CWS Market Review – March 23, 2018

“There are two kinds of people who lose money: those who know nothing, and those who know everything.” – Henry Kaufman

The stock market took a big bath on Thursday. At 2 p.m., the Dow was down about 250 points, but after that, things got really bad. By the closing bell, the Dow had lost 724.42 points. The S&P 500 closed at 2,643.69 which is its lowest level in six weeks.

On Monday, I was on CNBC’s “Closing Bell.” I got a chance to expand on an important point I made in last week’s issue. The recent attack on free trade, combined with the defenestration of Facebook and the blocking of some high-profile mergers, aren’t disparate events. Rather, these are part of a single trend which is a fundamental change to the economic order that has prevailed since the end of the Cold War.

I think the effect of this is starting to spook Wall Street. Free trade and market liberalization simply don’t hold the clout they used to. I’m not saying this is right or wrong, but it is something profound that’s taking place, and investors need to understand the change.

In this week’s CWS Market Review, I’ll explain what I mean. I’ll also look at this week’s Fed meeting. For the sixth time this cycle, the Fed decided to raise interest rates. Real rates are all the way up to nearly 0%. Before we get to that, let’s look at this week’s paroxysm.

Tariffs Slam Wall Street

On Monday, the S&P 500 dropped 1.42% for its worst day in several weeks. What’s interesting about Monday’s market action is that our Buy List largely sidestepped the damage. The big loser of the day was Facebook while several other social media stocks felt the heat. However, our Buy List lost -0.74%. A single day’s outperformance of 68 basis points is quite good. More importantly, it highlights a growing gap between overvalued “story” stocks and the high-quality ones we favor.

The riskier sectors of the market are very fragile. Consider that the S&P 500 Tech Sector has underperformed for the last five days in a row. I don’t think this will stop. I have to stress how distorted the market has become. On Monday, nearly two-thirds of the stocks in the S&P 500 managed to outperform the index. That shows the huge impact of a small group of very large stocks.

None of this is being helped by the Trump administration’s tariff policy. On Thursday, the Trump administration said it will impose stiff tariffs on Chinese imports. The goal is to narrow our trade deficit with China. The president has said that the tariffs could be as much as $60 billion.

The administration had previously announced tariffs on steel and aluminum. Those will go into effect today. On Thursday, metal stocks were very big losers. US Steel lost 11% in the day’s trading. Fortunately, we don’t have any steel, copper or aluminum stocks on our Buy List, so we’re safe there.

Unfortunately, we do have a few cyclical stocks like Signature Bank (SBNY), Sherwin-Williams (SHW) and Wabtec (WAB), and those got dinged on Thursday. The inflated areas of the market still look quite risky, and this includes many tech names.

This week, the Justice Department urged a judge to block the merger between AT&T and Time-Warner. As with political matters, I won’t say if this is good or bad, but it will make other companies think twice before planning a big merger. This also comes on the heels of the dissolution of the Broadcom/Qualcomm merger. Not that long ago, no one would have batted an eye at these mergers. Not so any more.

Let me highlight a few bargains on our Buy List. Alliance Data Systems (ADS) has been sinking like a stone. The stock is currently going for less than 10 times its projected earnings for this year. My Buy Below on ADS is currently $252, but if you can get it below $225, you’ve gotten a good deal. Carriage Services (CSV) also looks good here. The shares are going for less than 14 times forward earnings. Finally, let me put in a kind word for Check Point Software (CHKP). The cybersecurity stock is attractive below $105 per share.

For the Sixth Time this Cycle, the Fed Hikes Interest Rates

On Wednesday, the Federal Reserve decided to raise interest rates. Their target for the Fed funds rate is now 1.50% to 1.75%. Adjusted for inflation, that’s still negative, but only by a little bit. This latest increase wasn’t exactly a surprise; it was widely expected on Wall Street. This is the Fed’s sixth rate increase of this cycle.

What makes this latest policy statement interesting is that the Fed sounded more upbeat on the economy. Specifically, the Fed said, “the labor market has continued to strengthen and that economic activity has been rising at a moderate rate.” Unfortunately, wage gains have been pretty mediocre, but at least they’re rising. The good news is that inflation continues to be contained although there have been some hints that the rate of inflation may be accelerating.

This Fed meeting was also noteworthy because it’s the first one with Jay Powell as chairman. This week’s meeting was followed by a press conference with Chairman Powell. I’ll give him points for being far more direct than either Yellen or Bernanke. Powell is a lawyer by training whereas the two former Fed chairs are professors. Academics, especially those in Econ, love to hedge their answers. Alan Greenspan once said, “I guess I should warn you, if I turn out to be particularly clear, you’ve probably misunderstood what I’ve said.” We won’t be hearing that from Powell. Interestingly, Powell’s press conference was also the shortest post-meeting conference on record.

With this meeting, the Fed also released its economic projections for the next few years. I’ll caution you that the Fed isn’t very good at predicting things. Still, their outlook is influential. The Fed sees the economy growing, in real terms, by 2.7% this year and 2.4% next year. That’s an increase from their December forecast which saw the economy rising by 2.5% this year and 2.1% in 2019. I suspect that’s probably due to tax reform.

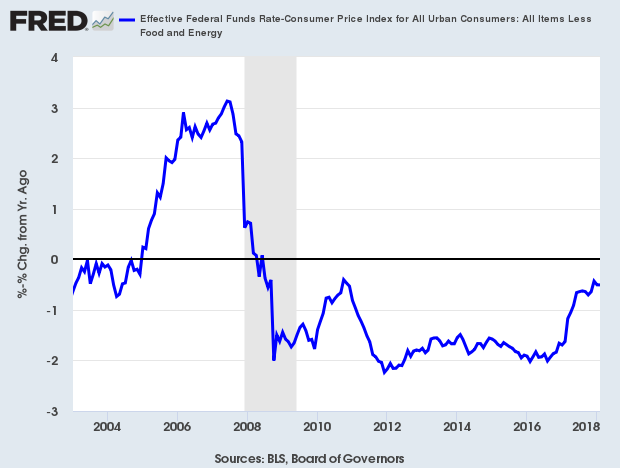

Here’s a look at the inflation adjusted Fed funds rate:

The Fed sees the unemployment rate dropping from the current level of 4.1% to 3.9% by the end of this year and then to 3.6% (!) by the end of next year. If the Fed is right on this last point, then it would be the lowest unemployment rate since the 1960s. Despite the brighter outlook, the Fed kept its inflation outlook basically unchanged. In other words, the Fed sees itself as handling the economy brilliantly over the next few years.

Now here’s where it gets interesting. The Fed is almost evenly split on the outlook for rate hikes for this year. Eight FOMC members think we’ll need no more than two hikes this year while seven think we’ll need at last three more. The futures market sees another hike coming in June, then another in September, and that’s it for this year.

After that, the median FOMC voters see two more hikes in 2019. If that’s right, then it would mean we’ll finally hit the “neutral rate” 21 months from now. To boil it all down, we’re still a long way from a recession.

The three best indicators for looking at a recession are initial jobless claims, the real Fed funds rate and the yield curve. Initial jobless claims are still very low. The real Fed Funds rate is higher but still below neutral. The yield curve has narrowed, but it’s still positive. The bottom line is that there’s no imminent worry of a recession.

FactSet’s Earnings Preview

FactSet Research Systems (FDS) is due to report Q2 on Tuesday, March 27. The company is a data provider for the investment community. That’s a surprisingly profitable business. Three months ago, FDS reported Q1 earnings of $2.04 per share. That was six cents better than Wall Street’s consensus. The downside is that their revenue came in a little light. Wall Street had been expecting $331.2 million. Instead, it was only $329.1 million.

The poor revenue news caused the stock to take a tumble. The lower share price helped convince me that it was a good opportunity to add it to our Buy List. I’m glad we did. FDS has been a nice winner for us this year (except for on Thursday).

The good news in the Q1 report is that FactSet said they expect full-year earnings to range between $8.25 and $8.45 per share, on revenue of $1.34 to $1.36 billion. For Q2, Wall Street expects earnings of $2.06 per share. I think that’s a bit too low. I’m expecting something between $2.08 and $2.11 per share, but I won’t be too concerned if I’m off by a few pennies.

One factor I’ll be watching is FactSet’s operating margin. More often than not, a healthy operating margin is the hallmark of a strong company. For Q1, FactSet’s adjusted operating margin dropped to 31.7% from 33.0% in the Q1 one year prior. The company blamed the lower margin on restructuring costs. I hope to see this metric stabilize.

FactSet is currently trading above our $202 Buy Below price. I want to see the earnings report before I decide to adjust our Buy Below price.

Buy List Updates

Two of our Buy List stocks split 2-for-1 this week. On Monday, AFLAC (AFL) split 2-for-1. This means shareholders got twice as many shares, and the share price roughly fell by half. Then on Tuesday, it was Fiserv’s (FISV) turn to split. Technically, the split goes into effect on the trading day before, as the new shares are distributed after the close.

For tracking purposes, I assume the Buy List is a $1 million portfolio that’s equally weighted at the start of the year. For AFLAC, I’m adjusting our starting price to $43.89 per share. Also, the number of shares will double from 455.6847 to 911.3694. For Fiserv, I’m adjusting the starting price to $65.565 per share and the number of shares doubles to 610.0816.

Our Buy Below prices for both stocks split as well. AFLAC is now a buy up to $47 per share, and Fiserv is a buy up to $72 per share.

On Wednesday, shares of General Mills got hit hard after a lousy earnings report. The problem for us is that took down shares of Smucker (SJM) and Hormel Foods (HRL). This is typical Wall Street thinking. They assume that if one company in a sector is having issues, then they all are. In this case, that’s simply not true with either stock. A few weeks ago, Hormel met earnings and raised guidance and their dividend. It was Hormel’s 52nd consecutive annual dividend increase. Also, Smucker beat earnings and raised guidance.

That’s all for now. Next week is the final trading week of the first quarter. The stock market will be closed on March 30 for Good Friday. This is the one day of the year when the market is closed but most businesses are open. The biggest report will be the final revision to Q4 GDP. That’s due out on Wednesday. Then on Thursday, we’ll get the reports on personal income and spending for February. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Syndication Partners

I’ve teamed up with Investors Alley to feature some of their content. I think they have really good stuff. Check it out!

Buy This 17% High-Yield Stock Selling at a Temporary Discount

Last week a Federal Energy Regulatory Commission (FERC) ruling sent the MLP and energy infrastructure stocks into a tailspin. The news release caused an immediate 10% drop in the MLP indexes. Prices recovered to close at a 5% decline. A closer read of the facts shows the fears were overblown and this steep drop may end up in hindsight as the MLP sector’s equivalent of the March 2009 bottom of the last stock bear market.

Here is the scary headline from Bloomberg:

Pipeline Stocks Plunge After FERC Kills Key Income-Tax Allowance

The reality is that the ruling only applies to interstate (not intrastate, which is most pipeline miles) pipelines and to just one of the methods a pipeline company can use to set interstate transport rates.

In the bigger picture, MLP values have been falling since late January. Over the same period companies in the sector reported 2017 fourth quarter results that were very positive. MLP fundamentals have been improving for several quarters, and the trend will continue as North American oil and gas production continues to grow.

If you own quality MLPs that have fallen in value, it is a good time to add more to your positions. In my Dividend Hunter newsletter, my primary MLP recommendation is the InfraCap MLP ETF (NYSE: AMZA). This ETF pays monthly dividends which benefit from option selling by the fund managers. After the big FERC fueled drop, AMZA yields over 17%. See here to find out more.

Dump These 3 Steel Stocks as Tariff’s Rip Up the Industry

The imposition of a 25% tariff on imported steel by President Trump has certainly been a headline grabber. But it obscures the long-term problems faced by the U.S. steel industry.

And it only addresses one side of the classic economic equation for any commodity – supply and the industry’s struggle against cheap imports. The share of the U.S. steel market taken by imports was only 26.9% in 2017, up slightly from 2016’s level of 25.4%.

I expect the benefits of the tariffs to the steel companies to disappear as quickly as a morning fog on a hot summer day.

This makes the stocks of the steel companies un-investable or, if you have a high risk tolerance, outright shorts. Especially at these elevated price levels, which seemed to have all the possible good news already factored in. That’s why you should sell these three steel stocks without delay.

Posted by Eddy Elfenbein on March 23rd, 2018 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His