CWS Market Review – September 6, 2022

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The late summer stall is now turning into something substantial. In 14 trading days, the S&P 500 has given back 9.22% which is more than half of what it gained in the previous two months. As I’ve said, all bear market rallies should be assumed to be phony until proven otherwise.

On Friday, the government reported that the U.S. economy created 315,000 net new jobs last month. Perhaps the most remarkable stat from this report is that it was very close to Wall Street’s forecast of 318,000. I’m afraid Wall Street economists don’t normally have a very good track record of predicting the monthly jobs reports. Or much else.

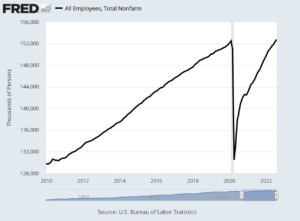

This was the second-lowest monthly gain of the last 16 months. That’s not a reflection on August being so poor but rather on the previous 16 months being very good. In July, the economy added 526,000 jobs. In two months (March and April 2020), the U.S. economy lost 21.991 million jobs. In the 28 months since then, it has made back 22.231 million jobs. That certainly makes for an interesting chart.

Much of the media reported that the unemployment rate rose 0.2% to 3.7%. While that’s technically correct, I dug through the numbers and found that the unemployment rate rose to 3.65% which rounds up to 3.7%. Sure, it’s not a major issue, but the uptick in unemployment is nothing out of the ordinary. Part of that was driven by more people entering the workforce. The labor force participation rate increased to 62.4%.

The labor force participation rate gets a lot of attention, perhaps too much, but one issue with that number is that it’s heavily influenced by demographics. In the 1960s and 70s, that meant women entering the workforce. In recent years, it’s been the aging of the population. That’s why one key stat I like to follow is the labor force participation rate for prime working-age adults (aged 25 to 54). For August, that was 82.8%. That’s very good, and it’s nearly back to pre-pandemic levels.

One weak spot is wage growth, or lack thereof. In August, wages rose by 0.4%. Over the last 12 months, wages are up 5.6%. That’s still below the rate of inflation. We really need to see this number improve.

Another weak spot is that the number of full-time jobs fell to 242,000. Part-time jobs increased by 413,000. This jobs report had ammo for the bulls and the bears.

I should add that historically the August jobs report has been notoriously volatile. Last year, the initial estimate for August was 235,000. That was later revised higher to 483,000. If that’s the case, I have to wonder if it’s even worthwhile to release the initial estimate.

The government also lowered the June jobs number by 105,000. The number for July was lowered by 2,000.

Professional and business services led payroll gains with 68,000, followed by health care with 48,000 and retail with 44,000. Leisure and hospitality, which had been a leading sector in the pandemic-era jobs recovery, rose by just 31,000 for the month after averaging 90,000 in the previous seven months of 2022. The unemployment rate for the sector jumped to 6.1%, its highest since February.

Manufacturing rose 22,000, financial activities gained 17,000 and wholesale trade increased by 15,000.

We’re in an odd situation where the labor market is strong, yet companies are announcing layoffs. The market took the report as being “weak.” That seems off base to me, but the stock market started off Friday well; but then share prices lagged as the day wore on. Nearly the same thing happened on Tuesday.

The next test for the market will come next Tuesday when the government releases the CPI report for August. While there’s been some encouraging news regarding inflation, we still have a long way to go. The price for gasoline has been falling consistently for several weeks.

The big battle on Wall Street right now is for what the Fed will do at its meeting later this month. Some traders expect a 0.5% rate hike while others think it will be 0.75%. Thanks to Powell’s “pain” comment in Jackson Hole, the 0.75% crowd has the upper hand. Still, the jobs report gave the 0.5% hike faithful some ammo. My take is that we should listen to Powell. There’s going to be more pain ahead.

For investors, this means they should continue to focus on conservative stocks such as those you’ll find on our Buy List. In fact, we’ve been outpacing the market in recent days. This is common—our stocks will fall when the market retreats but not as much as the overall market does.

What Happened to the 60/40 Portfolio?

One of the old standbys on Wall Street is the 60/40 portfolio. This is the idea that your portfolio should be 60% in stocks and 40% in bonds.

The idea of the 60/40 portfolio is pretty simple. If stocks started to fall, then the bond market would probably rise which would cushion the blow. Conversely, if bonds started to retreat, stocks were likely to rally.

Since 1976, stocks and bonds have fallen in the same month only 15% of the time. After lots of testing, the 60/40 allocation seems to work best. That gives investors nice gains while reducing volatility.

Except for this year. This has been the annus horribilis for 60/40. It’s having its worst year since 1936.

The culprit isn’t hard to find. It’s inflation. Inflation acts like kryptonite to financial markets. This means that the two elements of the 60/40 portfolio aren’t balancing each other out. Both are down. Higher prices have caused bonds to fall. Plus, the Fed’s response to inflation has led stocks to fall.

There’s also been an important calendar effect. The stock market peaked on the first trading day of the year while many bond indexes peaked a few weeks before the end of 2021.

Another important point is that the 60/40 had a strong run in the years leading up to 2022. Even when adding in 2022, that still means the 60/40 has delivered gains close to its long run average. The 60/40 will have its day in the sun again, but that probably won’t happen until the Fed gets inflation under control again.

We’re also in the period of the year that’s historically been weak for stocks. Looking at the complete history of the Dow Jones Industrial Average, the stock market has historically hit a peak on September 6. After that, stocks retreat until October 29. Historically, the loss has averaged about 2.23%. That may not sound like much, but it stands out when compared to a 126-year average.

Tootsie Roll Is a Stock Like No Other

I used to be a big fan of Tootsie Roll. Not just the candy but the stock. I bet most people assume that Tootsie Rolls are made by Hershey or some other big-time chocolatier.

Not so. Tootsie Roll is its own company. Or to be proper, Tootsie Roll Industries. Its ticker symbol is TR. I remember it as being a classic defensive stock with a great long-term track record.

Then the oddest thing happened. Tootsie Roll disappeared. Not the candy but the stock. It became a ghost. It’s a mystery wrapped in an enigma wrapped in a Tootsie Pop.

Yet, TR still exists. It trades. It pays a small dividend. It’s even a member of the small-cap S&P 600. While some companies keep a low profile, Tootsie went full D.B. Cooper.

The crux of the matter is that a majority of Tootsie is owned by one family. No other company in the S&P 500 has that high a percentage of insider ownership, even Elon at Tesla.

Since the Gordon family owns a majority, they can pretty much do whatever they want. In this case, that means running TR as if it were a private company. The current CEO is 90-year-old Ellen Gordon who was the wife of Melvin Gordon who ran the company from 1962 until he retired shortly before his death in 2015. Before Melvin ran the company, it was headed by Ellen’s father and before that, her uncle. This is a family business.

Tootsie basically ignores the investing world. No Wall Street analyst bothers following the stock. Try calling the company. You won’t get far. They don’t do interviews or investors calls.

Then in early 2021, the improbable happened. Tootsie somehow became a meme stock. The shares nearly doubled in three days. Traders quickly lost interest and TR soon settled back where it had been.

The sad truth is that Tootsie Roll’s business hasn’t done very well in recent years. It’s been mostly flat. The company has issued 3% stock dividends each year for the last several years. (That’s effectively a 103-to-100 stock split.) Although the quarterly dividend has stayed at nine cents per share since 2015, the stock splits have increased the actual payout for long-term shareholders.

One thing going for it is name recognition. That’s very important in business. I bet Tootsie Roll has at least 95% name recognition.

The typical bull case for Tootsie is that it will eventually be bought out for a nice premium. Eh, I’m not so sure. You might have to wait a long time for that to pan out. The family seems determined to keep control.

With Tootsie, perhaps I’m being too cynical and I’m overlooking what’s really a positive story. There’s a family that’s been running their business their own way for decades and they’re determined to ignore the hordes of the investing world.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want to learn more about the stocks on our Buy List, please sign up for our premium service. It’s $20 per month, or $200 per an entire year.

Posted by Eddy Elfenbein on September 6th, 2022 at 7:18 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- August 2026

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His