CWS Market Review – September 8, 2021

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year.)

What Happened to Value?

A few days ago, the great tweeter Ramp Capital, asked, “What useless talent would you like to have that you can’t profit from?”

Nate Geraci answered, “Value investing.”

Value investing

— Nate Geraci (@NateGeraci) September 5, 2021

I have to admit I laughed.

It’s sadly true. Value investing hasn’t been a very good strategy for the last several years. In fact, value investing has lagged the overall market for more than 14 years. The last value peak came in May 2007.

How could this be? When I was getting my MBA, we were all taught that value investing was one of the strategies that could beat the market over the long term. There are gobs of academic studies to back this up.

The idea is simple enough: Load up on stocks with low P/E Ratios or high dividend yields, sit back, wait and eventually count your winnings. It makes sense. Value stocks were stocks that were tossed aside by the market for whatever reason, so value investors simply profited from stocks regressing to the mean.

But what’s happened since 2007? To be precise, value investing has been unprofitable. It’s merely been less profitable than growth investing. To be sure, there have been periods of value lagging before. But that’s usually been two to three years. Nothing like 14. The current growth cycle will soon be old enough to get her learner’s permit.

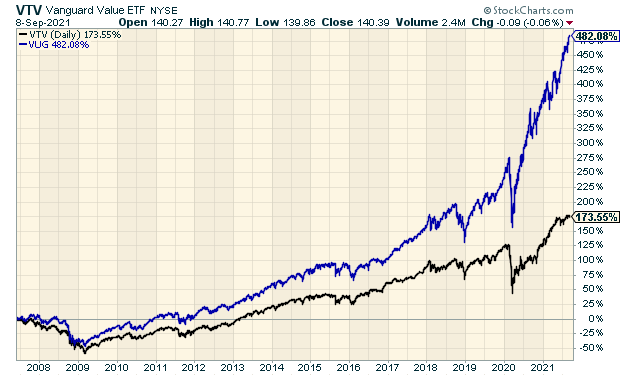

Here’s a chart of the Vanguard Value ETF (VTV), in black, along with the Vanguard Growth ETF (VUG), in blue, since May 2007.

Yikes! So what happened to value? The answer is interesting because it’s not really about value. Instead, it’s about how we measure value. This is what happens when you blindly follow one metric without looking at the broader picture. The value indexes are made based on a stock’s price-to-book ratio. By book value, we mean the accounting value of the company.

But this isn’t a neutral factor. Not by a long shot. The book values of many financial and energy stocks are very elevated. As a result, lots of stocks are being mislabeled, in my opinion, as being value stocks.

For example, nearly every major bank has a book value that’s fairly close to 1.0. Not many are above 1.6. Citigroup’s (C) is just 0.79. This means that nearly every major financial company gets put in the value bin. The same is true for many energy companies, but that’s not how it should work.

Ideally, the relative performance of the value index should reflect investors’ appetite for risk. Now it’s simply an index that’s heavily slanted to large oil companies and the major banks. Banks haven’t done that well since the financial crisis and the price of oil peaked in 2008. The value indexes aren’t telling us that value has been weak. Instead, they’re just reflecting the changes happening in two sectors of the economy.

Let’s look at some numbers. The S&P 500 Value Index currently has a 21.1% weighting in financial stocks and a 5.2% weighting in energy stocks. Meanwhile, financial stocks make up just 2.8% of the S&P 500 Growth Index. Energy stocks are a scant 0.1%. Banks and financials have nearly ten times the weighting in value that they do in growth.

This is an important lesson in stock analysis. Effect A may not be caused by Factor A. Instead, the inputs can be all wrong and as a result, you’re getting bad outputs.

If I had my way, the value and growth indexes would not be determined by the particular accounting of different industry sectors. Instead, I would base them on how each stock behaves. If a stock broadly moves with other value stocks, then it’s a value stock. Same for growth. The judgment of the market is smarter than that of accountants.

Free Onions!

It’s time to free onions. By that, I don’t mean cost-free onions. Instead, I mean we should liberate onions!

In the United States of America, it’s against the law to trade onion futures. In 1958, Congress passed the Onion Futures Act. This sounds like something made up by a satirical newspaper, but it’s all true.

How did this law come to be? Well, that’s an interesting story.

**Eddy lights his pipe**

It started back in 1955. That’s when two onion traders, Sam Siegel and Vincent Kosuga, cornered the market for onions. Think Goldfinger, but onions instead of gold.

It turns out that there are many layers to this story. It’s a dicey situation and it may end in tears. (Sorry.)

Onion trading was actually a big deal years ago. It was one of the most popular contracts on the Chicago Mercantile Exchange. Siegel and Kosuga gradually bought millions of onions. They then shorted onion futures and dumped their vast onion horde on the market. The price for onions plunged. The price for a 50-pound bag of onions fell from $2.75 to just 20 cents. So many onions were going to Chicago that there were shortages in the rest of the country.

At one point, a 50-pound bag of onions was worth less than the bag that held them. As you might imagine, the public was not pleased. Siegel and Kosuga made millions. Meanwhile, farmers were crushed as they held vast amounts of worthless onions.

When the people get angry, that’s when politicians jump in. Congress passed the ban and President Eisenhower signed it into law. The bill was sponsored by Congressman Gerald Ford.

As a side note, the ban provided economists with a real-world arena to test an economic question: Does the presence of a futures market make the price of the underlying commodity more or less volatile? In other words, is speculation good or bad? Like many things economic, there’s conflicting data.

In recent years, onion prices have been very volatile. I think we’ll soon see onions futures return to the market.

(Yesterday, someone on Reddit wondered if their grocer’s coupon for onions violated the law. It doesn’t.)

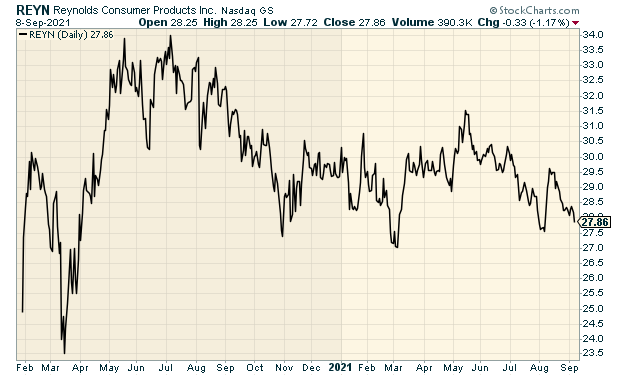

Stock Focus: Reynolds Consumer Products

This week’s featured stock is Reynolds Consumer Products (REYN). I have to confess that I love consumer products companies.

I say this for several reasons.

The first is that these are often products consumers pretty much have to buy. Reynolds for example, makes Reynolds Wrap. Everyone has heard of it and nearly everyone uses it.

This is important because when the economy goes into a nose-dive, folks generally don’t cut back much on their household items. Instead, you’ll see broad weakness in areas like vacation-oriented businesses or homebuilders.

When the economy is on its knees, people cut back on the expensive stuff. Sales of Reynolds Wrap, not so much.

This is also important because we’ll witness steadier business performance. When looking at the financial statements of a consumer products company, we’ll probably see steady increases in sales, profits and dividends. This makes forecasting much easier, and that makes it easier for us to value a stock.

As a stock-picker, I’m always leery of companies that rely too much on “the promise” of future growth. With these defensive companies, there’s less guesswork.

Found in Nearly Every American Kitchen

First, let’s look at the back story of Reynolds Consumer Products. Reynolds’s products can be found in 95% of American kitchens. Open one drawer and you’ll see Reynolds Wrap and Reynolds Aluminum Foil. Look under the sink and there are the Hefty Bags. Look somewhere else and you’ll see paper plates and cups. Reynolds makes the stuff you usually don’t think about but would certainly miss if it wasn’t around.

Reynolds also does a nice business with “private labels.” In plainer terms, this means Reynolds also makes the store-brand knock-off stuff you see in the shopping aisles. The private label business usually does better during a recession, but Reynolds does well since they have both ends of the market covered.

Reynolds is also the exclusive private label supplier to Amazon.

Reynolds usually ranks #1 or #2 in just about every product segment. Most shoppers know the names and that helps brand loyalty. The company generates $3.2 billion in sales annually.

Who doesn’t love a red solo cup?

The company used to be part of Alcoa, but they were sold off to a private equity firm a few years ago. Reynolds then had its IPO in January of last year. This was before the coronavirus hit the U.S. economy and stock market.

The IPO was priced at $26 per share, and investors liked what they saw. On the first day of trading, the shares got as high as $29.46. Within a few days, they were on the doorstep of $32 per share. The rally soon ended as the economy went into lockdown and the shares plunged below $22.

That’s actually not so bad when you compare it to everyone else. When people get scared, they seek out quality.

Pretty soon, Reynolds made back everything it lost and by early June, the stock made an all-time intra-day high of $36 per share. Since then, the stock has slowly drifted lower. When a good stock lags like this, it gets my attention.

Reynolds has already increased prices twice this year without any major problems. That’s a very good sign. In previous issues, I’ve talked about how the ability to raise prices is a good sign of having a competitive edge.

I also like that the company generates a lot of cash flow. One of my concerns is that the company carries a lot of debt. (That’s often a shady IPO strategy. The mother company shoves its debt onto the company they’re about to spin off.) While Reynolds does have a lot of debt, it can be managed; but it will take time and, of course, money. In fact, the company has already pared back its debt position.

Last month, Reynolds reported fiscal Q2 earnings of 39 cents per share on sales of $873 million. That topped estimates by one penny per share. Reynolds expects full-year earnings between $1.54 and $1.64 per share. That’s probably too low but only by a few cents per share. Reynolds pays a quarterly dividend of 23 cents per share. That works out to a yield of 3.30%.

There’s a lot I like about Reynolds Consumer Products. If the Q3 earnings report is good, REYN could be a member of our 2022 Buy List.

I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you haven’t had a chance, you can subscribe to our premium newsletter. It’s only $20 a month or $200 a year. Please join us!

Posted by Eddy Elfenbein on September 8th, 2021 at 7:41 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His