its PayPal subsidiary. If you recall, Carl Icahn had been pressuring eBay earlier to make such a move. The company repeatedly shot down the idea, but PayPal makes a lot of money, and it could be very lucrative for eBay to let them go.

On Thursday, the online magazine “The Information” said that eBay has been telling prospective candidates for PayPal’s new CEO that a spinoff could be in the works. Honestly, that doesn’t strike me as that big of a deal. It seems quite natural that the spinoff topic would be addressed in a job interview. That doesn’t mean it will happen. Publicly, I expect eBay will still speak out against any spin-off.

What’s more interesting to me is how strongly the market reacted to the idea. The market clearly wants PayPal spun off, and that will cause shareholders to pressure the board to make a deal happen. I’ve been following stocks long enough to know that if a board of directors thought wearing clown shoes would help their stock, they’d do it before sunrise. Look for a deal to happen at some point, but it may take time. In the meantime, I’m raising our Buy Below on eBay to $58 per share.

Before I go, let me highlight a few Buy List stocks that look especially good right now. I really like Ford Motor ($F). I think the automaker will make another run at $18 very soon. Cognizant Technology Solutions ($CTSH) is also a very good buy if you’re able to get it below $47 per share. Shares of Qualcomm ($QCOM) pulled back sharply after the last earnings report. It’s coming back quickly, and I think that trend will continue. My Buy Below for QCOM is $79, but if you can pick up shares below $77, then you got a good deal.

That’s all for now. Next week is the final trading week for August. The year is nearly two-thirds over. The next big econ report will come on Thursday when the government revises the Q2 GDP report. The initial report came in at 4%, which surprised a lot of people. Not many folks had been expecting such a strong number. Now we have some more trade data, so the updated figure could be different. On Friday, we’ll get the report for Personal Income. This is usually a reliable metric for how well the overall economy us doing. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – May 16, 2014

Eddy Elfenbein, May 16th, 2014 at 7:09 am“If you would know the value of money, go and try to borrow some.”

– Benjamin FranklinOn Monday, for the first time in history, the S&P 500 cracked 1,900. The Dow Jones Industrials also reached an all-time record high. But what’s surprising, and perhaps a little disconcerting, is that the bond market is rallying as well. In fact, the bond market has been doing even better than the stock market. On Thursday, the yield on the 10-year Treasury dipped below 2.5% to hit a six-month low (see the chart below).

These twin rallies seem to be the result of dueling hypotheses. If the stock market is rallying, that should mean that the economy is improving. At least, that’s the conventional wisdom. And when the bond market rallies, that’s often the omen of a recession. So what’s going on here?

In this week’s CWS Market Review, I’ll delve into the numbers and try to untangle the market’s bipolar disorder. I’ll also tell you what to do now to take advantage of this confusing market. We’ll also look at the latest from DirecTV. Up until now, there was a lot of chatter about a possible deal with AT&T. Now a deal is a very real possibility, and it may happen soon.

This week’s bad news was a sluggish outlook from Buy List member CA Technologies. I’ll have all the details in a bit. Plus, I’ll preview next week’s earnings reports from dividend champs Medtronic and Ross Stores. But first, let’s look at the market’s mixed message.

Why Stocks and Bonds Are Rallying Together

Wall Street seems terribly confused that stocks and bonds are rallying at the same time. For so long, we’ve assumed that they must always move in opposite directions. But that’s not necessarily the case.

While stocks and bonds have often been polar opposites, that usually reflects diverging opinions on the economy. Now, however, I think they’re both rallying, but for different reasons.

The stock market is easy. It’s up because investors see the economy doing well. Even though the GDP numbers for Q1 were pretty bad, a lot of the big banks on Wall Street think that growth for Q2 will come in over 3%. Maybe even higher.

The jobs market also continues to improve. There are still a lot of people out there looking for work, and the long-term unemployed figures are frustratingly high. But just this week, we learned that initial jobless claims dropped down to 297,000. That’s the lowest number in seven years. The jobs report for April was quite good. In 89 days (Feb/Mar/Apr), the U.S. economy created 713,000 new jobs.

Earnings aren’t bad either. For the first-quarter earnings season, 76% of the companies in the S&P 500 beat earnings expectations, while 53% beat sales expectations. What’s really telling for me is that cyclical stocks continue to do well. The Morgan Stanley Cyclical Index ($CYC) has outpaced the S&P 500 this year. The market’s recent pain has been centered on high-profile momentum stocks, but areas like Materials and Energy, the sectors most sensitive to the economy, have largely side-stepped the damage.

In any market, it’s interesting to see where the current “axis” is. By that I mean that to look at the stocks that are the best or worst performers each day. Sometimes the split is between growth and value, or risk and safety. Lately, the big split is between large-cap and small-cap. That’s most likely a reflection of the currency market. Larger firms to be more internationally focused while smaller firms are more domestically oriented.

This makes sense because outside of the U.S., the eurozone and Britain have been getting back on their feet. What’s interesting is that they’ve been helped by money running away from emerging markets. The euro recently hit a two-year high while the British pound touched a five-year high. Meanwhile, Janet Yellen and Fed have made it clear that interest rates need to stay low well after all the bond buying is done.

The bond market is also being helped by Uncle Sam’s improved finances. There’s still a lot of red ink, but not nearly as much as before. The Congressional Budget Office now sees this year’s budget deficit coming in at a “mere” $492 billion. As big as that sounds, it’s the smallest by far in recent years. The smaller the deficit, the less borrowing there is. This year’s deficit is projected to be 2.8% of GDP which would be the fifth-straight reduction. It would also be less than the average deficit of the last 40 years.

So these two rallies aren’t really a contradiction. Instead, the fight for capital has changed. Stock investors see an improved job market and more consumers. Bond investors see improved government finances and less borrowing. As long as short-term rates are low, the rational choice is to be invested in a diversified portfolio of high-quality stocks like our Buy List.

CA Technologies Is a Buy up to $32 per Share

On Thursday morning, CA Technologies ($CA) became our final Buy List stock to report earnings this season. For March, which ended their fiscal Q4, CA earned 61 cents per share. The good news is that this was three cents better than estimates. Their full-year forecast implied a range for Q4 of 57 to 64 cents per share.

The bad news is that for the coming fiscal year, ending next March, CA gave us a range of $2.45 to $2.52 per share. That was below the Street’s estimate of $2.54 per share. Traders didn’t like that news at all, and the shares tanked 3.4% on Thursday, to close at $29.05. Frankly, I find that reaction pretty puzzling. While the guidance is indeed lower than expectations, that should be seen within the context of CA’s beating expectations by a roughly similar amount. Perhaps some traders just wanted out.

Around here, we like to put our emotions aside and look at the numbers. Going by Thursday’s closing price, CA yields more than 3.4%, and the stock is going for about 12 times this year’s earnings. The company also said it’s going to buy back $1 billion worth of stock. CA isn’t a fast-growing company, but it has its strengths. I still like this stock, but I’m dropping our Buy Below down to $32 per share to reflect the recent selloff. Don’t let this guidance scare you. These quiet stocks have a way of pulling through.

AT&T Could Buy DirecTV within Two Weeks

Now let’s get to the fun stuff. In the last two issues of CWS Market Review, I’ve discussed the possibility of AT&T ($T) buying DirecTV ($DTV). There have been a lot of rumors about this, and the rumors gradually became whispers, and then the whispers became speculation. Now the speculation is officially news.

After the closing bell on Monday, the Wall Street Journal reported that a DTV/AT&T deal could come within two weeks. They’re talking about a price somewhere in the low- to mid-90s for DTV. The deal will probably be a mix of cash and stock.

I know this is exciting to see someone ready to buy out one of our stocks, but let me remind you that no deal has been made. Deals fall apart all the time. There are still financing and regulatory issues, plus the possibility of shareholder objections. I’m not saying any of these will happen, but I’m reminding you that problems can arise.

About the deal. All things being equal, companies would prefer to make acquisitions using their stock. It’s like having a currency you can print for free. Well, almost free. The issue with AT&T is that it pays a generous dividend (5% currently), so issuing more shares means sending out more dividend checks.

If a deal comes about, for track-record purposes, I’ll assume any cash from the deal will go directly into AT&T stock. That way, we’ll still have 20 stocks on our Buy List. AT&T will simply replace DirecTV. As always, I’ll provide complete details when and if this ever happens. Either way, DirecTV remains a very good buy up to $89 per share.

Expect a Small Earnings Beat from Medtronic

We have two Buy List stocks, Medtronic and Ross Stores, that are on the April, July, October, January reporting cycle. Both are due to report next week. Medtronic ($MDT) will report its fiscal fourth-quarter earnings on Tuesday morning, May 20. In February, they hit estimates on the nose. The medical-devices company also gave Q4 guidance of $1.11 to $1.13 per share. Wall Street has chosen the middle and expects $1.12 per share.

Interestingly, Bernstein thinks they’ll slightly beat expectations (but not on the top line). I think that’s probably right. They have a $70 price target. Medtronic has done well for us as it’s rallied in fits and starts over the last two years (see below). Last month, MDT finally surpassed its all-time intra-day high set more than 13 years ago.

I also expect that Medtronic will increase its dividend next month. That’s not much of a prediction on my part, since Medtronic has increased its dividend every year for the last 36 years. Medtronic is a good buy up to $65 per share.

Expect Strong Earnings from Ross Stores

Ross Stores ($ROST) continues to be one of my favorite retailers. They’re due to report earnings after the bell on Thursday, May 22.

At the start of last year’s holiday shopping season, Ross warned investors that business was coming in light. The stock got hit pretty hard, but when the results came in, it really wasn’t that bad. Wall Street had been expecting $1.09 per share. Ross said it would be between 97 cents and $1.01 per share. Ultimately, they made $1.02 per share. That’s really a microcosm of the last earnings season: companies warned that profits would be below expectations, then beat those lowered expectations.

Make no mistake, Ross is still doing quite well. For all of 2013, Ross earned $3.88 per share, which was a nice increase over the $3.53 from 2012. The fiscal year for 2012 was 53 weeks, which added 10 cents per share to that year’s earnings.

The best news was that Ross recently bumped up their dividend by 17.6%. The quarterly payout rose from 17 to 20 cents per share. That marked the 20th year in a row that Ross has increased its dividend. Not many retailers can say that.

For Q1, Ross sees earnings coming in between $1.11 and $1.15 per share. I think they have a very good shot of beating that. For all of 2014, Ross has a range of $4.05 to $4.21 per share. I think they can beat that as well, but it’s still early. The shares have been trending downward lately and are a very good buy here. Ross Stores remains a buy up to $76 per share.

I want to briefly comment on a few of our other Buy List stocks. McDonald’s ($MCD) has been doing very well lately. The burger giant recently hit a new all-time high. I noticed that UBS raised their price target on MCD from $107 to $120 per share. I’m raising our Buy Below on McDonald’s to $106 per share.

I want to reiterate what I said last week about Bed Bath & Beyond ($BBBY) being an outstanding buy. The home-furnishings store will report earnings again in another month, and I’m expecting good news. BBBY remains a very good buy below $66 per share.

While the rest of the market was getting hit hard on Thursday, shares of Oracle ($ORCL) rallied to a new 14-year high. This one took a while to pay off for us, but the shares are up more than 40% from last summer’s low. Once again, we see that being patient is a very good strategy. The only downside is, it takes time. Oracle is a solid buy up to $44 per share.

That’s all for now. There won’t be a newsletter next week. I’m going to get an early jump on the Memorial Day weekend. Don’t worry. I’ll cover our two Buy List earnings reports on the blog. Also, on Wednesday, the Fed will release the minutes from their last meeting. Expect traders to carefully scrutinize it for any clues about when interest rates will rise. I’ll be back in two weeks with more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – February 28, 2014

Eddy Elfenbein, February 28th, 2014 at 7:47 am“A bull market is like sex. It feels best just before it ends.” – Barton Biggs

The fourth time’s a charm! For three days in a row, the S&P 500 rallied above 1,850 and was ready to make a new all-time record close, but each time, the bears arrived late in the day to pull us back down. On Thursday, it looked like it was going to happen for a fourth time, but this time, the bulls prevailed, and the S&P 500 closed at 1,854.29—a new record close.

We’re coming up on the fifth anniversary of a generational low for stocks. The climate back then was dreadful. On Friday, March 6, 2009, the Labor Department reported that the unemployment rate had hit a 25-year high and the economy had lost a staggering 651,000 non-farm payroll jobs the previous month. That morning, the S&P 500 touched an evil-sounding intra-day low of 666.79, which was the index’s lowest point in more than 12 years. The Dow was in even worse shape. Adjusted for inflation, the Dow was back to where it had been 43 years before.

The closing low came the following Monday, March 9, when the S&P 500 finished at 676.53. That was nine years to the day after the Nasdaq Composite first closed above 5,000. Now it was roughly one-quarter of that. The following day, Ben Bernanke told the Council on Foreign Relations that he thought we should review our mark-to-market accounting rules, and a few weeks later, the FASB agreed. That gave a huge boost to the rally. Five years on, the S&P 500 has gained 174%. Including dividends, it’s up 205%. In plainer terms, investors have tripled their money in five years. This is one of the greatest rallies in Wall Street history.

So where do we go from here? In this week’s CWS Market Review, we’ll take a look at the economy and how it could impact our portfolios. I’ll also highlight some good news from our Buy List. An entertaining battle of billionaires is helping our position at eBay. The stock just touched an all-time high. Also, Ross Stores just announced that it’s raising its dividend by 17%. This is the 20th year in a row that Ross has increased its payout. Not many stocks can make that claim. But before we get to that, let’s look at some recent economic news and what it means for us.

Why the Housing Market Holds the Key

On Thursday, new Federal Reserve chair Janet Yellen told Congress that it’s possible the Fed would hold off on its tapering plans if there were a “significant change” in the economic outlook. Frankly, that’s not really news; the Fed has consistently held this line. But this time, investors are taking it more seriously since the economic news has been less favorable. Eric Rosengren, the president of the Boston Fed, who incidentally was the only FOMC member in favor of cutting rates in September 2008, said the Fed should be “very patient” in cutting stimulus. Lousy weather has been a convenient scapegoat for poor numbers, but it’s pretty hard to separate out what’s been caused by the weather and what hasn’t.

On Thursday, the Commerce Department said that orders for durable goods fell 1% last month. But on closer inspection, there were bits of good news in this report. If you exclude transportation, which can be very volatile, durable-goods orders actually rose 1.1% last month. That was the biggest increase since May. Economists were expecting a decline of 0.3%.

On Wednesday, the Census Bureau said that new-home sales rose to a five-year high. The housing situation is critical in determining where the economy goes from here. Even though new-home sales are up, the current level is still near the low point of previous cycles. That tells you just how crazy the housing boom was. It created a massive, gigantic oversupply of homes. All those empty homes weren’t incinerated. Instead, it’s taken us this long to work off the inventory. Only now is housing inventory back to normal.

This is why I’m optimistic on housing. We’ve finally burned off that excessive inventory, and people are going to need more new homes. Normally, housing leads a recovery, and we didn’t get that this time. As a result, we got a sluggish recovery—and for many folks, there was no recovery at all. In fact, I think we could have very easily dropped back into a recession in 2011-12 if not for the assistance of the Federal Reserve. Budget-cutting from the government was a major drag on the economy. (Please note I’m not saying whether I approve of this or not, just that government austerity was a big factor.)

It’s true that mortgage rates have risen. The average rate for a 30-year fixed mortgage jumped from 3.35% last May to 4.33% now. While higher mortgage rates have crushed the refi market (Wells Fargo just announced more layoffs in their mortgage unit), they don’t appear to be holding back new buyers. The simple fact is that we’ll need more new homes. Despite the poor weather, the economy is slowly gaining steam. That’s why I strongly doubt we’ll see the Fed shelve its tapering plans this year.

Let me also touch on the consumer end of the economy. Retail stocks got off to a terrible start this year. That was reflected on our Buy List with bad performances from Ross Stores and Bed Bath & Beyond, but they weren’t alone. Nearly everyone from Walmart on down had a lousy quarter. The retail sector came back to life this week; even troubled retailers like J.C. Penney and Target saw big gains this week.

I suspect that the bad times for retailers have passed. The facts are clear. Consumers have paid down their debts. The great enemy of consumer spending, the price at the pump, is below its average of the last three years. Lastly, the labor market has improved, though at a very leisurely rate.

The Perils of Complacency

One of the concerns I have is the unintended consequences of the Federal Reserve’s policies. No matter how you feel about QE, and I do think it’s been a plus for stocks, massive bond buying distorts the market’s gauging of risk and reward. In short, the Fed has encouraged more risk-taking. That was understandable when everyone was terrified, but what about now?

I’ll give you an example of some possible distortions we’re seeing. Since February 3, the most-shorted stocks, meaning those with the most bets against them, have done the best. The hated stocks have doubled the return of the rest of the market. Tesla is a perfect example. Shorts make up an astounding 37% of their shares, yet the stock has skyrocketed. Shares of Tesla got to $265 this week; a year ago, they were at $35.

Another example is in the biotech sector. In the last ten weeks, the biotech index is up 25%, yet one-third of the companies don’t turn a profit. Facebook broke $71 per share this week, which is more than 90 times last year’s earnings. Some folks are claiming that the rash of big-ticket M&A deals is due to non-existent returns from sitting on cash. Also, everyone’s favorite alternative asset, gold, is having a good year so far (after a very rough 2013). Or we can look at the bond market. The yield spread between junk debt and Treasuries narrowed to its lowest level in six years (see below).

These are all signals that investors are willing to shoulder more risk. On one hand, that’s a good thing. The danger comes when investors become complacent and feel they have little reason to worry. Consider that investors have become programmed to buy every dip. Since the bull market began five years ago, there have been 19 nervous breakdowns of 5% or more. Every single one was turned back.

The problem with risk is the things we don’t know we don’t know. Let’s look at what’s been happening in China’s economy. The growth of their “shadow banking” system has been alarming. No one truly knows its size. What if there’s a major default in China and that ignites a panic? What’s interesting is that growth from China has helped ease our pain from the Great Recession.

I don’t have a specific worry that I see looming on the horizon. Rather, it’s that I see investors becoming sloppy. I’m not so concerned about a large-scale bubble; I worry about small things like poorly thought-out acquisitions. (Peter Lynch has referred to this as the “Bladder Theory” of corporate finance.) The key for investors is not to be tempted by easy gains or to feel the need to chase stocks for fear of being left behind. Frustrated investors are bad investors. Now let’s look at a long-term strategy that works.

Our Buy List Is up for the Year

I’m happy to report that our Buy List is up slightly for the year, and we’re leading the market. Of course, it’s still very early, but through Thursday, our Buy List is up 0.45% this year, while the S&P 500 is up 0.32% (not including dividends). Bear in mind that only a few weeks ago, we were down nearly 6%. Our Buy List has beaten the S&P 500 for the last seven years in a row. Now let’s look at some recent news from our Buy List stocks.

Just after I sent you last week’s CWS Market Review, Express Scripts ($ESRX) had a rough day on the market. Shares of ESRX dropped 4% last Friday. This was despite reporting earnings that were in line with estimates, and they offered a good guidance for this year. I’m a little baffled by the market’s sour reaction, as there was little in this report that anyone should find surprising. The company said it’s aiming to return 50% of its cash flow to investors as dividends or buybacks. I still like Express Scripts and think it’s a good buy up to $83 per share.

Shares of eBay ($EBAY) had a good week, and we have our friend Carl Icahn to thank. The multi-gazillionaire released three open letters this week. In them, he’s reiterating his call for eBay to spin off their very lucrative PayPal business. The company has made it abundantly clear that they’re not interested.

The battle between Icahn and eBay’s board is getting ugly. Icahn doesn’t like the fact that Scott Cook and Marc Andreessen are on the board. Cook founded Intuit which competes against PayPal, and Andreessen’s company bought Skype from eBay and then sold it to Microsoft.

Pierre Omidyar, eBay’s chairman and founder, shot back and said that Icahn’s views are “false and misleading.” I love it when billionaires fight, especially when it helps our stock. Thanks to the high-profile kerfuffle, shares of eBay rallied above $59 on Thursday and took out the all-time high from 2004. Now Icahn has challenged eBay to a public debate, which sounds a bit nutty. The irony is that ever since Icahn went on the warpath, Omidyar has made $450 million from the eBay rally. My take: I think it’s clear that the board isn’t going to budge. Meanwhile, I’m raising my Buy Below on eBay to $62 per share.

This is actually a lull period for Buy List earnings reports. Our only earnings report for the next several weeks will be Oracle ($ORCL), which should report sometime in mid-March. I’m expecting another good report from them. Oracle tested our patience last year, but I think it’s starting to pay off. For Q3, Oracle sees earnings coming in between 68 and 72 cents per share. On Thursday, the shares broke above $39 for the first time since Bill Clinton was president. Oracle remains a very good buy up to $41 per share.

Ross Stores Announces Big Dividend Increase

After the closing bell on Thursday, Ross Stores ($ROST) reported Q4 earnings of $1.02 per share. This is for the crucial holiday shopping quarter. In November, the deep-discount retailer spooked Wall Street when it said that Q4 earnings would be below forecasts. The Street had been expecting $1.09 per share; Ross said to expect between 97 cents and $1.01 per share.

Overall, Ross is doing quite well. For the entire year, Ross earned $3.88 per share which was a nice increase over the $3.53 from 2012. The fiscal year for 2012 was 53 weeks which added 10 cents per share to that year’s earnings.

Michael Balmuth, Ross’s CEO, said, ”Our fourth-quarter sales performed in line with our guidance, with earnings that were slightly better than expected, primarily due to above-plan merchandise gross margin. Despite a very promotional retail environment throughout the holiday season, customers responded favorably to the compelling bargains we offered on a wide assortment of fresh and exciting name-brand fashions and gifts.”

Now for some guidance. For Q1, Ross sees earnings coming in between $1.11 and $1.15 per share. Wall Street had been expecting $1.20. For all of 2014, Ross sees a range of $4.05 to $4.21 per share. The Street was at $4.34 per share. That’s a disappointing forecast, and the shares were weak in the after-hours market.

But there is good news. Ross announced a 17.6% dividend increase. The quarterly payout will rise from 17 cents to 20 cents per share. This is Ross’s 20th year in a row of raising its dividend. At 80 cents per share for the full year, that works out to a yield of 1.1%. I’m raising my Buy Below on Ross to $76 per share.

That’s all for now. Next week, we get several important economic reports. On Monday, the ISM report comes out. Last month’s report was surprisingly weak, so it will be interesting to see if this was a temporary move or the start of a larger trend. The Fed’s Beige Book comes out on Wednesday, followed by the productivity report on Thursday. Then on Friday is the big jobs report for February. The last two jobs reports were noticeably subdued, and it appears that the weather excuse has outlived its welcome. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – August 23, 2013

Eddy Elfenbein, August 23rd, 2013 at 7:13 am“To achieve satisfactory investment results is easier than most people realize;

to achieve superior results is harder than it looks.” – Benjamin GrahamWall Street’s been having a tough time so far this August. Through Wednesday, the S&P 500 fell on ten of the previous 13 days. Thanks to the low volatility of late summer, these dips haven’t stung very much. Measuring from the market’s peak on August 2, the index lost nearly 4%, though we gained some of that back on Thursday. Interestingly, the Dow Industrials fell to their lowest level relative to the S&P 500 in five years.

Now a 4% haircut isn’t much of a downswing. It’s only a minor dent in the rally we’ve had this year. However, the big concern on everyone’s mind is that Ben Bernanke and his friends at the Fed are finally going to start “tapering” their bond purchases next month. I’ll have more on that in a bit. Wall Street had more headaches yesterday as “technical issues” caused trading to be halted on the Nasdaq for three hours.

But the action that’s caught my attention hasn’t been in the stock market. It’s in the bond market. Interest rates have spiked dramatically in the U.S., and the long bond is near its worst selloff in 13 years. In early May, the 10-year Treasury was yielding 1.63% (see chart below). On Thursday, the yield got as high as 2.92%, and a lot of folks expect us to break 3% any day now.

In this week’s CWS Market Review, we’ll take a closer look at what’s causing bond traders so much grief. We’ll also take a look at recent Buy List earnings reports from Medtronic ($MDT) and Ross Stores ($ROST). (Ross beat consensus by five cents per share and looks to break out soon.) But first, let’s focus on the dramatic rise in bond yields.

Why Are Rates Rising? It’s the Economy

The stock and bond markets have a rather unusual relationship. The two markets can basically be described as “frenemies.” On one level, they’re competitors for investors’ capital. Money will go wherever it’s treated best. The catch is that neither market will prosper for long if the other one is suffering. After all, the bond market is debt, and if companies have to shell out higher interest costs, that will cut into their bottom line. Meanwhile, if companies aren’t making a profit, then they can’t pay back their loans. Stocks and bonds are rivals under the same flag.

Sometimes the two markets move together as if they’re waltzing partners, and other times they act in near-perfect opposition. As a very general rule of thumb, the bond market leads the stock market by about six months to a year.

Long-term interest rates officially hit their low thirteen months ago, but the decline since then was rather slight. That is, until this May, when the rout really got going. The 10-year yield is now where the 20-year yield was in June, and where the 30-year yield was in May. So the question to ask is, why is the bond market falling so sharply?

The popular answer is that it’s due to the Federal Reserve pulling out of its bond buying. But I’m not so sure. Let’s review the situation: The Fed meets again in mid-September, and the central bank has successfully convinced Wall Street to expect a scaling-back of asset purchases. This week, in fact, the Fed released the minutes of its last meeting, and those minutes indicated that the other FOMC members are on board with Bernanke’s tapering plan. Personally, I think it’s too early to start tapering. If they do announce a tapering, and they probably will, I expect it to be modest, which means the Fed hasn’t left the bond market at all: they’re simply buying less. This really shouldn’t be a big deal.

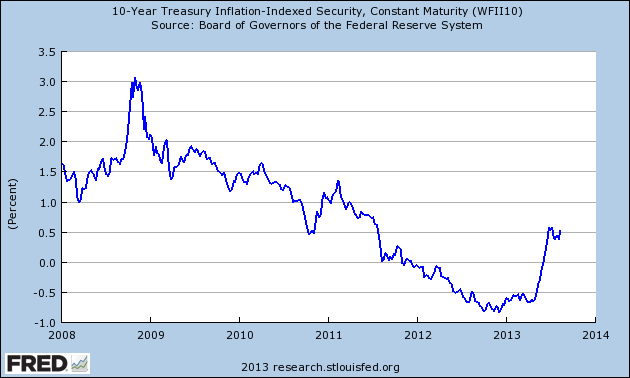

That’s why I don’t believe the taper talk is the reason for higher interest rates. Other people think the higher rates are due to inflation. The gold market has rebounded lately, but that’s coming after a pretty rough year. The yellow metal is still off more than $500 an ounce since last year’s high. The CPI reports continue to be quite tame. Also, the yield on the 10-year TIPs, the inflation-protected bonds, has climbed largely in step with the regular 10-year bond (see chart below). In other words, investors aren’t demanding a greater inflation discount for their bonds. They just want a higher yield.

The influence of the Fed does show up in the middle part of the yield curve. For example, the spread between the two- and three-year Treasuries was only 10 basis points on May 6. Now it’s up to 40 points. That’s probably investors factoring in a short-term rate increase down the road. Interestingly, spreads among longer-dated bonds have actually tightened up a bit.

This leads me to believe that the reason for the higher rates is an improving economy. The key fact in favor of this thesis is that the dollar has been fairly stable. If yields were rising as the dollar was falling, then I’d be more concerned. I’ve also been impressed by how economically cyclical stocks have held up, and that’s despite a weak market for tech stocks. We also got encouraging earnings reports this week from broad-based retailers like Best Buy ($BBY) and TJX ($TJX). Also, Home Depot ($HD) had a good report plus they raised guidance.

The most intriguing bit of evidence in favor of the stronger-economy view is that junk-bond spreads have narrowed. In an unusual twist, AA-rated bonds are now yielding less than AAA bonds. But that’s not due to the market’s irrationality (which we can never completely discount). Rather, it’s due to the fact that investors want the shorter maturities that AA bonds usually carry. So investors want still bonds; they’re simply less willing to get locked into long positions.

Mortgage rates have climbed as well, and I am concerned that that could disrupt the housing market. The recent reports, however, show that housing is doing quite well. Our Buy List member Wells Fargo ($WFC) made news this week when they announced they’re eliminating 2,300 mortgage jobs. But that’s due to a decline in refinancings, not fewer originations.

The takeaway for investors is to not be too concerned about any taper talk. Its influence on the market is easily overstated. If bond traders are right, the economy is due for a rebound later this year and into 2014. That will be very good for our Buy List. Now let’s turn to our recent earnings reports.

Medtronic Hits Earnings Consensus on the Nose

On Tuesday, Medtronic ($MDT) reported fiscal first-quarter earnings of 88 cents per share, which was in line with expectations. Revenues rose to $4.08 billion, which was $40 million short of estimates.

Shares of Medtronic pulled back after the earnings report, but I think it was a fine quarter. Demand for defibrillators was a bit weak, as was the demand for MDT’s InFuse bone-growth product. Interestingly, Medtronic said they’re planning to expand beyond medical devices and into health services. I think that’s a smart move.

Medtronic’s CEO, Omar Ishrak, said, “We delivered on the bottom line, overcoming a number of challenges through strong operating discipline.” The best news was that MDT reiterated its full-year forecast of $3.80 to $3.85 per share. That’s for fiscal 2014, which ends next April. They made $3.75 per share last year and $3.46 per share the year before. In June, Medtronic raised its dividend for the 36th year in a row. Business is still going well here, and I think they can easily hit their full-year guidance. Ishrak said they’re looking to generate $25 billion in free cash flow over the next five years. Medtronic remains a solid buy up to $57 per share.

Ross Stores Delivers a Solid Earnings Report

After the close on Thursday, Ross Stores ($ROST) showed very strong fiscal Q2 earnings of 98 cents per share. That was five cents better than Wall Street’s consensus. It was even better than Ross’s own projections. After the last earnings report in May, Ross said to expect Q2 earnings to range between 89 and 93 cents per share.

Quarterly sales rose 9% to $2.551 billion. The important metric for retailers, comparable-store sales, rose 4% last quarter. That’s a very good number. ROST’s CEO, Michael Balmuth, said, “Operating margin for the second quarter grew to a record 13.6%, up from 12.8% in the prior year.” For Q2, Balmuth said he sees earnings coming in between 75 cents and 78 cents per share. That’s below Wall Street’s consensus of 79 cents per share, but Balmuth noted that it’s a cautious outlook.

For Q4, Ross sees earnings ranging between 99 cents and $1.03 per share. Wall Street had been expecting $1.10 per share. The guidance for Q3 and Q4 is based on comparable-store sales growth of 2% to 3%, which is very conservative. Add it all up, and Ross sees full-year earnings of $3.80 to $3.87 per share. Note that last year’s fiscal year included 53 weeks. Adjusting for that, Ross is projecting earnings growth of 11% to 13%.

This was an excellent quarter for Ross. Don’t let the tepid forecast bother you. They’re just being conservative. Ross Stores is an excellent buy up to $70 per share.

Before I go, I want to highlight three especially good buys on our Buy List. Ford ($F) looks very good below $17. The stock actually dipped below $16 earlier this week. The last earnings report was outstanding. Cognizant Technology ($CTSH) is a very good buy if you can get it below $73 per share. The recent earnings report and guidance was also very good. Keeping with tech, Microsoft ($MSFT) is a bargain below $33 per share. The stock currently yields 2.84%, and you can expect a dividend increase next month.

That’s all for now. Next week is the final week of summer. It went by fast, didn’t it? I expect trading activity to remain subdued until after Labor Day. On Monday, the census Bureau will report on durable orders. The report will come on Wednesday, when the government will revise the Q2 GDP growth numbers. The initial report was a sluggish 1.7%, but the subsequent trade numbers suggest a strong upward revision. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – August 16, 2013

Eddy Elfenbein, August 16th, 2013 at 7:14 am“The voice of reason is small, but persistent.” – Sigmund Freud

Youch! Thursday was the worst day for the S&P 500 in nearly two months. By the time the closing bell rang, the index had dropped 1.43% for the day and was back to 1,661.32. Of course, we’re still higher than we were on July 4th. If you take a step back and look at the larger picture, Thursday’s loss was small potatoes. In fact, the most prominent feature of the recent rally is how tame it’s been.

Let’s look at some facts: Morgan Housel notes that 2013 is on track to have the fewest daily swings of 1% or more since 1995. Going by that measure, this year could be the seventh-least-volatile year since 1928.

What’s also interesting is that the stock market rally has been remarkably consistent. The S&P 500 has traded above its 150-day moving average every day for the last eight months. This is the ninth-longest such streak since 1980. In plainer terms, the market has climbed slowly upward almost nonstop since the election. It’s been so placid that this recent break appears more dramatic than the numbers say.

In this issue of CWS Market Review, we’ll take a look at what caused Thursday’s market headache. We’re only five weeks away from the Fed’s September meeting, and more folks on Wall Street think the guardians of the temple will start pulling back on their bond-buying program. We’ll also focus on the upcoming earnings reports from Medtronic ($MDT) and Ross Stores ($ROST). But first, let’s look at why good news for the jobs market is apparently bad news for investors.

Initial Jobless Claims Lowest Since 2007

I’m always suspicious of any pat explanation for why the market does this or that on a given day. Just because some market activity coincides with some bit of news doesn’t mean the news is the cause. Oftentimes, traders are looking for an excuse to do something, and if some event in the larger world vaguely resembles a reason, they’ll take it.

On Thursday morning, we actually got a piece of very good news. The government reported that initial claims for unemployment had dropped to 320,000. This is significant because that’s the lowest reading since October 2007, which was the top of the market.

Any news about the labor market has to be viewed in the context of the Federal Reserve’s plans for later this year. The Fed has already told us that they’re looking to taper their bond purchases at some point, and that will largely be determined by how strong the jobs market is. So traders probably took the good news about yesterday’s jobless claims as evidence that the Fed will begin paring back on their bond purchases.

I’ve said before that I disagree with the view that the stock market will be stranded without the Fed’s help. The Fed is merely discussing pulling back on the level of support they’re giving investors. No one is pulling the rug out from under the market. As a general rule of thumb, investors place far too much emphasis on what the Fed does (I know, this is a screaming heresy to a lot of folks on Wall Street).

I’m also a doubter that the Fed will make any tapering decision at its September 17-18 meeting. I appear to be in the minority on this point. I should also add that my views on what the Fed will do have been pretty off the mark this year. The good news for us is that forecasting what government eggheads will do isn’t a prerequisite for being a good investor.

This leads to an odd situation where good news on the jobs market leads to bad news for investors, because it signals that the end of QE is within sight. The more dramatic response to any shift in Fed policy hasn’t been in the stock market, but in the bond market. On Thursday, the yield on the 10-year Treasury bond topped 2.8% for the first time in two years. The yield has nearly doubled in the last year. More broadly, last summer may have marked the peak of an astonishing 31-year rally for bonds.

The importance of long-term bond yields is that they usually (though not always) coincide with outperformance of cyclical stocks. They’re called cyclical for a reason, and if the cycle is in their favor, they can do very well. Two summers ago, the bond market gave the stock market a world-class beat down, and the cyclicals got hammered hardest of all.

If there’s any evidence against the Fed making a move next month, we got it with two reports this week. The first was a rather lackluster report on retail sales. This is usually a good clue on how strong consumer spending is. It also tells us how well some of our Buy List stocks, like Bed Bath & Beyond ($BBBY) or Ross Stores ($ROST), are doing.

I was also disappointed by this week’s report on industrial production. This is a key data series watched by the people who decide whether there’s a recession or not. Industrial production has been noticeably flat for the past five months. If there’s going to be a second-half pickup, we should see it soon.

As impressive as the market’s rally has been, a lot of it has been based on earnings growth ramping up later this year. As I’ve said, if that’s the case, the stock market is still quite cheap. But if that thesis doesn’t play out, stocks could take a tumble. The Street’s earnings estimates for Q3 have dropped from $30.27 in March 2012 to $27.17 today. The Q4 estimate is down, but not as much, falling from $31.18 in March 2012 to $29.13 today. Analysts now expect the S&P 500 to earn $108.51 this year, and $122.37 next year. As always, I caution against putting too much faith in estimates beyond a few months out.

What to do now: Our strategy is to be focused on high-quality stocks. Our Buy List has had a very good run since April, so we can expect it to catch its breath. Right now, I think Cognizant Technology Solutions ($CTSH) is a solid value. I also think Oracle ($ORCL) looks good below $33 per share. Please don’t get too worried about what the Fed may or may not do. Good companies can do well in any environment. Now let’s look at our Buy List earnings coming next week.

Medtronic Is a Buy up to $57 per Share

Medtronic ($MDT) is due to report its earnings next Tuesday, August 20th. The Street currently expects 88 cents per share. That sounds about right to me. I was very impressed by MDT’s last earnings report in May. The medical-device company topped consensus by seven cents per share.

The big surprise last quarter was that sales of pacemakers and defibrillators rose. Pretty much everyone was expecting more declines. Sales of defibrillators rose by 1.5%, and pacemakers were up by 2.6%. Company-wide, revenues were up by 3.8%. Medtronic’s CEO said that for the first time in four and a half years, sales of defibrillators and spinal products rose in the U.S. in the same quarter.

For their last fiscal year, which ended in April, Medtronic made $3.75 per share, which is up from $3.46 per share for the year before. In May, the company said it sees FY 2014 earnings ranging between $3.80 and $3.85 per share. Last week, MDT came within two cents of hitting $56 per share. The shares have pulled back with the market’s recent slide, but it’s nothing too severe. Remember that a few weeks ago, Medtronic raised its quarterly dividend for the 36th year in a row. Not many companies can say they’ve done that. Medtronic remains a very good buy up to $57 per share.

Ross Stores Is a Buy Below $70 per Share

Ross Stores ($ROST) is due to report earnings next Thursday, August 22nd. Unfortunately, the discount retailer has gotten punished over the last few days. At the beginning of August, ROST was closing in on $70 and threatening to make a new 52-week high. But some bad news for the retail sector, including disappointing earnings from Walmart and a tepid retail-sales report, brought shares of ROST down to $64.89 by the closing bell on Thursday.

Make no mistake, Ross is a very well-run outfit, and I’m not at all worried about its prospects. In May, the company reported fiscal Q1 earnings of $1.07 per share, which matched forecasts. Quarterly sales rose 8% to 2.54 billion, and same-store sales were up 3%.

Ross said that it sees Q2 earnings coming in between 89 and 93 cents per share. The Street foresees 93 cents per share, which may be a penny or two too high. But bear in mind that this is still a pretty nice increase over the 81 cents Ross earned in last year’s Q2. For the entire year, Ross projects earnings between $3.70 and $3.81 per share. Ross Stores is a very good buy up to $70 per share, and it’s especially good if you can get it below $65.

Nicholas Financial Announces Dividend of 12 Cents per Share

On Tuesday, Nicholas Financial ($NICK) said they’d be paying out another 12-cent quarterly dividend. I thought there was a chance they might increase their dividend. I think we may see a two- or three-cent-per-share increase this December, at the time of their shareholder meeting. Going by Thursday’s close, NICK now yields 3.16%.

That’s all for now. Next week will probably be another quiet week on Wall Street. All the big money guys are chillaxing at their cribs in the Hamptons. On Wednesday, the Fed will release the minutes from their last meeting. This might contain clues to what they have planned for their September meeting. Expect folks to read too much into it. We also have earnings reports from Medtronic and Ross Stores. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Ross Stores Earns $1.07 per Share for Q1

Eddy Elfenbein, May 23rd, 2013 at 5:55 pmAfter the closing bell, Ross Stores ($ROST) reported first-quarter earnings of $1.07 per share. That’s up 15% from a year ago. Q1 Sales rose 8% to $2.54 billion. Comparable store sales were up by 3%.