Archive for July, 2009

-

RIP: John S. Barry

Eddy Elfenbein, July 24th, 2009 at 10:37 amLet’s take a moment to honor the memory of John S. Barry who recently passed away. Mr. Barry’s service to American capitalism can be found in each can of WD-40.

He didn’t invent the stuff, but he ran the company that put it in 80% on American homes. In fact, it was Barry’s idea to change the name of the Rocket Chemical Company into the WD-40 Company (WDFC).Mr. Barry was fiercely dedicated to protecting the secret formula of WD-40, not to mention its trademarks and distinctive container. The company never patented WD-40, in order to avoid having to disclose the ingredients publicly. Its name became synonymous with the product, like Kleenex.

Mr. Barry acknowledged in interviews with Forbes magazine in 1980 and 1988 that other companies, including giants like 3M and DuPont, made products that closely resembled WD-40.

“What they don’t have,” he said, “is the name.”

Mr. Barry brought marketing coherence and discipline to the company. He spruced up the packaging and increased the advertising budget, but most of all he pushed for distribution. He emphasized free samples, including the 10,000 the company sent every month to soldiers in the Vietnam War to keep their weapons dry.

Within a little more than a decade, Mr. Barry was selling to 14,000 wholesalers, up from 1,200 when he started.

He kept tight control of the product. When Sears wanted to package WD-40 under its own label, Mr. Barry said no. When another big chain wanted the sort of price concessions to which it was accustomed, he refused.

He pushed to get WD-40 into supermarkets, where people buy on impulse. He also began an aggressive effort to sell WD-40 in foreign countries.

“We may appear to be a manufacturing company,” Mr. Barry said to Forbes, “but in fact we are a marketing company.” -

More on Mo

Eddy Elfenbein, July 24th, 2009 at 10:19 amOver at the Economist, Buttonwood highlights a study that touches on one of our favorite subjects—momentum investing. The study shows that momentum has been a big winner.

Over the period 1980-2009, AQR’s momentum index returned 13.7% a year against 11.2% for the Russell 1000 index. The volatility of the momentum index was rather higher but the Sharpe Ratio (excess return divided by volatility) was still better than the Russell index. In the smallcap section, the return was 15.4% a year. Again the volatility was high but the Sharpe ratio was significantly better than that of the Russell 2000.

Analysis shows that stocks with the big mo (as the first President Bush called it) are more correlated with growth than value. Potentially this makes the approach a good diversifier for value investors who, as is well known, suffer from some terrible periods of underperformance. Adding a 50% momentum weight to a value portfolio would have increased both returns and volatility by a percentage point over the last 29 years, a decent trade-off.The problem, of course, is that this has already happened. Some analysts, like David Merkel, think that the momentum is getting crowded—and I suspect he’s right.

I think the fascinating part is the fact that the stock market is self-aware. That’s a crucial point — it’s not a blank slate. The market knows where stocks have been and past prices do have an impact on future prices. -

Gasparino Responds to Crossing Wall Street

Eddy Elfenbein, July 23rd, 2009 at 3:21 pmWhen he talks about the “one blogger” who made the George Eliot remark yesterday, that was me.

I’ll reiterate—I’m a CG fan. I use my real name and most other finance bloggers use their real names as well.

The reason some folks don’t is due to serious professional concerns. Sure, I’m not wild about the use of pseudonyms, but I think we ought to respect it.

And everybody—pen named or real named—ought to be civil. -

More Diverse Financial Journalism

Eddy Elfenbein, July 23rd, 2009 at 3:03 pmJustin Fox comes to the defense of Matt Taibbi in the name of “more diverse” financial journalism.

Indeed, it would be more diverse to include both honest and dishonest journalism, but I still fail to see the benefits. -

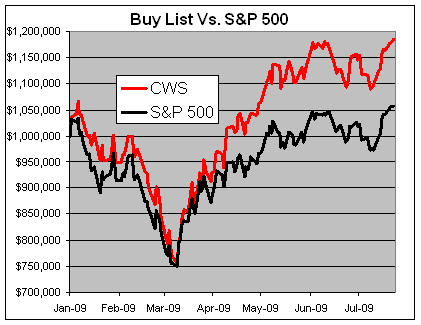

The Dow Breaks 9,000

Eddy Elfenbein, July 23rd, 2009 at 11:38 amThe market is up strongly today to another new post-March high. Our Buy List is now up over 20% this year. The Dow just broke 9,000 and the S&P 500 peaked above 975. Since March 9, the S&P 500 is up 44% and our Buy List is up 59%.

Thanks to recent article in Barron’s, Bed Bath & Beyond (BBBY) is over $35 today which is a new 52-week high.

Here are some earnings updates for our Buy List:

Yesterday, Eli Lilly (LLY) posted a very strong earnings beat and guided higher. The company earned $1.12 which was 10 cents higher than consensus. They made 99 cents per share for last year’s Q2 so that’s decent growth. LLY also raised its full-year EPS range to $4.20 to $4.30, from its earlier range of $4 to $4.25. This stock is a good buy.

Danaher (DHR) has been the dud so far. They reported earnings of 89 cents per share, one penny ahead of expectations. That’s a big drop-off from a year ago when they earned $1.09 a share. It’s a tough environment for Danaher, but it’s still a solid company.

SEI Investments (SEIC) saw its earnings-per-share drop from 24 cents to 22 cents, which was a penny better than consensus. Business has been rough for SEIC but the earnings drop for the second quarter is far better than the earnings drop for the first quarter. Hopefully, things will continue to improve for them. -

The Buy List Hits a New High

Eddy Elfenbein, July 22nd, 2009 at 4:44 pmBoo-Yah! We’re up 18.56% for the year.

Not only is this blog free — it makes you money. If you started the year with $1 billion, I made you over $185 million.

(BTW, did I mention the 2&20? We’ll talk later.) -

“People Who Don’t Matter On Wall Street”

Eddy Elfenbein, July 22nd, 2009 at 1:32 pmTo people who aren’t familiar with the ways of Wall Street, one of the things I try hardest to convey is the absurd level of male-posturing. You have to see it to believe it. It’s as if a squadron of B-52s douses the Street each morning with massive amounts of testosterone.

This is all the more absurd because Wall Streeters are well…let’s be honest, geeks in suits. They don’t work with their hands and most wouldn’t know how to operate a hammer to save their lives. Never fear, they’ve found a sure-fire way to make up for their inadequacy.

It’s with that that I turn to Charlie Gasparino’s response to Janet Tavakoli:I generally don’t respond to people who don’t matter on Wall Street. But any rational, sane person who hasn’t been either hitting the bottle or smoking a joint would watch what I said about Goldman Sachs and come away with two things. 1) I am very tough on them– they always complain about what I say. and 2) In the so-called ‘caving’ clip I was letting them give their side of the story because that’s what journalists do. If someone named Janet thinks I’m selling out, she’s entitled to her opinion, which I hate to break it to her, really doesn’t matter.

I’m a big fan of Gasparino, but that’s an awful statement. Whenever I see an ad hominem attack, it has zero effect on me except I assume that the ad hominemer has a weak case.

Here’s Gasparino responding — the fun begins around 2:30:

“Tyler Durden is probably not even his name!” Yes, that’s right Charlie. Also, George Eliot wasn’t a man. -

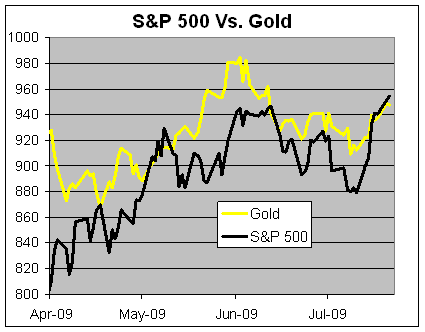

The S&P 500 Edges Out Gold

Eddy Elfenbein, July 22nd, 2009 at 12:09 pmFor the last several weeks, the price of gold and the S&P 500 have followed each other closely. Most of the time, gold has been ahead, but just recently stocks have gained the upper hand.

Although stocks have been perking up lately, the last ten years have been all about gold. Consider that in 2000 the S&P 500 used to be five times the prices of gold and now they’re equal. But in 1980, gold was more than seven times the S&P 500. -

Stryker’s Q2 Earnings

Eddy Elfenbein, July 21st, 2009 at 4:56 pmAfter the closing bell, Stryker (SYK) reported second-quarter earnings of 73 cents a share. This was the same as last year’s Q2 and it was a penny a share better than consensus. Sales came in at $1.634 billion which was down 4.6% from last year’s second quarter. Adjusting for currency moves, it’s about flat.

This is a decent report, not great but in this environment, it’s certainly respectable. I wouldn’t be surprised if Stryker is at the trough of its earnings cycle—and if that means flat growth, that’s pretty good.

I was pleased to see the company back its previous guidance for full-year EPS of $2.90 to $3.10. In January, Stryker originally pegged this year in a range of $3.12 to $3.22. Then in April, they lowered it to the current range. Personally, I think $3 may be a stretch, but we’ll see. For comparison, last year came in at $2.83 and 2007 came in at $2.40.Second Quarter Highlights

* Net sales of $1,634 million were flat (0.1% decrease) on a constant currency basis (4.6% decrease as reported)

* Orthopaedic Implants sales increased 5.1% on a constant currency basis (0.2% decrease as reported)

* MedSurg Equipment sales decreased 7.7% on a constant currency basis (11.0% decrease as reported)

* Net earnings decreased 4.7% from $306 million to $291 million

* Diluted net earnings per share were unchanged at $0.73

“In a challenging environment, we were very pleased with the growth of our U.S. Orthopaedic Implant businesses, which accelerated from last quarter and showed strong year-over-year gains. This performance, combined with our heavy focus on controlling costs across the company preserved our diluted earnings per share results in the face of the steep short term slowdown in our MedSurg businesses, and the foreign currency headwinds in the quarter,” commented Stephen P. MacMillan, President and Chief Executive Officer.

Net sales were $1,634 million for the second quarter of 2009, representing a 4.6% decrease compared to net sales of $1,713 million for the second quarter of 2008, and were $3,236 million for the first half of 2009, representing a 3.3% decrease compared to net sales of $3,347 million for the first half of 2008. On a constant currency basis, net sales decreased 0.1% for the second quarter and increased 1.6% for the first half.

Net earnings for the second quarter of 2009 were $291 million, representing a 4.7% decrease compared to net earnings of $306 million for the second quarter of 2008. Diluted net earnings per share for the second quarter of 2009 were unchanged at $0.73 compared to the second quarter of 2008. Net earnings for the first half of 2009 were $572 million, representing a 4.0% decrease compared to net earnings of $596 million for the first half of 2008. Diluted net earnings per share for the first half of 2009 increased 0.7% to $1.44 compared to $1.43 for the first half of 2008.

Sales Analysis

Domestic sales were $1,047 million for the second quarter of 2009, representing a decrease of 0.5%, as a 9.1% increase in shipments of Orthopaedic Implants was offset by an 11.0% decrease in shipments of MedSurg Equipment. Domestic sales were $2,089 million for the first half of 2009, representing an increase of 0.2%, as a result of a 7.5% increase in shipments of Orthopaedic Implants offset by an 8.0% decrease in shipments of MedSurg Equipment.

International sales were $587 million for the second quarter of 2009, representing a decrease of 11.0%. The impact of foreign currency comparisons to the dollar value of international sales was unfavorable by $77 million in the second quarter of 2009. On a constant currency basis, international sales increased 0.6% in the second quarter of 2009, as a result of a 0.4% increase in shipments of Orthopaedic Implants and a 1.1% increase in shipments of MedSurg Equipment. International sales were $1,146 million for the first half of 2009, representing a decrease of 9.1%. The impact of foreign currency comparisons to the dollar value of international sales was unfavorable by $164 million in the first half of 2009. On a constant currency basis, international sales increased 3.9% in the first half of 2009, as a result of a 3.3% increase in shipments of Orthopaedic Implants and a 5.2% increase in shipments of MedSurg Equipment.

Worldwide sales of Orthopaedic Implants were $1,014 million for the second quarter of 2009, representing a decrease of 0.2%, and were $1,987 million for both the first half of 2009 and 2008. On a constant currency basis, sales of Orthopaedic Implants increased 5.1% in the second quarter and 5.7% in the first half of 2009, based on higher shipments of reconstructive, trauma, spinal and craniomaxillofacial implant systems.

Worldwide sales of MedSurg Equipment were $620 million for the second quarter of 2009, representing a decrease of 11.0% as reported and 7.7% on a constant currency basis based on lower shipments of surgical equipment and surgical navigation systems; endoscopic, communications and digital imaging systems; and patient handling and emergency medical equipment. Worldwide sales of MedSurg Equipment were $1,248 million for the first half of 2009, representing a decrease of 8.2% as reported and 4.4% on a constant currency basis as higher shipments of surgical equipment and surgical navigation systems were offset by lower sales of endoscopic, communications and digital imaging systems and patient handling and emergency medical equipment.The company also reduced its sales forecast by just a hair. Bottom line: This is a good stock and it’s still a relative bargain.

-

Open Letter to Dennis Kneale

Eddy Elfenbein, July 21st, 2009 at 3:36 pm(I’m a little new to phony arguing so here goes.)

Dear Mr. Kneale,

Listen Dennis — I’m tired you “telling it like it is.” Oooh, that burns me up! But you know what I really can’t stand? It’s your no holds barred approach. YuckI can’t tell you how angry it makes me when you stand up for the little guy!

Mt. Kneale, we both know that I have no arguments, so the only way I’m going to respond to you is by calling you names! Do you understand that, Beaker?

Mind you, I’m terrified to appear on your show, however if invited, I will appear.

You stupid, stupidhead.

Love,

Eddy

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His