CWS Market Review – October 25, 2019

“99% of the troubles that threaten our civilization come from too optimistic accounting.” – Charlie Munger

We’re at the high tide of earnings season. We had seven Buy List earnings reports this week, and there are another six coming our way next week. If that’s not enough, there’s a Federal Reserve meeting next week as well, plus a jobs report next Friday.

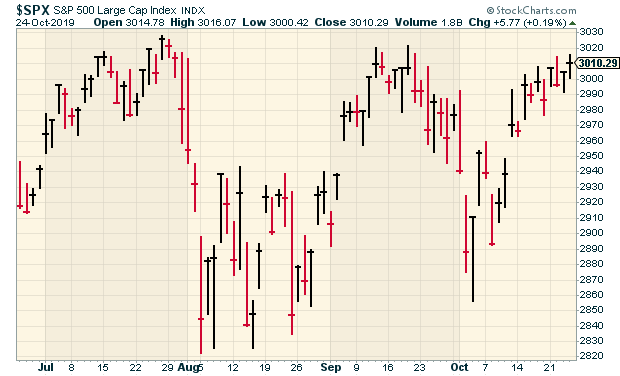

So far, Wall Street seems to like earnings season. On Thursday, the S&P 500 closed at 3,010.29. That’s the highest close in nearly three months, and we’re very close to a new all-time high. In fact, the S&P 500 Total Return Index, which includes dividends, finished Thursday just 0.02% from an all-time-high close.

In this week’s CWS Market Review, I’ll summarize all the earnings reports for you. So far, every one of our stocks has beaten earnings expectations. Stand-outs so far include Sherwin-Williams, which beat earnings, increased guidance and gapped up to a new high. The same for Raytheon. AFLAC beat and guided higher, but no new high. At least, not yet.

There’s so much earnings news that I won’t have time to discuss the Fed meeting, but you can expect the Fed to cut rates again. Now let’s take a look at this week’s Buy List earnings reports.

This Week’s Earnings Reports

Here’s an updated look at this season’s earnings calendar:

| Company | Symbol | Date | Estimate | Results | Eagle Bancorp | EGBN | 16-Oct | $1.07 | $1.08 | Signature Bank | SBNY | 17-Oct | $2.70 | $2.75 | Sherwin-Williams | SHW | 22-Oct | $6.48 | $6.65 | Globe Life | GL | 23-Oct | $1.69 | $1.73 | AFLAC | AFL | 24-Oct | $1.07 | $1.16 | Cerner | CERN | 24-Oct | $0.66 | $0.66 | Danaher | DHR | 24-Oct | $1.15 | $1.16 | Hershey | HSY | 24-Oct | $1.60 | $1.61 | Raytheon | RTN | 24-Oct | $2.86 | $3.08 | Check Point Software | CHKP | 28-Oct | $1.40 | Stryker | SYK | 29-Oct | $1.90 | Cognizant Technology Solutions | CTSH | 30-Oct | $1.05 | Moody’s | MCO | 30-Oct | $2.00 | Church & Dwight | CHD | 31-Oct | $0.61 | Intercontinental Exchange | ICE | 31-Oct | $0.96 | Becton, Dickinson | BDX | 5-Nov | $3.30 | Broadridge Financial | BR | 6-Nov | $0.71 | Fiserv | FISV | 6-Nov | $0.99 | Disney | DIS | 7-Nov | $0.95 | Continental Building Products | CBPX | TBA | $0.40 |

On Tuesday, Sherwin-Williams (SHW) posted Q3 adjusted earnings of $6.65 per share. That beat Wall Street’s estimates of $6.48 per share. This was a very good quarter for the paint people. The CEO said:

“Sherwin-Williams delivered strong results in the quarter as adjusted earnings per share increased 17.1% year-over-year to $6.65. Our performance in the quarter was driven by continued strength in North American architectural paint markets, which offset choppiness in some industrial-end markets. U.S. and Canada same-store sales growth was 8.1% as our pro painting customers continued to report strong demand. As a result of this strong volume and operating efficiencies, consolidated gross margin expanded over 300 basis points to 45.7%. Adjusted EBITDA margin in the quarter improved 150 basis points to 18.9% compared to the prior year.

“For the second consecutive quarter, all three operating segments increased segment profit and margin compared to the same period last year. In The Americas Group, our North American paint stores generated strong growth in all regions and all customer-end markets, led by double-digit growth in residential repaint. With the strong volume, the team delivered incremental operating margin of approximately 37%, and we have opened 31 net new stores year to date.

Segment profit in The Americas Group increased $85.9 million to $663.7 million in the quarter and increased $122.1 million to $1.61 billion in nine months, due primarily to higher paint-sales volume and selling-price increases.

The best news is that Sherwin increased its full-year guidance range to $20.90 – $21.30 per share. The previous range was $20.40 to $21.40 per share. Since Sherwin has already made $16.83 per share for the first nine months of this year, the new range implies Q4 earnings of $4.07 to $4.47 per share.

Sherwin-Williams is now up 117.3% since we added it to the Buy List in 2017. This week, I’m lifting our Buy Below on SHW to $590 per share.

On Wednesday, Globe Life (GL) reported Q3 net operating income of $1.73 per share compared with $1.59 per share for the year-ago quarter. Wall Street had been expecting $1.69 per share. This was GL’s first earnings report under the new name. Here are some highlights from the quarter:

• Net income as an ROE was 12.0%. Net operating income as an ROE excluding net unrealized gains on fixed maturities was 14.7%.

• Life underwriting margins at Liberty National Exclusive Agency and American Income Exclusive Agency increased over the year-ago quarter by 12% and 9%, respectively.

• Health underwriting margin at Family Heritage Exclusive Agency increased over the year-ago quarter by 12%.

• Life premiums increased over the year-ago quarter by 7% at American Income Exclusive Agency, and health premiums increased over the year-ago quarter by 7% at both Family Heritage Exclusive Agency and American Income Exclusive Agency.

• Life net sales at Liberty National Exclusive Agency and American Income Exclusive Agency increased over the year-ago quarter by 12% and 9%, respectively.

• 932,946 shares of common stock were repurchased during the quarter.

The stock hit a new high on Thursday. Globe Life has quietly turned into a nice winner for us this year. I’m keeping the Buy Below at $100 per share.

Thursday was an especially busy day for us. We had five Buy List earnings reports.

Let’s start with Hershey (HSY). The chocolate folks reported earnings of $1.61 per share. That beat Wall Street by a penny per share.

It was a good quarter, but Hershey didn’t change its full-year guidance of $5.68 to $5.74 per share. That’s the same story as three months ago. With the Q2 earnings beat, I thought Hershey would raise guidance, but it didn’t. The company seems to be low-balling Q4.

The guidance implies Q4 earnings of $1.18 to $1.24 per share. Wall Street had been expecting $1.27 per share. On the bright side, Hershey increased full-year sales guidance by a tiny bit. Hershey remains a buy up to $162 per share.

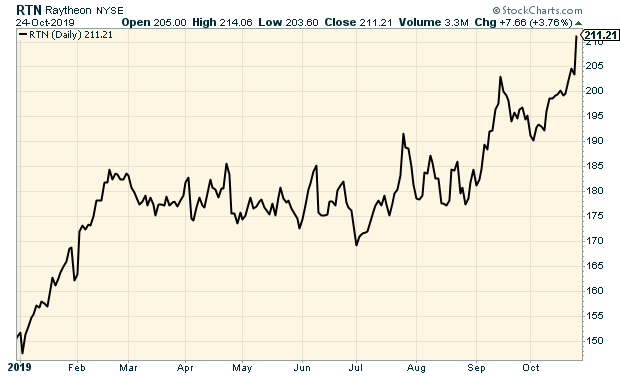

Raytheon (RTN) had a great Q3. The defense company made $3.08 per share which was 22 cents better than estimates. Sales for the quarter rose by 9.4% to $7.45 billion. Raytheon also boosted its full-year range to $11.70 to $11.80. The previous range was $11.50 to $11.70.

The company said the earnings beat was driven by higher net sales in classified programs. (I’m afraid to ask.) For the quarter, Raytheon’s bookings grew by 8.4% to $9.44 billion. Their backlog was up 7% to $44.6 billion. The shares rallied nearly 4% on Thursday and made a new high.

Raytheon is planning to merge with United Technologies (UTX). The merger should happen sometime during the first half of next year. RTN shareholders will get 2.3348 shares of Raytheon Technologies. This week, I’m lifting my Buy Below on Raytheon to $220 per share.

Danaher (DHR) reported Q3 earnings of $1.16 per share. That was a penny better than estimates. For Q4, Danaher sees earnings ranging between $1.32 and $1.35 per share. The works out to full-year earnings of $4.74 to $4.77. That’s a little lower than the previous guidance of $4.75 to $4.80 per share.

There are two important notes to add. One is that Danaher is buying GE’s Biopharma business. The deal should close sometime in Q4. Also, Danaher recently IPO’d Envista (NVST), which was their dental business. Danaher still owns about 80% of the company.

For Q3, Cerner (CERN) made 66 cents per share, which was in the middle of their guidance of 65 to 67 cents per share.

For Q4, Cerner expects earnings between 73 and 75 cents per share on revenue of $1.41 billion to $1.46 billion. The healthcare-IT firm sees new-business booking ranging between $1.45 and $1.65 billion. The Q4 earnings guidance is effectively a narrowing of their previous full-year guidance. Previously, Cerner had expected 2019 earnings of $2.64 to $2.72 per share. With new Q4 guidance, that works out to $2.66 – $2.68 per share.

This report is basically what I had expected—maybe a tad light, but nothing to worry about. Earlier this year, Cerner reached an agreement with Starboard Value to start paying a dividend and increase its buyback authorization by $1.5 billion. Cerner remains a buy up to $71 per share.

For Q3, AFLAC (AFL) made $1.16 per share which beat the Street by nine cents per share. Forex added two cents per share to their bottom line.

The good news is that the duck stock raised its full-year guidance to a range of $4.35 to $4.45 per share. That’s a big increase over the old guidance of $4.10 to $4.30 per share. The range is based on the 2018 exchange rate of ¥110.39 yen to the dollar.

AFLAC said it’s aiming to buy back $1.3 to $1.7 billion worth of stock this year. AFLAC remains a buy up to $57 per share.

Six More Reports Next Week

Now let’s look ahead to next week which will be another busy week of earnings for us.

On Monday, Check Point Software (CHKP) is due to report. The stock has not done well for us this year. The earnings really haven’t been that bad. Wall Street, however, hasn’t liked the earnings guidance.

For Q3, Check Point told us to expect earnings to range between $1.36 and $1.44 per share on revenue of $480 to $500 million. That’s not bad. For the entire year, CHKP projected earnings between $5.85 and $6.25 per share and revenue between $1.94 and $2.04 billion.

Three months ago, Stryker (SYK) raised its guidance for 2019. The orthopedics company now expects full-year organic net sales to rise by 7.5% to 8.0%. Stryker expects earnings to range between $8.15 and $8.25 per share. The previous range was $8.05 to $8.20 per share.

For Q3, Stryker sees earnings between $1.87 and $1.92 per share. It should be able to top that. The earnings report is due out on Tuesday. The stock is up nearly 35% for us this year.

Cognizant Technology Solutions (CTSH) has not been a strong performer for us this year. I’ve been patient with CTSH, but we need to see signs that business is improving. After the May earnings report, CTSH lost 18% in two days. The last earnings report was somewhat of an improvement, but we need to see more.

Cognizant said it now expects full-year earnings between $3.92 and $3.98 per share. That’s an increase from the previous range which was $3.87 to $3.95 per share. However, that was a big cut from the initial guidance of at least $4.40 per share. For Q3, Cognizant expects revenue growth in the range of 3.8 to 4.8% in constant currency. The earnings report will come out on Wednesday. Wall Street expects earnings of $1.05 per share.

Moody’s (MCO) is scheduled to report earnings on Wednesday. This is our top-performing stock this year, with a YTD gain of 54%. The jewel in the crown is Moody’s Analytics which makes up about 40% of revenues. Three months ago, Moody’s beat earnings and raised guidance. For 2019, Moody’s expects earnings between $7.95 and $8.15 per share. Consensus is for $2 per share.

Church & Dwight (CHD) will report on Thursday. For Q3, CHD sees earnings of 60 cents per share, and $2.47 for the entire year. The company has grown organic sales by more than 4% for five quarters in a row. The stock took a sharp drop in early September after an investment firm came out with a negative piece on the consumer-products company. I won’t address the specifics of their allegations, but I’ll note that these things happen every so often. Wall Street expects 61 cents per share.

Last is Intercontinental Exchange (ICE). The exchange operator is also due to report on Thursday. ICE didn’t offer EPS guidance, but it did for a few other metrics. What stood out to me was the ranges for data revenue. ICE said Q3 data revenues are expected to be in a range of $550 million to $555 million. For all of 2019, ICE sees data revenues in a range of $2.19 billion to $2.24 billion. The analyst consensus is for 96 cents per share.

That’s all for now. Lots more earnings next week. The Federal Reserve meets on Tuesday and Wednesday. Expect a rate cut. The policy statement will be out on Wednesday at 2 p.m. ET. Also on Wednesday, we’ll get our first look at the Q3 GDP report. The October jobs report is due out on Friday morning. The last report showed the lowest unemployment rate in 50 years. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on October 25th, 2019 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His