CWS Market Review – October 26, 2018

“The best time to invest is when you have money.” – John Templeton

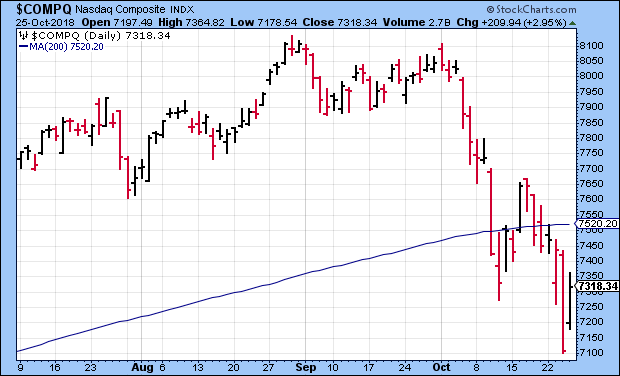

In last week’s issue, I warned you: “the storm hasn’t passed. We’re due for some more turbulence soon.” And indeed, more turbulence came. On Wednesday, the S&P 500 fell more than 3%, and the Nasdaq plunged 4.4% for its worst day in seven years.

Wall Street is still on pins and needles. Moreover, we’re right in the middle of third-quarter earnings season. This was a very busy week for our Buy List earnings reports; we had seven reports this week. Most of our reports are beating expectations, but we had an earnings miss from Sherwin-Williams plus an earnings warning from Ingredion. I’ll fill you in on the details in just a bit.

This will be a packed issue. First, I’ll summarize what’s been freaking out Wall Street. I’ll then cover all of our Buy List earnings reports, and I’ll preview next week’s reports (another seven!). There’s a lot to cover, so let’s dive right in.

Riding Out the October Storm

The recent market sell-off has many different causes, but the most important is higher interest rates from the Federal Reserve. From that, there are several ripples that are impacting the markets.

The most prominent effect has been on the housing market. Mortgage rates recently touched a seven-year high. As a result, marginal buyers are pushed out of the market. This week’s new-homes sales report was a total dud. The number for September was lousy, and on top of that, the previous three months were all revised lower. Some of that can be blamed on the hurricanes, but not all of it. In the last year, new-home sales are down 13%.

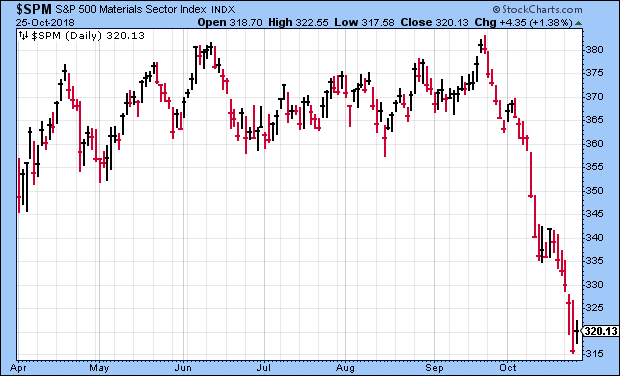

We can see the impact on the stock market by looking at housing-related stocks. (Later on, I’ll discuss the earnings miss from Sherwin-Williams.) The Housing ETF (XHB) has been in free fall. Also, the S&P 500 Materials Sector (XLB) has been dropping like a stone. Remember that housing touches many different industries like flooring, construction, paint, home security, wire, tools, some retail and mortgages.

Closely related to the drop in housing has been the weakness in REITs and regional banks. The Regional Bank ETF (KRE) has been lagging badly. The local real-estate market tends to weigh heavily on regional banks. What’s interesting is that we’re watching a near mirror-image of the Trump Rally after the 2016 election. All the sectors that soared after the election are doing poorly, while the ones that were left behind are now doing better (or less badly). As a group, stocks with high volatility have been getting crushed, while more stable stocks are leading. The recent divide between High Beta and Low Vol may be the most outstanding feature of the market this month.

By the way, some commentators have been discussing the Tech sector as if it’s been thrown out the window. Eh…not really. Tech, as a whole, has been holding up better than many other areas.

The damage to the market this month has been impressive. Until Thursday, the S&P 500 fell 13 times in 15 sessions. The index went 74 days in a row without a 1% change in either direction. In the last 12 days, it’s happened seven times. I’ll warn you that Thursday was a classic “contra-trend” move. That’s when the market makes a big move in either direction and sprinkled in are a few days that are the complete opposite of what’s been happening. The days tend to be dramatic and misleading as the current trend reasserts itself. Eventually, however, all trends come to an end.

Let me add some words of caution. I’m not a believer that the housing cycle is over. I’m more inclined to believe this is just a rough few months and that we’re still on the way up. I suspect that fears of a housing bust have an outsized hold on Wall Street’s mind. Given the events of ten years ago, I certainly understand, but we’re not anywhere close to a situation like that.

For the near term, we’re not yet in the clear. Don’t expect the Fed to alter its course. The key to watch is the 200-day moving average. Once we clear that for a few days, then I expect things to settle down. This may take a few weeks to sort out, but our stocks will continue to be an oasis. On Wednesday’s big down day, our Buy List outpaced the S&P 500 by more than 1%. When investors get scared, they flock to quality. Now let’s look at some earnings news.

Six Earnings Reports This Week

We had three Buy List earnings reports on Wednesday. Before the bell, Check Point Software (CHKP) reported Q3 earnings of $1.38 per share. That was two cents above Wall Street’s estimates. Revenues were $471 million. The company had told us to expect Q3 earnings between $1.30 and $1.40 per share and revenue between $454 million and $474 million.

Check Point also said it bought Dome9 in order to boost its position in cloud security.

“Third quarter results reached the top end of our projections, with better than anticipated strength coming from the US and Europe,” said Gil Shwed, Founder and CEO of Check Point Software Technologies. “Today we announced the acquisition of Dome9. This new addition to Check Point’s Infinity architecture delivers enhanced Cloud Security with advanced active policy enforcement and multi-cloud protection capabilities. The combination of Dome9 and Infinity CloudGuard product family further differentiates Check Point in the rapidly evolving Cyber Security environment,” Shwed concluded.

On the earnings call, the company said it expects Q4 earnings of $1.56 to $1.67 per share on revenue of $500 million to $528 million. Wall Street had been expecting $1.65 per share on revenue of $515.29 million. Check Point remains a buy up to $120 per share.

After the close on Wednesday, AFLAC (AFL) reported Q3 earnings of $1.03 per share which was four cents better than estimates. The yen averaged ¥111.48 during the quarter, so thankfully the exchange rate didn’t have a big impact on their numbers.

For Q3, AFLAC had been expecting earnings of 87 cents to $1.02 per share (a wide range), which assumed an exchange rate of ¥110 to ¥115 to the dollar. So far this year, AFLAC has made $3.11 per share. That’s a 19.6% increase over last year.

Now for guidance. AFLAC sees itself coming in at the “high end” of its previous guidance, which was $3.90 to $4.06 per share. That assumes an exchange rate of ¥112.16 to the dollar.

If by “high end” AFLAC means $3.98 to $4.06 per share, then that means they see Q4 coming in between 87 cents and 95 cents per share. Wall Street had been expecting 96 cents per share. I think the Street expected them to raise guidance. I’m dropping AFLAC’s Buy Below to $47 per share.

Also after Wednesday’s close, Torchmark (TMK) reported Q3 operating earnings of $1.59 per share. That beat Wall Street’s forecast of $1.53 per share. That’s up from $1.23 one year ago.

Now for guidance. Torchmark sees 2018 earnings between $6.08 and $6.14 per share. That implies Q4 earnings of $1.51 to $1.57 per share. Wall Street had been expecting $1.56 per share.

Torchmark also gave initial guidance for next year. Torchmark sees 2019 ranging between $6.45 and $6.75 per share. The consensus on Wall Street was for $6.56 per share. Torchmark is a buy up to $91 per share.

Thursday morning, we got our first earnings miss. Sherwin-Williams (SHW) said it made $5.68 per share for Q3. That was seven cents below Wall Street’s estimate. Sales rose 5% to $4.73 billion.

Here’s what the CEO had to say:

Revenue growth slowed from the pace set in the second quarter, due primarily to slower growth in some North American architectural businesses, a sequential slow-down in some of our industrial businesses in China and Europe and unfavorable currency translation rate changes. The price increases implemented over the past 12 months have largely kept pace with accelerating raw material inflation on a consolidated basis, but some of our Performance Coatings businesses continue to lag in that effort. During the quarter, our Global Supply Chain team incurred incremental costs in an effort to keep pace with load-in demand during what is traditionally our peak sales volume quarter.

Business is still doing well for Sherwin. EBITDA from continuing operations is up 16.9% so far this year. Sherwin also lowered the upper end of its full-year guidance range to $19.05 to $19.20. The previous range was $19.05 to $19.35 per share. I’m lowering our Buy Below to $400 per share.

After the bell on Thursday, Cerner (CERN) reported Q3 earnings of 63 cents per share which matched Wall Street’s consensus. Q3 revenue rose 5% to $1.34 billion.

For Q4, Cerner expects revenue between $1.37 billion to $1.42 billion. The midpoint of that range is 6% growth. For Q4 earnings, Cerner expects 62 to 64 cents per share. That’s a little weaker than I had been expecting. Wall Street was at 67 cents per share. Cerner’s outlook puts its full-year forecast at $2.45 to $2.47 per share. Cerner is a buy up to $67 per share.

Stryker (SYK) reported Q3 earnings of $1.69 per share which was at the top of its previous range of $1.65 to $1.70 per share. Organic sales rose 7.9%. Impressively, Stryker increased its operating margin to nearly 25%.

For Q4, Stryker expects $2.13 to $2.18 per share. For all of 2018, Stryker sees earnings between $7.25 and $7.30 per share. That’s an increase of three cents to both ends of their previous guidance. I like this stock a lot. Stryker remains a buy up to $181 per share.

The last Buy List earnings report this week is from Moody’s (MCO). The company is due to report later this morning. The credit-rating agency had a very good report three months ago. Moody’s recently reaffirmed its full-year EPS guidance of $7.65 to $7.85. For Q3, the consensus on Wall Street is for $1.78 per share. I’ll cover the report on the blog.

Seven More Buy List Reports Next Week

On Tuesday, two of our Buy List stocks are due to report. After its last earnings report, shares of Cognizant Technology Solutions (CTSH) got punished by the market. In July, CTSH was over $82 per share, and recently it’s been near $70 per share, yet business has been good.

For Q3, CTSH expects earnings of at least $1.13 per share, and for all of this year, it expects at least $4.50 per share. Earlier this year, CTSH lowered its full-year EPS guidance from $4.53 to $4.47. So they’ve reclaimed some of that lost ground.

Shares of Wabtec (WAB) have been sagging lately. The stock got dinged last month after JP Morgan questioned some of the assumptions behind the GE deal. The company responded with a press release stating that the merger deal “continues to make progress,” and that they expect it to be complete by early 2019.

Wabtec then amended their proxy, noting that they expect to see a minor adjustment in revenue and EBIT for next year. They’re still standing by their financial estimates for the deal. Wall Street expects Q3 earnings of 95 cents per share.

Then on Wednesday, we’ll get three more reports. Frankly, Carriage Services (CSV) has been a disappointment this year. The last earnings report wasn’t that good. Their current outlook, however, is fairly optimistic. I want to see better results from them soon. For Q3, Wall Street expects 22 cents per share.

This summer, Fiserv (FISV) reiterated its full-year range of $3.02 to $3.15 on internal revenue growth of at least 4.5%. Since Fiserv has already made $1.51 per share for the first half, the guidance means they expect $1.51 to $1.64 per share for the second half. In September, the board authorized a buyback of 30 million shares of stock. That’s about 7.5% of their outstanding shares. It’s our top stock this year. For Q3, Wall Street expects 77 cents per share. I’m expecting a beat.

Intercontinental Exchange (ICE) is a very good company, and they had a good earnings report three months ago. ICE doesn’t offer EPS guidance, but they said they expect Q3 data revenue between $530 million and $532 million. For Q4, it’s expected to be between $538 million and $542 million. One item impacting the business has been the recent battle over market data fees. I’ll have more on that next week. For Q3, Wall Street expects earnings of 80 cents per share.

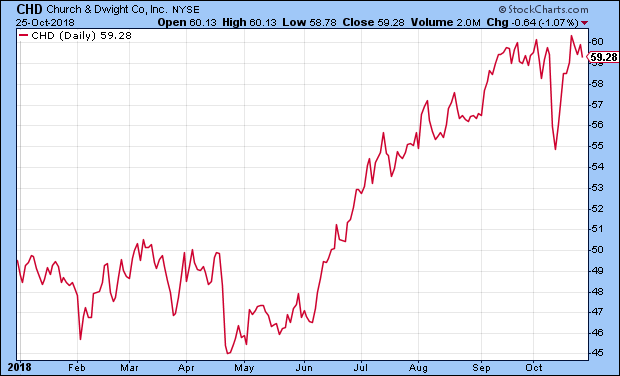

On Thursday, there are two Buy List reports. Church & Dwight (CHD) had a good Q2 earnings report over the summer. For Q3, CHD expects 53 cents per share and $2.26 to $2.28 for the year. Not only has CHD been stable in this market, but the shares made a new high last week.

On Monday, Ingredion (INGR) warned that Q3 earnings will be about $1.70 per share. Wall Street had been expecting $1.96 per share. Previously, Ingredion had stood by its full-year guidance of $7.50 to $7.80 per share. Now INGR expects $6.80 to $7.05 per share. On Monday, the stock dropped 7.6%.

Ingredion blamed weak currencies in developing markets plus power outages in North America. The company said it will require more than one quarter to recover. I’m not pleased with this stock.

Before I go, I wanted to make two adjustments to our buy prices of stocks that reported last week. I’m lowering the Buy Below for Alliance Data Systems (ADS) to $221 per share. I’m also dropping Signature Bank (SBNY) to $118 per share.

That’s all for now. More earnings to come next week. We’ll also get several key economic reports. Personal income and spending comes out on Monday. Tuesday is consumer confidence and Case-Shiller. Wednesday is the ADP payroll report. On Thursday, we get the ISM report, plus construction spending. Then on Friday is the big one—the October jobs report. The report for September showed the lowest unemployment rate in nearly 50 years. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. I’ll be on talking markets on Bloomberg later today. The segment runs from 3:50 pm to 4:10 pm ET.

Posted by Eddy Elfenbein on October 26th, 2018 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His