CWS Market Review – December 14, 2021

(This is the free version of CWS Market Review. I’m going to unveil our 2022 Buy List on December 24. To see the new list, make sure you’re a premium subscriber. You can get the premium newsletter for $20 per month or $200 for the whole year.)

The Worst Inflation in 40 Years

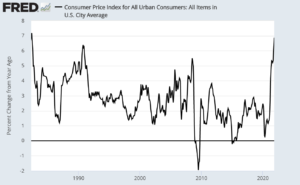

Last Friday, the government released the inflation report for November and it confirmed that the U.S. is now having its worst bout of inflation in 40 years.

Remember how Fed Chairman Jerome Powell kept telling us that inflation is merely “transitory”? Well, that’s all out the window. Now it looks like the Fed may ramp up its tapering bonds. (My apologies for the confusing syntax. By this I mean the Fed will reduce their bond purchases at a faster pace than before.)

First, let’s look at the numbers. For November, headline inflation increased by 0.78%. That’s actually a slight decrease from October’s rate of 0.94%. For its part, the Federal Reserve puts a lot of the blame on the supply-chain crisis. In other words, the Fed says it’s not the fault of the Fed.

I’m reminded of this quote from Milton Friedman:

Central bankers always try to avoid their last big mistake. So every time there’s the threat of a contraction in the economy, they’ll overstimulate the economy by printing too much money. The result will be a rising roller coaster of inflation, with each high and low being higher than the preceding one.

Personally, I’m not so worried about supply issues. As long as there’s money to be made, someone will come along and fix it. That just takes time. I’m more worried about consumers becoming used to higher prices. Once that mentality settles in, it’s hard to shake loose.

Over the past year, consumer prices have increased by 6.88%. That means that if you have a $1 million portfolio, inflation eats up $68,800 every year. That’s the highest year-over-year rate of inflation since June 1982.

The “core rate” of inflation, which excludes volatile food and energy prices, was a little better behaved. For November, the core rate was up by 0.54%. Over the past year, the core rate is up by 4.96%. That’s the fastest core rate in 30 years.

By the way, the core rate comes in for a lot of criticism. It’s not that we ignore food and energy costs. That’s obviously an important part of every family’s budget, especially lower-income folks. Inflation is an especially cruel tax on the poor and those on fixed income.

The problem is that food and energy can be highly volatile. As a result, the month-to-month prices may not give us an accurate measure of the trend in inflation.

For example, here’s a surprisingly optimistic fact. November’s rise in core inflation was the fifth highest in the past eight months. That could suggest that inflation may already be cresting. I think it’s far too early to say that conclusively, but it’s something to take note of.

There’s still more evidence of high inflation. Today we learned that wholesale prices are up 9.6% over the last year ending in November. That’s the highest on record which sounds impressive, but the data series only goes back 11 years. Still, it was higher than Wall Street’s estimate of 9.2%.

The wholesale numbers are important to watch because higher inflation would hit this sector first before wending its way to consumers. Businesses generally do their best to make prices for the consumer as stable as possible.

Inflation has an unusual impact on businesses and, in turn, on stocks. Not all earnings are the same, and inflation exacts a heavy toll on asset-heavy businesses. Companies with high assets relative to their profits tend to report ersatz earnings.

Inflation has an impact similar to putting a magnet near a compass. Everything gets a little screwy. Historically, stocks have not performed well during periods of high inflation. Investors who lived through the 1970s will certainly recall that. During the entire decade of the 70s, the Dow gained a grand total of 38 points.

While inflation has been tough on stocks, there’s only one thing worse for stocks, and that’s deflation. What the market truly loves is low consistent inflation. In other words, pretty much what we had over the last 30 years, minus 12 months.

Of course, the recent inflation numbers haven’t scared off stock investors. On Friday, the S&P 500 closed at an all-time high. Our 67th record high this year. Last week was the second-best week for the S&P 500 all year.

However, the problem isn’t inflation per se. The threat for stocks is really the threat from bonds. Inflation doesn’t impact the stock market directly. Instead, inflation wrecks the bond market and that throws sand in the gears of the stock market. The higher bond yields are greater competition for stocks.

The last time inflation was this high.

The Federal Reserve is meeting this week, today and tomorrow, and I think there’s a good chance that the Fed will change its taper policy. Previously, the Fed said it will reduce its pace of bond buying by $15 billion each month. They may double that. That means the Fed would be on pace to wrap up its bond purchases by March of next year. We can assume that rate hikes would come shortly after that.

The bond market is already pricing in the rate increase. The futures market now sees three rate hikes coming next year. This is a sudden change from only a few months ago. On June 3, the two-year Treasury was yielding just 0.09%. Now that’s all the way up to 0.66%. That’s still very low, but it’s higher than where it was. Over the same time, the three-year yield has jumped from 0.16% to 0.95%.

It’s as if the bond market is saying, “rates aren’t rising now, but they soon will be.” The Fed will release its policy statement tomorrow at 2 pm.

The Stock Market Is Still on Defense

I’ve become a broken record on this topic, but it’s too important to set side. The stock market has become much more defensive over the past month. Riskier stocks have been feeling the pain. Meanwhile, the stable stocks are doing just fine. Even though the surface of the stock market appears fairly staid, the undercurrents are quite dramatic.

On our Buy List, stocks like Church & Dwight (CHD) and Hershey (HSY) have been at or near new highs. But former high-fliers like Nvidia (NVDA) and Tesla (TSLA) are down sharply. Tesla is more than 20% off its recent high.

Here’s another look at the S&P 500 High Beta Index (red) compared with the S&P 500 Low Volatility Index (blue). Since November 8, the Low Vol Index is up by 3% while the High Beta stocks are down over 8.3%.

This is a direct result of the Fed’s willingness to tackle inflation. Once the Fed gets tough, rates will go up. That’s why the defensive stocks are prospering. Already this year, we’ve had more than one rotation. Those have petered out. This one may not.

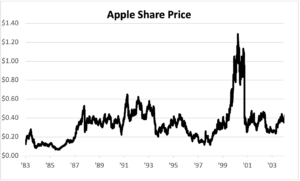

Apple’s Lost 20 Years

Every so often, I tweet this fact: “If you had invested $10,000 in Apple (AAPL) on June 6, 1983, by April 17, 2003, you’d be sitting on $8,400.”

I’ll usually get a few responses telling me that this can’t possibly true. Or I obviously left out stock splits. Nope, the numbers are correct.

It’s remarkable to consider that Apple, which is on the doorstep of a $3 trillion valuation, didn’t do much for nearly 20 years. I think there’s an important lesson for investors in that.

Even if you’re right about the stock, you can get the timing all wrong. It even took a few years after Steve Jobs had returned to Apple for it to turn around. It’s also a reminder that companies are always changing. Sometimes for the better, but not always.

Oh…by the way, that $10,000 investment is now worth more than $6.2 million.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. Don’t forget to sign up for our premium newsletter.

Posted by Eddy Elfenbein on December 14th, 2021 at 6:53 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His