CWS Market Review – April 5, 2019

“Investing isn’t about beating others at their game. It’s about controlling yourself at your own game.” – Benjamin Graham

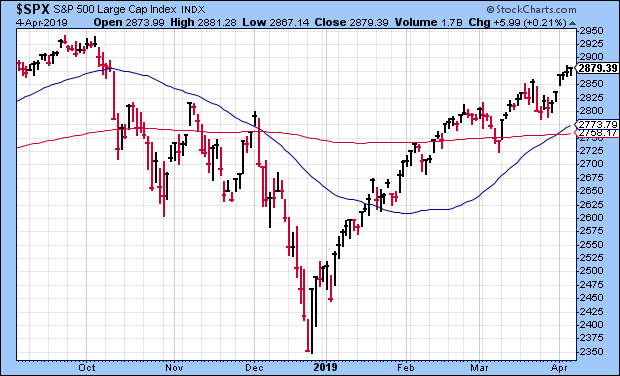

T.S. Eliot famously wrote that “April is the cruelest month.” Actually, as far as stocks go, it’s been pretty good. The market has risen 12 times over the last 13 Aprils. Plus, April 2019 has gotten off to a solid start. This builds upon a very good start to the year. We just wrapped up the best first quarter for stocks in 21 years.

That could be a good omen. Consider that of the last 19 times that each of the first three months of the year were higher, 18 times the rest of the year was green as well. The only exception came in 1987.

During the day on Wednesday, the S&P 500 got as high as 2,885. That’s a six-month high. In fact, we’re not that far from an all-time high. The dividend-adjusted S&P 500 came within 0.5% of making a new all-time high. (Dividends are small, but they do add up!)

The market has now rallied for six days in a row. Despite the rebound in share prices, I have to confess that there’s not a lot going on in the stock market right now. Each week, I strive to bring the latest and greatest on Wall Street, but it’s been quite dead lately.

We’re in that odd lull before earnings season. In just a few days, we’ll have all the news we can bear. But for right now, it’s crickets out there. Don’t fret. In this week’s CWS Market Review, we’ll take a look at some recent economic data. I’ll also run through the new earnings report from RPM International. Plus, I’ll cover some news impacting our Buy List stocks. But first, let’s review some mildly weak economic news.

The U.S. Economy May Be Stagnating

In recent weeks, there’s been more talk about the possibility of an interest-rate cut by the Federal Reserve. Larry Kudlow, the president’s top economic advisor, said the Fed should cut rates immediately by 0.5%.

Until now, I’ve been a doubter, and I still think it’s a long shot. But I’ve become somewhat less doubtful. What’s the reason? Well, some recent economic news has been noticeably tepid. The standout example is the February jobs report. According to the government number crunchers, the U.S. economy created just 20,000 net new jobs in February. That was way below expectations.

I’m writing this to you on Friday morning, so the March jobs report may already be out by the time you’re reading this. That report includes a revision to the numbers from February, and it’s likely the revision is higher.

But that’s not the only data. For example, the weekly jobless-claims report got weaker at the start of this year. The weakness seemed to coincide with the government shutdown, so it caused a major uproar. Sure enough, on Thursday, we learned that initial jobless claims fell to 202,000. That’s the lowest since the 1960s.

On Wednesday, the ADP payroll report said that just 129,000 private sector jobs were created last month. That’s the lowest figure in 18 months. For the first time since December 2016, goods-producing jobs shrank. It’s possible that the labor market is beginning to stagnate as global growth is softening.

That’s probably what’s driving the talk of a rate cut. What’s interesting is that the yield curve isn’t exactly flat. Rather, it has a notch. At the moment, yield on the six-month Treasury exceeds the yield on the three-year by 16 basis points. That’s very unusual, and it only makes sense if bond traders expect a short-lived rate cut in a larger tightening cycle.

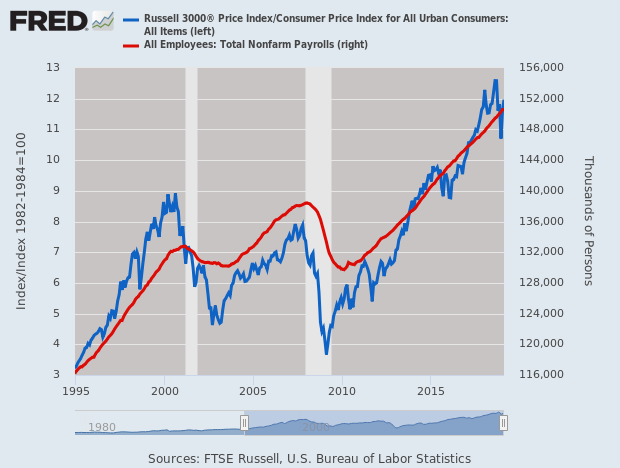

Here’s a chart of nonfarm payrolls (red) with the Russell 3000 adjusted for inflation (blue).

Last week, the government lowered its estimate on Q4 GDP growth. The initial report said the U.S. economy grew by 2.6% in the last three months of 2018. The updated report lowered that figure to 2.2%. That basically puts Q4 right in line with the trend of the current expansion. The economic recovery is notable for its length and its meandering speed. Compared with previous recoveries, the current one hasn’t been particularly strong.

On Monday, the ISM Manufacturing Index was reported to be 55.3 for March. That’s up from 54.2 in February, but that report was the lowest in six months. A recession usually aligns with an ISM reading somewhere in the mid-40s. On Wednesday, the Non-Manufacturing Index fell to 56.1 for March. That’s down from 59.7 for February. That was below expectations, and the lowest point since August 2017.

As I mentioned before, there hasn’t been much happening on Wall Street this week, but that will soon change. Next Friday, earnings season will kick off when JPMorgan and Wells Fargo report earnings. As we stand at the beginning of earnings season, the wave of lower guidance seems to have passed. Since September, Wall Street analysts had chopped this year’s earnings estimate for the S&P 500 by 5% to $167.80. Apple and the Energy sector were key drivers in the lower estimates. Analysts now expect to see top-line growth of 4.4% and an earnings decline of 9.8%.

The week after next, the first of our Buy List stocks will report. Between mid-April and early May, 20 of our 25 Buy List stocks will report earnings. I don’t have the complete list yet, but Eagle Bancorp (EGBN) will report on April 17; then Danaher (DHR) and Check Point (CHKP) will report on the 18th. There will probably be others. Overall, I expect more good results from our stocks. On Thursday, we got the latest off-cycle earnings report from a Buy List stock, and it was quite good.

RPM International Is a Buy up to $65 per Share

In last week’s issue, I confessed that RPM International (RPM) has been a disappointment this year. The January earnings report was a dud, and the company had some (to my ears) tired excuses. Still, I’m not ready to pull the plug. The company owns a broad selection of well-known brands like Rust-Oleum.

The good news is that Thursday’s earnings report alleviated some of my concerns. For the third quarter of RPM’s fiscal year, the company earned 14 cents per share. That exceeds the company’s own range of 10 to 12 cents per share. I’ll note that Q3 is typically RPM’s slowest of the year. Quarterly sales rose 3.4% to $1.14 billion. For the year, sales are up 5.3%.

Frank Sullivan, RPM’s president and CEO, said, “Organic growth was 4.3% and acquisitions contributed 2.1%, while foreign exchange was a significant headwind that reduced sales by 3.0%. Price increases helped to offset higher raw-material costs, which have risen for seven straight quarters, as well as higher costs for freight, labor and energy. International markets remained challenged and resulted in reduced operating earnings from most geographies around the world.” The currency issue is a big problem for RPM.

The good news is that RPM provided a pretty optimistic forecast. The company sees Q4 earnings ranging between $1.12 and $1.16 per share. At one point on Thursday, shares of RPM gapped up nearly 8%. RPM eventually finished the day at $60.63 per share for a gain of 2%.

This is an encouraging report. The major concern is still the currency issue, but RPM doesn’t have much control over that. Remember that this is a solid outfit. RPM has increased its dividend every year for the last 45 years. This week, I’m raising my Buy Below on RPM International to $65 per share.

Buy List Updates

Earlier this week, shares of Raytheon (RTN) were downgraded by UBS. I usually ignore these news items, and I’m not going to bother refuting them. Still, the downgrade was enough to ping the shares for a 4% loss on Wednesday. The analyst lowered Raytheon from buy to neutral. (I’m not neutral on any stock!) He also lowered his price target from $220 to $200 per share, which is still a pretty juicy target. Anyway, I’m not concerned by the downgrade and am expecting good earnings later this month. Raytheon is a buy up to $190 per share.

This Thursday, April 11, is a big one for Disney (DIS). At 5 p.m. ET, Disney will have its Investor Day webcast. With the big Fox deal done, this is the day when Bob Iger is expected to map out Disney’s plans to take on Netflix. Goldman Sachs recently said, “it is the dawn of a new era at Disney.” That’s true.

Going into the meeting, there seems to be a lot of negative sentiment. Some folks think it will be bad news, and that may be what’s weighing on the share price. Personally, I have a more faith in Disney. Plus, with expectations so low, it may be easy to impress investors. Disney remains a buy up to $118 per share.

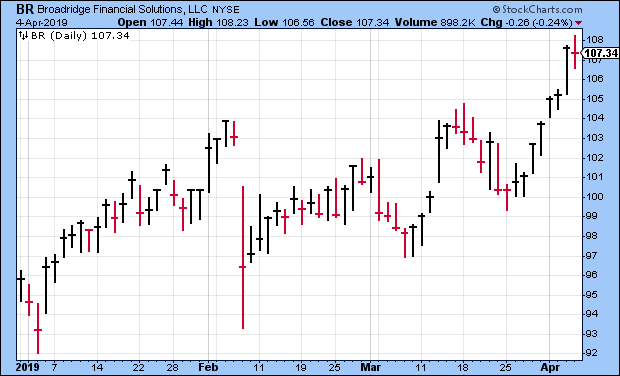

I’ve neglected discussing Broadridge Financial Solutions (BR), and that should change. In February, the shares got smacked down after a lousy earnings report. BR made 56 cents per share, 15 cents below expectations. Despite the big drop, Broadridge has gradually recovered, and the stock just hit a new YTD high.

The rally shouldn’t be too surprising. Broadridge has maintained a favorable outlook. The company said it sees earnings growth of 9% to 13% for this fiscal year, which is already half over. Since they made $4.19 per share last year, the guidance works out to $4.57 to $4.73 per share this year. For the current quarter, Broadridge sees revenue between $1.195 billion and $1.245 billion and earnings of $1.40 to $1.56 per share. Look for some improved results in May. This week, I’m raising my Buy Below on Broadridge Financial Solutions to $113 per share.

That’s all for now. There are a few key economic reports next week. On Monday, the factory-orders report comes out. On Wednesday, we’ll get the CPI report for March. Also on Wednesday, the Fed will release the minutes from its last meeting. The jobless-claims report comes out on Thursday. On Friday, the Q1 earnings season begins as JPMorgan and Wells Fargo are due to report earnings. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. I’ll be on Bloomberg TV’s market-wrap segment this Monday, April 8 at 3:50 pm ET.

Posted by Eddy Elfenbein on April 5th, 2019 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His