Archive for August, 2013

-

Pitching Records and Investing

Eddy Elfenbein, August 26th, 2013 at 1:08 pmOn Saturday, Detroit’s Max Scherzer pitched another gem and he increased his won-loss record this season to a remarkable 19-1. Scherzer just pulled ahead of Pittsburgh’s Roy Face’s record for single season winning percentage of 18-1 set in 1959. Scherzer has another seven or eight starts this year, and to break Face’s record, he can’t afford to have another loss.

Scherzer has pitched incredibly well this year. He leads or is near first in just about every pitching category. What I find interesting, though, is Face’s 18-1 mark from 1959.

More than any other record I can think of, Face’s incredible won-loss record seems the most due to luck. We often hear from academics that the record of any great money manager is simply due to luck. If you flip enough coins, surely you’ll see a fantastic run of consecutive heads. It’s just probability.

With investing, I usually think that’s a bogus argument, but in Face’s case, it appears to be correct. Let me clear: Roy Face pitched very well in 1959, just not 18-1 well. Looking closely at his 1959 season, the run of luck he had seems extraordinary.

For one, Face wasn’t a starter. He was one of the first regular closers in baseball. Also, anyone’s won-loss record isn’t solely due to their performance of the pitcher. His teammates have a lot to do with it. Face had a remarkable ability that year to come on in relief when the game was tied, and thanks to his fellow Pirates, he’d get credited for the win. Or blow the save, then get the win. After all, shortening a baseball game to one or two innings greatly raises the importance of luck to your outcome.

That year, the Pirates went 78-76 but they were an amazing 19-2 in extra-inning games, plus 36-19 in one-run games.

What does this mean for investing? Realize that looks can be deceiving. Almost anything can happen with a small enough sample size. Concentrate on numbers that are subject to lower volatility. That’s why I like stocks with long histories of raising their earnings and dividends. That’s not luck, it’s earned.

One-year performance marks for a stock or mutual fund are like won-loss records for pitchers — they really don’t tell you much. In fact, in many cases those are the worst investments to have due to mean reversion.

Still, I’m rooting for Scherzer to go the rest of the season without a loss.

-

The Case For The Economy

Eddy Elfenbein, August 26th, 2013 at 10:53 amIn Friday’s CWS Market Review, I said that it’s very likely the rise in long-term interest rates is due to greater optimism about the U.S. economy. The morning’s durable goods report certainly doesn’t aid that thesis, but Bill McBride of Calculated Risk lays out the reasons why he thinks the next few years will be good for the economy.

For one, the economy has been held back by cutbacks in state and local government. That trend appears to be over. The U.S. budget deficit is also shrinking quite quickly. Next year, we have a good shot of coming in at less than 3% of GDP. In fact, given the state of the labor market, some might think that’s too austere. Also, American households have significantly delevered themselves over the past five years. Financially speaking, we’re in much better health today.

Perhaps the best variable in the economy’s favor is the housing market. Bear in mind that the general cycle of the economy is very close to that of the housing market. During the boom, so many houses were built that we had a very large amount of inventory overhang. Now it appears to be wearing off. Simple demographics tell us that despite any increase in mortgage rates, the demand for new homes will increase. McBride writes:

Starts averaged 1.5 million per year from 1959 through 2000. Demographics and household formation suggests starts will return to close to that level over the next few years. That means starts will come close to doubling from the 2012 level.

Residential investment and housing starts are usually the best leading indicator for economy, so this suggests the economy will continue to grow over the next couple of years.

-

Harris Raises Dividend 13.5%

Eddy Elfenbein, August 26th, 2013 at 10:06 amExcellent news today from Harris Corp. ($HRS). The board has raised the quarterly dividend from 37 cents to 42 cents per share. That’s a 13.5% increase. Based on Friday’s close, HRS yields 2.95%. The shares are currently up 41 cents today. A few weeks ago, Harris reported earnings significantly better than estimates. The company earned $1.41 per share compared with Wall Street’s consensus of $1.15 per share. Business is clearly going well there.

Turning to economics, this morning’s report on orders for durable goods was pretty lousy. July orders fell by 7.3% which was the biggest drop in 11 months. Economists were expecting a drop of 4%. Bloomberg notes:

The report shows struggling overseas markets and the effects of federal government spending cuts are lingering and holding back manufacturing, which accounts for about 12 percent of the economy. Further improvement in the labor market and sustained demand for automobiles and housing would help spur production through the second half of the year.

Microsoft ($MSFT) is down 49 cents today, which is about 1.4%, but that’s after its strong post-Ballmer showing from last Friday.

Bespoke Investment Group reminds us that the S&P 500 is back above its 50-day moving average. We snapped a five-day streak over closing below the 50-DMA.

-

Morning News: August 26, 2013

Eddy Elfenbein, August 26th, 2013 at 6:46 amECB Council Members Split in Jackson Hole Over Rate Cuts

China Economy Showing Clear Signs of Stabilisation: National Bureau of Statistics

Greece Could Return to Debt Market in Late 2014, Stournaras Says

Japan May Dip Into Budget Reserves To Fight Fukushima Toxic Water

Wall Street Is So Obsessed With The Taper, It’s Missing The Bigger Threat Coming Out Of Washington

America Movil to Back KPN German Sale After Bid Sweetened

Amgen to Buy Onyx for $10.4 Billion to Gain Cancer Drug

ONGC May Raise Overseas Debt for $2.64 Billion Purchase

ING Sells Korean Life Insurance Unit for $1.7 Billion to MBK

Abercrombie & Fitch Might Need Those Plus-Size, Unpopular Teens After All

Young Tech Sees Itself in Microsoft’s Ballmer

As Amazon Stretches, Seattle’s Downtown is Reshaped

Muriel Siebert, Pioneer at NYSE, Dies at 80

Joshua Brown: Being Ben Bernanke

Jeff Miller: Weighing the Week Ahead: Will Fear Beget More Fear?

Be sure to follow me on Twitter.

-

Foghorn Unplugged

Eddy Elfenbein, August 24th, 2013 at 10:09 pm -

Ballmer to Resign, MSFT Surges

Eddy Elfenbein, August 23rd, 2013 at 9:15 amHere’s a rule of thumb: If you happen to be the CEO of a major corporation and the news of your resignation causes your stock to gain $24 billion in market value, you probably made the right call.

Microsoft ($MSFT) said today that Chief Executive Officer Steve Ballmer has decided to retire within the next 12 months. In the pre-market, MSFT is up $2.87, or 8.86%. The company has 8.33 billion shares outstanding, so today’s surge comes to $23.9 billion. Again, that’s for someone to no longer be there.

-

CWS Market Review – August 23, 2013

Eddy Elfenbein, August 23rd, 2013 at 7:13 am“To achieve satisfactory investment results is easier than most people realize;

to achieve superior results is harder than it looks.” – Benjamin GrahamWall Street’s been having a tough time so far this August. Through Wednesday, the S&P 500 fell on ten of the previous 13 days. Thanks to the low volatility of late summer, these dips haven’t stung very much. Measuring from the market’s peak on August 2, the index lost nearly 4%, though we gained some of that back on Thursday. Interestingly, the Dow Industrials fell to their lowest level relative to the S&P 500 in five years.

Now a 4% haircut isn’t much of a downswing. It’s only a minor dent in the rally we’ve had this year. However, the big concern on everyone’s mind is that Ben Bernanke and his friends at the Fed are finally going to start “tapering” their bond purchases next month. I’ll have more on that in a bit. Wall Street had more headaches yesterday as “technical issues” caused trading to be halted on the Nasdaq for three hours.

But the action that’s caught my attention hasn’t been in the stock market. It’s in the bond market. Interest rates have spiked dramatically in the U.S., and the long bond is near its worst selloff in 13 years. In early May, the 10-year Treasury was yielding 1.63% (see chart below). On Thursday, the yield got as high as 2.92%, and a lot of folks expect us to break 3% any day now.

In this week’s CWS Market Review, we’ll take a closer look at what’s causing bond traders so much grief. We’ll also take a look at recent Buy List earnings reports from Medtronic ($MDT) and Ross Stores ($ROST). (Ross beat consensus by five cents per share and looks to break out soon.) But first, let’s focus on the dramatic rise in bond yields.

Why Are Rates Rising? It’s the Economy

The stock and bond markets have a rather unusual relationship. The two markets can basically be described as “frenemies.” On one level, they’re competitors for investors’ capital. Money will go wherever it’s treated best. The catch is that neither market will prosper for long if the other one is suffering. After all, the bond market is debt, and if companies have to shell out higher interest costs, that will cut into their bottom line. Meanwhile, if companies aren’t making a profit, then they can’t pay back their loans. Stocks and bonds are rivals under the same flag.

Sometimes the two markets move together as if they’re waltzing partners, and other times they act in near-perfect opposition. As a very general rule of thumb, the bond market leads the stock market by about six months to a year.

Long-term interest rates officially hit their low thirteen months ago, but the decline since then was rather slight. That is, until this May, when the rout really got going. The 10-year yield is now where the 20-year yield was in June, and where the 30-year yield was in May. So the question to ask is, why is the bond market falling so sharply?

The popular answer is that it’s due to the Federal Reserve pulling out of its bond buying. But I’m not so sure. Let’s review the situation: The Fed meets again in mid-September, and the central bank has successfully convinced Wall Street to expect a scaling-back of asset purchases. This week, in fact, the Fed released the minutes of its last meeting, and those minutes indicated that the other FOMC members are on board with Bernanke’s tapering plan. Personally, I think it’s too early to start tapering. If they do announce a tapering, and they probably will, I expect it to be modest, which means the Fed hasn’t left the bond market at all: they’re simply buying less. This really shouldn’t be a big deal.

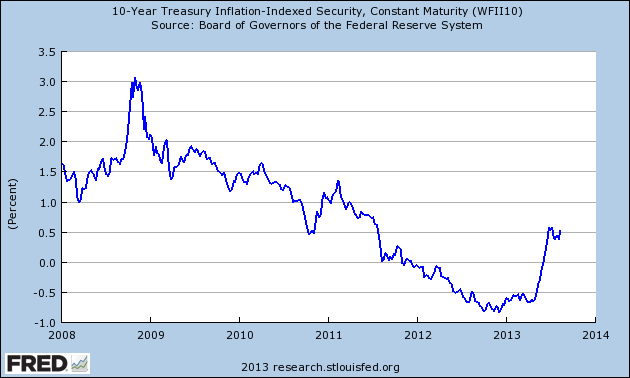

That’s why I don’t believe the taper talk is the reason for higher interest rates. Other people think the higher rates are due to inflation. The gold market has rebounded lately, but that’s coming after a pretty rough year. The yellow metal is still off more than $500 an ounce since last year’s high. The CPI reports continue to be quite tame. Also, the yield on the 10-year TIPs, the inflation-protected bonds, has climbed largely in step with the regular 10-year bond (see chart below). In other words, investors aren’t demanding a greater inflation discount for their bonds. They just want a higher yield.

The influence of the Fed does show up in the middle part of the yield curve. For example, the spread between the two- and three-year Treasuries was only 10 basis points on May 6. Now it’s up to 40 points. That’s probably investors factoring in a short-term rate increase down the road. Interestingly, spreads among longer-dated bonds have actually tightened up a bit.

This leads me to believe that the reason for the higher rates is an improving economy. The key fact in favor of this thesis is that the dollar has been fairly stable. If yields were rising as the dollar was falling, then I’d be more concerned. I’ve also been impressed by how economically cyclical stocks have held up, and that’s despite a weak market for tech stocks. We also got encouraging earnings reports this week from broad-based retailers like Best Buy ($BBY) and TJX ($TJX). Also, Home Depot ($HD) had a good report plus they raised guidance.

The most intriguing bit of evidence in favor of the stronger-economy view is that junk-bond spreads have narrowed. In an unusual twist, AA-rated bonds are now yielding less than AAA bonds. But that’s not due to the market’s irrationality (which we can never completely discount). Rather, it’s due to the fact that investors want the shorter maturities that AA bonds usually carry. So investors want still bonds; they’re simply less willing to get locked into long positions.

Mortgage rates have climbed as well, and I am concerned that that could disrupt the housing market. The recent reports, however, show that housing is doing quite well. Our Buy List member Wells Fargo ($WFC) made news this week when they announced they’re eliminating 2,300 mortgage jobs. But that’s due to a decline in refinancings, not fewer originations.

The takeaway for investors is to not be too concerned about any taper talk. Its influence on the market is easily overstated. If bond traders are right, the economy is due for a rebound later this year and into 2014. That will be very good for our Buy List. Now let’s turn to our recent earnings reports.

Medtronic Hits Earnings Consensus on the Nose

On Tuesday, Medtronic ($MDT) reported fiscal first-quarter earnings of 88 cents per share, which was in line with expectations. Revenues rose to $4.08 billion, which was $40 million short of estimates.

Shares of Medtronic pulled back after the earnings report, but I think it was a fine quarter. Demand for defibrillators was a bit weak, as was the demand for MDT’s InFuse bone-growth product. Interestingly, Medtronic said they’re planning to expand beyond medical devices and into health services. I think that’s a smart move.

Medtronic’s CEO, Omar Ishrak, said, “We delivered on the bottom line, overcoming a number of challenges through strong operating discipline.” The best news was that MDT reiterated its full-year forecast of $3.80 to $3.85 per share. That’s for fiscal 2014, which ends next April. They made $3.75 per share last year and $3.46 per share the year before. In June, Medtronic raised its dividend for the 36th year in a row. Business is still going well here, and I think they can easily hit their full-year guidance. Ishrak said they’re looking to generate $25 billion in free cash flow over the next five years. Medtronic remains a solid buy up to $57 per share.

Ross Stores Delivers a Solid Earnings Report

After the close on Thursday, Ross Stores ($ROST) showed very strong fiscal Q2 earnings of 98 cents per share. That was five cents better than Wall Street’s consensus. It was even better than Ross’s own projections. After the last earnings report in May, Ross said to expect Q2 earnings to range between 89 and 93 cents per share.

Quarterly sales rose 9% to $2.551 billion. The important metric for retailers, comparable-store sales, rose 4% last quarter. That’s a very good number. ROST’s CEO, Michael Balmuth, said, “Operating margin for the second quarter grew to a record 13.6%, up from 12.8% in the prior year.” For Q2, Balmuth said he sees earnings coming in between 75 cents and 78 cents per share. That’s below Wall Street’s consensus of 79 cents per share, but Balmuth noted that it’s a cautious outlook.

For Q4, Ross sees earnings ranging between 99 cents and $1.03 per share. Wall Street had been expecting $1.10 per share. The guidance for Q3 and Q4 is based on comparable-store sales growth of 2% to 3%, which is very conservative. Add it all up, and Ross sees full-year earnings of $3.80 to $3.87 per share. Note that last year’s fiscal year included 53 weeks. Adjusting for that, Ross is projecting earnings growth of 11% to 13%.

This was an excellent quarter for Ross. Don’t let the tepid forecast bother you. They’re just being conservative. Ross Stores is an excellent buy up to $70 per share.

Before I go, I want to highlight three especially good buys on our Buy List. Ford ($F) looks very good below $17. The stock actually dipped below $16 earlier this week. The last earnings report was outstanding. Cognizant Technology ($CTSH) is a very good buy if you can get it below $73 per share. The recent earnings report and guidance was also very good. Keeping with tech, Microsoft ($MSFT) is a bargain below $33 per share. The stock currently yields 2.84%, and you can expect a dividend increase next month.

That’s all for now. Next week is the final week of summer. It went by fast, didn’t it? I expect trading activity to remain subdued until after Labor Day. On Monday, the census Bureau will report on durable orders. The report will come on Wednesday, when the government will revise the Q2 GDP growth numbers. The initial report was a sluggish 1.7%, but the subsequent trade numbers suggest a strong upward revision. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: August 23, 2013

Eddy Elfenbein, August 23rd, 2013 at 6:29 amU.K. Economic Growth Accelerates to 0.7%

Emerging Stocks’ Emerging Problems

U.S. Jobless Claims Fell to Five-Year Low Over Past Month

Treasuries Head for Second Weekly Decline Before New Home Sales

Nasdaq Shuts Trading for Three Hours After Computer Error

Alibaba Said to Seek HKEx Approval for Partners to Control Board

Icahn Says He Will Meet With Apple’s Cook on Buyback

UPS Drops Health Benefits for Spouses in U.S.

ABN AMRO Posts Fall in Profit as Provisions Rise

J.C. Penney Will Use A Poison Pill To Guard Against Another Bill Ackman

Electric Carmaker Tesla Hits Roadblock In China Over Trademark

Xiaomi (Or ‘The Apple Of China’) Is The Most Important Tech Company You’ve Never Heard Of

Big Brands Race To Secure Luxury Supplies From Reptiles To Roses

Jeff Carter: NASDAQ Shuts Down

Credit Writedowns: How QE’s Potential Unwind Reveals The Existence Of The Currency Wars

Be sure to follow me on Twitter.

-

Turn Those Machines Back On!

Eddy Elfenbein, August 22nd, 2013 at 2:33 pmThe NASDAQ is still down.

-

Can You Tell Something Went Wrong?

Eddy Elfenbein, August 22nd, 2013 at 12:45 pmCheck out the intra-day chart of Facebook ($FB). Starting at noon, it completely flatlines. The volume also dried up.

Trading Halted in Nasdaq Securities

U.S. stock exchanges on Thursday halted trading in all securities listed on the Nasdaq Stock Market NDAQ because of a technical issue, exchange officials said.

Nasdaq OMX Group Inc. announced the halt at 12:15 p.m. ET Thursday, and other exchanges followed suit. Nasdaq also said it was halting trade in its options markets. A spokesman for Nasdaq declined further comment.

Notices of halts in individual securities started to cross the wire at about 12:18 p.m. ET in alphabetical order by ticker symbol, starting with the exchange-traded fund iShares MSCI All Country Asia Information Technology ETF, ticker AAIT.

The issue stemmed from a data feed that provides market data for Nasdaq-listed securities, the exchanges said in notices sent to traders.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His