CWS Market Review – September 27, 2019

“Reality is merely an illusion, albeit a very persistent one.” – Albert Einstein

This week, House Speaker Nancy Pelosi announced a formal impeachment inquiry into President Trump. According to The New York Times, the inquiry will look at “charging him with betraying his oath of office and the nation’s security by seeking to enlist a foreign power to tarnish a rival for his own political gain.” As usual, I’ll skip the politics and focus on what it means for the stock market and our portfolio.

The simple answer is, “not much.” One of the mistakes investors make is to confuse what happens in the headlines with what concerns the stock market. The market has a mind of its own, and what it’s principally concerned with is earnings and interest rates. In the long run, it’s just earnings.

In this week’s issue, I’ll examine this important issue in more depth. I’ll also cover some recent economic news. We had a very good earnings report from FactSet. However, their guidance wasn’t so hot, and traders nailed the shares. I’ll tell you what it all means. I’ll also preview next week’s earnings report from RPM International. But first, let’s dig into Washington’s latest political brawl.

Don’t Be Scared of Impeachment Killing the Market

At least once a week, I get an email asking me if the stock market is about to crash because of something President Trump has done. I get similar emails asking the same question but about the Democrats.

I routinely remind investors to not let their political views upend their investing strategy. It’s not just amateurs who need this advice. In 2009, The Wall Street Journal famously ran an op-ed warning us that “Obama’s Radicalism Is Killing the Dow.” That article came at almost the exact low.

Folks on the left haven’t done much better. On election night in 2016, S&P 500 futures started plunging, leading Paul Krugman to write, “If the question is when markets will recover, a first-pass answer is never.” Not exactly. The futures were wrong, and the market started to rally.

I don’t mean to make fun of either side. It’s natural to think that what’s in the political news must impact the stock market, but that’s just not the way it works. I don’t mean to say that policy doesn’t impact the market. It certainly does, but it usually does so in unintended ways.

This week, I was invited on The Compound with my friends Josh Brown and Michael Batnick. I’ve been of a fan of theirs for a long time, and I never miss The Compound, so it was a thrill to go on. You can see the video here.

During our discussion, we talked about the potential impact of impeachment on the stock market. First, there’s the mathematical fact that even if President Trump is impeached by the House, he would probably be acquitted by the Senate because you need 67 votes to convict and the Senate is currently controlled by the Republicans.

On the issue of impeachment, we don’t have a lot of data points to work with. President Clinton was formally impeached by the House on December 19, 1998. The trial began in January, and President Clinton was acquitted on all counts on February 12, 1999.

The story is complicated because Russia defaulted in August 1998, and that led to the collapse of the hedge fund Long-Term Capital Management in September. That shook the market, and the S&P 500 closed below 1,000 on October 9.

After that, the stock market rallied right through the impeachment proceedings. The NASDAQ rallied especially hard, and within a few months, it became the famous tech bubble. Through it all, the impeachment proceedings had little impact on the markets. If people were worried, it didn’t show up in the averages.

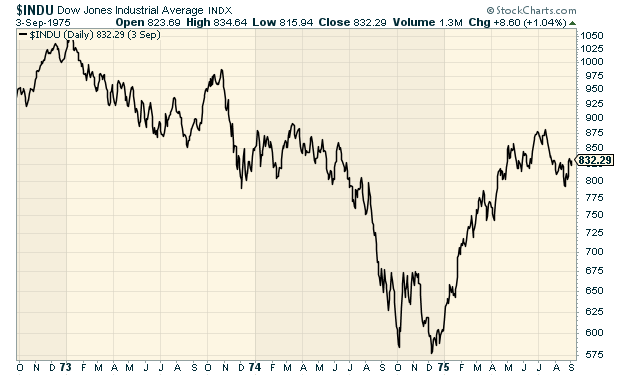

The case of Richard Nixon was more serious, even though he resigned before he was formally impeached. There were very serious events in 1973-74 like the OPEC oil embargo, the 1973 Yom Kippur War and the resurgence of inflation. On top of that, the U.S. officially entered a recession in December 1973.

The recession and inflation were probably good enough reasons for the market to flop, but there may also have been a concern that the President didn’t have the latitude to respond to any crisis. The bear market of 1973-74 was one of the worst on record. Investors hadn’t seen anything like it since the Depression. At that time, there were many market participants who had lived through the Great Depression.

If anything, Nixon’s resignation in August was closer to a buy signal, even though the Dow didn’t reach its low until December 6, 1974. On that day, the Dow closed at 577.60 which was its lowest point in the last 55 years (1964 to present). For context, the Dow lost more than that in one day three times last month.

In 1973-74, the threat of a nuclear war was real. There was talk of Soviet troops occupying the Golan Heights. At one point, U.S. forces went to Defcon 3. This was a scary time. That’s why Watergate’s impact on the market needs to be seen as part of many bad things happening at the same time.

In 2019, things are much calmer. This week, we got the final revision to Q2 GDP, and it showed real growth of 2%. That’s not great, but it’s moving in the right direction. The stock market has actually been rather calm lately. That may change once earnings season starts, but I doubt any news from Washington will take down the stock market.

Don’t let the noise from Washington rattle you. Our strategy is working just fine. Now let’s look at our one Buy List earnings report from this week.

FactSet Drops on Weak Guidance

On Thursday, FactSet (FDS) released a very good earnings report for its fiscal Q4. The problem was that their guidance for next year was pretty low.

Let’s start with the good news. For its fiscal Q4, FactSet said that revenues rose 5.3% to $364.3 million. Annual Subscription Value, or ASV, rose to $1.48 billion. Quarterly earnings rose 18.6% to $2.61 per share. Wall Street had been expecting $2.47 per share.

I was particularly glad to see FactSet’s operating margin come in at 33.9%. For the quarter, client count rose by 119 to 5,574. User count rose by 3,871 to 126,833. FactSet’s annual retention rate is running at 89%. The company now has 9,681 employees.

This was FactSet’s 39th year in a row of revenue growth and 23rd year in a row of EPS growth.

“FactSet performed well in full-year 2019, delivering solid revenue and strong EPS growth, despite market headwinds,” said Phil Snow, FactSet CEO. “To further our winning proposition in the marketplace, we will be accelerating critical investments over the next three years from a position of strength, capitalizing on industry trends and enhancing our core offerings. We are making investments today so that FactSet can continue to deliver long-term value for all our stakeholders.”

For the whole year, EPS rose to $10.00. Their guidance had been for $9.80 to $9.90 per share. Before that, it was $9.50 to $9.65 per share, so business has been humming along.

On its current guidance, FactSet is being very conservative. The company sees earnings next year (ending in August 2020) ranging between $9.85 and $10.15 per share. That’s basically no growth at all. The range is -1.5% to +1.5%. Wall Street had expected $10.52 per share.

FactSet sees revenues ranging between $1.49 billion and $1.50 billion. That’s up from $1.44 billion for the year that just ended.

Traders punished the stock, and by the closing bell, FDS was off by 9.3%. While this is frustrating, there’s no need for concern. The stock is back where it was six months ago (almost exactly). Despite the drop, FDS is up 22.78% for us this year.

This week, I’m lowering our Buy Below on FactSet to $265 per share.

Earnings Preview for RPM International

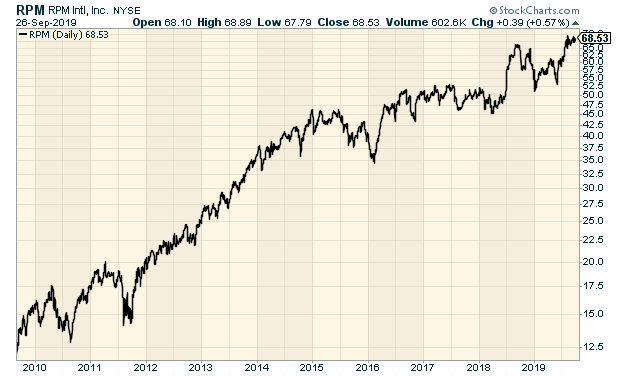

RPM International (RPM) is due to report on October 2. This will be for their fiscal Q1, which ended in August. The company owns a broad selection of well-known brands like Rust-Oleum.

The business outlook seems to be improving for RPM. For Q4, the company earned $1.24 per share which was 10 cents more than estimates. Net sales rose by 2.8% to $1.6 billion. Unfortunately, they were dinged a bit by forex, but you really can’t avoid that. The company sees 2020 earnings of $3.30 to $3.42 per share. For Q1, Wall Street expects earnings of 92 cents per share.

Even though RPM is a boring stock, it’s doing well for us. The shares hit a new all-time high two weeks ago. The stock came close to breaking through $70 per share. Ten years ago, it was going for $18 per share.

RPM has increased its dividend every year for the last 45 years. I’m expecting number 46 in October. My current Buy Below is $71 per share. I may raise it soon, but I want to see the earnings results first.

That’s all for now. The fourth quarter starts next week. With the turn of the month, we’ll get several important economic reports. The ISM Manufacturing report is due out on Tuesday. The last one wasn’t so hot. On Wednesday, ADP will release its payroll rate. Then on Friday, we’ll get the big September jobs report. The unemployment rate has been stuck at 3.7% for three months in a row. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on September 27th, 2019 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His