CWS Market Review – January 10, 2020

”It is impossible to produce superior performance unless you do something different from the majority.” – John Templeton

The new decade got off to a violent start. Only a few hours into 2020, the U.S. military attacked and killed Iranian general Qasem Soleimani. Iran then struck back in a seemingly understated rocket attack. Fortunately, no Americans were injured.

As usual, I’ll leave the geopolitical commentary to others. But I will say that these latest tensions pose no obvious threat to the financial markets or to our Buy List. The evening of the attack, the futures market fell sharply. However, once actual trading resumed, markets were much calmer. In fact, the S&P 500 recently broke out to another fresh all-time high.

This is the typical script. Markets react quickly, and often wrongly. However, they can right themselves quickly as well. Some experts are saying that this round of the confrontation is already over. I certainly hope so.

In this week’s CWS Market Review, I want to discuss our new Buy List in greater detail. We also have Q4 earnings season coming up soon. I’ll preview next week’s earnings report from Eagle Bancorp (EGBN). I’ll also cover the recent earnings report from RPM International (RPM). The company beat the Street by three cents per share. But first, let’s talk a little more about our 2020 Buy List.

Why I Did What I Did

Whenever I make the Buy List changes, I make sure to get all the performance stats in the newsletter. Unfortunately, that gives short shrift to the “why” behind the changes. Now that I have more time, I want to go into why I made the alterations I did,

I feel that if I’m doing my job correctly in the newsletter, then the sell stocks shouldn’t be a big surprise. Continental Building Products (CBPX) was an easy decision since the company will soon be bought out.

The same goes for Raytheon (RTN). It’s hooking up with United Technologies. I had considered the benefits of holding the new company, but the old Raytheon would only be a small part.

Signature Bank (SBNY) was also an easy call. The bank never showed the level of growth I expected. Also, the taxi-medallion issue dragged on far too long.

JM Smucker (SJM) was also an easy one. I really wanted to stay with this one, but their premium dog-food business has been a disaster. The numbers got worse and worse. Frankly, I should have seen this coming. Last year, SJM lowered full-year guidance twice. Companies need to stick to what they’re good at.

Cognizant Technology Solutions (CTSH) ran into a brick wall last year. In May, the company cut full-year guidance by more than 10%. Apparently, the banking sector hadn’t been spending as much as CTSH expected. The results since then haven’t been much better. I had to let CTSH go.

It’s time to sell a stock when the company is no longer the company I bought. In the case of Continental and Raytheon, that’s literally the case. With the others, it’s more subjective. But just because a stock had a rough year, it’s not necessarily a reason to sell. Later on, I’ll discuss Eagle Bank, which ran into trouble last year. But I think it’s a good opportunity to hold onto. It’s still the company we originally bought.

Now let’s look at the new buys.

Ansys (ANSS) makes simulation software for engineers. Whenever you see a designer working with a 3-D model on a computer screen, there’s a good chance he or she is using Ansys software. Before building a bridge, a skyscraper or an airplane, the designer wants to make sure that it can withstand the pressure it will experience in real life.

Ansys is a classic “wide moat” company. Once a customer starts using their software, there’s a good chance he or she will become a long-term buyer. Ansys maintains an operating profit margin in excess of 35%, and their gross margin runs around 90%. Ansys is not exactly a value stock, but I think there are occasions when it’s worth it to pay extra for an outstanding company. Ansys is a buy up to $270 per share.

Middleby (MIDD) makes industrial cooking equipment for restaurants and hotels. Their equipment is sold under 50 different brand names. Selim Bassoul led the company since 2001. Under his leadership, the company lapped the overall market 100 times, but he suddenly retired last year, and the stock suffered. This is a good time to get in. Middleby is a buy up to $120 per share.

Silgan (SLGN) is one of the leading makers of metal containers in the world. In North America, Silgan holds the #1 position in metal food containers. Silgan’s containers are used by customers such as Campbell’s Soup, Del Monte and Nestlé.

Silgan supplies highly-engineered triggers, pumps, sprayers and dispensing closure solutions for health care, garden, home, and beauty and food products. Silgan also makes plastic containers used by personal care, pharmaceutical and other companies. About 80% of its revenue comes from North America. The shares are going for about 13 times next year’s earnings. Silgan is a buy up to $34 per share.

Stepan (SCL) makes specialty and intermediate chemicals. I know it sounds dull, but Stepan’s products are used in a broad range of industries. Although Stepan is classified with other specialty-chemical companies, it doesn’t have a competitor that precisely matches its businesses.

Stepan makes surfactants. They’re the key ingredient in cleaning compounds, the stuff that makes detergents and shampoos clean and foam. Stepan also makes germicidal quaternary compounds. That’s a scary name for killing germs, mold and mildew. Hospitals and restaurants depend on these. Stepan also has a polymer group. This is for plastics and polyester products. Think of a laminate board for the construction industry plus coatings, adhesives and sealants.

Stepan has increased its dividend for the last 51 years in a row. Stepan is a buy up to $110 per share.

Trex (TREX) makes wood-alternative decking and railing. In my opinion, what they make looks a lot like wood, but it’s cheaper and involves a lot less maintenance. Trex is also better for the environment. Their railings are especially common at stadiums and arenas across North America.

It’s not a value stock, but there’s a lot of potential. I think Trex can earn $3 per share this year. Also, Trex has a solid balance sheet and doesn’t carry a dime in long-term debt. It’s already up 7.8% for us this year. My Buy Below on Trex is $97 per share.

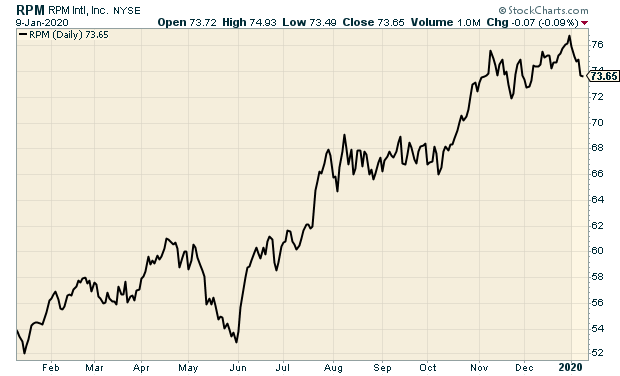

RPM International Beats Earnings

On Wednesday morning, RPM International (RPM) reported fiscal Q2 earnings of 76 cents per share. That’s a good result. Wall Street had been expecting 73 cents per share. Net sales rose 2.8% to $1.40 billion. RPM had record cash flow and EBIT margin improved by 180 basis points.

For fiscal 2020 (ending in May), RPM sees earnings ranging between $3.30 and $3.42 per share. That’s reiterating the same guidance they gave us in July. Wall Street expects full-year earnings of $3.35 per share.

Overall, the numbers were pretty good. This is from the earnings report:

“Our very strong bottom-line growth in the quarter was primarily driven by our 2020 MAP to Growth, which is enabling us to grow earnings at a faster rate than those of our peers. Actions taken included delayering management, consolidating manufacturing, and shedding low-margin product lines to free up capacity for more value-added, EBIT-accretive volume. Pricing and moderating raw material inflation also positively impacted results,” stated Frank C. Sullivan, RPM chairman and chief executive officer. “In spite of a challenging macroeconomic environment, we were pleased with our solid organic-sales growth in the quarter of 3.5%, which resulted from market-share gains and pricing. Acquisitions contributed 0.6% to the quarter’s top-line growth, while foreign currency translation was a 1.3% headwind.”

For Q3, RPM expects sales to be up 2.5% to 4.0%, and 25% to 30% in adjusted growth in earnings before interest and taxes. RPM sees earnings-per-share in the “high-teens to low-20-cent range.”

I’m pleased with this report. RPM International remains a buy up to $77 per share.

Earnings Preview for Eagle Bancorp

Earning season is here, and as usual, the banks are among the first companies to report. Now that Signature is no longer on our Buy List, that leaves just Eagle Bancorp (EGBN) which is scheduled to report Q3 earnings on January 15.

Eagle’s banking business is doing quite well. The problem is Eagle’s legal troubles. Six months ago, the stock got a super-atomic wedgie after disclosing unusually high legal bills. We stuck with Eagle, and I’m glad we did.

Eagle can’t go into the details, but there seem to be issues surrounding the financial impropriety of Washington, D.C. city councilman Jack Evans. I want to be clear that there’s no specific wrongdoing charged against Eagle. Their former CEO, however, might not be in the clear. At this point, we simply don’t know a lot of details. That’s always the frustrating part of an “ongoing investigation.” I should also say that Eagle faces no regulatory restrictions.

I want to mention two recent events. One is that Eagle recently hired a new Chief Legal Officer. Also, Jack Evans has resigned from the D.C. City Council. He was about to be expelled.

I want to underscore some important stats about Eagle. Nonperforming loans are just 0.66% of total assets. Another key stat for any bank is the efficiency ratio. That’s the ratio of non-interest expense to total revenue. For Q3, Eagle’s efficiency ratio was 38.34%. That’s pretty good. In 2019, Eagle snapped its ten-year streak of quarterly earnings growth.

From its August low to its December high, Eagle gained more than 34%. It’s still not back where it was last summer, but it’s a start. For next week’s report, the consensus on Wall Street is for $1.07 per share.

Buy List Updates

I also want to raise the Buy Below prices on two of our Buy List stocks. Ross Stores (ROST) has been doing very well lately. The deep discounter had a very good earnings report for Q3, and I’m expecting more good news next month when the Q4 report comes out. This week, I’m lifting our Buy Below on Ross Stores to $129 per share.

I also want to increase the Buy Below on Cerner (CERN). The healthcare-IT firm will report earnings on February 4. For Q4, Cerner expects earnings between 73 and 75 cents per share on revenue of $1.41 billion to $1.46 billion. I’m raising my Buy Below to $79 per share.

That’s all for now. The December jobs report is due out later today. On Tuesday, we’ll get the latest inflation numbers. I think they’ll be quite modest. Then on Thursday, the latest retail-sales report is due out. The most recent data haven’t been very good. Next Friday, the industrial-production report is due out. The last report was quite good. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on January 10th, 2020 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His