CWS Market Review – October 18, 2022

The stock market is surging again. Yesterday, the S&P 500 gained 2.65%, and today the index was up another 1.14%.

I’m fine with the gains, but we’ve been burned before. As we know, the stock market loves to use big short-term gains to lure investors back. We’re not falling for it. We’re still in the market, but we’re cautious about it.

Here’s an interesting stat: Prior to today, the S&P 500 was up only five times in the last 20 sessions, but all of those up days were up big. The smallest of the five was a gain of 1.97%.

In other words, the stock market has been working in two modes. Stocks are either zooming higher or they’re down. There seems to be no middle ground. The last two days were in up mode.

Right now, Wall Street’s attention is on focused on earnings season. It’s still early, but we’ve already had several important earnings reports. Goldman Sachs (GS) crushed its earnings ($8.25 versus the estimated $7.69). Johnson & Johnson (JNJ) made $2.55 per share which was a seven-cent beat. Lockheed Martin (LMT) earned $6.71 per share which beat the Street by four cents. Netflix (NFLX) had good news (finally!). The stock is up 14% after hours.

The good news may have calmed the market for the time being. Instead of worrying only about inflation, interest rates and the Federal Reserve, investors are seeing clear evidence that many companies are still making a healthy profit.

The first Buy List stocks will report earnings later this week, and I’m expecting good results. I think there’s a good chance that Stepan (SCL) will announce its 55th dividend increase in a row. There aren’t many companies that can say that.

Our strategy continues to work very well in this market. Here’s a look at the AdvisorShares Focused Equity ETF (CWS) since mid-June:

I need to be clear that our ETF is based on the Buy List, but it’s not exactly the Buy List. Still, it mimics it very well. When investors get scared, they seek out quality and for the last several months, that’s us. Also, we just got our fifth star from Morningstar for our overall rating. You can learn more about the ETF at the AdvisorShares website.

Last Thursday, the stock market got spooked again by another lousy CPI report. Instead of showing that inflation is fading away, the data says it’s still plaguing the economy. For September, headline inflation was up by 0.4% which was 0.1% more than estimates. Core inflation was up by 0.6%. Wall Street had been expecting 0.4%.

This report has pretty much ended discussion on the next Fed meeting. The futures market now places a 95.2% chance that the Fed will hike by 0.75% at its November meeting. I’d say that’s about 4.7999% too low, but that’s me.

It’s not just the November meeting; futures traders are now placing a 66% chance of another 0.75% hike in December. If that’s right, that would mean the Fed will hike by 0.75% five times in a row. These rate hikes are going to do some damage.

Economists See a Recession Coming Next Year

Speaking of which, the Wall Street Journal recently surveyed economists and they placed the odds of a recession starting in the next 12 months at 63%. That’s up from 49% in July. They expect the economy to contract in the first two quarters of 2023.

In July, the economists were expecting the economy to grow in real terms at an annualized rate of 0.8% in Q1 of 2023. Now that’s been pared back to -0.2%. For Q2, the forecast has been pulled back from +1% to -0.1%.

Most economists expect the Fed to raise interest rates too far. That’s a serious concern that I share. The problem with the Fed’s interest rate policy strategy is that it takes a long time to see the results. Historically, that’s caused Fed members to see the lag time as evidence that they’re not pursuing their policy hard enough.

The Fed may also soon impact the labor market.

Economists believe that nonfarm payrolls will decline by 34,000 a month on average in the second quarter and by 38,000 in the third quarter. According to the last survey, they expected employers to add about 65,000 jobs a month in those two quarters.

If there’s a silver lining, it’s that economists see the recession being shorter than the historical average. I would not be surprised to see the Fed start cutting interest rates sometime in 2023. A more pliant Fed would also convince me that any rally is real and not some head-fake.

The healthcare sector has done very well this year in relative terms. That’s not much of a surprise since healthcare tends to be one of the better defensive sectors. Even in a recession, people don’t cut back much on their medical expenses. At least, not the way they do for cars or houses.

Before this year, healthcare had been lagging the market for six years. Beginning in late November, the tide started to turn. At the same time, this is when we saw so many of the high-flying stocks of the Covid era start to lose momentum. More than a few have crashed.

The healthcare sector briefly lagged again this summer during another bear-market rally. As that rally faded, healthcare again started to lead the market. This is a trend that may continue into next year.

Stock Focus: Mettler-Toledo International (MTD)

I’m a big of Mettler-Toledo International (MTD) but the stock doesn’t seem to get much attention, despite having a market cap of $26 billion and a remarkable performance history.

Mettler-Toledo makes scales and lab equipment. It’s a competitor of Thermo Fisher Scientific (TMO). The company is incorporated in the United States, but the headquarters are in Switzerland. The stock IPO’d 25 years ago at $14 per share, and it’s been a huge winner. MTD has never split or paid a dividend. The shares are currently trading at $1,200 (on the nose!). That works out to an annualized gain of nearly 20%.

Mettler-Toledo is having another strong year. For Q2, MTD reported earnings of $9.39 per share. That was a 16% increase over last year’s Q2. It topped Wall Street’s forecast by 63 cents per share. The company also increased full-year EPS guidance to a range between $38.85 and $39.05. That was an increase of 65 cents per share to the low end and 55 cents per share to the high end.

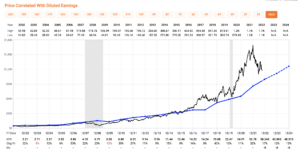

But what I like best about MTD is its “earnings line.” By that I mean that the company’s annual EPS line (the blue line below) is very consistent.

(The chart is from FastGraphs.)

This is an important point about stock valuations. Consider this hypothetical:

Imagine you have two companies that are equal in every way. Both are expected to earn $1 per share next year. However, there’s one important difference. Company A is expected to earn $1 per share, plus or minus two cents per share. Company B is expected to earn $1 per share, plus or minus 20 cents per share. Which stock will have the higher share price?

In almost all normal cases, company A will have a higher share price. This is because Wall Street values the stability of earnings. The premium of A over B will ebb and flow over time depending on the market’s appetite for risk. The premium probably won’t be very much, but it will be visible over the long term.

I use this thought exercise because Mettler-Toledo may have the steadiest earnings line I know of, and that’s why Wall Street gives it a high valuation. Going by today’s price and the company’s latest guidance, MTD is trading at more than 30 times earnings—and that’s in a bear market. The stock is down in 2022. Late last year, MTD was trading north of $1,700 per share.

I also like that Mettler-Toledo has bought back so many shares over the years. I’ve been critical of many companies that use share buybacks as a way of enriching executive bonuses, but MTD has reduced its share count.

For Q3, Mettler-Toledo expects earnings between $9.75 and $9.85 per share. The consensus on Wall Street is for earnings of $9.83 per share. I would be surprised if Q3 earnings came in at less than $10 per share.

In summary, I like Mettler-Toledo a lot. The sad part is that I understand why it’s so expensive.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want to learn more about the stocks on our Buy List, please sign up for our premium service. It’s $20 per month, or $200 per an entire year.

Posted by Eddy Elfenbein on October 18th, 2022 at 6:34 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His