CWS Market Review – November 22, 2022

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Bob Iger Returns to Disney

The big story on Wall Street, at least not involving the letters FT or X, is that Bob Chapek has been fired as the top mouse at Disney (DIS). The company said that Bob Iger would be returning. So they’re changing Bobs. This is especially interesting news to us because Disney had been a Buy List stock.

We ditched Disney at the end of last year and that appeared to be a shrewd move on our part. The stock was down about 40% for the year until last week. After the news of Iger returning, shares of Disney rose as much as 9.99% in Monday’s trading.

Pro-tip: If the news of you leaving your job causes the value of the company to increase instantly by $16 billion, perhaps it wasn’t meant to be.

Disney was a tough purchase for us because we got many of the big things right. We thought that Disney’s streaming service would be a hit, and in the initial months, it proved to be much better than expected.

We added Disney at the end of 2018 at $109.65 per share. The earnings reports were quite good. By April, shares of Disney got to $142 and by November, the stock was over $153. I felt vindicated. I was suddenly a genius!

Then came Covid and the game completely changed. Within a few days, shares of Disney plunged to $80. Sadly, I was no longer a genius. Our entire profit had been wiped out in a few weeks. The whole world got locked down and that included Disney World.

I remember that in an interview, I described Disney as a company that seemed to be tailor-made to be harmed by Covid. It’s actually rather remarkable. Disney’s business is movies, sports and theme parks. If that’s not enough, they also have a cruise line. Everything Covid wrecked is where Disney stood. This is also when Bob Chapek took over.

But then it appeared that Covid would be a big help for Disney. Everyone cooped up in their homes could just stream their way to Disney’s catalog. On top of that, the government and the Fed were throwing tons of money Wall Street’s way, so of course Disney would benefit.

Shares of Disney soared. Less than a year after hitting $80, Disney got to $200! Once again, I was a genius.

Oddly, Chapek seems to have improved in recent months. Over the summer, the company had a solid earnings report. Profits were up and Disney was becoming a major rival to Netflix. The board even extended his contract. Everything seemed great at the Mouse House.

That is, until Disney’s last earnings report which was a disaster. The theme park business was ugly. The streaming business was ugly. ESPN was ugly. Everything everywhere all at once turned ugly.

The streaming service lost $1.5 billion. In one day, Disney’s stock fell 13%. That was its worst day since 9/11. It seemed like Wall Street got blindsided.

Despite the losses, Chapek was very optimistic for the business. So much so that it damaged his credibility. (Lesson: people dislike spin more than the actual bad news being spun.) This was especially tough on Disney because the theme park business has gotten much better. Also, activist hedge funds have been putting pressure on the company.

I didn’t realize it at the time, but the earnings report appears to have been the catalyst that set the board in motion. Now Iger has been hired to be Disney’s CEO through the end of 2024. Bear in mind that Chapek was Iger’s handpicked choice to follow him.

Chapek made several missteps and his relationship with Iger turned cold. Disney also found itself in the middle of several high-profile political arguments. I wonder how much of this was an Iger-led coup. His prints may be near the dagger.

Chapek’s major business decision was to put Disney’s streaming business front and center. The business also includes Hulu and ESPN+. Chapek named his protégé, Kareem Daniel, head of a Disney’s Media and Entertainment Division. Iger didn’t waste any time firing Mr. Daniel on Monday.

In this case, we were ahead of the game. We decided to get rid of Disney at the end of last year when the stock was at $154.89. While that was down from Disney’s high, it turned out to be a very good exit price. The stock was recently as low as $86 per share.

Now I’m not sure if I was a genius or not. In three years, we made 45% in our Disney investment. We got in at a bad time and then waited too long to get out. Still, we got out.

Overall, I’m not sure if changing the person at the top is enough to help Disney. The problems are deep and the entertainment landscape is changing quickly. That’s a common myth, that a change in leadership can revive a company. Sometimes it can, but the problems are often very complex.

The broader lesson on Disney is that we did our homework, and we were vindicated. Still, the story changed, and we were smart enough to cut ties. It wasn’t a massive win or a massive failure. We made money and we moved on. On Wall Street, that’s good enough.

In the near-term, Iger’s re-installation at the top will be a morale boost; but for now, I’m going watch Disney’s stock as a spectator.

Stock Focus: IDEX Corp.

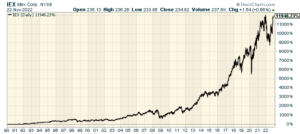

This week, I want to focus on IDEX Corp. (IEX) which is another one of those boring mid-cap industrial stocks that seem to get little attention. The corporate name is derived from “innovation, diversity and excellence.” IDEX is based near Chicago, and it currently has a market cap of about $18 billion.

IDEX is not to be confused with Ideanomics which has IDEX as its ticker, or IDEXX Laboratories.

IDEX is a highly decentralized organization. The company owns 45 largely unconnected businesses. It might be more convenient to list what businesses they’re not in. IDEX makes things like fluidic systems and optics systems and also fire and rescue equipment. Not so sexy, is it?

Still, IDEX’s performance is worthy of respect. Since 1990, the stock is up 120-fold. IDEX now has 8,000 employees and manufacturing operations in more than 20 countries. The company is divided into three main units: Fluid & Metering Technologies, Health & Science Technologies and Fire & Safety / Diversified Products.

The company is having a very good year. Last month, IDEX reported Q3 earnings of $2.14 per share. That beat the Street by 14 cents per share, and it was up 20% over last year. The CEO said, “In the third quarter, we achieved record sales, double digit organic growth across all three of our segments and solid operating margin performance driving record EPS and strong free cash flow generation.”

The company also raised its guidance. IDEX said it expects to make between $1.92 and $1.97 for Q4. That implies full-year earnings of $8.04 to $8.09. If that’s right, it would be an increase of 17% to 18% over last year.

As a conservative estimate, I’d say IDEX can make $8.50 per share next year and $9 per share in 2024. That would give the stock a forward P/E of around 26. That’s high but not unreasonably. Unfortunately, the shares have gained 33% over the last five months. Alas, we can’t invest in a rearview mirror.

CWS Earns Its Fifth Star

We had very good news this week. Morningstar awarded CWS, our exchange-traded fund, its fifth star. This is a big deal.

We got it for our three-year and five-year performance, plus our three-year risk-adjusted performance. The ETF is based on our Buy List.

Here’s the press release from AdvisorShares:

BETHESDA, Md., Nov. 22, 2022 /PRNewswire/ — AdvisorShares announced that the AdvisorShares Focused Equity ETF (Ticker: CWS) has received a Five-Star Morningstar Rating™. CWS earned five stars for its overall (out of 535 funds), five stars for its three-year (out of 535 funds) and five stars for its five-year (out of 494 funds) risk-adjusted returns in Morningstar’s Mid-Cap Growth category, as of October 31, 2022.

The AdvisorShares Focused Equity ETF bases its investment strategy on Eddy Elfenbein’s popular Crossing Wall Street “Buy List.” Elfenbein’s Buy List has published annually since 2006 and carries a wide following. The ETF applies a buy-and-hold strategy: it invests in the stocks of well-run companies that have a history of marketplace dominance, rising sales and earnings, reasonable value, and a record of rising dividends.

Elfenbein believes that a disciplined buy-and-hold strategy is ideal for riding out market storms. CWS strives to buy the highest-quality stocks at the lowest possible prices. By focusing on value, CWS aims to reduce its risk to broad-based market drops. A commitment to value also aids long-term capital appreciation.

CWS also has an innovative fulcrum fee structure where the management fee is directly tied to the ETF’s performance.

Past performance is not indicative of future results. For standardized and month-end performance and more information about CWS, please visit advisorshares.com/etfs/cws.

AdvisorShares regularly hosts live webinars featuring portfolio managers and strategists, including Mr. Elfenbein and other leading industry experts. You may learn more and register at the AdvisorShares Event Center for upcoming event sessions and educational insights.

Here’s our recent performance. We’re the black line. The S&P 500 ETF is the blue line.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want to learn more about the stocks on our Buy List, please sign up for our premium service. It’s $20 per month, or $200 per an entire year.

Posted by Eddy Elfenbein on November 22nd, 2022 at 7:08 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His