CWS Market Review – November 13, 2020

“A good decision is based on knowledge and not on numbers.” – Plato

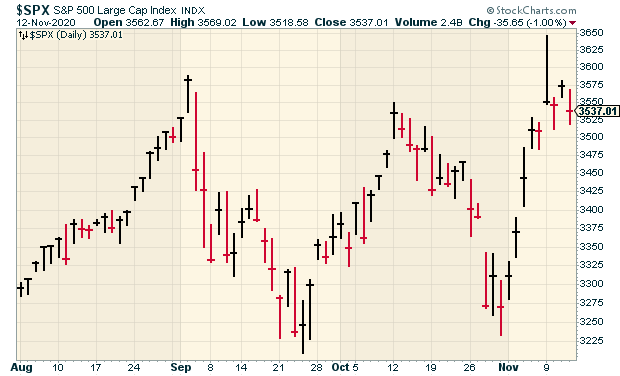

The entire world got encouraging news this week with the promising results of a vaccine for the coronavirus. The stock market was elated by the news as the Dow and S&P 500 rallied to new all-time intra-day highs. Our Buy List also reached a new high.

This week’s market action was very unusual. I covered some of this in a special alert I sent you on Monday. Just to give you an idea of how dramatic trading was, consider this stat: The ten worst-performing stocks this year through November 8 were up an average of 23% on Monday and Tuesday!

Everything seemed to go haywire. On Monday and Tuesday, the Nasdaq Composite lost 340 points while the Dow gained 1,100 points. The S&P 500 is off to its best November start in 65 years.

In this week’s issue, I’ll sort it out for you. Frankly, what we’re seeing isn’t new. Instead, it’s a continuation of a trend that started in September: namely, value stocks outperforming growth.

Also in this issue, I’ll go over the recent earnings report from Hershey. The chocolate folks not only beat the Street, but they raised guidance as well. Disney also had an encouraging earnings report. Later on, I’ll preview next week’s earnings report from Ross Stores, a stock that’s gained 23% since October 30. But first, let’s look at this hectic week on Wall Street.

Wall Street Celebrates Vaccine News

After the news of Pfizer’s successful vaccine test broke, stocks immediately shot higher. At one point on Monday, the S&P 500 was up nearly 4%. The Dow rallied 1,600 points.

Right now, 86% of stocks are trading above their 200-day moving average. That’s the broadest the market has been since January, and the second highest in the last five years.

Equally important were the kinds of stocks that were rallying this week. It seemed that all the stocks that been caged up for months were suddenly let loose. Banks and financial stocks soared. Oil and energy stocks charged higher. Airlines, cruise stocks and malls all saw huge gains. (Heck, even Denny’s soared.)

At the other end of the trade, so many stocks that had been doing so well under the coronavirus started to sag. For example, while the Nasdaq did close higher, it only did one-third as well as the S&P 500. Zoom, the video-conferencing stock, has been the super star stock of the pandemic. This week, Zoom lost one-quarter of its value in two days.

Housing stocks, in particular, were hit hard. Our favorite deck stock, Trex, got knocked down. I’ll have more to say on Trex in a bit. Even cleaning stocks like Clorox dropped sharply. It’s a good reminder of how broad the economic impact of the coronavirus has been. It’s also interesting to note that the big shifts came despite little or no news specific to each company. Instead, traders were playing the economic impact. (Or I should say, the perceived economic impact.)

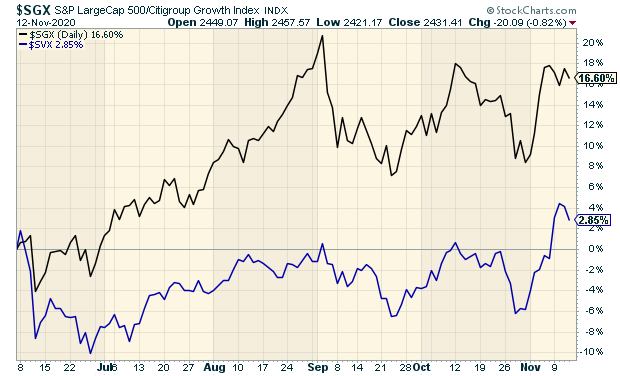

The larger theme that connects all these points is the shift from growth stocks to value stocks. We saw the first hint of this shortly after Labor Day. At that time, the rotation was fast and hard. Stocks like Tesla lost one-third of their value in a week. Meanwhile, many value stocks held up well.

On Monday and Tuesday of this week, the S&P 500 Value Index rose by 5.35%. Meanwhile, the S&P 500 Growth Stock Index dropped by 1.66%. That’s a very big divergence for such a short period of time. (In the chart above, value is blue and growth is black.)

The rotation also signals an optimistic outlook for the economy. In particular, you can see that in the strength of energy stocks. The S&P 500 Energy Index gained an amazing 17% on the first two days of this week. Of course, that sector has been in a world of pain for a long time. Still, a recovering economy needs fuel.

The rotation to value began after Labor Day, but soon let up. This week, it returned with a vengeance. I don’t think it’s over. Bear in mind that there have been several false starts for value. This time, I think it’s real. Don’t expect to see more of those easy tech gains like we saw this summer. Going forward, the market is going to place greater emphasis on valuation and dividends. Make sure your portfolio has plenty of high-quality names. Speaking of which, let’s look at the earnings report from Hershey.

Hershey Beat Earnings and Raised Guidance

We had a very good earnings report from Hershey (HSY) last week. On Friday, the chocolate company earned $1.86 per share for its third quarter. Wall Street had been expecting $1.72 per share. Quarterly revenues were up 4.2% to $2.22 billion. That beat the Street by $60 million. Organic sales grew by 3.8%. Consensus was for 2.5%.

CEO Michele Buck said:

“We had a strong third quarter, with accelerated reported net-sales growth of 4%, adjusted diluted EPS growth of more than 15% and confectionery share gains across markets, including an almost 190-basis-point gain in the U.S. Our core U.S. business remains healthy as consumers reach for small treats during the pandemic, and our decision to lean into Halloween ahead of the season supported consumers’ desire to find new and creative ways to celebrate safely. We also saw sequential improvement in the areas of our business hit hardest by COVID-19, including our international markets, owned retail locations and food-service business.”

Hershey also raised its guidance. The company now expects full-year earnings of $6.18 to $6.24 per share. That’s up 7% to 8% over last year. For the first three quarters of this year, Hershey has made $4.80 per share. That implies Q4 earnings of $1.38 to $1.44 per share. Wall Street had been expecting $1.38 per share.

I like these results. On Thursday, the stock snapped a seven-day winning streak where it rallied more than 11%. I’m raising our Buy Below on Hershey to $160 per share.

Winter of DIS Content

After the bell on Thursday, Disney (DIS) said it lost 20 cents per share for its third quarter. Despite the loss, Disney exceeded expectations on nearly every count. Wall Street had been expecting a loss of 71 cents per share.

Quarterly revenue came in at $14.71 billon, which topped estimates of $14.2 billion. Total revenue was down 23% from a year ago. The parks business is still hurting. Disney said it expects Disneyland to be closed for the rest of the year. Disney World is operating at 35% capacity. Disney estimated that Covid-19 has cost their parks $2.4 billion in operating income in the fourth quarter. Revenue for the Parks division was down 61% from a year ago.

The big number everyone’s been waiting for is 73 million. That’s the number of Disney+ subscribers. The service is now one year old, and it’s been an amazing start for them. That’s a net increase of 12.5 million subscribers for the third quarter.

Disney continues its successful strategy of placing its streaming service at the center of its business model. The entertainment giant continues to have more and better content than just about everyone.

I cautiously use this comparison, but Netflix currently trades at 54 times next year’s earnings estimate, while Disney is in the ballpark at 52 times earnings. This comparison isn’t precise, because Disney is involved in so many businesses that aren’t remotely similar to Netflix. Still, the plan for Disney is to move to a business that can generate a Netflix-like earnings multiple.

Disney was also pleased with the results from Mulan. This is an interesting story because Disney offered the movie for “Premium Access.” Subscribers could buy the film for $30.

Shares of DIS jumped about 4% in Thursday’s after-hours trading. This week, I’m lifting my Buy Below on Disney to $150 per share.

Earnings Preview for Ross Stores

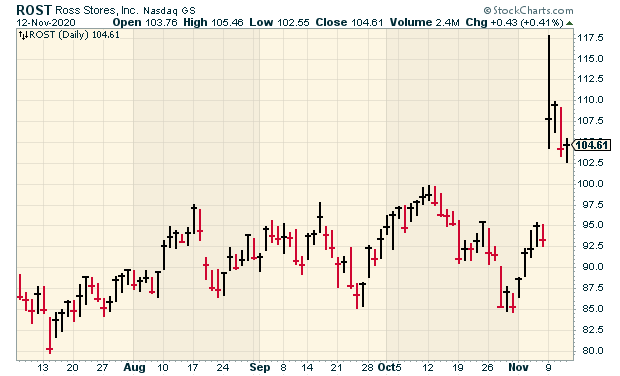

Few stocks have been impacted by the coronavirus quite like Ross Stores (ROST). There’s been good news recently for the deep discounter, and it couldn’t have come at a better time. Ross is due to report earnings next Thursday, November 19.

Optimism for an economic reopening has greatly helped shares of Ross. In a recent seven-day stretch, shares of Ross vaulted more than 28%, and that includes a 15% leap on Monday. (Check out the chart below.)

Ross had a terrible fiscal Q1 earnings report. That’s to be expected when you have to shut down all of your stores. For Q2, which ended on August 1, business was a little better. Ross was able to make a profit for Q2 of six cents per share. That’s small, but Wall Street had been expecting a loss of 26 cents per share. For comparison, Ross made $1.14 per share for last year’s Q2.

Business still remains tough. Total sales for Q2 dropped from $4.0 million last year to $2.7 million this year. Comparable-store sales, which is a key metric for retailers, dropped by 12%.

I’m expecting better results for Q3. The consensus on Wall Street is that Ross will report earnings of 60 cents per share and sales of 3.42 billion. Thanks to the recent rally, I’m lifting my Buy Below on Ross Stores to $110 per share.

Buy List Updates

Given this past week’s drama, I have two more Buy Below price adjustments to make. I’m lowering our Buy Below on Trex (TREX) to $78 per share. There’s nothing wrong with Trex. I just want the Buy Below to reflect the recent rotation.

I’m also raising our Buy Below price for AFLAC (AFL). The last earnings report was very good. The duck stock is a buy up to $44 per share.

Hormel Foods (HRL) will report its Q4 earnings before the market opens on Tuesday, November 24. This is for the quarter ending in October. For Q3, Hormel earned 37 cents per share, which was a three-cent beat. The Spam folks said that Q4 should mirror the strength seen in Q3. The food-service business will likely post a year-over-year decrease for Q4.

Stryker (SYK) completed its acquisition of Wright Medical. The deal was first announced a year ago. Stryker paid $30.75 for each share of Wright. The company recently reported great numbers for Q3. Due to the pandemic, Stryker can’t offer guidance for Q4. I’m raising Stryker’s Buy Below to $233 per share.

That’s all for now. There are a few important economic reports next week. On Tuesday, the retail-sales report and industrial-production report are due to be released. Then on Wednesday, we’ll a get a look at the existing-home-sales report. On Thursday, we get another report on jobless claims. Last week’s report was 709,000, which isn’t that far from the highest numbers we saw during the recession of 2007-2009. Also on Thursday, Ross Stores will report its earnings. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on November 13th, 2020 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His