CWS Market Review – October 6, 2017

“A bull market is like sex. It feels best just before it ends.” – Barton Biggs

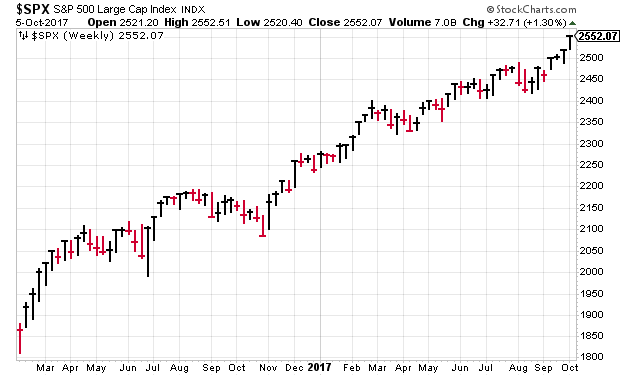

It feels like I’m running out of ways to describe how calm and steady this market has been. This is truly one of the most remarkable markets in history.

Consider just a few stats. Since the election, the Dow has made 83 record closes. The S&P 500 has now risen for eight days in a row, and 16 times in the last 19 sessions. The index has gone 22-straight days without a daily fall of more than 0.3%. Historically, those days happen about 30% of the time, and we haven’t seen one in 22 days. The S&P has also run 17-straight days of closing, up or down, by no more than 0.5%. Thursday was the index’s sixth-straight all-time high.

Not only are we at all-time highs, but volatility has nearly melted away. On Thursday, the Volatility Index, otherwise known as the VIX, closed at an all-time low of 9.19. It’s been lower on an intra-day basis, but Thursday was the lowest close ever. This is just amazing.

In this week’s CWS Market Review, we’ll take a closer look at the baby-step rally and what it means for us. I’ll also cover the recent earnings report from RPM International. They beat expectations and gave investors their 44th-consecutive annual dividend increase. Not many stocks have done that. I’ll also have some updates on our Buy List stocks. But first, let’s look at the calm, cool and record-high stock market.

Doing Nothing Is the Smartest Thing to Do

I was invited on CNBC’s Trading Nation on Thursday. We usually do three segments, one of which is live on the air; the other two go up on the Internet. In one of the taped segments, the host, Eric Chemi, asked me about the market’s volatility and what investors ought to do about it.

I was stumped for a moment because you’re expected to give some insightful perspective on whatever the subject is. In this instance, the answer is simple: keep doing what you’re doing. Just stay with your stocks and don’t get scared out of anything. I told the host that investors shouldn’t “overthink” this market. Just lie back and think of capital gains.

I apologize if this advice isn’t terribly interesting or earth-shattering, but nothing is what you should be doing right now. Go do it. Luckily, we have many good positions on our Buy List, and the market has definitely swung our way in recent weeks. Since August 24, our Buy List is up 5.98% while the S&P 500 is up 4.64%. As I said, this won’t last forever.

This is a broad generality, but awful markets don’t spring directly on the heels of good markets. Rather, the market’s biggest plunges have typically come when stocks are already sliding. The market performs much better than average when it’s already at an all-time high. Also, volatility tends to be much lower. Bad markets create volatility, not the other way around.

Stock market be all pic.twitter.com/IWowiol3o7

— Eddy Elfenbein (@EddyElfenbein) October 5, 2017

I want to highlight a few currents running just beneath the surface of this market. For example, financial stocks have done quite well over the last month (we also talked about this on CNBC). For example, Bank of America just touched its highest price since 2008 (it’s still less than half its 2007 high).

Obviously, the changing perception of what the Fed will do in December is a major factor helping bank stocks. Also, a lot of the big banks haven’t done so well since the start of the year, so they’re playing catch up. This week we saw cycle-high yields for both the one- and two-year Treasuries. This is typically the area of the yield curve that’s most sensitive to interest rates. The one-year yield is up to 1.35%. Three years ago, it was at 0.10%.

Even better than the big banks are the regional banks. My favorite in this area continues to be Signature Bank (SBNY). The New York-based institution got a modest rebound recently, but it’s still below $130 per share. I think it’s possible for SBNY to earn $10 per share next year.

For the most part, this has been a balanced rally lately. Of course, many big energy stocks are a long way from their new highs. The key sectors in recent weeks have been Materials, Tech, Industrials and Financials. Healthcare has also been doing well.

The big standout has been the small-cap arena. The Russell 2000 has roared to life over the last several weeks. This rally is part of a trend that started last year. In less than 20 months, the Russell 2000 is up close to 60%. The even smaller small-caps, the micro-caps, have been en fuego. Charlie Bilello points out that the Micro-cap ETF (IWC) has been down only three times in the last 33 days. At one point, IWC was up 18 days in a row.

One of the weak areas of this market has been Consumer Staples. In fact, Staples have lagged since early 2016, right at the same time small-caps started to soar. Part of this is clearly a shunning of defensive areas in favor of a little more risk. Defensive names usually shine when things are rough. After all, when the economy drops, folks don’t really cut back on their purchases of Campbell Soup. Instead, they don’t buy cars or homes or go on vacations.

Here’s the small-cap Russell 2000 (black), the large-cap S&P 500 (gold) and the Consumer Staples ETF (blue):

I like Consumer Staples for the steadiness of their business, but I have to concede that this is a bad part of the cycle for them. Stocks like Hormel Foods (HRL) and Smucker (SJM) are near the bottom of our Buy List this year. It’s tough to do well when you’re a quality player but your sector is not in favor. I still like these stocks, but we won’t see any improvement until the cycle turns, and that’s usually when things start looking bad for the economy.

Some Buy List stocks that look particularly good right now include Signature Bank (SBNY), Danaher (DHR), Alliance Data Systems (ADS) and Stryker (SYK). Remember to pay attention to our Buy Below prices. Now let’s look at our first Buy List earnings report in several weeks.

RPM International Raises Dividend for the 44th Year in a Row

On Wednesday, RPM International (RPM) reported fiscal Q1 earnings of 86 cents per share. That was two cents above expectations.

“We derived significant benefits from the nine acquisitions made in fiscal 2017, along with our selling, general and administrative (SG&A) cost-reduction actions taken last year. Rising raw-material costs negatively impacted gross profit margins. As a result, we instituted price increases, which began to take effect late in the quarter. After three years of foreign-currency headwinds attributable to the strengthening U.S. dollar, currency translation was essentially neutral this quarter,” stated Frank C. Sullivan, RPM chairman and chief executive officer.

This was for their fiscal Q1, which ended in July. Previously, RPM said they were expecting Q1 earnings ranging between 83 and 85 cents per share, so the company is doing a bit better than expectations.

When RPM originally made that forecast, it disappointed investors. Wall Street had been expecting 89 cents per share for Q1. So in retrospect, the company wasn’t only three cents short of the original forecast.

In July, RPM said they expected earnings for the fiscal year between $2.85 and $2.95 per share. That was below Wall Street’s expectation of $3 per share. RPM reiterated their $2.80 to $2.95 range this week.

On Thursday, RPM announced a 6.7% dividend increase. In last week’s issue, I said I was expecting a modest increase, but this one is pretty decent. The quarterly dividend will rise from 30 to 32 cents per share. This is RPM’s 44th annual dividend in a row. That’s quite a streak.

Shares of RPM pulled back a bit after the earnings report. At one point on Friday, RPM got to $50.29 per share, although it recovered some lost ground. Going by Thursday’s close, the new dividend yields 2.48%. Using the mid-point of the company’s earnings forecast, the shares are going for 17.8 times this fiscal year’s earnings.

I’m keeping my Buy Below at $55 per share. RPM is a good stock, but it will take some time to shine.

Buy List Updates

There hasn’t been much news on Buy List, but I wanted to make a few adjustments. In last week’s issue, I mentioned the recent rally in shares of Ross Stores (ROST). The deep discounter usually reports fiscal Q3 earnings just before Thanksgiving. This week, I’m going to raise my Buy Below on Ross to $68 per share. I expect to see good numbers from Ross this holiday season.

One of our surprising winners lately has been Cinemark (CNK). I say surprising because the stock collapsed during August, but it has roared back lately. Cinemark got a boost this week when an analyst at Morgan Stanley upgraded the movie chain. He said that fears of a box-office slowdown are overblown. I’m lifting my Buy Below on Cinemark to $41 per share.

I also want to raise my Buy Below on Moody’s (MCO). In July, Moody’s crushed expectations by 17 cents per share. They also raised their full-year guidance range to $5.35 to $5.50 per share. That was an increase of 20 cents per share at both ends. MCO is now a 50% winner for us this year.

When the last earnings report came out, I raised my Buy Below to $141 per share. Moody’s just broke that this week. I’m now lifting my Buy Below on Moody’s to $151 per share.

That’s all for now. While many government offices will be closed on Monday in honor of Columbus Day, the stock market will be open. Some of the early earnings reports will be coming next week as well. On Wednesday, we’ll get a look at the minutes from the last Fed meeting. On Friday, we’ll get a look at the retail-sales report and consumer inflation last month. I’ll be curious to see if we’re anywhere close to the Fed’s 2% target. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on October 6th, 2017 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His