Archive for September, 2014

-

CWS Market Review – September 26, 2014

Eddy Elfenbein, September 26th, 2014 at 7:05 am“The stock market is designed to transfer money from the active to the patient.”

– Warren BuffettThis market continues to be dominated by the strong U.S. dollar. This is a very important point that all investors need to understand. There’s barely a sector of the market that’s not being impacted by the rallying greenback. The difference is that lately, the market’s no longer going higher.

On Thursday, the stock market had its second-biggest drop in the last 24 weeks. The S&P 500 lost 1.62% to close at 1,965.99. That’s a five-week low. The Dow slipped below 17,000, and the Nasdaq Composite was especially hard hit. That index closed below 4,500 for the first time since mid-August.

It was only one week ago that the market reached its “Alibaba Peak.” Last Friday morning, the S&P 500 touched its all-time intra-day high of 2,019.26, and 122 minutes later, Alibaba made its market debut. That may not be a coincidence.

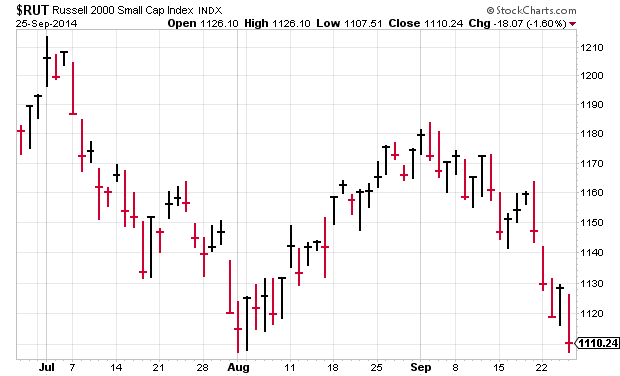

On Thursday, the dollar index broke out to a four-year high, and you can see the evidence everywhere. The yield spread between U.S. and German bonds reached a 15-year high. Gold dropped below $1,210 per ounce for the first time this year, and the small-cap Russell 2000 Index is now down 8.1% since July 3.

In this week’s CWS Market Review, I want to take a closer look at an important issue that has been driving the stock market: share buybacks. For years, Corporate America has been buying back its own shares at an impressive pace. Now, however, the buyback party looks to be coming to an end—and that might be good news. I’ll explain why in a bit.

Later on, we’ll take a look at the solid earnings report from Bed Bath & Beyond. The home-furnishings stores leaped more than 7% on Wednesday after they reported strong quarterly earnings. Speaking of buybacks, a few weeks ago, BBBY went to the bond market to borrow money so they could buy back gobs of their shares, and that’s what helped drive their earnings success. Or I should say their earnings-per-share success. We’ll also take a look at Medtronic’s tax inversion and the dividend increase from McDonald’s (their 38th in a row). But first, let’s look at what’s driving all these buybacks.

Why Share Buybacks Are Beginning to Fade

Anyone else remember when companies used to have lots of shares outstanding? Every quarter, the number of shares has slowly been getting smaller. More and more companies have been using their cash hordes to repurchase their own shares. The benefit for shareholders comes down to simple math. Having fewer shares helps your earnings-per-share, and investors like that. Howard Silverblatt, the main stat guy at S&P, notes that 295 companies in the S&P 500 reduced their share count last quarter.

On one hand, fewer shares is a good thing for investors, as it makes their holdings more valuable. But my take is that I’d prefer to see companies use their cash to expand their operations. That’s the best way to reinvest shareholder money: grow the business. But I can’t fault companies for buying back so much stock. What’s the point of keeping your cash in the bank, where you’d get 0.01%? After all, stocks are cheap and buyback announcements make for great PR.

I have two major complaints with share buybacks. One is that companies shouldn’t be in the stock market game. It’s a great idea to buy back a stock that’s cheap, assuming it rallies later on. But a lot of companies have tossed enormous sums of money at very expensive stocks, only to watch those assets fall. Cisco Systems is a perfect example. Remember a bank called Lehman Brothers? They used to be in the news a lot a few years ago. Anyway, Lehman spent $1 billion buying its own stock during the six months leading up to May 2008. I wince whenever I think about that. The Economist notes, “In all, America’s financial sector repurchased $207 billion of shares between 2006 and 2008. By 2009 taxpayers had had to inject $250 billion into the banks to save them.”

I’m also leery of companies sitting on too much cash. Peter Lynch has referred to this as the “Bladder Theory of Corporate Finance.” Even Apple got complaints from investors like Carl Icahn and David Einhorn for the size of its cash position, and it´s promised to return more money to shareholders. I also don’t like how many companies issue huge amounts of stock options for executive compensation, but they use share buybacks to mask how much they’re diluting their share base. There are exceptions like DirecTV which actually reduce their share count.

But we need to consider the fact that buybacks are popular with investors. Merrill Lynch found that companies with the largest buybacks crushed the market last year. But this year, the biggest repurchasers are performing nearly the same as the rest of the market. Actually, slightly worse. Perhaps, buybacks have lost their cool.

That could be the case. There are early indications that the buyback fever is fading. In Q2, companies in the S&P 500 bought back $116.2 billion worth of stock. That’s a decrease of 1.6% over last year, and a drop of 27.1% from Q1. Of course, stock prices are higher as well.

But that’s not all. Ironically, this could be an optimistic sign, because it means that companies are spending more money on growing their operations. Or, as crazy as this may sound, actually giving raises to their employees! When the financial crisis hit, buybacks were a no-brainer. Also, companies tend to be conservative with their dividend increases because it looks especially bad if you have to cut them later on. It’s generally assumed that a company will maintain its current dividend indefinitely.

There´s basic economics at work here. The U.S. economy has added close to nine million jobs in the last five years (we’ll get another jobs report next week). Those new jobs are an investment in a company’s future, and it’s encouraging to see firms take a more optimistic view of their future. A few days ago, Tesla said it’s building a new battery factory in Nevada. In response, the stock soared. In retrospect, the buyback craze was a result of low prices, low interest rates and a dragging economy. That’s coming to an end, and so, too, is the buyback frenzy. Now let’s take a look at a slumbering Buy List stock that’s taken full advantage of share buybacks.

Bed Buyback & Beyond

After the closing bell on Tuesday, Bed Bath & Beyond ($BBBY) reported earnings for its fiscal second quarter. Earnings announcements have been rather nerve-wracking for the home-furnishings chain; the stock has plunged after the last three earnings reports.

I’m pleased to say that that streak has come to an end. Shares of BBBY jumped more than 7.4% on Wednesday after Bed Bath & Beyond reported quarterly earnings of $1.17 per share. The company had previously said that earnings would range between $1.08 and $1.16 per share. Last week, I said that I expected earnings in the top end of that range, so the results were even better than I was expecting.

What’s interesting about BBBY’s earnings is the impact of buybacks. The company has been gobbling up its own shares at a furious pace. Net earnings fell 10.2% from the same quarter one year ago; however, there were 10.7% fewer shares. Presto! Earnings-per-share rose.

Bed Bath & Beyond recently floated a $1.5 billion bond offering to fund its share buybacks. Last quarter, BBBY spent $1 billion to buy back 16.9 million shares. Working out the math, that means they paid less than $60 per share on average, so they’re already in the money. Once again, it’s basic economics. The bond deal cost BBBY 4.38%, so it’s not exactly a back breaker. In fact, Standard & Poor raised their rating on Bed Bath & Beyond to AAA- from BBB+.

I’ve often said that I’m not a big fan of share buybacks, but I’ll give credit to BBBY for being another firm that´s actually reducing its share count. The company isn’t finished with buybacks either. There’s still another $1.8 billion remaining in the current buyback program. BBBY projects its share count will fall by another 13 million by the end of the fiscal year.

Bed Bath & Beyond gave us guidance for Q3 and Q4. For the third quarter, which ends in November, Bed Bath sees earnings ranging between $1.17 and $1.21 per share. For Q4, which is the all-important holiday season, they see earnings ranging between $1.78 and $1.83 per share. For the entire year, their earnings forecast is $5.00 to $5.08. BBBY sees comparable-store sales rising by 2% to 3% in Q3 and 4% to 5% in Q4.

The full-year forecast is the first time they’ve given us a specific EPS range, but it exactly comports with the “mid-single-digits” language they’ve used for several months. Not once have they budged from that forecast. Since the company made $4.79 per share last year, the current EPS guidance translates to annualized growth of 4.4% to 6.1%.

Adding up the two quarterly guidance ranges gives us a full-year range of $5.04 to $5.13. I’m probably reading too much into that, but it’s something to note. Overall, this was a solid quarter for BBBY. The stock remains a good buy up to $70 per share.

Medtronic Down on Tax-Inversion Rules

This week, Medtronic ($MDT) learned an important lesson that many of us have known for a long time—you simply can’t become Irish because you feel it. Shares of MDT dropped close to 3% on Tuesday, and still more on Wednesday and Thursday, after the government announced new rules for “tax inversions.” That’s what Medtronic is trying to do as it buys Ireland’s Covidien ($COV) and moves its HQ to the Emerald Isle. The move would cut their tax bill by a good amount.

I’ll be honest with you—I don’t know what impact the new rules will have on the MDT/COV deal, and it sounds like no one else knows at this point either. The lawyers are still looking it over. The key issue is a company’s holding of cash outside the United States. In Medtronic’s case, they hold close to $14 billion outside the country. Medtronic wants to loan some of that to their new parent, but the new rules might stop that.

Bloomberg reported that Medtronic released a statement saying, “We are studying the Treasury’s actions. We will release our perspective on any potential impact on our pending acquisition of Covidien following our complete review.” Don’t let the recent sell-off rattle you. Medtronic remains a buy up to $67 per share.

McDonald’s Raises Its Dividend for the 38th Year in a Row

I wanted to say a quick word about McDonald’s ($MCD), which has been a problem child this year. The company has been trying to right itself after several missteps. The results don’t yet reflect this, and the last sales report was truly terrible.

In the CWS Market Review from three weeks ago, I said I was concerned that Mickey D’s wouldn’t raise their dividend this year. I’m pleased to say that that wasn’t the case. Last week, McDonald’s announced that they’re raising their quarterly dividend from 81 to 85 cents per share. The burger giant aims to return $18 billion to $20 billion to shareholders from 2014 through 2016. The new dividend is payable on December 15 to shareholders of record as of December 1. Going by the new dividend and Thursday’s closing price, McDonald’s now yields 3.61%. McDonald’s remains a conservative buy up to $101 per share.

Two more things to mention. DirecTV ($DTV) shareholders approved the AT&T merger with 99% of the vote. Also, Cognizant Technology Solutions ($CTSH) is very cheap at the moment. The shares are at a seven-week low. If you can pick up CTSH below $45, that’s a very good purchase.

That’s all for now. The third quarter comes to a close next Tuesday. After that, we’ll get the important turn-of-the-month economic reports. The September ISM report comes out on Wednesday. There’s a chance it could hit a 10-year high. Also on Wednesday, we’ll get the ADP jobs report. Then on Friday will be the official jobs report from the government. The last report was on the weak side. I doubt that’s the start of a trend. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: September 26, 2014

Eddy Elfenbein, September 26th, 2014 at 6:26 amEuro at Lowest Since 2012 on Draghi’s Dovish Comments

Draghi’s Trillion-Euro Pump Finds Blockage in Spain

S&P Upgrades India Rating Outlook

Modi Faces U.S. Damages Case Over Gujarat Riots

Russia: Putin’s Power Politics

Dollar Stands Tall; Asian Shares End Week on Low Note

A Year Later, Most Mega IPOs Are Mega Laggards

S&P Dow Jones Indices Says Alibaba to Be Added to China-50 Index

Difficult Decision For Yahoo: What Should It Do With Proceeds From Alibaba Share Sale?

Banana Group Fyffes Offers Chiquita Bigger Slice of Merger Deal

How Nike, Inc. Just Sprinted Past Expectations

Boards Of Hyundai Motor Affiliates Approve Signing Of $10 Billion Land Deal

BlackBerry Reports Smaller Quarterly Loss

Michael Pettis: On the Global Economy and Economics

Joshua Brown: Stocks Take Off Their Beer Goggles

Be sure to follow me on Twitter.

-

Dollar Hits Four-Year High

Eddy Elfenbein, September 25th, 2014 at 2:56 pmThe strong dollar keeps getting stronger. The yield spread between U.S. and German bonds reached a 15-year high. The dollar index just hit a fresh four-year high today:

-

Morning News: September 25, 2014

Eddy Elfenbein, September 25th, 2014 at 6:52 amChina Considering Replacing Central Bank Head

Lithuania Feels Squeeze in Sanctions War With Russia

Mars Mission: Investors See ‘Mangalyaan Success’ as India Growth Story Model

U.S. New-Home Sales Surge 18% in August

Wal-Mart Really Wants To Be Your Bank, Retailer Launches Mobile Checking Account

Apple CEO Cook Goes From Record Sales to IPhone Stumbles

SEC Probe Adds to Pimco’s Troubles

H&M Third-Quarter Profitability Declines on Garment Costs

Can Pilots Cause Air France KLM To Crash?

BP: Has the Stock Market Overreacted?

U.S. Online-Education Company Udacity Raises $35 MIllion for ‘Nanodegrees’

Cullen Roche: “The Passive/Active Distinction is About Cost”

Jeff Carter: What Important Truth Do Very Few People Agree With You On?

Be sure to follow me on Twitter.

-

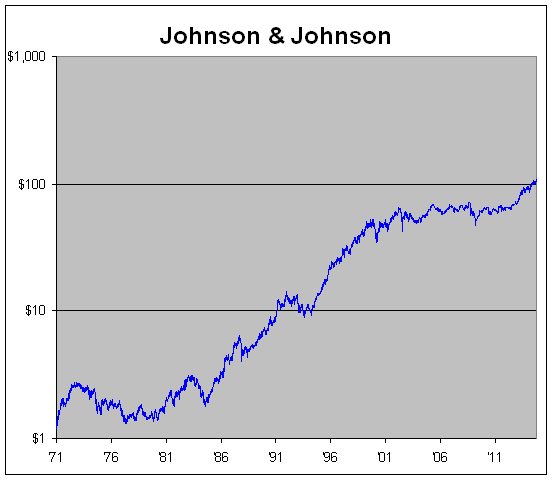

Johnson & Johnson Hits New All-Time

Eddy Elfenbein, September 24th, 2014 at 5:42 pmMany healthcare stocks have been doing quite well lately. I just noticed that Johnson & Johnson ($JNJ) closed at a new all-time high today of $108.54. I’ve followed JNJ for many years (and it used to be on our Buy List), I’ve noticed that is has traditionally split its shares when it has gotten close to $100 per share. We may see a split announcement soon.

I think it’s interesting to note that JNJ went nowhere for more than 10 years. It hit a high in March 2002, and it was still trading below that in June 2012. But that was a great time to buy.

JNJ’s long-term record is amazing. On May 26, 1970, JNJ was going for 78 cents per share (that’s adjusted 48-for-1 in stock splits). That’s a gain of nearly 140 fold in 44 years, which does include dividends.

-

Highlights for BBBY’s Conference Call

Eddy Elfenbein, September 24th, 2014 at 11:56 amThere was a lot of good info in yesterday’s earnings call with Bed Bath & Beyond. Seeking Alpha has the transcript here, but I wanted to post some highlights. This is a scatter shot of different quotes from different people:

Standard & Poor’s has raised our credit ratings to single A-minus from Triple B+, which speaks to the strength of our company and our future prospects.

Net sales for the fiscal second-quarter or approximately $2.9 billion, approximately 4.3% higher than in the prior year net sales of approximately $2.8 billion. Of this increase, approximately 78% is attributable to the increase in comp sales and approximately 22% is primarily from new stores offset by a decrease in shipping income.

Second-quarter comparable sales increased by approximately 3.4% compared with an increase of 3.7% last year.

Turning to the balance sheet, during the second-quarter we received $1.5 billion from the notes offering of which $1.1 billion was subsequently used to fund our accelerated share repurchase program, which commenced during the second-quarter, and is expected to be completed before the end of the calendar year.

During the second-quarter, we completed our previous $2.5 billion share repurchase program, which was approved in 2012 and began to repurchase shares under our new $2 billion authorization program approved in July 2014. This new authorization had a remaining balance of approximately $1.8 billion at the end of the quarter and which we currently plan to complete during fiscal 2016.

Turning to the remainder of the year, our current models for each quarter and full-year include the following; one, for the fiscal third quarter, we are modeling comparable sales to increase in the range of 2% to 3%. For the fourth quarter, we are modeling comparable sales to increase in the range of 4% to 5%. This will bring the modeled full-year comp sales to a range of 2.6% to 3.1%.

We are modeling diluted weighted average shares outstanding to be approximately 184 million for the third quarter, 178 million for the fourth quarter, and 189 million for full year.

Based on these and other planning assumptions, we are modeling net earnings per diluted share to be approximately $1.17 to $1.21 for the third quarter, and approximately $1.78 to $1.83 for the fourth quarter bringing the full-year modeled net earnings per diluted share to a range of $5 to $5.08.

Here are the sales and earnings figures for the past few quarters:

Quarter Sales Gross Profit Operating Profit Net Profit EPS May-99 $356,633 $146,214 $28,015 $17,883 $0.06 Aug-99 $451,715 $185,570 $53,580 $33,247 $0.12 Nov-00 $480,145 $196,784 $50,607 $31,707 $0.11 Feb-00 $569,012 $238,233 $77,138 $48,392 $0.17 May-00 $459,163 $187,293 $36,339 $23,364 $0.08 Aug-00 $589,381 $241,284 $70,009 $43,578 $0.15 Nov-01 $602,004 $246,080 $64,592 $40,665 $0.14 Feb-01 $746,107 $311,802 $101,898 $64,315 $0.22 May-01 $575,833 $234,959 $45,602 $30,007 $0.10 Aug-01 $713,636 $291,342 $84,672 $53,954 $0.18 Nov-02 $759,438 $311,030 $83,749 $52,964 $0.18 Feb-02 $879,055 $370,235 $132,077 $82,674 $0.28 May-02 $776,798 $318,362 $72,701 $46,299 $0.15 Aug-02 $903,044 $370,335 $119,687 $75,459 $0.25 Nov-03 $936,030 $386,224 $119,228 $75,112 $0.25 Feb-03 $1,049,292 $443,626 $168,441 $105,309 $0.35 May-03 $893,868 $367,180 $90,450 $57,508 $0.19 Aug-03 $1,111,445 $459,145 $155,867 $97,208 $0.32 Nov-04 $1,174,740 $486,987 $161,459 $100,506 $0.33 Feb-04 $1,297,928 $563,352 $231,567 $144,248 $0.47 May-04 $1,100,917 $456,774 $128,707 $82,049 $0.27 Aug-04 $1,273,960 $530,829 $189,108 $120,008 $0.39 Nov-05 $1,305,155 $548,152 $190,978 $121,927 $0.40 Feb-05 $1,467,646 $650,546 $283,621 $180,980 $0.59 May-05 $1,244,421 $520,781 $150,884 $98,903 $0.33 Aug-05 $1,431,182 $601,784 $217,877 $141,402 $0.47 Nov-06 $1,448,680 $615,363 $205,493 $134,620 $0.45 Feb-06 $1,685,279 $747,820 $304,917 $197,922 $0.67 May-06 $1,395,963 $590,098 $148,750 $100,431 $0.35 Aug-06 $1,607,239 $678,249 $219,622 $145,535 $0.51 Nov-07 $1,619,240 $704,073 $211,134 $142,436 $0.50 Feb-07 $1,994,987 $862,982 $309,895 $205,842 $0.72 May-07 $1,553,293 $646,109 $154,391 $104,647 $0.38 Aug-07 $1,767,716 $732,158 $211,037 $147,008 $0.55 Nov-08 $1,794,747 $747,866 $203,152 $138,232 $0.52 Feb-08 $1,933,186 $799,098 $259,442 $172,921 $0.66 May-08 $1,648,491 $656,000 $118,819 $76,777 $0.30 Aug-08 $1,853,892 $739,321 $187,421 $119,268 $0.46 Nov-08 $1,782,683 $692,857 $136,374 $87,700 $0.34 Feb-09 $1,923,274 $785,058 $231,282 $141,378 $0.55 May-09 $1,694,340 $666,818 $142,304 $87,172 $0.34 Aug-09 $1,914,909 $773,393 $222,031 $135,531 $0.52 Nov-09 $1,975,465 $812,412 $245,611 $151,288 $0.58 Feb-10 $2,244,079 $955,496 $370,741 $226,042 $0.86 May-10 $1,923,051 $775,036 $225,394 $137,553 $0.52 Aug-10 $2,136,730 $874,918 $296,902 $181,755 $0.70 Nov-10 $2,193,755 $896,508 $305,110 $188,574 $0.74 Feb-11 $2,504,967 $1,076,467 $461,052 $283,451 $1.12 May-11 $2,109,951 $857,572 $288,948 $180,578 $0.72 Aug-11 $2,314,064 $950,999 $371,636 $229,372 $0.93 Nov-11 $2,343,561 $958,693 $357,020 $228,544 $0.95 Feb-12 $2,732,314 $1,163,669 $550,765 $351,043 $1.48 May-12 $2,218,292 $887,199 $313,398 $206,836 $0.89 Aug-12 $2,593,015 $1,032,669 $365,137 $224,330 $0.98 Nov-12 $2,701,801 $1,074,010 $361,649 $232,750 $1.03 Feb-13 $3,401,477 $1,394,877 $598,034 $373,872 $1.68 May-13 $2,612,140 $1,032,971 $323,101 $202,490 $0.93 Aug-13 $2,823,672 $1,113,484 $389,766 $249,304 $1.16 Nov-13 $2,864,837 $1,121,690 $374,647 $227,197 $1.12 Feb-14 $3,203,314 $1,297,437 $527,073 $333,299 $1.60 May-14 $2,656,698 $1,030,885 $300,701 $187,052 $0.93 Aug-14 $2,944,905 $1,134,045 $368,741 $223,953 $1.17 -

Morning News: September 24, 2014

Eddy Elfenbein, September 24th, 2014 at 7:15 amDraghi Helps Halt European Stock Sell-Off; Oil Slips

German Business Confidence at Lowest Level in Over a Year, Ifo Survey Shows

RBS’s Citizens Arm Raises $3 Billion in U.S. IPO Below Range

Treasury’s Clampdown on Tax Inversions Takes Bite Out of Share Prices

Dallas Fed Hires Search Firm to Find Fisher Replacement

Yellen Warns on Market Calm Before ’Considerable Time’ Up

Impact of Home Depot Breach on Rise

PayPal Takes Baby Step Toward Bitcoin, Partners With Cryptocurrency Processors

GM Expects to Sell Over 3 Million Cars in China This Year

Air France Low-Cost Europe Plan Withdrawn, Minister Says

Where Profit Margins Are Hefty, Online Upstarts Muscle In

Pimco Total Return ETF Drawing SEC Scrutiny, WSJ Reports

Soda Makers Pledge to Cut Calories 20% By 2025. Is It Too Late?

Howard Lindzon: Robinhood…The Future of Mobile Brokerage

Cullen Roche: Warren Buffett Is Right To Hate Gold

Be sure to follow me on Twitter.

-

Bed Buyback & Beyond!

Eddy Elfenbein, September 23rd, 2014 at 4:55 pmEarnings are out for Bed Bath & Beyond ($BBBY) and they were quite good. The company earned $1.17 per share last quarter. If you recall, the home furnishings company had given us a range of $1.08 to $1.16 per share, so they beat their own estimates.

The reason for the earnings beat is quite simple—they bought back a ton of shares. Last quarter, the company bought back $1 billion worth of stock, or 16.9 million shares. Net earnings fell 10%, but earnings-per-share increased by one penny.

For fiscal Q3, which ends in November, the company sees earnings ranging between $1.17 and $1.21 per share. They also gave us fiscal Q4 guidance of $1.78 to $1.83 per share (you can see how important the holiday shopping season is for them).

For the entire year, BBBY sees earnings coming in between $5.00 and $5.08 per share. Looking at the two separate quarterly guidance ranges adds up to $5.04 to $5.13 per share. The stock is currently up $5.01 to $67.70 per share in the after-hours market. That’s a gain of 8%.

-

Medtronic Down on Tax Inversion Rules

Eddy Elfenbein, September 23rd, 2014 at 1:52 pmMedtronic ($MDT) is learning a lesson today that many of us have known for a long time—you simply can’t become Irish because you feel it. Shares of MDT are down after the government announced new rules for “inversions.” That’s what Medtronic is trying to do as it buys Ireland’s Covidien and move its HQ to the Emerald Isle. The move would cut their tax bill by a good amount.

I’ll be honest with you-I don’t know what impact the new rules will have on the MDT/COV deal. And it sounds like no one else knows at this point either. The lawyers are still looking it over.

The key issue is a company’s holding of cash outside the United States. In Medtronic’s case, they hold close to $14 billion outside the country. Medtronic wants to loan some of that to their new parent, but the new rules might stop that.

Bloomberg reported that Medtronic released a statement saying, “We are studying the Treasury’s actions. We will release our perspective on any potential impact on our pending acquisition of Covidien following our complete review.”

-

Equity Versus Assets

Eddy Elfenbein, September 23rd, 2014 at 10:59 amI wanted to discuss an important topic that’s often misunderstood by investors, and that’s the difference between equity and assets.

When new investors look at the list of things to invest in, they tend to see it as a giant list of similar options; stocks, bonds, commodities, forex, real estate and so on. But this blurs an important point which is that stocks are unique. There’s no other class quite like them.

All other assets are things. They just sit there. If you buy some gold and leave it alone, in 50 years it will still be there, just sitting there. There are income-producing assets like bonds and real estate, which makes them a little better than commodities. But still, they’re just things. They can neither think nor create.

Equity, on the other hand, is wholly different. It’s a legal entity by which people can come together and employ said assets to make goods and services for people. It’s almost analogous to looking at the difference between a pile of car parts and a fully assembled car. The business works to make a profit, and it keeps investing those profits in the business to make still more profits.

Some trader right now is investing in, say, copper. I wish them well. But remember that copper has no independent value. By itself, it’s just an element. Not to get too philosophical, but copper’s entire value is based on what it can do for us. What are the goods and services it can enhance? For that to happen, copper needs to pass though the hands of a business.

This is why long-term studies of what’s been the best investment usually have stocks at the top, followed by bonds and real estate followed by commodities. When you’re investing in a company, you’re really investing in human ingenuity—the way that people can come together and figure out how to make something useful from those assets.

Real estate, for example, is a nice investment. I hope everyone owns their own home. But in the long run, real estate will never, ever, ever, ever outpace stocks. Never. This isn’t just my opinion, it’s reality. It won’t happen because it can’t happen.

A house is simply an asset. No matter how hard it tries, it will never be anything more than an asset. A house does its job by just sitting there. But a stock is different. A stock is part ownership in a corporation. A corporation is people using assets to create wealth. This ain’t just a matter of definitions.

You can buy a share of stock of a company that can buy a house. A house can’t invest in a corporation. You can form a corporation and issue stock. With the proceeds, you can do cool things, like…buy a house and rent it for profit. After a while, you’ll have enough money to buy another house. Then another and another. Soon, you’ll have a nice stable of houses. That’s what businesses do—they grow. If they don’t grow, they’re replaced by businesses that do. It’s that simple, and a house can never do that.

-

Archives

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His