Archive for July, 2010

-

Well, At Least Someone Is Making Money

Eddy Elfenbein, July 31st, 2010 at 9:07 pmBernanke made some coin last year:

Federal Reserve Chairman Ben Bernanke’s personal finances recovered in 2009, disclosure forms released by the central bank on Friday showed.

Bernanke listed assets in a range of $1.2 million to $2.5 million. They had slipped to between $822,011 to $1.8 million in the previous year, from $1.7 million and $2.5 million in 2007.

Bernanke’s assets included annuities, mutual funds and money market funds. His two largest holdings were annuities from the TIAA-CREF financial services company worth between $500,001 and $1 million each. -

Moog Beat By a Penny

Eddy Elfenbein, July 30th, 2010 at 8:39 pmOne more Buy List stock report. Moog (MOG-A) earned 64 cents per share which beat Wall Street’s estimates by a penny a share.

In 2008, Moog earned $2.75 per share and that dropped to $1.98 per share last year. Last November, Moog said to expect EPS for this fiscal year (ending in September) between $2.15 and $2.35. They reiterated that in February. Then in May, Moog said to expect $2.35 per share which they reiterated today. On top of that, they gave an estimate for FY 2011 of $2.70 a share.

The CEO also had something interesting to say:With third-quarter profits up 83.6 percent and earnings per share rocketing 73 percent, respectively, Robert Brady, the chairman of Moog, declared the recession is over for the aerospace and defense manufacturer.

The stock was up 2.8% today and it’s our third best-performing stock this year.

-

Mad Men: Lie Vs. Lay

Eddy Elfenbein, July 30th, 2010 at 1:29 pm -

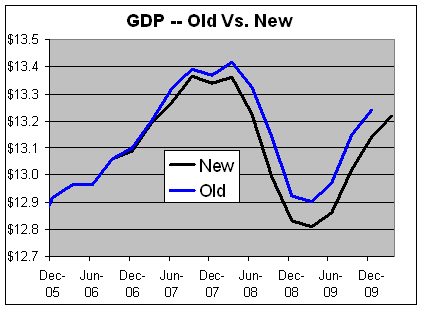

Recession Receded Worst Than Previously Thought

Eddy Elfenbein, July 30th, 2010 at 11:15 amToday’s Q2 GDP report came out and it was ugly. The economy grew by just 2.4% in real terms for the second three months of the year. That was below the Street’s forecast of 2.6%.

The Commerce Department also revised the GDP numbers going back to Q4 of 2006 and it turns out that the recession was even worse than they thought.

Check out the old numbers versus the new ones:

Nothing is as surprising as the past. -

NICK’s ROE 14.5%

Eddy Elfenbein, July 30th, 2010 at 10:47 amHere are still more stats from NICK’s earnings report.

The beginning and ending shareholder equity figures for the last quarter were $101,361,000 and $97,437,000. That averages to $99,399,000. NICK earned $3,425,500 for the quarter so that comes to a quarterly ROE of 3.45%. Annualized that comes to 14.51%.

So this stock is almost like a 14.5% subprime bond that’s going for less than par and it’s credit quality is improving.

That’s not a perfect analogy but it does place the stock in some context. -

96 Years Ago, the NYSE Shuts Down

Eddy Elfenbein, July 30th, 2010 at 10:09 amOn July 30, 1914, the Dow plunged 6.9% — from 56.20 to 52.32. There apparently were some difficulties in Europe. The NYSE then decided to shut down. Gary Alexander explains it:

The Federal Reserve was finally formed in 1913 – in the nick of time, right before one of the scariest bank crises of the 20th Century. Early in the morning of Friday, July 31, 1914, the London Stock Exchange announced that it would suspend trading until further notice, the first time it had done so in its centuries-long heritage. World War I was beginning all over Europe, and stock markets had already closed in Vienna, Rome and Berlin. The U.S. stock market was in a state of panic, with blue chip stocks falling 20% or more on July 30, on record volume. If the New York Stock Exchange opened for trading on July 31, it would be the only open stock market in the world. Since markets were then connected by undersea cables, all the world’s sellers would converge on Wall Street. In fact, the overnight sell orders “at any price” were lined up for the opening bell, so the NYSE governors decided to close for only the second time in its history.

The NYSE was effectively closed from July 31, 1914 to the middle of April, 1915. But on that fateful Friday, July 31, 1914, U.S. banks stayed open, and the rush to convert cash to gold wiped out many banks. From July 27 to August 7, $73 million in gold was withdrawn from New York banks alone. But the presence of the Federal Reserve insured that most of those banks survived.Here’s the NYT‘s story.

-

AFLAC’s Dividend Streak Is in Jeopardy

Eddy Elfenbein, July 29th, 2010 at 10:31 pmWhen AFLAC (AFL) reported earnings on Tuesday, the company also declared a dividend for the third quarter of 28 cents per share. This news caught my attention because AFLAC hasn’t raised its dividend all year, and the company is famous for its yearly dividend increases.

AFLAC has raised its dividend every year for the past 27 years so if they’re taking this year off, it’s big news. They now have just one quarter to go to keep the streak alive.

Fortunately, CEO Dan Amos said on the conference call that a fourth-quarter increase is probably on the way:As I have conveyed over the last several quarters, we would like to return to that policy, when we believe it’s prudent to do so, extending our lengthy record 27 consecutive annual increases in the cash dividend that it is important to us and to our owners.

Along those lines, I fully expect the Board of Directors to approve a modest increase in the cash dividend effective with the fourth quarter of this year. Additionally, we continue to believe that share repurchase is an effective means for enhancing shareholder value.Personally, I can do without the share repurchase. But getting back to the dividends, what’s especially impressive is that AFLAC has not only raised its dividend consistently, it’s done so by a lot. According to my numbers, AFLAC has raised its dividend by at least 12% every year since 1991. That’s as far back as my data goes so the streak may be even longer.

I’m almost positive (say 99% confident) that this is the longest current double-digit dividend increase streak going. I’ve searched and searched and haven’t found one exception.

What’s peculiar is that AFLAC is financially strong enough that it can easily raise its dividend. The company earned $1.35 last quarter so the 28-cent dividend translates to a modest payout ratio of 20.7%. What are they afraid of?

I think it’s that the simply want to build up capital and show the market that they’re in strong financial shape. It’s odd that a move like this could only happen after a crisis, not before. -

NICK Earns 29 Cents a Share

Eddy Elfenbein, July 29th, 2010 at 10:34 amEarnings just came out and they’re outstanding:

Nicholas Financial, Inc. (Nasdaq:NICK – News) announced that for the three months ended June 30, 2010, net earnings, excluding change in fair value of interest rate swaps, increased 65% to $3,426,000 as compared to $2,081,000 for the three months ended June 30, 2009. Per share diluted net earnings, excluding change in fair value of interest rate swaps, increased 61% to $0.29 as compared to $0.18 for the three months ended June 30, 2009. See reconciliations of the Non-GAAP measures on page 2. Revenue increased 9% to $14,952,000 for the three months ended June 30, 2010 as compared to $13,694,000 for the three months ended June 30, 2009.

According to Peter L. Vosotas, Chairman and CEO, “We are pleased to report record 1st quarter revenue and earnings. Our results were primarily impacted by an increase in revenues, a reduction in the net charge-off rate and an increase in the cost of borrowed funds. During the first quarter we have added four branch offices to our 12 state branch network, bringing the total to 54 locations. The Company continues to evaluate additional markets for future branch locations and subject to market conditions, could open additional branch locations during the year. The Company remains open to acquisitions should an opportunity present itself.”I knew NICK was doing well but these results are even better than what I expected. Here are the estimates I made earlier:

Receivables: $235 million to $240 million

Gross yield: 24% to 25%

Interest Expense: 3% to 4%

Provision for Credit Losses: 4%, maybe less

Pre-Tax Yield: 9%

And here are the results:

Receivables: $238.3 million

Gross yield: 25.08%

Interest Expense: 2.58%

Provision for Credit Losses: 2.68%

Pre-Tax Yield: 9.43%

A few months ago, I said that NICK could earn $1.10 a share this calendar year (the fiscal year ends in March, I used calendar year simply for market comparison).

That must have seemed wildly optimistic but now it seems easy. NICK has made 57 cents a share for the first six months of this year. The stock’s book value is up to $8.57.

Here’s something to think about: NICK’s net yield and pre-tax yield are the highest since Q2 of 2007. Also, the provision for credit losses is the lowest since then. The major difference is that receivables are now 28% higher and net revenues are 27% higher.

So the stock is 27% higher, right? No! NICK was as high as $12.55 in May 2007! -

Becton, Dickinson Kills It

Eddy Elfenbein, July 29th, 2010 at 9:35 amBecton, Dickinson (BDX) had a great earnings report this morning. They earned $1.29 per share for the quarter which was five cents more than estimates.

“We are pleased with our results this quarter, with each of our three segments contributing to our growth. We delivered earnings per share from continuing operations of $1.29, which is in line with the Company’s expectations,” said Edward J. Ludwig, Chairman and Chief Executive Officer. “Despite the challenging global economy, we expect to deliver bottom-line growth of approximately 9 percent foreign-currency neutral, which is in line with our previously communicated range of 8 to 10 percent for the full fiscal year 2010. Profits and cash flows continue to improve as a result of operational efficiencies. We are also pleased to announce that we are increasing our share repurchases to $700 million from $550 million, which supports our ongoing commitment to return value to shareholders.”

They also raised full-year EPS guidance to $5.10 to $5.15. The stock is higher in this morning’s trading.

-

$837 Billion in Cash

Eddy Elfenbein, July 28th, 2010 at 9:19 amThat’s how much cash that non-financial companies in the S&P 500 are currently sitting on. That’s worth about 10% of their market value which is much higher than normal.

The odd thing about this gigantic cash pile is that these companies are barely being paid any interest by keeping this money in cash. It shows you just how scared they are.

Matt Krantz points out that the amount of cash is up 26% in the last year. By contrast, dividends are only up 5.9% and M&A spending is down -9.5%. If the economy can avoid a double dip, then there might be enough fuel already to power a rally.

- Tweets by @EddyElfenbein

-

-

Archives

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His {kind=link}