CWS Market Review – August 30, 2022

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Holy Jackson!

In last week’s issue, I talked about how the impressive summer rally had finally faced some pushback. Until very recently, the bulls had been having a great summer.

We first got a little hiccup after the Federal Reserve released the minutes of its last meeting. Things got a lot worse on Friday when Fed Chairman Jerome Powell said we’re in for “more pain.”

Yikes! One must understand that central bankers simply don’t speak that way. Obfuscation is part of the job description. Alan Greenspan famously said, “I know you think you understand what you thought I said but I’m not sure you realize that what you heard is not what I meant.”

Powell’s words had an immediate impact, and the market gods were displeased. During the trading day on Friday, the Dow lost more than 1,000 points and the Nasdaq Composite dropped 4%. The market fell again on Monday and Tuesday. Since August 16, the S&P 500 has lost over 7%.

It’s about time the Fed acted boldly. To be perfectly honest, the central bank helped cause the inflation, and its predictions consistently understated the threat of higher prices.

Here’s the trend of the Fed’s projection for inflation in 2022:

Sep 2019: 2.0%

Dec 2019: 2.0%

Jun 2020: 1.7%

Sep 2020: 1.8%

Dec 2020: 1.9%

Mar 2021: 2.0%

Jun 2021: 2.1%

Sep 2021: 2.2%

Dec 2021: 2.6%

Mar 2022: 4.3%

Jun 2022: 5.2%

The emergence of inflation was clearly visible one year ago, yet the Fed did nothing. The Fed currently projects inflation of 2.2% in 2024. Yeah, right.

“They Will Also Bring Some Pain”

Let me explain what Powell said and why it was so jarring to the market. First off, this wasn’t just any address. Powell was speaking at the Fed’s annual end-of-summer conference in Jackson Hole, Wyoming.

Since there’s no Fed meeting this month, the conference gets a lot of attention. In previous years, the Fed has used that Jackson Hole conference to announce major changes in policy.

The backdrop of this year’s meeting was a very impressive summer rally. In fact, as I mentioned in last week’s issue, the bulls finally faced some resistance only after the Fed released the minutes of its most recent meeting.

There’s also the all-important issue of persistent inflation. While there has been some improvement, mostly with energy, Americans are still facing rising costs for nearly everything.

Furthermore, there’s concern that the Fed may not realize the enormity of the job before them. I have to count myself among this group. It’s easy for the Fed to talk tough, but it’s quite another to act tough.

Here’s the broader text of what Powell said. I’ve added the boldface.

Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance. Reducing inflation is likely to require a sustained period of below-tren growth. Moreover, there will very likely be some softening of labor market conditions. While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.

Powell was unambiguous that the Fed intends to defeat inflation. Powell said, “We will keep at it until we are confident the job is done.” That’s unusually blunt language for a central banker. The remarks were also unusually brief.

The Fed has already raised short-term interest rates by 0.75% at its last two meetings. Recently, however, some Fed members have expressed concern about the damage the economy has experienced. Just ask anyone you know who works in the housing sector.

There was some concern that the Fed might announce a “pivot” in Jackson Hole and plan on a softer interest-rate policy. Alas, the pivot never came.

Some Possible Softening of Inflation

As it turns out, Friday was also the day that the government released its PCE inflation report. This is the Fed’s preferred measure of inflation. According to the PCE, inflation rose by 6.3% in the 12 months ending in July. That’s down from 6.8% for the 12 months ending in June. While inflation may be decelerating, it’s still high. The goal of 2% inflation is based on the PCE.

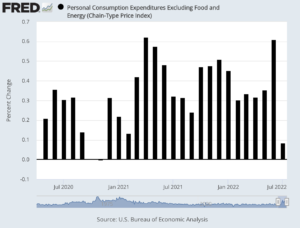

The core PCE rate, which excludes food and energy, is up 4.6% over the last year. During July, the core PCE rate increased by 0.1%. That’s a very big drop from the 0.6% increase we had in June. Powell said, “restoring price stability will likely require maintaining a restrictive policy stance for some time.”

Much of inflation is really an expectations game. If the public expects more inflation, then there will be more inflation. If the public expects inflation to wane, then it will wane. The problem is that once expectations become embedded in the public’s perception, then it’s very hard to undo that. That’s part of the reason why Powell is sounding so tough.

On Friday, Powell said, “The longer the current bout of high inflation continues, the greater the chance that expectations of higher inflation will become entrenched.” He also noted that the economy “continues to show strong underlying momentum” despite some mixed signals on growth.

This Friday, the government will release the official jobs report for the month of August. The last report showed the lowest unemployment rate in 53 years. Some folks had been expecting to see a drop off in the jobs market. So far, that hasn’t happened.

For Friday, the consensus on Wall Street is that the economy created 318,00 net new jobs last month and that the unemployment rate will hold steady at 3.5%. That sounds about right.

The Federal Reserve’s next meeting is on September 20-21. Previously, it had been a tossup in the market’s mind as to whether the Fed would raise interest rates by 50 basis points or by 75 basis points. However, after Powell’s comments, the 75-basis-point camp now has a solid majority among futures traders.

On Tuesday, we learned that jobs openings reached 11.24 million. That was much higher than expectations. That’s nearly two openings for every unemployed person. Economists also like to track the number of people who quit their jobs, and that’s still high. This probably suggests that workers have the upper hand in being able to demand higher wages since it’s relatively easy to find work elsewhere.

That’s all for now. The stock market will be closed on Monday for Labor Day. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want to learn more about the stocks on our Buy List, please sign up for our premium service. It’s $20 per month, or $200 per an entire year.

Posted by Eddy Elfenbein on August 30th, 2022 at 6:57 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His