I want to expound on what I said the other day about the use of Price/Earnings Ratios. It works like this, picking stocks (good), timing the market (bad).

I also criticized the idea of using P/E ratios based on ten years’ worth of earnings. Now I want to show you why.

First off, I got this historical data off Robert Shiller’s website which has monthly numbers going back 140 years.

Now I have to explain my analysis carefully, and I have to apologize because it’s not easy to do. Plus, whenever I attempt this, I get dozens of emails asking what the hell I’m talking about. (Note, dear reader, I’m criticizing my articulational abilities, not your comprehensional skillz.)

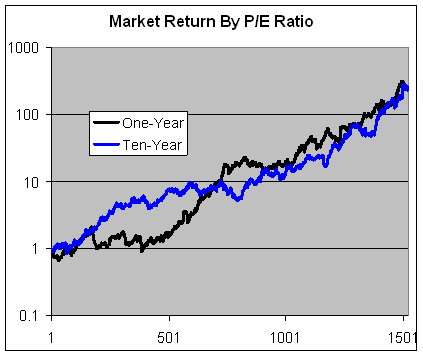

Deep breath. I take all of the monthly data of stock market returns and P/E ratios. I then resort the data, not by time, but this time by P/E ratio, highest to lowest. Then, I calculate all those individual monthly returns. Basically, it’s a stock market graph, not by time, but by declining P/E ratio.

If the P/E ratio has an impact on the market, I would expect the line to droop down early on, then rally frenetically with lower ratios. If the P/E ratio has no impact, then I expect that the line would rise in a smooth diagonal line. Here’s a look at how the 10-year and 1-year P/E Ratios stack up:

As you can see, the 1-year P/E ratio has some impact on market returns, but not much. The market shows a net loss up to the 390th data point which corresponds to a P/E ratio of about 17.8. That means that all over the market’s net gains have come when the P/E Ratio is less than 17.8. According to Shiller’s data, that’s almost the entire time since 1996.

Still, I'm not impressed by the one-year's performance. Compare that to this dramatic graph showing the market's performance ranked by the previous day's gain.

The 10-year P/E has, in my opinion, almost no impact on equity prices. The blue line barely wiggles on its way down the P/E Ratio scale. Knowing what the 10-year ratio was gave you zero input on what stock prices were about to do.

]]>