CWS Market Review – June 19, 2020

“The expectation of an event creates a much deeper impression on the exchange than the event itself.” – Jose de la Vega, 1688

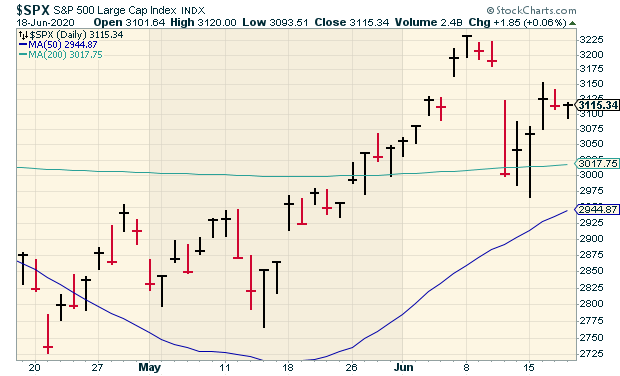

After last Thursday’s unpleasantness, when the S&P 500 plunged nearly 6%, the stock market has been much more relaxed this week. At one point on Monday, the S&P 500 was down 2.5% during the day. Yet by the closing bell, the index had eked out a small gain. That was only the third time in the last ten years that a 2.5% drop wound up being a day in the black.

So the bulls haven’t all been scared off. In this week’s issue, I want to cover some of the recent economic data, which hasn’t been good; it just hasn’t been quite as terrible as previous data. I’ll also preview next week’s earnings report from FactSet. The stock is having a good year for us. I also have some updated Buy Below prices for you. But first, let’s review some recent economic data.

Where the Economy Can Improve, It’s Improving

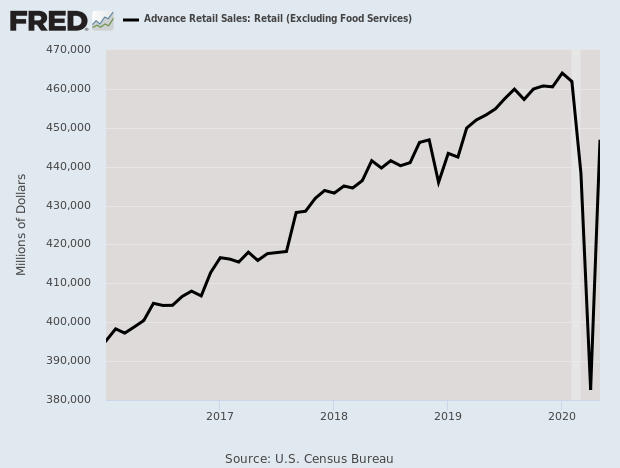

On Tuesday, the Census Bureau said that retail sales rose an amazing 17.7% last month. It’s not often you see a retail-sales report beat Wall Street’s consensus by 10%. Last month’s result was the best on record, by far.

Get used to seeing a lot of that. We saw lots of economic data recently that was among the worst on record. Now that some sectors have reopened, it’s only natural that we’re seeing a pronounced snap back.

So is the economy back on track? Not exactly. While the retail-sales report is good news, the government’s stimulus checks clearly played a role. We still have a long way to go till the economy is fully back on its feet. Much of that will be due to the course the coronavirus ends up taking. Gradually, more companies are getting back to normal.

Here’s the retail-sales chart. Sometimes the chart really does tell the story.

Disney World looks to start reopening on July 11. Disney World Hong Kong just reopened, and Shanghai Disneyland opened up in May. Speaking of Disney World, the NBA looks to finish off its regular season starting in late July. All games will be played at the ESPN Wide World of Sports Complex in Disney World.

Also on Tuesday, we learned that industrial production rose by 1.4% in May. Some factories are coming back online, albeit only partially. The economy is a long way from full capacity. Industrial production is still 15.4% below where it was in February.

In last week’s issue, I mentioned that the recession-dating committee officially declared that the recession had started. There’s a good chance that this could be one of the quickest recessions on record. There was a brief recession in 1980 that only lasted six months. We could see something like that. The difference is that this recession is much steeper.

This week, we learned that homebuilder confidence rose sharply in June. That’s a good sign. On Wednesday, the Commerce Department said that housing starts rose 4.3% in May. This was the first increase since January. Housing starts are still bad, but the increase is off the lowest reading in five years. This aligns with the previous report which tells us that the economy is in rough shape, but where it’s allowed to improve, it’s improving.

On Thursday, the jobless-claims report fell to 1.508 million. It’s odd to say that’s a good number, but it’s the tenth-straight improvement in a row. Continuing claims decreased slightly, from 20.606 million to 20.544 million.

Finding a Competitive Advantage

Since this is a fairly short issue, I wanted to talk a little more about proper stock selection and how to find superior investments. I’m often asked about this, and it’s an interesting but complex topic.

I’ll try to keep it simple. My basic plan is to find companies with a distinct competitive advantage. Here’s a good way to think about this (I’m heavily borrowing from our friends at Investopedia for this example).

Let’s say you have a lemonade stand and business is going well. You suddenly have an idea. Normally, your stand buys lemons each morning. Instead of doing that, you decide to buy a bunch of lemons at the beginning of the week. Your supplier gives you a bulk discount.

Let’s say, this cuts your cost of goods sold by 20%. In terms of economics, this is a huge deal. This means you can cut your prices by 20%, thereby gaining market share, and it will have zero impact on your gross profit margins. This is great news for you and your business.

As much as we love this, there’s one small problem. While it’s a great idea, it’s just an idea—and one that can be easily copied by your competitors. Once they discover the secret, your advantage is gone.

Now let’s say you come up with a second idea. You invent a revolutionary new lemon squeezer that’s so good, you get 20% more juice out of each lemon. Once again, this is a huge deal in terms of business economics. You’re effectively cutting your costs of goods sold by 20%, and again, you can pass those savings on to your customers with no impact on your gross margins.

But there’s a crucial difference between the first example and the second. In the second case, you can patent your lemon squeezer. That means you can line up state power to enforce your invention monopoly. The idea in the first example isn’t protected the same way.

The second example shows the kind of company I look for. I look for firms that do things that no one else can do. Several stocks on our Buy List have strong competitive advantages. In particular, I think of companies like Moody’s (MOC) or Fiserv (FISV).

With that said, how do you know if a company has a strong competitive advantage? There are a few characteristics that typically show up.

Oftentimes, the company we’re looking at has a consistent operating history. Sales and earnings edge higher nearly every year. There may be bad years, but the positive trend is clear.

This tells me a few things about the business. First and most obviously, it’s a growing enterprise with a steady demand for its products. It also tells me that management is probably on the ball. That’s because in a dynamic marketplace, you need to make a lot of small corrections to keep the ship moving.

A company with a consistent operating history also probably has a loyal customer base. Never overthink a business. You can make a lot of money selling the same thing to the same people. Ask Starbucks (SBUX).

Lastly, investing in companies with a consistent track record is an easy way of reducing risk. I’m not a fan of “oil well” stocks. These are companies that appear flat broke but are pinning all their hopes on some deal that may never come. There are too many of these stocks around. When in doubt, I always prefer a stock that grows its business each year.

A company should also have the ability to raise prices. This is a subtle rule, so let me explain what I mean.

You’ll notice that I didn’t say I look for companies that do raise their prices. Rather, the key is finding ones that, if the need arises, can raise their prices.

Think about the items in your home or office. Now imagine which ones you would still buy even if they raised their price by 10% or 15%. Some items you’d simply stop buying. But not all.

Why? Maybe you’re attached to it. Or maybe it’s an integral part of your day. I have friends who would make their daily Starbucks run no matter what.

Also, a company that has the ability to raise its prices most likely has a firm handle on its costs. That way, it can pass savings along to its customers, which builds customer loyalty

There’s a risk component as well. No company wants to raise prices, but it’s nice to be in a position where they can do so if need be.

Ability to raise prices is often a sign that a company has a dominant position in its market. I often think of Harley-Davidson (HOG), the legendary hog stock and former Buy List member.

I also like to see a company that is the dominant player in a niche market. A company doesn’t have to own the world to be successful. Owning the best autobody shop in town, or the best Thai restaurant in town, can be a great business.

Why? Because the firm is doing something no else can do. In business, there’s a term called “switching costs.” This refers to the cost for a consumer to change his or her preference. With toothpaste, folks aren’t so picky. With eating habits, people can be very picky.

For a business, you want to be the dominant player, even if it’s in a very narrowly-defined market. Think of the ratings agencies. If you want to float a bond, you pretty much have to deal with Moody’s or S&P.

Warren Buffett often tells the story that the perfect business to own is an unregulated toll road. The fixed costs are low, and drivers need to use it.

On our Buy List, we have Broadridge Financial Solutions (BR). This is the dominant player in share-voting proxies. This is the kind of business not one person in 20 ever thinks about, but it fills a concrete need.

You can spot a dominant player because it often has modest debt levels, wide operating margins and strong cash flow.

I hope that gives you a better idea of what I look for when selecting our Buy List stocks. I’ll have more details in upcoming issues. Now let’s look at next week’s earnings report.

FactSet Earnings Preview

FactSet (FDS) is due to report its earnings on Thursday, June 25, before the stock market opens. This will be for FactSet’s fiscal Q3 earnings, which ended on May 31.

I like this company a lot, and it’s one of the stocks that has a strong “moat,” meaning a strong position in its market. Three months ago, FactSet reported solid results from its fiscal Q2. The company earned $2.55 per share which beat consensus by six cents per share. Quarterly revenue rose 4.2% to $369.8 million. This was for the quarter that ended on February 29, so coronavirus didn’t have a noticeable impact on its operations.

For FactSet, the key stat to watch is Annual Subscription Value, or ASV. For Q2, that stood at $1.44 billion. ASV is growing at more than 4%. At the end of Q2, FactSet’s client count reached 5,699, and the user count is up to 128,896. Annual ASV retention is over 95%.

At the time of the Q2 report, FactSet stood by its full-year earnings estimate of $9.85 per share to $10.15 per share. Like nearly everybody else, FDS rallied nicely off its low, although the stock recently pulled back over 10% in four trading days.

Wall Street currently expects Q3 earnings of $2.43 per share. That sounds about right.

Updated Buy Below Prices

Before I go, I want to update a few of our Buy Below prices.

Ansys (ANSS), a new stock for us this year, has been doing well lately. The May earnings report was quite good. This week, I’m raising our Buy Below on Ansys to $300 per share.

Church & Dwight (CHD) has rallied for the last four days in a row. It’s now up 10.6% this year. The shares just hit a nine-month high on Thursday. I’m raising my Buy Below on CHD to $80 per share.

Danaher (DHR) has also been acting well lately. The stock hit another new high this week. It’s now a 14.7% winner for us this year. I’m lifting our Buy Below to $185 per share.

That’s all for now. Next week, we’ll get the existing-home sales report on Monday and the new-home sales report on Tuesday. Thursday morning will be busy, as the jobless claims report is due out. At the same time, the Q1 GDP revision comes out. This will be the second revision to Q1 GDP growth. As if that weren’t enough, we’ll also get the report on durable goods at the same time. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on June 19th, 2020 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His