CWS Market Review – July 31, 2020

“It is a capital mistake to theorize before one has data. Insensibly, one begins to twist facts to suit theories, instead of theories to suit facts.” – Arthur Conan Doyle

What a busy week this has been! We had several more Buy List earnings reports. So far, our stocks are doing very well. In fact, the Buy List has nearly made back everything it lost earlier this year. The last few weeks have been particularly good for us. Since July 13, our Buy List has gained 7.53% compared with 2.88% for the S&P 500. This earnings season, all of our stocks have beaten Wall Street’s estimates (so far).

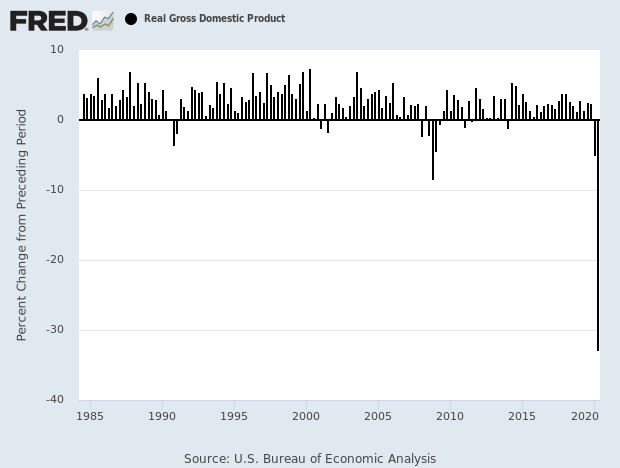

On Thursday, the government said that the U.S. economy contracted at a 32.9% annualized rate during the third quarter (see chart below). That’s by far the worst on record. It’s three times worse than the previous record. We knew it was coming but it’s still jarring to see. Also on Thursday, we learned that jobless claims rose for the second-straight week. That’s after falling for 15 weeks in a row. I’m afraid that’s not a good sign.

We also had a Federal Reserve meeting this week. The central bank didn’t make any changes to interest rates, but Chairman Jerome Powell said that economic growth is “well below” where it was before the pandemic. The Fed has signaled that it will keep rates near 0% though 2022. It may even be longer.

But this week’s CWS Market Review is all about earnings. I’ll go over the seven earnings reports we got this week, and I’ll preview the batch coming next week. Let’s jump right in.

Our Latest Buy List Earnings Reports

Here’s our updated Earnings Calendar:

| Company | Ticker | Date | Estimate | Result |

| Check Point Software | CHKP | 22-Jul | $1.44 | $1.58 |

| Eagle Bancorp | EGBN | 22-Jul | $0.74 | $0.90 |

| Globe Life | GL | 22-Jul | $1.53 | $1.65 |

| Silgan | SLGN | 22-Jul | $0.65 | $0.85 |

| Stepan | SCL | 22-Jul | $1.20 | $1.65 |

| Danaher | DHR | 23-Jul | $1.08 | $1.44 |

| Hershey | HSY | 23-Jul | $1.13 | $1.31 |

| RPM International | RPM | 27-Jul | $1.01 | $1.13 |

| AFLAC | AFL | 28-Jul | $1.07 | $1.28 |

| Sherwin-Williams | SHW | 28-Jul | $5.85 | $7.10 |

| Cerner | CERN | 29-Jul | $0.61 | $0.63 |

| Intercontinental Exchange | ICE | 30-Jul | $1.04 | $1.07 |

| Moody’s | MCO | 30-Jul | $2.21 | $2.81 |

| Stryker | SYK | 30-Jul | $0.55 | $0.64 |

| Church & Dwight | CHD | 31-Jul | $0.63 | |

| Trex | TREX | 3-Aug | $0.65 | |

| Disney | DIS | 4-Aug | -$0.61 | |

| Ansys | ANSS | 5-Aug | $1.16 | |

| Fiserv | FISV | 5-Aug | $0.93 | |

| Middleby | MIDD | 5-Aug | $0.41 | |

| Becton, Dickinson | BDX | 6-Aug | $2.04 | |

| Broadridge Financial Solutions | BR | 11-Aug | $2.09 |

Let’s start with RPM International (RPM). On Monday, RPM reported its fiscal Q4 earnings. This is for the quarter that ended on May 31. As I expected, due to Covid-19, the company had a tough quarter. Sales fell 8.9% but the breakdown was interesting. Sales were flat in the U.S. but down 25% internationally. While RPM withdrew its guidance, the company did say that it expected Q4 sales to fall 10% to 15%, so they beat that forecast.

Net income fell to 84 cents per share from $1.02 per share last year. However, once you exclude charges and investment losses, then quarterly income fell 8.9% to $1.13 per share. Even though results were down, it was still the second-best quarter in the company’s history. Wall Street had been expecting earnings of $1.01 per share.

RPM has a strong balance sheet and plenty of liquidity, so I’m hardly worried about their survival.

For the full year, RPM made $3.07 per share. That’s an increase of 13.3% over last year. Before the virus hit, RPM had been expecting full-year earnings to range between $3.30 and $3.42 per share.

For fiscal Q1, which ends next month, RPM expects net sales growth “in low single digits and adjusted EBIT growth of 20% or more.” RPM isn’t providing any full-year guidance yet.

After the earnings report, shares of RPM gapped up to a new 52-week high but pulled back later. I’m raising my Buy below on RPM to $90 per share. The company has raised its dividend every year since 1973.

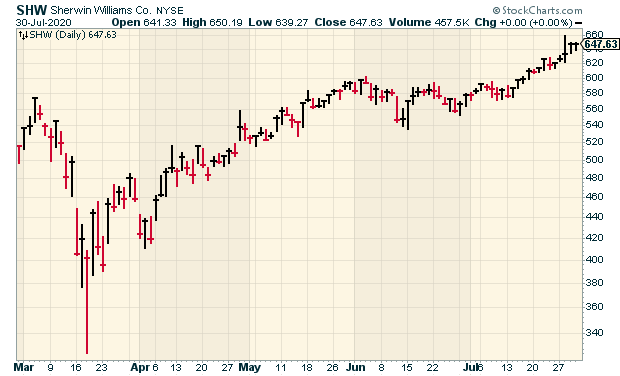

On Tuesday, Sherwin-Williams (SHW) had a great earnings. For their fiscal Q2, the paint people earned $7.10 per share. That easily beat Wall Street’s estimate of $5.85 per share. Sales fell 5.6% to $4.60 billion.

For Q2, diluted net income increased to $6.48 per share. That’s up from $5.03 per share a year ago. However, there’s also 62 cents for “acquisition-related amortization expense.” That brings us up to $7.10 per share.

The best news is that Sherwin is increasing its full-year range to $19.21 to $20.71 per share which includes $2.54 per share in acquisition-related amortization expense. That previous range was $16.46 per share to $18.46 per share, including a $2.54 per share acquisition-related amortization expense. For Q3, the company sees net sales up or down in the low single digits.

This was an outstanding report. Sherwin also got to a new high this week. The stock has doubled since its March low. I’m raising our Buy Below to $700 per share.

Last week, I told you that AFLAC (AFL) should be able to beat earnings and the duck stock did just that. After the closing bell on Tuesday, AFLAC reported Q2 earnings of $1.28 per share. Total revenues were $5.4 billion which was down a bit from the $5.5 billion of one year ago.

Net income was $805 million or $1.12 per share. That’s up from $1.09 per share for last year’s Q2. With insurance companies, we always want to look at the adjusted earnings because investment gains and losses can have a big impact on net income. Adjusting for that brings us to $1.28 per share. Wall Street had been expecting $1.07 per share.

During Q2, the yen/dollar exchange rate averaged 107.65. That was 2.1% stronger than the average rate from last year’s Q2. That knocked off a penny per share in earnings so adjusted for currency, AFLAC’s earnings rose 12.4% to $1.27 per share.

AFLAC is usually pretty good at giving guidance, but they don’t have much to say this time, which is understandable. The CEO did say that AFLAC is committed to defending its dividend streak of 37 consecutive annual hikes. Clearly, the company is doing well. AFLAC remains a buy up to $37 per share.

On Wednesday, Cerner (CERN) reported fiscal Q2 earnings of 63 cents per share. The range Cerner had given was for earnings of 60 to 64 cents per share. Wall Street had been expecting 61 cents per share.

Overall, I’m pleased with these numbers. The healthcare-IT firm said that bookings were $1.34 billion, which was $100 million above the high-end of the company’s guidance. Quarterly revenue fell 7% to $1.43 billion. That was $10 billion below the company’s expected range.

For the quarter, Cerner had operating cash flow of $259 million and free cash flow of $64 million. Total backlog now stands at $13.66 billion.

Now for guidance. For Q3, Cerner expects revenue to range between $1.35 billion and $1.40 billion, and they expect full-year revenue between $5.45 billion and $5.55 billion. The latter range is a downgrade from their previous guidance.

For earnings, Cerner expects Q3 to range between 70 and 74 cents per share. For the whole year, they see earnings between $2.80 and $2.88 per share. The previous range was $2.78 to $2.90 per share. Wall Street had been expecting $2.83 per share.

At first, the shares dropped as much as 5.5% on Thursday, but the stock gained back some ground. I was pleased with these results even though the revenue forecast was a little light. I’m lifting our Buy Below on Cerner to $75 per share.

On Thursday, Intercontinental Exchange (ICE) reported Q2 earnings of $1.07 per share. That’s a 14% increase over last year. Revenues rose 8% to $1.4 billion. ICE’s operating margin is at 59%. Wall Street had been expecting earnings of $1.04 per share.

So far this year, ICE has bought back $1.1 billion of its stock and paid out $330 million in dividends. For Q3, ICE expects data revenues of $575 million to $580 million. ICE remains a buy up to $100 per share.

Stryker (SYK) had a tough quarter, but it still delivered an impressive profit. Quarterly sales fell 24%. Earnings fell 67.7% to 64 cents per share. Wall Street was looking for 55 cents per share.

Here’s the breakdown by Stryker’s three business segments. Orthopaedics had a net sales decline of 29.9%. MedSurg’s net sales dropped 17.3% and Neurotechnology and Spine dropped by 29.6%. It was bad all across the board.

Stryker is in a tough spot since the business environment is so poor for them. Still, it’s a solid and well-run outfit. I’m not worried about Stryker in the long term. Stryker remains a buy up to $200 per share.

Moody’s (MCO) had an outstanding quarter. The ratings agency earned $2.81 per share. That’s 60 cents per share more than what Wall Street had been expecting.

In fact, the results were so good that Moody’s significantly raised its earnings guidance. Moody’s now sees full-year earnings of $8.80 to $9.20 per share. That’s up from the previous forecast of $8.15 to $8.55 per share.

This was an outstanding quarter. Moody’s remains a buy up to $290 per share.

Six More Earnings Reports Next Week

Church & Dwight (CHD) reports later today. This has been a steady winner for us. Unfortunately, C&D withdrew its guidance, but Wall Street expects Q2 earnings of 63 cents per share. Church & Dwight actually benefited from the coronavirus outbreak, especially brands like Arm & Hammer and some hygiene products.

After that, we have six more earnings reports next week.

Trex (TREX) has been a huge winner for us this year. Through Thursday, it’s up 55.6% for us. In May, Trex blew past Wall Street’s forecast for Q1. The deck company made 73 cents per share, 12 cents more than the Street’s consensus estimate. Quarterly sales rose 12% to $200 million. Gross margin rose 620 basis points to 44.8%.

Trex has withdrawn its guidance but the company said it expects Q2 sales between $180 million and $190 million. Trex also halted all share repurchases. Their earnings report is due out on Monday. The Street consensus is for earnings of 65 cents per share.

If I went into a lab and designed a company to be impacted by the coronavirus, it would probably look a lot like Disney (DIS). The company is focused on movies, sports and travel. It even has a cruise line. All these businesses have suffered. Disney will bounce back, but it will take time. Disney reports on Tuesday. For Q2, Wall Street is looking for a loss of 61 cents per share.

Three more stocks are scheduled to report on Wednesday. Ansys (ANSS) had a solid report three months ago. The company made 83 cents per share which was three cents more than estimates.

For Q2, Ansys expects earnings between $1.01 and $1.33 per share. For all of 2020, they see earnings between $5.61 and $6.23 per share. Wall Street had been expecting $1.43 for Q2 and $6.26 for the whole year.

For Q2, Wall Street expects $1.16 per share.

Fiserv (FISV) is having a rare “off” year for us. So far, the stock is down 13% this year. The company only matched Wall Street’s earnings three months ago. The company has also withdrawn its guidance.

I did spot some encouraging signs in the last earnings report. For example, Fiserv’s adjusted revenue increased slightly to $3.48 billion. Free cash flow rose 3% to $760 million. Operating margin increased 10 basis points to 27.8%.

Wall Street expects 93 cents per share for Q2. Only AFLAC and Fiserv have been on the Buy List for all 15 years.

In the CWS Market Review issue from May 15, I told you I like Middleby (MIDD) below $60 per share. Since then, the stock has rallied over 40%. If you’re betting on an economic recovery, Middleby is a good way to play it. At one point, Middleby was down 60% for us on the year. It’s also doubled off its low. The consensus is for earnings of 41 cents per share.

Becton, Dickinson (BDX) is due to report on Thursday. In May, Becton said it had earnings of $2.55 per share for Q1. That was 19 cents better than expectations. Quarterly revenue came in at $4.253 billion which topped the Street’s consensus of $4.13 billion. Their Life Sciences unit fared especially well.

Becton recently got a massive order for 177 million syringes and needles for COVID-19 vaccination programs. The company withdrew its 2020 guidance. For Q2, Wall Street expects $2.04 per share.

That’s all for now. Next week is the first week of the month and that’s when we get a lot of key economic reports. On Monday, the ISM Manufacturing Index comes out. Tuesday is factory orders. The ADP payroll report comes out on Wednesday. Thursday is another jobless-claims report. That leads us up to Friday and the July jobs report. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on July 31st, 2020 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His