CWS Market Review – December 6, 2022

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Case for the U.S. Economy

So far, December hasn’t been so merry for the bulls. The stock market fell today for the fourth day in a row. This comes after an impressive run since the middle of October. Today was the second day in a row that more than 400 stocks in the S&P 500 lost ground.

Is this a small pause in the middle of an overall bull market, or is it the sign of bad things to come? We don’t know the answer just yet. Unfortunately, the market gods can be an ill-tempered bunch.

In this week’s issue, I want to look at the case for optimism. What if everyone, including me, has been wrong about the economy for next year?

For the last several weeks, I’ve believed that the U.S. economy was headed toward a recession next year. I still think it’s very likely, but I want to look at the opposing case. What if the economy surprises us all and continues to grow in 2023?

One of the hardest parts of investment analysis is that it forces you to rethink your prior beliefs constantly. Investors often cause trouble for themselves by clinging to a position that’s no longer tenable. It’s not easy to admit that you had something wrong, but that’s why we have sell orders.

For starters, let’s look at why the economy might face an uphill climb next year. Obviously, the Federal Reserve has hiked interest rates several times, and it’s probably not done. The central bank is also reducing its gigantic balance sheet. That’s a hurdle for economic growth.

The housing sector has already felt the squeeze. This sector stands directly in the line of fire between the Fed and the economy. One of our favorite stocks, Trex, the deck company, is down sharply this year. We also know that the U.S. economy posted negative growth for both Q1 and Q2, although that was for technical reasons.

The tech industry is facing a slowdown and many well-known firms are laying off people. Meta Platforms is down 60% this year. Tesla is down by 48%. Pepsi just announced some corporate layoffs today as well. The economy’s biggest problem is that a few months ago, inflation reached its highest levels in 40 years. It’s not just energy prices that are up. We’ve seen inflation hit nearly every consumer category.

With higher interest rates, the yield curve has become flat and even inverted. That’s often one of the best early indicators that a recession is on the way. Over the last month, the yield on the 10-year Treasury is down about 70 basis points.

The spread between the two- and ten-year Treasuries has been negative every day since early July. The two-year yield has recently been more than 80 basis points higher than the ten-year yield. We haven’t seen a gap like that in over 40 years.

Of course, the most prominent early warning sign was the stock market, which is an imperfect predictor. The S&P 500 peaked on the first trading day of this year. By mid-October, the index was down more than 25%. The damage was particularly felt among growth stocks.

Now let’s look at reasons for optimism. I want to be careful not to overstate the case. Last week, the government revised higher its report for Q3 GDP growth. The initial report said the economy grew in real terms at a 2.6% annualized rate. Now the numbers say it was up by 2.9%.

The Atlanta Fed’s GDPNow forecast now expects Q4 GDP growth of 3.4%. If that’s right, it’s telling us that not only is the economy growing, but it’s accelerating into next year.

Last Friday’s jobs report was a decent one. The U.S. economy added 263,000 net new jobs last month. Wall Street had been expecting an increase of 200,000. The unemployment rate stayed at 3.7%.

Perhaps the best news is that wage growth is finally heating up. During November, wages increased by 0.6%. That was double the rate Wall Street had been expecting.

Leisure and hospitality led the job gains, adding 88,000 positions.

Other sector gainers included health care (45,000), government (42,000) and other services, a category that includes personal and laundry services and which showed a total gain of 24,000. Social assistance saw a rise of 23,000, which the Labor Department said brings the sector back to where it was in February 2020 before the Covid pandemic.

Construction added 20,000 positions, while information was up 19,000 and manufacturing saw a gain of 14,000.

The CNBC article had a great quote from Brian Coulton, chief economist at Fitch, “the Fed is tightening monetary policy, but somebody forgot to tell the labor market.” I think that’s right.

Most importantly, more good news may be brewing on the inflation front. Some commodity prices are starting to cool off. Charlie Bilello points out that lumber prices are at their lowest levels since June 2020. That’s down 78% from its peak in May 2021. Oil futures closed today at their lowest prices of the year. Next Tuesday, the government will release the CPI report for November.

Another omen for better economic news is that the stock market has done well over the last several weeks. From October 12 to November 30, the S&P 500 gained 14%. The Fed meets again next week, and the consensus is that the Fed will hike by 0.5%. This will break the run of four consecutive 75-point increases. It’s clear that the Fed is close to the end of its rate hikes.

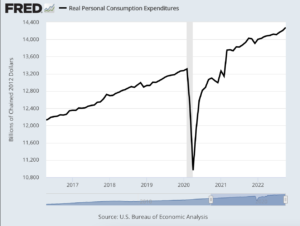

Real consumer spending has been increasing (see chart above), and these numbers will look better as inflation continues to cool. For October, real PCE rose 0.5%. That’s the highest rate since January. Jamie Dimon said that consumers are sitting on $1.5 trillion in excess savings.

I’m not yet convinced that the economy can avoid a recession next year, but I do have to concede that there are growing reasons in favor of a “soft landing.” The most important factor to watch is the path of inflation. The more inflation cools off, the better it is for investors and the economy.

World’s Simplest Stock Valuation Measure

This week, I’d like to show you something special. I call it the world’s simplest stock valuation measure:

Growth Rate/2 + 8 = PE Ratio

Let me emphasize that this is simply a quick-and-dirty valuation tool, and it shouldn’t be used as a precise measure of a stock’s value. But when I’m first looking at a stock and want to see roughly how it’s priced, this is what I’ll use.

For example, let’s look at Bristol-Myers Squibb (BMY). Wall Street expects the company to earn $7.94 per share next year. They also see the company’s 5-year growth rate at 4.14%. (You can find this data at Yahoo Finance. This is the page for BMY.)

If we take half the growth rate and add 8, that gives us a fair value P/E Ratio of 10.07. Multiplying that by the $7.94 estimate gives us a fair price for Bristol of $79.96. The current price for Bristol-Myers Squibb is $79.92, so it’s almost perfectly in line.

Let’s look at FedEx (FDX) which has a higher growth rate. Wall Street sees FedEx earning $17.98 per share next year. They peg the five-year growth rate at 9.3%. Our formula gives us a fair value multiple of 12.65, and that multiplied by $17.98 works out to a value of $227. FedEx is currently at $173.

I like to find stocks that are going for more than 30% below our fair value. As I said, that’s just one tool I use to find bargain stocks.

This tool doesn’t work well with highly cyclical stocks because those companies tend to have earnings that soar and plunge depending on where we are in the economic cycle. Energy stocks are a good example. Also, the valuation tool tends to be conservative. Not many investors buy a stock like Tesla (TSLA) because it passes some valuation screen.

There’s no magic behind the tool. It’s a simplified version of a very complex model that I used to use. I found that I could get 90% of the results with 10% of the work. That’s how the World’s Simplest Tool was born.

I’ve found that the valuation tool is good at spotting anomalies. For example, Wall Street expects earnings next year from Altria (MO) of $5.05 per share. The Street’s five-year estimated growth rate is 4.16%. That gives us a price of roughly $51 per share. MO is currently going for $46, or about 10% below our price. To me, that indicates not how cheap the shares are but rather how nervous Wall Street is about owning controversial and legally problematic stock.

When you see a stock that may superficially be a bargain, you then need to look at why. Oftentimes, a cheap stock is cheap for a very good reason. There truly are diamonds in the rough, but you really need to hunt for them.

Before I go, I want to draw your attention to a strong period of outperformance for our ETF which is based on our Buy List. Over the last eight months, the stock market is down 13% while we have a tiny gain.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want to learn more about the stocks on our Buy List, please sign up for our premium service. It’s $20 per month, or $200 per an entire year.

Posted by Eddy Elfenbein on December 6th, 2022 at 6:52 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His