Archive for October, 2016

-

Stock-Picking Strikes Back!

Eddy Elfenbein, October 31st, 2016 at 3:16 pmI wanted to highlight a few bits from this Bloomberg piece. Correlations within the S&P 500 have fallen from very high levels. At the same time, active managers have rebounded relative to their benchmarks.

But while the benchmark gauge churns, stocks within it have gotten more lively. A measure of 30-day realized correlation among S&P 500 constituents has eased 34 percent since reaching a four-year high in October 2015, according to data compiled by Bloomberg.

Active managers have reaped benefits. According to Bank of America Corp., the proportion of large-cap funds beating their benchmarks reached 58 percent in the third quarter, compared with 18 percent in first six months. That marked the best period since the second quarter of 2015, and the second-best since the start of 2009.

Among growth funds, 71 percent exceeded returns on the Russell 1000 Growth Index, while 63 percent of value investors beat their benchmark. It was the most since 2013 for both groups.

(…)

Fund managers are currently holding 5.8 percent of their portfolios in cash, the most since the period after the Sept. 11, 2001, terrorist attacks, according to a survey conducted by Bank of America Corp. The level was matched in July after the U.K. voted to leave the European Union.

-

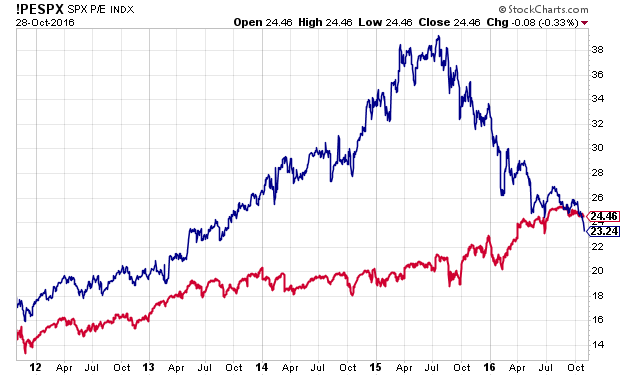

P/E Ratio of Healthcare Stocks

Eddy Elfenbein, October 31st, 2016 at 11:31 amI thought this was a fascinating chart. It shows the P/E Ratio of Healthcare stocks (blue) compared with the P/E Ratio of the S&P 500 (red).

-

Personal Spending Rose 0.5% in September

Eddy Elfenbein, October 31st, 2016 at 11:19 amThis morning, the government reported that personal spending rose 0.5% in September. That’s a pretty good number. Personal income rose by 0.3%. Economists had been expecting increases of 0.4% for both.

Consumer spending accounts for about two-thirds of total output in the U.S. and household outlays have been the main driver of economic growth throughout most of the expansion. But Americans had appeared more cautious in recent months amid declining confidence in the economy.

In the third quarter of the year, personal-consumption expenditures rose at a 2.1% pace, down from 4.3% during the prior period, according to separate data released last week. The University of Michigan’s consumer sentiment index, meanwhile, matched a two-year low in October.

Here’s personal spending (PCE) going back a few years:

-

Morning News: October 31, 2016

Eddy Elfenbein, October 31st, 2016 at 6:25 amWorld Shares Mostly Lower as FBI Probe Raises US Uncertainty

EU, Canada Finally Sign Groundbreaking Trade Deal

Bob Doll Says October’s Bond Rout Means U.S. Economy Improving

GE Nears Deal to Combine Oil-and-Gas Business With Baker Hughes

Legoland Becomes First Brick in Dubai’s Southern Expansion

Coke Ginger Designed To Tempt Health-Conscious Australians With New Infusion

Japan’s Largest Shipping Firms to Merge Container Operations

Honda Net Profit Jumps as Company Shows Signs of Rebound

Sony Cuts Forecast on Impairment for Sale of Battery Unit

No One Saw Tesla’s Solar Roof Coming

Qualcomm Appears To Have Overpaid For NXP

Chevron’s Financials Signal A Turning Point

Media’s Odd Couple: Proudly Freewheeling HBO and Buttoned-Up AT&T

Howard Lindzon: Twenty Minute VC Interview

Cullen Roche: Obama’s Great Economic Blunder

Be sure to follow me on Twitter.

-

The FBI News….

Eddy Elfenbein, October 28th, 2016 at 3:02 pmYou can always tell by looking at traders. The news of the FBI investigation broke at 1 pm here in the east.

-

Q3 GDP Grew by 2.9%

Eddy Elfenbein, October 28th, 2016 at 9:00 amToday we got our first look at Q3 GDP. The government said the economy grew in real terms by 2.9% during the third three months of the year. That’s the best growth rate in two years.

Still, this has been a very weak recovery in historical terms.

Here’s a look at quarterly growth rates.

-

CWS Market Review – October 28, 2016

Eddy Elfenbein, October 28th, 2016 at 7:08 am“They say you never go broke taking profits. No, you don’t. But neither do

you grow rich taking a four-point profit in a bull market.” – Jesse LivermoreThis week’s CWS Market Review will be all about earnings. Nine of our 20 Buy List stocks reported earnings this week. Most were pretty good, but not all. In this week’s issue, I’ll discuss all of them. Plus, I’ll preview one more Buy List earnings report coming this week.

I also have several new Buy Below prices for you. Please note that many of the new Buy Below prices are downward adjustments. That doesn’t mean I’m any less confident about the stocks. It simply reflects each stock’s most recent price action.

Despite all the earnings news this week, the stock market as a whole has been fairly tame (see above). We’ve now gone 12 straight days without a daily move of more than 0.62%. For 79 straight days, the S&P 500 has closed in the 2100s.

Earnings from Wabtec, Express Scripts and CR Bard

Before I get to this week’s earnings, I want to mention Microsoft (MSFT). Last week, the software giant reported very good earnings. On Friday, after the newsletter came out, the stock gapped up to $61 per share, which was an all-time high. This is a good example of a stock that was clearly a good buy, but the market wasn’t waking up to that fact. It takes time, but the market eventually sees the truth. Microsoft remains a buy up to $63 per share.

On Tuesday, three of our Buy List stocks reported earnings. Wabtec (WAB) was the first, and so far, only earnings miss. The rail-services company earned 94 cents per share, which was five cents below estimates.

Wabtec also lowered its full-year forecast again. The previous range was $4 to $4.20 per share. They now expect full-year earnings of $4 to $4.04 per share.

Raymond T. Betler, Wabtec’s president and chief executive officer, said: “Our transit business continues to perform well, while the freight markets remain challenging due to overall rail-industry conditions and the sluggish global economy. We have continued to focus on controlling what we can by aggressively reducing costs, generating cash and investing in our growth opportunities, including acquisitions. At the same time, we are progressing toward completion of the Faiveley Transport acquisition and remain excited by its growth and improvement opportunities.”

The company’s freight group is struggling, and that’s largely behind the disappointing numbers. Still, their cash flow numbers are decent. On Wednesday, the DOJ said that Wabtec will have to divest Faiveley Transport North America’s entire U.S. freight-car brakes business in order to complete its buyout of Faiveley. That shouldn’t be a problem. WAB is a good company in a tough time for its business. This week, I’m lowering my Buy Below on Wabtec to $82 per share.

After Tuesday’s closing bell, Express Scripts (ESRX) reported Q3 earnings of $1.74 per share. That matched Wall Street’s estimate on the nose. The company had previously given us a range of $1.72 to $1.76 per share.

Now for guidance. Express narrowed its full-year range from $6.33 to $6.43 per share to $6.36 to $6.42 per share. That translates to Q4 earnings of $1.84 to $1.90 per share. Wall Street had been expecting $1.85 per share. Overall, this was a good quarter for ESRX.

“The healthcare industry demands that we stay ahead of future trends and deliver solutions to emerging issues facing today’s market,” said Tim Wentworth, CEO and President. “Doing so deepens the trusted relationships we have built with our clients, resulting in another strong year in terms of client retention and new sales.”

Express also narrowed its expected retention rate for next year from 96% – 98% to 97% – 98%. It sounds minor, but it’s very good to see. The stock was largely unmoved by the earnings report.

For the most part, the company is doing well, but the stock has lagged this year. Express is also dealing with an unpleasant legal mess with Anthem. It’s too early to say how that will turn out, but I still like ESRX. I’m lowering our Buy Below on Express Scripts down to $74 per share.

I was on CNBC last week, and Brian Sullivan asked me what stock looked to beat earnings. I said I thought medical devices company CR Bard (BCR) was a top candidate to beat the Street. The company had given a range for Q3 of $2.51 to $2.55 per share. I said that was too low. I also said that Bard would guide higher for the rest of the year.

Bard reported on Tuesday, and it turns out, I was right. The company earned $2.64 per share for Q3. That’s up 16% from last year, and it easily topped Wall Street’s estimate of $2.56 per share.

Timothy M. Ring, chairman and chief executive officer, commented, “The results this quarter demonstrate the continued strength of the economic engine of our business. We continue to increase investments in geographies, products, platforms, and programs that we believe can drive revenue growth longer term. During this period of increased investment in 2016, we have also been able to deliver attractive bottom-line returns for shareholders. We have increased our full-year financial guidance every quarter this year, and we are doing so again today. We expect a strong finish to what has been a very strong year for us so far.”

Bard now expects full-year sales growth of 8% to 9%. Excluding currency, that’s 9% to 10%. I was also right on guidance. For earnings, Bard sees profits ranging between $10.23 and $10.28 per share. That’s an increase on the previous range of $10.10 to $10.20 per share. Wall Street had been expecting $10.17 per share.

Bard’s new range implies Q4 guidance of $2.70 to $2.75 per share. Wall Street had been expecting $2.74 per share. This was an excellent quarter for Bard.

With the stock action, I wasn’t quite so prescient. Bard did rise on Wednesday: at one point it was up 2.5%. But that didn’t last long. Soon enough, the shares drifted back to $210. I’m not worried at all about Bard, but I’m dropping my Buy Below to $217 per share.

Earnings from Fiserv and Biogen

On Wednesday, we got earnings from Biogen and Fiserv. I’m pleased to say that Biogen (BIIB) creamed estimates. The biotech stock reported Q3 earnings of $5.19 per share. That beat the Street’s consensus by 22 cents per share.

All across the board, Biogen had a very good quarter. Last quarter, their star drug, Tecfidera, had sales growth of 10% to just over $1 billion.

Chief Executive George Scangos announced in July he would be leaving, allowing a new chief to lead the company as it works to reignite growth. The biotechnology giant has also drawn takeover interest from drug companies such as Merck Co. and Allergan PLC, The Wall Street Journal reported in August.

Over all for the third quarter, Biogen reported a profit of $1.03 billion, or $4.71 a share, up from $965.6 million, or $4.15 a share, a year earlier. Excluding the restructuring charges, among other items, per-share earnings rose to $5.19 from $4.48.

Total revenue rose 6% to $2.96 billion. Analysts had projected adjusted earnings of $4.97 a share on sales of $2.91 billion, according to Thomson Reuters.

Remember that Biogen is planning to spin off its hemophilia business. The new company will be called Bioverative. (Yuck, who names these?) The spinoff will probably happen sometime early next year. I’m lowering my Buy Below on Biogen to $310 per share.

After the closing bell, Fiserv (FISV) reported Q3 earnings of $1.14 per share. That was one penny more than expectations. Fiserv is about as consistent as they get.

The financial-services company saw its revenue grow by 5%. Last quarter, earnings-per-share rose 11%, and they’re up 15% for the year. Operating margins dropped a bit to 32.8%. Free cash flow rose 12% to $747 million.

”Strong operating performance in the quarter drove double-digit adjusted earnings-per-share growth and excellent free cash flow,” said Jeffery Yabuki, President and Chief Executive Officer of Fiserv. “Outstanding sales results in the quarter should provide additional market momentum and growth.”

For all of 2016, Fiserv expects EPS between $4.43 and $4.46. That means Q4 EPS between $1.15 and $1.18. Wall Street had been expecting $1.16.

Yabuki said, “We continue to expect strong operating results despite a slight shortfall in revenue growth for the year. We anticipate revenue growth to accelerate in the fourth quarter and into 2017.”

The shares took a small hit after the earnings report, but I still like Fiserv a lot. I’m lowering my Buy Below to $105 per share.

Earnings from Ford Motor, AFLAC, Stryker and Stericycle

Now on to Thursday and four more Buy List earnings reports. Before the opening bell, Ford Motor (F) reported Q3 earnings of 26 cents per share. That was six cents more than consensus.

Ford’s earnings were down a lot from last year’s Q3, but investors had been expecting that, and the results a year ago were very strong. Ford’s quarterly revenues fell 6% and, more troubling, operating margins fell to 8.4%.

F-150 sales were pretty good, but a lot of those sales were to fleet buyers which tend to be less profitable. Frankly, this was a difficult quarter for Ford. The company spent a lot of time and money adjusting itself to much higher gas prices. Now that oil is still well below its high, consumers have gravitated to GM’s SUVs. I’m dropping my Buy Below on Ford to $13 per share.

After Thursday’s bell, AFLAC (AFL) said it earned $1.82 in operating earnings for Q3. That was eight cents more than estimates. The duck stock had given us a huge range of $1.58 to $1.86 per share. The stronger yen added 15 cents per share to AFL’s results. Adjusting for currency, AFLAC’s earnings were up 7.1% from last year.

AFLAC decided to raise its dividend from 41 to 43 cents per share. This is their 34th-consecutive dividend increase. The new payout gives the shares a yield of 2.45% based on Thursday’s close.

AFLAC said that if the yen averages 100 to 110 to the dollar for Q4, then they expect Q4 earnings between $1.53 and $1.82 per share. That would bring their full-year earnings to a range of $6.78 to $7.07 per share. AFLAC made $6.16 per share last year. AFLAC remains a solid buy up to $75 per share.

Stryker (SYK) said they earned $1.39 per share for Q3. That was two cents better than estimates. It was also better than the company’s own forecast of $1.33 to $1.38 per share. Quarterly revenues rose 17.1% to $2.83 billion, which also beat estimates.

This was a good quarter for Stryker. The orthopedics company felt confident enough to raise the low-end of its full-year guidance by five cents per share. They now expect 2016 earnings to range between $5.75 and $5.80 per share. That translates to Q4 results of $1.73 and $1.78 per share. The Street had been expecting $1.75 per share. I’m dropping my Buy Below price on Stryker down a tad to $119 per share.

Stericycle (SRCL) has been a terrible stock for us this year. I’ve grown concerned with management’s use of “rollups” to mask slowing organic sales growth. Some of my concerns were assuaged a little bit by the Q3 earnings report. The waste-management company earned $1.24 per share last quarter. That beat estimates by seven cents per share. Still, organic sales rose by just 0.3%.

“We were able to maintain consistent margin performance in the quarter despite revenue headwinds from previously discussed pricing pressure and softness in the manufacturing and industrial market,” said Charlie Alutto, President and Chief Executive Officer.

I’m lowering my Buy Below price on Stericycle to $80 per share.

We have one Buy List earnings report next week. On Tuesday, Cerner (CERN) is scheduled to report its results. For Q3, the health IT company sees earnings ranging between 59 and 61 cents per share.

Cerner’s stock has been a wild ride for us this year. By early March, it was down 17%. CERN then rallied 35% by early August. Since then, it’s slowly slid back.

Three months ago, Cerner reiterated its full-year guidance of $2.30 to $2.40 per share, but it lowered its full-year revenue guidance to $4.9 billion to $5.0 billion. The previous range was $4.9 billion to $5.1 billion.

That’s all for now. Lots more earnings next week. We’ll also get some of the key turn-of-the-month econ reports. Personal income and spending are on Monday. The ISM report is on Tuesday. Wednesday is ADP payroll. The Fed also meets on Wednesday. I strongly doubt they’ll do anything. That leads us up to Friday and the big jobs report. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: October 28, 2016

Eddy Elfenbein, October 28th, 2016 at 7:02 amRBS Warns on Profit Outlook After Trading Unit Boosts Revenue

Broadband Providers Will Need Permission to Collect Private Data

Wall Street’s Frantic Push to Hire Coders

UPS Puts $5.3 Billion in Air Power Behind Overseas Expansion

Alphabet Delivers a Resounding Beat

Amazon Takes Hit as Costs Surge

Toyota Invests In U.S. Car-Sharing Service

Xerox’s Quarterly Revenue Falls Nearly 3%

More Wretched News For Newspapers as Advertising Woes Drive Anxiety

General Electric Pursues Deal With Baker Hughes

Sharpie-Maker Newell Lifts Full-Year Profit, Sales Forecasts

Booz Allen Is Reviewing Its Security After the Arrest of Another NSA Contractor

U.S. Takes Down Call-Center Financial Scam

Howard Lindzon: Google Cuts Fiber…a Sad Day in American Technology History

Jeff Carter: What Is The One True Thing You Know?

Be sure to follow me on Twitter.

-

Morning News: October 27, 2016

Eddy Elfenbein, October 27th, 2016 at 7:42 amChina’s Slowing Industrial Profits Show Rising Debt Hampering Economy

U.K. Economy Wins Round One of Brexit Before Real Test Begins

Did Brexit Kill the British IPO Market?

Deutsche Bank Warns of Tough Times Ahead Due To U.S. Fine

Nissan Commits to Build New Models in Britain, Securing 7,000 Jobs

Ford Profit Falls Less Than Forecast Aided by Cost Controls

Twitter Beats Revenue, User Estimates and Cuts 9% of Workforce

China Logistics Company Raises $1.4 Billion in U.S. IPO

Qualcomm to Buy NXP Semiconductors For About $47 Billion Including Debt

VW Brand’s Massive Slump in Profit Sparks More Calls for Cost Cuts

Here’s The Big Problem Some Analysts Have With Tesla’s Results

Barclays Posts 35% Jump in Profit on Bond-Trading Revenue

AT&T Needs the Time Warner Content Factory to Survive

Cullen Roche: The Pitfalls of the Passive Investing Marketing Pitch

Jeff Miller: Things I Don’t Care About — And Neither Should You!!

Be sure to follow me on Twitter.

-

Fiserv Earned $1.14 per Share

Eddy Elfenbein, October 26th, 2016 at 4:09 pmAfter the closing bell, Fiserv (FISV) reported Q3 earnings of $1.14 per share, one penny more than expectations.

”Strong operating performance in the quarter drove double-digit adjusted earnings per share growth and excellent free cash flow,” said Jeffery Yabuki, President and Chief Executive Officer of Fiserv. “Outstanding sales results in the quarter should provide additional market momentum and growth.”

Here are some highlights:

• Adjusted revenue increased 5 percent in both the third quarter and first nine months to $1.31 billion and $3.86 billion, respectively, compared to the prior year periods.

• Internal revenue growth for the company was 4 percent in the third quarter, driven by 5 percent growth in the Payments segment and 2 percent growth in the Financial segment.

• Internal revenue growth for the company was 4 percent in the first nine months of 2016, led by 6 percent growth in the Payments segment and 1 percent growth in the Financial segment.

• Adjusted earnings per share increased 11 percent in the third quarter to $1.14 and 15 percent in the first nine months of 2016 to $3.28 compared to the prior year periods.

• Adjusted operating margin decreased 30 basis points to 32.8 percent in the quarter and increased 20 basis points to 32.2 percent in the first nine months compared to the prior year periods.

• Free cash flow increased 12 percent to $747 million in the first nine months of 2016 compared to the prior year period.

• Sales performance increased 34 percent in the quarter and 21 percent in the first nine months of 2016 compared to the prior year periods.

• The company repurchased 3.1 million shares of common stock for $329 million in the third quarter and 9.3 million shares of common stock for $933 million in the first nine months of 2016. As of September 30, 2016, the company had 8.1 million remaining shares authorized for repurchase.

For all of 2016, Fiserv expects EPS between $4.43 and $4.46. That means Q4 EPS between $1.15 and $1.18. Wall Street had been expecting $1.16.

“We continue to expect strong operating results despite a slight shortfall in revenue growth for the year. We anticipate revenue growth to accelerate in the fourth quarter and into 2017,” said Yabuki.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His