CWS Market Review – January 11, 2022

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Great Resignation

On Friday, the government released the jobs report for December. According to the Bureau of Labor Statistics, the U.S. economy created 199,000 net new jobs last month.

In normal times, that’s a pretty good number, but in the post-lockdown era, that’s not so good. It was less than half of Wall Street’s expectation of 422,000.

This was especially disappointing because two days earlier, the ADP jobs report doubled expectations. Also, the weekly jobless claims have continued to be near 52-year lows. I should mention that ADP uses real-time info. The government’s numbers will be revised in the months ahead. Sometimes these revisions can be quite large.

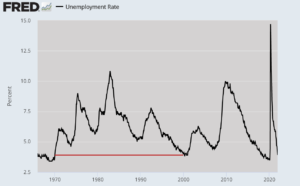

Despite the poor jobs figure, the unemployment rate fell to 3.894%. That’s lower than the unemployment rate for every single month during the entire 1970s, 1980s and 1990s.

(Your humble editor tweeted out that fact and it was retweeted by White House Chief of Staff Ronald Klain. Naturally, this demonstrates my immense power and influence.)

For December, average hourly earnings rose by 0.6%. In the last year, average hourly earnings are up 4.7%. Again, that sounds impressive until you realize that it’s less than the rate of inflation. The sad reality is that many workers are seeing a decrease in their standard of living.

Among business sectors, leisure and hospitality added 53,000 jobs, professional and business services added 43,000 and manufacturing added 26,000. One encouraging sign is that the broader U-6 unemployment rate fell 0.4% to 7.3%.

The labor force participation rate increased slightly to 61.91%. That’s the highest since March 2020. While more folks are gradually returning to the labor market, the U.S. continues to experience the Great Resignation.

What’s happening is that many folks near retirement age have decided to go ahead and retire right now. I’m sure many near-retirees have done well with the stock market, so retiring now may make sense for them. Who needs to deal with the daily rat race especially with Covid? During November, 4.5 million Americans quit their jobs. That’s an all-time record.

The labor force participation rate among prime-working-age adults (age 25 to 54) is holding up fairly well but the real decrease has come among people 55 and over. I suspect that we will see the labor force continue to expand. As my friend Gary Alexander wrote, “Covid and its consequences brought us a record level of savings, government benefits, and stimulus checks, which have now run dry and so work income is once again necessary.”

The Market Is Nervous about Tomorrow’s Inflation Report

The bond market wasn’t exactly placated by the jobs report. In fact, the futures market now believes that the Federal Reserve will hike interest rates four times in 2022. Futures traders now put a 21% chance on a fifth hike this year. I can’t say I’m surprised. The first rate hike could come as soon as March.

Nerves on Wall Street were soothed today during Federal Reserve Chairman Jerome Powell’s confirmation testimony. There weren’t any surprises. Powell said that the economy is ready for tighter monetary policy. He also said that the economy will only have “short-lived” impacts from Covid.

The markets liked what they heard. Actually, this was the second day in a row the market saw some big reversals. Yesterday, the Nasdaq dropped 2.7% before rallying 2.8% off its low. The index closed slightly in the black yesterday. Today we saw much the same. The Nasdaq initially fell by 0.7% but rallied by more than 2.1% off its low.

What we’re seeing is some pushback from the trend that I’ve talked so much about. During much of November and December, low volatility stocks strongly outperformed high beta. Lately, high beta is getting its revenge. Today, the S&P 500 High Beta index rose by 1.96% while the S&P 500 Low Vol Index fell 0.20%. I don’t expect this to last. The risky stocks still need to lag some more before they’re anywhere close to being reasonably priced.

The market may soon get a lot more interesting. This Friday is the unofficial start of the Q4 earnings season. Citigroup, Wells Fargo and BlackRock are due to report earnings. The stock market will be closed on Monday in honor of Dr. Martin Luther King’s birthday. Then on Tuesday, Goldman Sachs is scheduled to report. I suspect we’ll see very good results.

Tomorrow, the government will release the December CPI report. I think a lot of folks will be on pins and needles for this report. The inflation numbers last time were not good. For November, headline inflation rose by 0.78% while core inflation increased by 0.54%. Over the prior 12 months, headline inflation increased by 6.88% and core inflation rose by 4.96%.

These are some of the highest numbers we’ve seen in decades, and they’ve completely discredited the Fed’s line that it will be transitory. I wouldn’t be surprised if headline inflation for 2021 was close to 7.5%.

For tomorrow, Wall Street expects to see December headline inflation of 0.4% and core inflation of 0.5%. So far, the Fed has only hinted of rate hikes, but inflation may turn out to be a difficult dragon to slay in 2022.

The Fed has come under additional scrutiny lately due to Vice-Chairman Richard Clarida’s stock trades. In February 2020, Clarida sold some mutual funds that he bought back shortly thereafter at the same time the Fed was preparing its response to Covid. Clarida announced that he’s going to resign from the Fed at the end of this week. His term expires at the end of January.

Now let’s look at some good news from one of my favorite Buy List stocks.

Danaher Guides Above Expectations

We had some good news today from Danaher (DHR), one of our Buy List stocks. This is particularly welcome news because the shares had been a little weak lately. In any event, CEO Rainer M. Blair said that Q4 core revenue growth will be above the company’s previous guidance.

Let’s take a step back. In October, Danaher said it expected Q4 core revenue growth “in the low-to-mid teens percent range.” Now the company expects core revenue in the high teens. For Q4 non-core revenue growth, Danaher now expects “high-teens to low-twenties.”

Mr. Blair stated, “Our team delivered an outstanding finish to 2021, with better-than-expected results across all three reporting segments led by Life Sciences and Diagnostics. We were particularly pleased with the strength of our base business across the portfolio, which was up approximately 10% in the quarter. We also saw better than expected revenue growth in Cepheid’s molecular diagnostics business driven by both respiratory and non-respiratory testing demand.”

Blair continued, “Our performance is a testament to the power of our portfolio and our team’s commitment to the Danaher Business System, and we are excited about the opportunities ahead to continue building long-term, sustainable value for our shareholders.”

Danaher does so many things so well that it’s easy to overlook them. Danaher has beaten earnings for the last 26 quarters in a row. For the last six quarters, it’s beaten expectations by more than 10%.

We first added Danaher to our Buy List in 2017. Since then, DHR has gained more than 292% for us. Including dividends, it’s up 302%. That makes it a four-bagger for us.

Danaher will report its Q4 earnings on Thursday, January 27. Wall Street currently expects earnings of $2.48 per share.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. Don’t forget to sign up for our premium newsletter.

Posted by Eddy Elfenbein on January 11th, 2022 at 7:12 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His