CWS Market Review – August 23, 2022

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Great Summer Rally Stalls

The Great Summer Rally of 2022 has finally faced some pushback. On Friday, the S&P 500 fell by 1.29%. Under normal circumstances, that’s not much of a big drop, but considering this summer, it’s noticeable. That was the index’s largest drop since late June.

For more than two months, the bulls were partying, and no bears were in sight. The market increased in value by a cool $7 trillion. The S&P 500 was on pace for one of its best quarters in decades. At one point, the S&P 500 had its best start to a Q3 in 90 years!

Until this point, the market treated every minor dip as a chance to buy. Not this time. The selling pressure continued into Monday as the S&P 500 fell 2.14%. Again, that’s nothing huge, but it stands out in a market that had been so placid. The Nasdaq Composite fell by 2.55% on Monday. The market closed lower on Tuesday as well. In the last week, the S&P 500 has lost a little over 4%.

By the way, that can be a key sign of a change in the market, when a downside move is followed by an even larger downside move. The stock market tends to be very trend sensitive. In other words, whatever the market’s doing, the odds are that it will continue doing it. These trends often play out larger than you think possible.

That means the keys are the turning points. Unfortunately, you can never know the difference between some minor pushback and a true change in sentiment. The same holds true for now. I’ll note in passing that the market got the willies at nearly the precise point that it bumped up against its 200-day moving average (the bluish line in the chart above). I tend to be a skeptic on these technical indicators, but a lot of people think they’re very important, which in turn, makes them important.

What led the summer rally to stall? That’s hard to say, but I’d say it’s a round of the usual suspects. The top of which is the Federal Reserve. The market may be treating last week’s Fed minutes with some new-found respect.

In the minutes, the Fed made it clear that it intends to keep raising rates until inflation is soundly put back in its box, but there had been some doubters. It’s easy and cheap for the Fed to sound tough, but it’s quite another thing to deliver. We even saw in the futures market some expectations that the Fed might start cutting rates during the first half of next year.

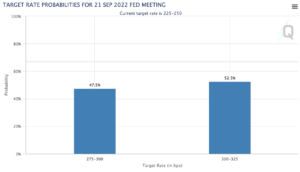

The event looming over the market is Fed Chairman Jerome Powell’s speech at Jackson Hole scheduled for this Friday. At the moment, the market is in a tug of war over what will happen with interest rates next month. One moment, expectations are for a 0.50% hike. Then they’re for a 0.75% hike. Then they’re back to 0.50%. Right now, 0.75% has a slight lead. Powell’s speech may clear things up.

The National Association for Business Economists recently ran a survey of business economists. It found that 52% of respondents said they were “not very confident” in the Fed’s efforts to fight inflation.

I doubt the recent downtick had anything to do with earnings. We have nearly the final numbers for Q2 and it was a decent earnings season. Earnings are up a little over 9% compared with a year ago, which is basically in line with inflation. As of today, 76.1% of companies beat on earnings, 71.3% beat on sales and 59.5% beat on both.

Apple Goes to the Bond Market

There’s some interesting news this week from Apple (AAPL). In a filing with the SEC, the computer giant said it’s going to issue long-term bonds and use the proceeds to pay out dividends and buy back its own stock.

In plainer terms, Apple is borrowing money to invest in itself. That’s not a bad idea if you can borrow for less than what you’re investing in. Right now, Apple pays a tiny dividend yield of 0.55%.

However, I think this move by Apple raises some important questions. The first is, should a company be involved in financial engineering? Some investors, including myself, believe a company should be solely focused on making money. What to do with that money should be left to the owners—the shareholders. I see moves like this as management encroaching on an area that’s not their concern. Unfortunately the government’s shifting tax policy has played a role in determining what companies do with their profits.

This isn’t just a buyback; Apple is borrowing money to fund the buyback. That raises another issue, what if Apple is paying too much for itself? Cisco famously lost billions of dollars investing in its inflated stock. A cash dividend to shareholders gives them the option to buy more or to invest their funds elsewhere.

What’s also interesting about this offering is that the bonds have a maturity of 7 to 40 years. According to Bloomberg, the offering is for $5.5 billion, and the bonds yield 118 points over similarly-dated Treasuries. The initial discussions were for a premium of 150 basis points, meaning there was unexpected demand for the bonds.

In December, Moody’s (MCO), a Buy List favorite, raised its long-term rating on Apple to AAA. That’s a huge deal. That’s roughly Wall Street’s equivalent of being a “made man” in the mafia. No one can touch you. Microsoft (MSFT) and Johnson & Johnson (JNJ) are the only other current members of the AAA club. If Wall Street thinks you’re on the same level as a sovereign government, perhaps you should have a similar debt load? Eh, I’m not so sure.

Apple is sitting on nearly $180 billion in cash. Four years ago, Apple had a cash position of $285 billion. There was a time when Apple had enough cash to buy every single team in the NFL, NBA, NHL and MLB.

Apple could also be taking advantage of lower interest rates. There’s been a surprising recovery in the bond market. During July, the yield on the 10-year Treasury fell by 33 basis points. That was the largest decline in yields in over two years.

Perhaps Apple sees inflation continuing to be a problem. One of the major issues with inflation is that it benefits borrowers at the expense of lenders. If the Fed is going to continue hiking rates, this offering could be quite remunerative for Apple.

This move also sends a positive message from Apple to the market that it plans to buy its stock for many years to come. Also, if Apple does something, then it gives cover for other boards of directors to do the same thing.

Barron’s Features Broadridge Financial Solutions

In our premium service, we’ve been doing well lately with Broadridge Financial Solutions (BR). The shares are up 30% in a little over two months. This is an interesting stock that should be better known.

We recently got a nice bump in Broadridge after the company released a very good earnings report. I was especially pleased to see that Barron’s recently featured the stock: “Broadridge Notches Steady Growth in Uncertain Times.” I won’t give away the whole thing, but here’s a sample:

Broadridge has been a steady stock for rocky times. That is thanks to a model heavy on recurring-revenue businesses and exposure to long-term trends that should remain in place no matter the near-term path of the economy or interest rates. Broadridge stock’s recent rally could cap gains in the near term, but the company’s long-term positive trajectory remains intact.

The company has a near monopoly in the business of managing and distributing investor communications for practically every public company in the U.S., plus mutual funds, exchange-traded funds, and more. That includes proxies, regulatory disclosures, and other reports and filings required of all U.S. securities issuers. Those are non-discretionary communications that companies and funds need to distribute no matter what the world is doing. That segment tends to grow at the pace of overall stockholdings in the U.S., with Broadridge able to eke out higher profit margins thanks to a continuing shift from printed documents delivered by mail to digital investor communications.

Broadridge also has a smaller but faster-growing segment focused on back-office functions for asset managers, investment banks and broker-dealers. Those include trade processing and settlement, record-keeping, and a variety of other compliance or regulatory functions. That is a software-as-a-service business that has expanded through a combination of organic growth and Broadridge buying companies with adjacent or complementary software and services.

For the fiscal year that ended in June, Broadridge earned $6.46 per share. That’s up 14% from last year. The company said it sees further growth of 7% to 11% for the current fiscal year. That works out to an earnings range of $6.91 to $7.17 per share.

The company also hiked its dividend for the 16th year in a row. For nine of the last 10 years, BR has increased its dividend by 10% or more.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want to learn more about stocks like Broadridge, please sign up for our premium service. It’s $20 per month, or $200 per an entire year.

Posted by Eddy Elfenbein on August 23rd, 2022 at 6:07 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His