Archive for August, 2008

-

Citigroup to Cut Costs

Eddy Elfenbein, August 27th, 2008 at 1:20 pmFrom Bloomberg:

Citigroup Inc., the biggest U.S. bank by assets, banned off-site meetings among investment- banking employees and cut back on color photocopying to reduce expenses as revenue declines.

Just to be clear, according to their most recent 10-Q, Citi has assets of $2.1 trillion.

-

The Best Central Banker in the World Today

Eddy Elfenbein, August 27th, 2008 at 11:58 amImagine a country whose central bank responded to growing inflation by raising interest rates, strengthening the currency and trying to win investor confidence. This may be shocking to some U.S. investors, but proper monetary policy is still being practiced. Just not here in the United States. I’d give the award for Best Central Banker in the World Today to Mexico’s Guillermo Ortiz.

This is a story that truly ought to be better known. Mr. Ortiz has now been at the helm of the Mexican central bank for over ten years and despite many obstacles (consider that 70% of Mexicans don’t even use banks), he’s emerged as the anti-Greenspan. Mr. Ortiz previously served Finance Minister where he helped clean up the mess surrounding the peso devaluation in 1994.

What impresses me about Oritz, who earned has a Ph.D. from Stanford, is that he’s made it unequivocally clear that the Banco de Mexico (or Banxico) intends to fight inflation until its wins. In the last three months, the bank has raised rates three times. Interest rates now stand at 8.25%, an amazing 625 basis points higher than in the U.S. even though inflation rates are roughly similar.

Make no mistake; the Mexican economy has its share of problems. Growth is slowing and inflation is on the rise. Of course, much of this is understandable considering their raucous, hung-over neighbors to the north—nearly 80% of Mexico’s exports go to the U.S. Still, my money’s on Ortiz. He’s even had the chutzpah to criticize our monetary policy as being “very lax.” Don’t expect to hear anything like that from Senators McCain or Obama.

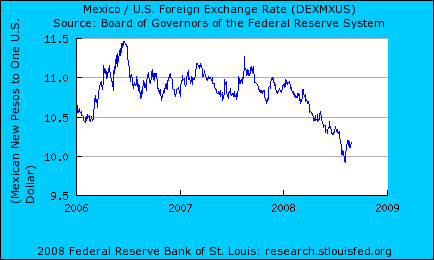

And what about that hopeless currency, the peso? Well, it’s on a roll this year. The peso is already up 7.5% for the year and earlier this month, it reached a six-year high. In my opinion, the rate gap between the U.S. and Mexico will only grow. The futures market seems certain that the Fed will hold steady for the rest of the year, but I think Banxico could very well raise rates again. Their next meeting is on September 19.

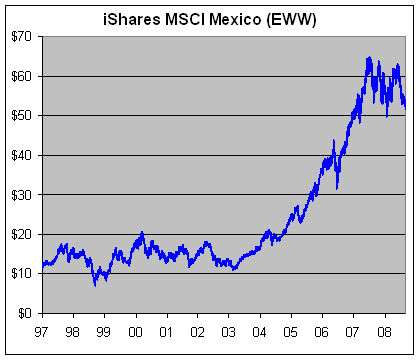

The most recent report for Mexican GDP showed that Q2 growth came in at 2.8%, which isn’t horrible but it was below expectations. The economy isn’t so fragile as to ward off monetary tightening. Retail sales are weak and the stock market is still hurting—the Bolsa is at a seven-month low. Of course, that comes on the heels of an enormous rally so some consolidation would be expected. Consider that shares of EWW, the Mexican ETF, more than quadrupled in five years.

What’s really hurting the economy is that less money is being sent home from workers living abroad. And by abroad, you can probably guess what country I mean. Speaking of which, Ortiz also favors, sit down for this one, stricter immigration controls in the U.S. so Mexico can hold on to its workers. Ortiz said, “I think Mexico needs its people. It would be best to keep its people in Mexico, and it would give incentives for Mexico to create the jobs that are needed.” Increíble!

I’m guessing Ortiz has some sympathy for Hank Paulson. When the Mexican financial system imploded, Ortiz was called into to clean up the mess. Paulson certainly has a tough task, but look at what Ortiz was facing—inflation reached 52% and investment fell by one-fourth. Thing got so bad that the former president basically can’t show his face Mexico and he’s been exiled to Ireland. By contrast, Senor Greenspan now works at Pimco! Thanks to Ortiz, Mexico righted itself and paid back its bailout money to the United States. In fact, Uncle Sam made a half-billion dollar profit.

The thing about finance, public or private, is that it’s really an issue of establishing confidence. If investors think you’re serious, then they’ll invest with you. So far, Ortiz seems to winning the battle of establishing credibility. The yield on Mexico’s long-term benchmark bond recently fell to its lowest level since June 6.

Mexico is a country with many deep rooted economic problems, however, the country has taken many steps in the right direction. For example, the election of the pro-market government of Felipe Calderon (cue Larry Kudlow) is helping to bring long-overdue economic reforms like privatizing the oil industry. Unfortunately, Calderon supports some poorly considered ideas like price controls. Unlike the United States, the Mexican government seems to be serious about fiscal discipline. Their legislature…er, not so much. One issue in particular that Ortiz wants addressed is reducing the government’s fuel subsidies. Good luck with that one, but at least he’s trying. (Incidentally, Ortiz wants to reduce the subsidies even though he thinks that will increase inflation in the near-term.)

The government recently announced that its current account deficit widen to over $2 billion which came as a shock to economists who were expecting a shortfall of $750 million. The trade deficit declined but that was helped by the increase in oil prices. The Mexican economy faces several significant challenges ahead. Most importantly, inflation is simply too high. But I think Ortiz realizes the difficulties and his current policies will help Mexico be well-prepared for the future. -

Looking at China’s Savings

Eddy Elfenbein, August 26th, 2008 at 9:45 amJohn Hempton at Bronte Capital has a novel explanation for China’s stratospheric savings rate. He says it’s due to their one-child policy. In any pre-Industrial economy, you’re retirement savings plan was very simple, you had children. Now you can’t so to compensate, you save, save, save. Hempton’s reckons “that the average Chinese person is saving maybe 46 percent of their income”.

This is an issue for us in the West because, as the theory goes, all that savings needs to be invested somewhere. And there’s simply too much money lying around, sooner or later it will go into dumb areas. Today, we’re at the later part. Hempton writes:My thesis – which will be expanded in future posts is that the brokers have become the intermediaries between this endless demand for products to save in (China, Petrodollars etc) and the endless willingness of the profligate in the West to spend. What they do is – through their trading, their securitisation and through other things they turn the complex financial instruments of the West (mostly but not entirely debt) into vanilla instruments that the Chinese and petrodollars want to buy.

In the Telegraph, Ambrose Evans-Pritchard notes a study by HSBC which claims that China is forcing its banks to buy dollars. In effect, the Chinese Fed is using its banking sector as a way to intervene in the currency markets.

Beijing has raised the reserve requirement for banks five times since March, quickening the pace with two half-point rises in late June.

This is having major spill-over effects into the currency markets because banks in China have been required over the last year to hold extra reserves in dollars rather than yuan. The latest moves have lifted the mandatory deposit from 15pc to 17.5pc of total lending since March.

“China has used the pretext of reserve requirement hikes to help slow yuan appreciation. We estimate that the PBOC [central bank] intervened by about $49.6bn in June,” said Daniel Hui, the bank’s Asia strategist.

Beijing has also slashed the amount of foreign debt banks operating in China can hold. The effect is to oblige the banks to become net buyers of dollars, halting the flow of foreign “hot money”. -

How Investment Banks Can Cut Costs

Eddy Elfenbein, August 26th, 2008 at 9:13 amFrom Andrew Ross Sorkin:

When Wall Street seeks to save money — “every dollar saved is a dollar made,” is the current catchphrase — it often turns to management consultants to help figure out which divisions should stay and which should go.

So McKinsey & Company published a helpful report last week on how investment banks can cut up to $2 billion in noncompensation costs. (We wouldn’t want to cut compensation, would we?)

“Initiatives to curb expenditures need not be extremely demoralizing to frontline employees,” McKinsey says, trying to find ways to save money without affecting the worker bees. So what does it recommend? Getting rid of the consultants. Yep, you read that correctly.Interesting. When Google went public, it tried to cut cost by eliminating the investment banks.

-

Tyler Cowen on the Economy

Eddy Elfenbein, August 25th, 2008 at 10:02 amFrom Saturday’s NYT:

Emerging from the current slowdown isn’t just a matter of political will or smart central banking. If the recipe for success requires smooth adjustment into new growth sectors, more savings from disposable income, cleaning up the housing mess, well-functioning energy markets, and more effective financial intermediation — all in the right combinations and in the right sequences — neither the government nor the Federal Reserve can control this process. The Fed can add regulatory and monetary clarity, but there isn’t any magic bullet. Beware of anyone who tells you there is.

The Japanese failed to break out of their recession quickly because they didn’t promptly close down or clean up their problem banks. So far, the Fed and other regulators show no signs of making this mistake; they have been vigilant in resolving crises as they occur. But that’s not enough to guarantee a successful transition. The American economy will be tested for its deftness — and the test will be difficult precisely because there isn’t a single enemy on which to focus.

HAVE you ever tried to undo a bunch of tangled wires or cords? If you don’t pull on the right wires in the right order, the mess becomes worse. If you pull too hard, the whole thing can break. But if your first pulls are good ones, the untangling becomes easier with each move.

That’s like our economy’s situation today. If we expect too much too quickly, we’ll make matters worse. But there is a way out of the mess, and it lies in our hands.

Be careful, and start pulling. -

Ben Stein Watch

Eddy Elfenbein, August 25th, 2008 at 9:50 amFelix Salmon regularly skewers Ben Stein’s incoherence in each week’s New York Times. (For the record, Stein’s the one who appears in the NYT, Felix writes on his blog). This week, Felix finds this sentence:

They walk in rows of three, each on a cellphone, not even talking to the people next to her.

You truly do not want to know the context. What caught Felix’s eye is that, up until that point, no female had been referenced. The “next to her” just appeared out of nowhere, which leads Felix to conclude that no one at the Times bothers to read his columns.

My take is that there was a previous sentence that had been edited out which had referred to the female, and the following sentence hadn’t been fixed. I have to think that the reason for the deletion and the female reference are related, but I could be wrong. -

Best Line of the Day

Eddy Elfenbein, August 25th, 2008 at 9:46 amPaul Kedrosky finds this gem from a French banker in 1907:

The U.S. is a great financial nuisance.

The Panic of 1907 was pretty ugly for investors. Here’s what I wrote last year on its 100th anniversary.

-

The Weekend Is Here

Eddy Elfenbein, August 22nd, 2008 at 5:27 pm -

Gas Prices Around the World

Eddy Elfenbein, August 22nd, 2008 at 1:46 pmHere’s a cool map looking at gasoline prices around the world. I’m glad I don’t live in Turkey ($11.17/gallon). On the other hand, I’m not about to move to Venezuela ($0.12 a gallon) either.

-

Defending Shorts

Eddy Elfenbein, August 22nd, 2008 at 11:42 amDoug Kass has an excellent article in the FT defending shorts:

Yet short-sellers have served as financial watchdogs, as many of their warnings have been spot on. The delusional dotcom boom in the late 1990s brought Cassandra-like utterings from the short-selling cabal that proved insightful but were largely ignored. After the subsequent 75 per cent collapse of the Nasdaq, a bull market in corporate fraud emerged and short-sellers such as David Rocker, founder of Rocker Partners, highlighted accounting problems at companies such as Sunbeam, Tyco and Lernout & Hauspie. Kynikos’ Jim Chanos played a role in uncovering the largest fraud in history when his contrary-minded analysis warned of Enron’s accounting shenanigans – which were emulated (but ignored by investors) in the banks’ recent dalliance with structured investment vehicles.

Short sellers have done the work that governments won’t and can’t. It’s absurd for governments to limit their opportunities. .

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His