CWS Market Review – May 11, 2021

“When I was young, I was a terrible investor. But after decades of hard work, I am no longer young.” – Douglas A. Boneparth

(This is the free version of CWS Market Review. Don’t forget to sign up for the premium newsletter for $20 per month or $200 for the whole year. Thanks for your support.)

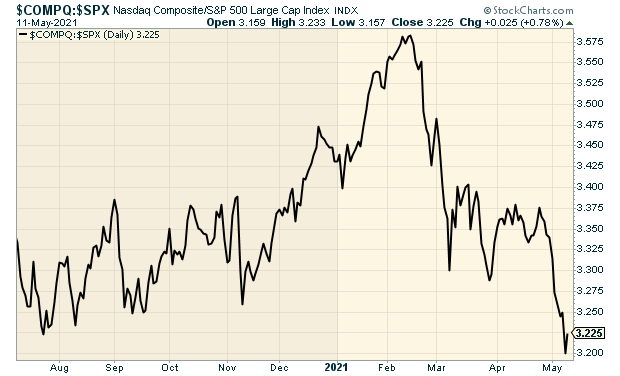

The Nasdaq Hits the Skids

Suddenly, the Nasdaq is getting a lot of attention from traders, and it’s not the good kind. The index trailed the S&P 500 for nine out of ten days. It would have happened again on Tuesday, but a big intra-day reversal held back the trend for at least one more day. At one point, the Nasdaq was down over 2% on Tuesday. Things may not get better soon. The Nasdaq also dipped below its 50-day moving average which is often a sign of more bad times to come.

What’s happening is that the Nasdaq is heavily weighted towards popular tech stocks such as the FAANG stocks (Facebook, Amazon, Apple, Netflix and Google), and those stocks have been feeling the heat.

It’s not just the FAANG names. In January, Tesla broke $900 per share. This morning, it dipped below $600. Alibaba is off over 30% from its 52-week high.

These stocks had been doing so well for so long, but now it appears that valuation concerns are finally coming to the surface. No doubt, Amazon is a great company, but should it really be going for 45 times next year’s earnings? Of course, that’s the problem with momentum investing. What happens when it becomes momentum in the other direction?

This is really a continuation of a trend that we saw in February and March when tech stocks badly lagged. That trend quickly petered out, until now. In fact, you can even trace a larger trend of tech names falling out of favor back to Labor Day. Instead of one continuous trend, we’ve seen sharp waves of a few weeks each where tech stocks get dinged.

Here’s a chart of the Nasdaq divided by the S&P 500:

Yesterday, the S&P 500 fell over 1% for the first time in two months. But it was an odd day because the down stocks were down a lot. Callie Cox has some revealing stats; 40% of stocks in the S&P 500 made a new high on Monday. On a big down day! Traders are running from growth as fast as they can.

It’s interesting that this rotation has occurred as the overall market has rallied. Friday was another all-time high close for the S&P 500. Normally, the popular names lead during the entire bull market. It appears that crypto and meme stocks have supplanted these areas as the place where the real risky business happens. Bloomberg quotes one energy trader, “All the fun that used to be had 30 years ago in the commodity markets and is no longer fun—that fun is now in crypto.” I think that’s right.

What I think is happening is that the rise in bond yields is putting the squeeze on valuations. Normally, earnings multiples are aligned with bond yields. The lower yields go, the higher P/E Ratios rise. Last summer, the 10-year yield was going for about 0.5%. Now it’s up to 1.6%. That’s certainly not high in an absolute sense, but it’s higher than where it was.

I’m a fan of Cathie Wood and her ARK Innovation ETF (ARKK), although the fund goes into areas of the market we generally avoid. She’s done a remarkable job, but her ETF has been clocked hard lately. ARKK has lost about 30% of its value in the last three months, and it’s been in a tailspin lately.

There’s also a liquidity concern with ARKK. Wood has so much money to manage that she owns more than 10% of the outstanding shares in a number of stocks. I often say that with ETFs, the liquidity issue isn’t the trading of the actual ETF. Instead, it’s the trading of the underlying securities. That’s why CWS has never had a liquidity problem. We’re mostly in mid- and large-cap stocks. If ARKK is hit with redemptions, that could spark a selloff in some of Wood’s smaller positions.

This underscores an important lesson about portfolio management. Several of her stocks are correlated with each other. An investor can have many stocks in his or her portfolio and still be very undiversified.

Even though we have a focused portfolio at our ETF (CWS), our portfolio has its hands in many different sectors. For example, shares of Hershey (HSY) quietly made a new high on Tuesday, even though many high-profit stocks looked nervous. You can see more info on the ETF here.

The Most Disappointing Jobs Report of All Time!

Wall Street is still in shock over Friday’s jobs report. Economists had been expecting an increase of one million jobs. Instead, the U.S. economy added just 266,000. The unemployment rate ticked up to 6.1%. One analyst said, “This might be one of the most disappointing jobs reports of all time.”

There’s already a lot of finger-pointing going on. This is an unusual time for the jobs market because more employers are simply having a hard time finding workers. This morning we learned that jobs openings hit a record high of 8.12 million.

Bloomberg reports that “many employers say they are unable to fill positions because of ongoing fears of catching the coronavirus, child-care responsibilities and generous unemployment benefits.” There are 2 million more jobs vacancies than new hires. That’s the highest on record.

The New York Times mentioned a beach restaurant that’s offering a case of 120 Minute India Pale Ale as a signing bonus. Not bad. The jobs report is especially frustrating as more state and local economies are getting back to normal.

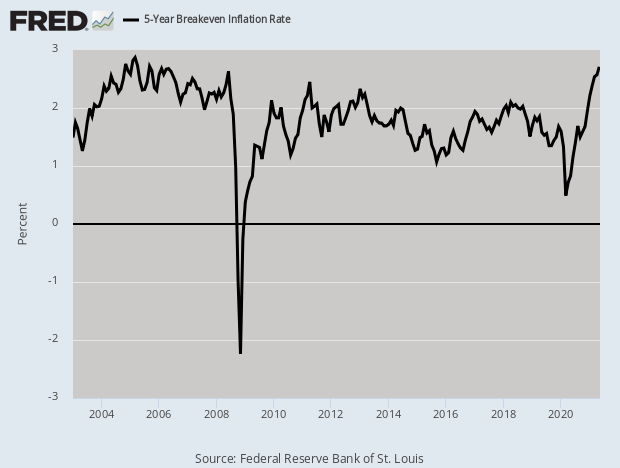

Tomorrow, the government will release its CPI figures for April. There’s growing talk that inflation is on the rise. Last week, Treasury Secretary Janet Yellen told The Atlantic that the Fed could easily handle inflation with modest rate increases. The market reacted harshly. Later that day, Yellen clarified that she wasn’t expecting inflation. She just meant that it could be handled if it arrived.

Instead of government officials, I prefer to see what the market thinks. A good gauge is the 5-year breakeven rate. That’s the difference between the 5-year Treasury and the 5-year TIPs. In other words, it’s the market’s guess as to the rates of inflation over the coming five years. The 5-year breakeven recently jumped above 2.7% which is a 13-year-year high. That fact is being mirrored in the foreign exchange market as the U.S. dollar is near a two-and-a-half year low.

Clearly, higher prices are on the way. One area where we seeing higher prices is at the pump. As a result of the recent pipeline attack, we’re seeing gas lines across parts of the southeastern U.S. According to GasBuddy, 7.6% of gas stations in Virginia didn’t have gasoline. In North Carolina, it was 5.8%. On Monday, gasoline demand jumped 20%. In five states; Georgia, Florida, South Carolina, North Carolina and Virginia, demand was up more than 40%.

All sorts of commodity prices are up. Corn is up more than 50% this year. Lumber prices are through the roof. The WSJ reports that farmers are planting like crazy. The newspaper notes that bullish bets on corn outnumber bearish ones by 17 to 1.

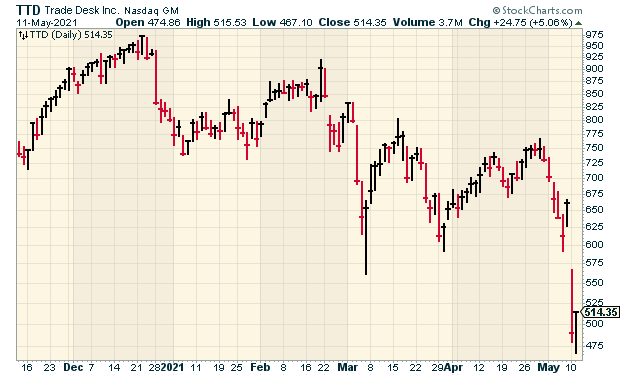

Stock Focus: The Trade Desk

On Monday, shares of the The Trade Desk (TTD), got absolutely pummeled. The stock plunged 26% in one day. This is noteworthy because The Trade Desk had been a big winner. From its low in March 2020 to its high in November 2020, TTD gained more than 560%.

Thanks to yesterday’s train wreck, this sounds like a good opportunity to take a closer look at this stock that’s still not very well-known.

The Trade Desk markets a software platform that’s used by digital ad buyers to build data-driven advertising campaigns. In other words, they help companies get the most bang for their buck on the web.

Ten years ago, Jeff Green left a job at Microsoft to start The Trade Desk. Microsoft had purchased Green’s online auction advertising company. While at Microsoft, he met Dave Pickles who would later become his partner at The Trade Desk. Today, Green is the CEO and Pickles is the CTO.

Green and Pickles’ idea was simple. They felt that the large tech companies had been stifling environment for online advertising by creating a “walled garden” approach to content and data. As a result, advertisers weren’t getting the kind of transparency they wanted. In stepped The Trade Desk.

The Trade Desk’s solution is that it offers a real-time bidding technology platform. This way, media buyers can target specific audiences with customized ads. Users can manage their digital ad campaigns in real time. They can even use third-party data to optimize their strategies. This saves a lot of time and money for companies’ media strategies.

The “open Internet” idea is a big deal. The large tech companies have dominated the advertising space for so long, and it’s ripe for being upended. What’s happened is that the major tech companies have fiercely guarded their territory and refused to give up any control of the advertising process. This hasn’t won them many friends among government regulators.

The Trade Desk is based in Ventura, CA. They currently have about 1,000 employees and a market cap around $24 billion. The Trade Desk had its IPO in September 2016 at $18 per share. After Monday’s plunge, it’s around $511 per share.

There’s been a lot of misunderstanding about The Trade Desk’s business and that’s because some investors seem to believe that it can easily be blown out by giants like Google or Facebook.

That’s not true and this highlights the key difference that The Trade Desk offers. If a company wants to advertise with, say, Google, then they go to Google. If a company wants to advertise with Facebook, then they go to Facebook.

But if a company wants to use The Trade Desk, then the Trade Desk can tell them that the best and most cost-effective place for them is The New York Times or The Wall Street Journal or Hulu or any number of places.

The Trade Desk is not a direct competitor to Google or Facebook. Jeff Green said that The Trade Desk is hardly a concern to those companies. The Trade Desk can and has partnered with just about anybody.

The company is enormously profitable and so many trends are working in The Trade Desk’s favor. Digital ad spending will continue to grow at a double-digit rate. The Trade Desk’s gross margins are close to 80%. I haven’t seen anyone else provide digital marketing managers the scope that the Trade Desk offers.

So what happened on Monday? Did they miss earnings? Not exactly. The Trade Desk reported earnings of $1.41 per share. That was 83% higher than expectations. Revenues were also above expectations.

If the results caused the stock to plunge, then I’m curious what the real expectations were for. The Trade Desk also said that Q2 revenue will be higher than expected. If that’s not enough, The Trade Desk also announced a 10-for-1 stock split. This is a very confident company. On Monday’s earnings call, Jeff Green said, “when we compete, we usually win.”

I like this company a lot and I’m keeping a close eye on it. The stock isn’t cheap (73 times next year’s earnings), but it’s certainly cheaper than where it was.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. Don’t forget to sign up for our premium newsletter. You can’t afford not to get it!

Posted by Eddy Elfenbein on May 11th, 2021 at 5:42 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His