Posts Tagged ‘orcl’

-

CWS Market Review – September 19, 2014

Eddy Elfenbein, September 19th, 2014 at 7:04 am“The market is fond of making mountains out of molehills and exaggerating

ordinary vicissitudes into major setbacks.” – Benjamin GrahamIs it ever! We all know how the market likes to be a major drama queen, and frankly, that’s what makes investing so much fun. This week, for example, was an exciting week for Wall Street. On Wednesday, Janet Yellen and her buddies on the Federal Open Market Committee decided to taper the Fed’s bond purchases by another $10 billion. Starting in October, the central bank will buy $10 billion in Treasuries and $5 billion in mortgage-backed securities. What this means is that the Fed will almost certainly wrap up Quantitative Easing once and for all at their next meeting in late October.

In addition to their regular policy statement, the Fed threw another statement our way:

A Declaration of Normalization Principles, which describes how the Fed will depart from (as they prefer to phrase it) “monetary accommodation.” I’ll explain what it all means in bit, but skipping all the econo-jargon, it means that we can expect low interest rates to stick around a while longer.That’s good news for investors, and the stock market approved of the Fed’s move. On Thursday, the S&P 500 galloped to 2,011.36, which is the index’s 34th record close of the year. There’s also some relief that the “no” side appears to have won in Scotland’s independence referendum.

Later on in this issue, we’ll look at the recent earnings report from Oracle ($ORCL). The enterprise-software king missed earnings yet again, but the really big news is that Larry Ellison is stepping down as CEO! I’ll tell you what it all means. We also got an 11% dividend increase from Microsoft ($MSFT), which is exactly what I predicted in last week’s CWS Market Review. I’ll also preview the upcoming earnings report from Bed Bath & Beyond ($BBBY). But first, let’s look at why the Fed isn’t going to raise rates anytime soon.

Expect Rates to Stay Low for a Long Time

On Wednesday, the investing world came to a halt to hear what the Federal Open Market Committee had decided. Since there has been some noticeable improvement in the economy, some investors were speculating that the Fed might ditch its key phrase “considerable time” as it pertains to the period between the end of Quantitative Easing and I-Day, the date of the first interest-rate increase. Previously, Janet Yellen described that period as lasting “around six months,” which was a big-time rookie mistake.

As it turns out, the Fed decided to keep its “considerable time” proviso. They also kept the affirmation that “there remains significant underutilization of labor resources,” which is a fancy way of saying there’s still a lot of folks out of work. And that’s certainly true.

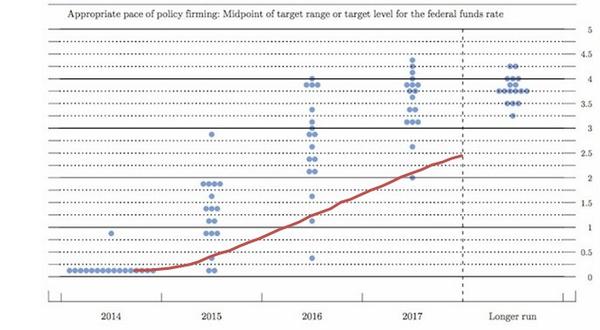

As I mentioned before, the Fed decided to taper its bond purchases, and the next meeting should bring the final taper. So that leads us to wonder: How much longer do we have to wait for rates to rise? We got a hint of that as the Fed also released its projections for the economy and interest rates. The Fed includes a scatter plot of blue dots for each of the 17 FOMC members (not all of whom vote). The most important chart shows where the 17 members of the FOMC see interest rates at year’s end for the next few years, as well as the forecast for the long run.

What I found truly surprising is how hawkish the projections are. Most Committee members see interest rates hitting 1% before the end of next year, and 2.5% before the end of 2016. That’s well ahead of the futures market. I’m surprised to see such a divergence between the Fed and the markets. In fact, it’s a divergence between the Fed and what the Fed has previously said. What’s going on? I noticed that there were two dissenters on the Committee this time, so we may see a growing divide at the Fed. The projections could be an indication that the inflation hawks are growing.

The chart below (courtesy of Jake of EconomPic) shows the FOMC’s projection for interest rates (the blue dots) along with what the futures market currently projects (the red line). Note how much more hawkish the FOMC is.

My view is that there’s no need to raise rates anytime soon. I think mid-2015 would be the earliest possible date. As the policy statement made clear, there’s still a lot of slack in the labor market, and inflation is dead as a doornail. This week, we got more evidence of how tame inflation has been. We actually had deflation last month. The government said that consumer prices fell 0.2% in August. Wall Street had been expecting no change.

Don’t think the low inflation was solely due to lower energy prices, however. The “core rate,” which excludes food and energy prices, was flat last month. Economists had been expecting an increase of 0.2%. This was the lowest core inflation report in more than four years. Remember that with 0% interest rates and deflation, real rates are positive!

There are also plenty of signs that the economy isn’t completely well. Last Friday, the government reported that Industrial Production fell 0.1% last month. This was the first decrease since January. This data series can be a bit bumpy, so it’s too early to say that this could be a sign of trouble. Interestingly, in the Fed’s economic projections this week, the central bank lowered its growth forecasts for next year.

I should also point out an important fact that’s often overlooked. The debate on Wall Street concerns when the Fed will start raising rates. But even when it does, real rates will still be negative, and they’ll probably stay that way for two more years, give or take. Consider that the yield on the five-year TIPs only recently crossed into positive territory.

On Thursday, we got some good news for the labor market. First-time jobless claims dropped to 280,000. That’s one of the lowest reports in the last 40 years. This report, however, can be very noisy, so economists prefer to focus on the four-week moving average. The last jobs report wasn’t very good, so this may be an omen of more strength down the road. As always, it’s important to look at the trend, not just one or two data points. (Naturally we don’t want to exaggerate any ordinary vicissitudes.)

What Does This Mean for Investors?

The market has had an interesting reaction to the Fed this week. In short, what’s been happening has continued to happen, only more so. But I think the market read too much into the Fed’s hawkish projections and assumes higher rates are on the way. Much of the action this week has been the strong-dollar trade (lower gold, lower bonds, higher stocks, large-caps beating small-caps).

The overall stock market responded to the Fed by rallying, but it’s an uneven rally, as we would expect. The spread between large- and small-caps has grown even larger, which is a natural reaction to a stronger dollar. The big boys are leading this rally by a good margin, and the Russell 2000 is actually down for the year. Here’s a remarkable stat: Nearly half of the stocks on the Nasdaq are down by 20% or more. In other words, there’s a stealth bear market going on, even as the broader rally continues.

As I mentioned last week, the U.S. dollar is strong, and it’s getting stronger. The dollar rallied to a six-year high against the Japanese yen. That helped push shares of AFLAC ($AFL) to a new 52-week low on Wednesday. The euro fell to a 14-month low against the dollar.

The same forces are at work in the gold pits. On Thursday, gold fell below $1,220 an ounce for the first time since January. Gold looks ugly, and I think it will get uglier. The Fed’s most important audience, the bond market, responded by selling off. On Thursday, the two-, three- and five-year Treasuries all closed at the highest yield in over three years. But any maturity less than that barely moved. While long-term yields fell for much of this year, they’ve started to rise over the past three weeks. One of the best economic indicators is the spread between the two- and ten-year Treasuries, and that’s increased a bit recently.

What to do now: Investors should continue to focus on high-quality stocks like those on our Buy List. I would pay particular attention to stocks with above-average dividend yields like Ford ($F), Wells Fargo ($WFC) and Microsoft ($MSFT). Now let’s look at one of my favorite tech stocks.

Larry Ellison Steps Down as Oracle’s CEO

After the closing bell on Thursday, Larry Ellison shocked Wall Street by announcing that he’s stepping down as CEO of Oracle ($ORCL). In his place, Mark Hurd and Safra Catz will both become CEO. Interestingly, Oracle’s statement has never referred to them as co-CEOs, which is a concept with a troubled history. Ellison will become Executive Chairman and Chief Technology Officer.

Honestly, I’m not a fan of the dual-CEO concept, and it rarely works. On top of that, no one is truly CEO as long as Larry Ellison is Chairman of the Board. I don’t mean that disrespectfully; I’m a big Larry fan. I like anybody who owns their own MIG-29 or Hawaiian island, but let’s remember that he owns 25% of the shares. I doubt this two-CEO configuration will last more than two years, but I’ll give it a fair shake.

Now on to earnings. For fiscal Q1, Oracle earned 62 cents per share, which was two cents below Wall Street’s estimate. In June, Oracle had given us an earnings range for Q1 of 62 to 66 cents per share. This is the third quarter in a row where Oracle has missed consensus. Quarterly revenues rose 3% to $8.6 billion, which was below the Street’s consensus of $8.78 billion. Oracle had been expecting growth of 4% to 6%.

Hardware continues to be a trouble spot for Oracle. For Q1, hardware sales dropped 8% to $1.2 billion. But there are some bright spots as well. Oracle’s cloud revenue rose more than 30% to $475 million. The company’s cash flow rose 7% to $6.7 billion, which is an all-time record. Oracle also said that it will repurchase $13 billion in shares.

On to guidance. For Q2, which ends in November, Oracle expects earnings to range between 66 and 70 cents per share. Wall Street had been expecting 74 cents per share. Oracle expects top-line growth between 0% and 4%. Frankly, this is a so-so earnings report. It’s not terrible, but it tells me Oracle is still having trouble in key markets. However, I’m not about to abandon them. Oracle remains a buy up to $44 per share.

Bed Bath & Beyond’s Earnings Preview

Bed Bath & Beyond ($BBBY) is due to report fiscal Q2 earnings on Tuesday, September 23. This certainly has a lot of shareholders nervous because the shares have been slammed by the market for the last three earnings reports. It’s clear that the market went overboard last time (down to $55?), and shares of BBBY have slowly inched their way back.

In June, the home-furnishings store told us to expect Q2 earnings to range between $1.08 and $1.16 per share. My numbers say that earnings will come in on the high-end of that range. For all the trouble BBBY has gotten from the market, the company has been consistent with its full-year earnings estimate. It expects earnings growth in the “mid single digits.” If we take that to mean 4% to 6% and apply it to last year’s earnings of $4.79 per share, it gives us a range of $4.98 to $5.08 per share for this year. That means the stock is going for less than 13 times earnings, which is quite reasonable. The company also floated its first bond deal in 20 years to fund $1.1 billion in share buybacks. I can’t say I’m a big fan of that move, but I understand the company’s impatience with the market. Bed Bath & Beyond remains a buy up to $70 per share.

Microsoft Raises Its Dividend By 11%

In last week’s CWS Market Review, I wrote:

Be on the lookout for a dividend increase soon from Microsoft ($MSFT). The software giant isn’t normally thought of as a dividend stock, but they’ve been working to change that. In the last four years, Microsoft has increased its dividend by 115%. The quarterly payout is currently 28 cents per share. I think MSFT will raise it to 31 cents per share.

I was right! After the closing bell on Tuesday, Microsoft ($MSFT) raised its quarterly dividend to 31 cents per share. That’s an increase of 11%. Over the last five years, MSFT has raised its dividend by 138%. The new dividend works out to $1.24 for the year. Going by Thursday’s close and the new dividend, Microsoft now yields 2.66%. Fiscal Q1 earnings are due out in another month. Last Friday, the shares broke above $47 for the first time since Bill Clinton was president. Microsoft remains a very good buy up to $48 per share.

That’s all for now. Next week is the last full week of trading before the end of the third quarter. We’ll get key reports and new and existing home sales. On Thursday, we’ll get the latest report on Durable Goods. Last month’s report was very strong thanks to a surge in aircraft orders. On Friday, the government will update the numbers for Q2 GDP growth. Goldman Sachs said it will be 4.7%, which would make Q2 the best quarter in more than eight years. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – September 12, 2014

Eddy Elfenbein, September 12th, 2014 at 7:13 am“Fate laughs at probabilities.” – Edward Bulwer-Lytton

The stock market is continuing with its subdued ways. This past Tuesday, the S&P 500 dropped 0.65%, for its worst day in five weeks. But the arresting part of that stat isn’t the drop; rather, it’s that the worst day in five weeks was a measly 0.65% loss. By historic standards, that’s barely a ripple, and going by what we saw a few years ago, it’s next to nothing. Tuesday’s plunge snapped the S&P 500’s streak of closing up or down by less than 0.5%. That was the longest such streak in 45 years. As I described it last week, this summer has been the Big Chill for Wall Street.

As I expected, the stock market has been a little weak lately. The S&P 500 is down from its all-time high from last Friday. But the interesting action hasn’t been in the stock market. Instead, the currency markets have suddenly become very interesting. Over the past few weeks, the U.S. dollar has gotten a lot stronger against many currencies around the world (see the chart of the dollar index below). If you’re a traveler, you’ve probably noticed the effects. Investors need to understand that a strong currency has a large impact on the economy and on our Buy List stocks. In this week’s CWS Market Review, I’ll review what it all means.

I’ll also take a look at the upcoming earnings report from Oracle ($ORCL). Their last report was a dud, but I’m expecting better news this time around. I also want to look at the recent weakness in eBay (EBAY), which is normally a solid stock. But first, let’s take a look at last week’s sluggish jobs report and what it means for the Federal Reserve’s interest-rate plans.

Expect Higher Rates Next Year

Last Friday, shortly after I sent out last week’s CWS Market Review, the government reported that the U.S. economy created only 142,000 jobs in August. This was well below Wall Street’s forecast, and it snapped the economy’s six-month streak of creating more than 200,000 jobs.

The weak jobs report put a wrench into the plans of folks who have been expecting the Fed to raise rates this coming spring. As I’ve said, I continue to like the stock market as long as interest rates are near the floor (although I expect some minor sluggishness this month). But once the Fed starts to raise interest rates, the game changes.

Think of it this way: It’s one thing to like Microsoft ($MSFT) when it’s yielding 2.4% and short-term rates are 0% (the one-month Treasury even went negative a few times this week), but it will be quite another if they’re both yielding 2%. As always, the game is about risk and reward.

Lately we’ve been seeing some signs of dissension within the Fed, but that’s to be expected as I-Day approaches. (That’s my term for the date of the Fed’s first rate increase.) Janet Yellen has tried to make it clear that the Fed isn’t on a pre-set course, and that they’ll change as events change. The Fed meets again next week, and all of Wall Street will be watching. In addition to another $10 billion taper announcement, we’ll hear updated interest-rate projections. (I’ll warn you, the Fed’s track record on predicting the economy is terrible.)

But rather than trying to parse various Fed statements for clues, I think it’s better to look at the Fed’s arch enemy, which is the bond market. Here I like to follow the one-year Treasury yield as it compares with the two- and three-year yields (see below). Think of this as the “Yellen Chart” because it’s mainly focused on the first rate increase. This is an interesting chart to follow because the one-year yield has been remarkably flat, but the two and three-year yields have climbed steadily higher. In fact, the yield on the three-year has tripled since April. Not only that, but the gap between the two- and three-years has widened as well. It’s as if the bond market were saying, “higher rates are on the way, but not just yet.”

There are also futures contracts that trade on the Fed funds rate. The latest prices indicate that the market expects the Fed funds rate to be at 0.25% by May 2015 and at 0.50% by September. That strikes me as a bit too soon. Right now, I’d place I-Day around the middle of next year.

What’s also interesting is that at the same time that the middle part of the yield curve has seen higher interest rates, the long yield of the yield curve has seen lower rates. The yield on the 30-year Treasury is down 69 basis points since the start of the year. Lately, however, long-term rates have started to edge higher, which is what I predicted four weeks ago.

What the Strong Dollar Means for Investors

In last week’s issue, I mentioned how the European Central Bank had decided to jump on the bond-buying bandwagon. The economy in Europe has been dreadful, and many euro bonds pay next-to-nothing yields. To quote myself, Mario Draghi is sending a loud message to currency traders: “Please, please, pleeezze bring the euro down!” They’re not alone. Japan has embarked on a similar strategy.

As a result, the U.S. dollar has soared. It’s not that the greenback is strong in an absolute sense. It’s that the dollar is the cleanest of the dirty shirts. Since July, the dollar has rallied from 101 yen to 107 yen today. Meanwhile, the euro has dropped from $1.37 to $1.29.

What’s the impact of the strong dollar? This can be confusing, since it seems normal to assume that the conjunction of the words “strong” and “dollar” can only yield positive results, but that’s not necessarily the case. Like many things economic, it involves tradeoffs. For example, a strong dollar tends to help imports but hurt our export market. Those of you who do a lot of international travel may have noticed that the stronger dollar helps your purchasing power abroad. The same forces are in play for companies. European stocks look cheaper for American companies, so we can expect to see more international buyouts (like Medtronic/Covidien).

A stronger dollar also takes some of the pressure off the Fed to raise rates so quickly. That’s part of the reason I’m skeptical of the futures market on interest rates. People want to invest in the dollar because they see better growth ahead. Goldman Sachs just said that the U.S. economy grew by 4.7% last quarter. If the dollar were weaker, the Fed would have to raise rates to entice people to hold dollars. The dollar rally has taken that potential problem off the table.

Now let’s consider the bad effects of the stronger dollar. The dollar’s rally against the yen has stung AFLAC ($AFL), which is one of my favorite Buy List stocks. The problem is that AFLAC does about 75% of its business in Japan. As a result, it has to convert that profit from yen into dollars. So a strong yen is good for AFL’s bottom line, but a weak one is bad. This is unfortunate, because as far as its business goes, AFLAC is doing quite well. Sadly, a lot of those gains are lost due to currency effects. It’s annoying, but to quote Hyman Roth, “this is the business we’ve chosen.”

In July, AFLAC said they expect full-year operating earnings to range between $6.16 and $6.30 per share, but that forecast assumes a yen/dollar exchange rate between 100 and 105. Now it’s up to 107, which explains why shares of AFLAC recently slipped below $60.

My view is that the currency effect is mostly transitory. Sometimes it helps you, sometimes it hurts. But if a company is well run, it will most likely stay that way. Unfortunately, AFLAC is getting the short end of this stick lately. I still like the stock a lot, and it’s an especially good buy below $60 per share.

A strong dollar also helps keep the lid on inflation, and you can see that in the commodities market. The last few inflation reports have been quite subdued. Last week, I talked about the weakness in gold. This is a direct outcome of the dollar’s surge. Commodity prices are staying well behaved. AAA recently said that the average price for gasoline fell to a seven-month low. In turn, that has helped U.S. consumers (remember the strong earnings report from Ross Stores). A lot of energy stocks have not joined in the rally this year. Stocks like Apple, Microsoft and Facebook are all up over 25% this year, but ExxonMobil, one of the largest companies in the world, is down for the year.

I think some of the dollar’s strength is due to Russia. In one sense, investors flock to a strong currency in times of stress. But also, any sanctions on Russia will probably hurt Europe as well. A strong dollar tends to correlate with large-cap stocks outperforming small-caps, but it’s not a very strong relationship.

The odd part of a rising dollar is that it’s usually the result of good news. People are more optimistic about the domestic economy. The problem is that the good news can lead to bad news like weaker imports. Investors should continue to focus on high-quality companies with strong positions in their markets. Don’t try to second-guess the forex market. That’s a sucker’s game. The best companies know how to plan for their markets and they act accordingly. As always, time is on the side of the disciplined investor. Now let’s look at Oracle’s upcoming earnings report.

Oracle Is a Buy up to $44 per Share

Now that we’re in September, we have two Buy List stocks that have quarters ending in August. Bed Bath & Beyond ($BBBY) is due to report its earnings on September 23. Next Thursday, September 18, Oracle ($ORCL) is due to report their fiscal Q1 earnings.

Three months ago, Oracle bombed their last earnings report. For Q4, the House of Ellison earned 92 cents per share, which was three cents below Wall Street’s consensus. The company had told us to expect earnings to range between 92 and 99 cents per share. It’s unusual to see Oracle hit the low part of their range.

Looking at the numbers, Q4 was surprisingly weak. Quarterly revenue rose only 3.4%, to $11.32 billion, which was $160 million below expectations. One of the keys for Oracle‘s business is sales of new software licenses. For Q4, that came in at $3.77 billion, which was flat. Their hardware revenue, now finally growing, rose only 2%, to $1.5 billion. One bright spot was that Oracle’s cloud revenue jumped 23% to $327 million.

Oracle has said they see Q1 earnings ranging between 62 and 66 cents per share. That’s not so bad. Wall Street had been expecting 64 cents per share. Oracle sees quarterly revenue growth between 4% and 6%. Breaking that down, they expect new software-license revenue to be up by 6% to 8%. Hardware will be between -1% and 3%, but cloud revenue is expected to be up by 25% to 35%. If their guidance is accurate, that tells us that last quarter’s weakness was temporary. Oracle remains a solid buy up to $44 per share.

Updates on Other Buy List Stocks

Be on the lookout for a dividend increase soon from Microsoft ($MSFT). The software giant isn’t normally thought of as a dividend stock, but they’ve been working to change that. In the last four years, Microsoft has increased its dividend by 115%. The quarterly payout is currently 28 cents per share. I think MSFT will raise it to 31 cents per share. The stock recently broke out to another 14-year high. Microsoft remains a buy up to $48 per share.

In last week’s CWS Market Review, I highlighted McDonald’s ($MCD) as an especially good buy. Not good timing on my part. This past week, MCD announced their worst monthly sales in ten years. Same-store sales fell 3.7% in August. When it rains, it pours. The company also said that problems with suppliers in China will knock 15 to 20 cents off this quarter’s bottom line. The burger joint is also getting bullied in Russia by Colonel Putin’s government. A number of McDonald’s have been shut down in Russia due to “sanitary” concerns. (Yeah, right.) The stock briefly dropped below $91 per share, which is a very good price. I’m keeping my Buy Below at $101, but if you can pick up shares under $93, that’s a good longer-term investment.

Shares of eBay ($EBAY) got beat up this week after Apple announced plans for Apple Pay, which will compete against eBay’s PayPal. PayPal is a big money-maker for eBay, and there’s been a lot of pressure on the company to sell the division. As I noted a few weeks ago, just a rumor of that news sent shares of eBay higher. Even though eBay has said they’re not interested in selling PayPal, I think the market’s evident interest will prevail. It usually does. I can’t say whether Apple Pay will crush PayPal, but I think it will add more pressure on eBay to move. The board also has “cover” to make an about-face. I’m lowering my Buy Below on eBay to $55 per share.

That’s all for now. The Federal Reserve meets again next week, on Tuesday and Wednesday. The Fed will update its economic projections (the blue dots), and Chairwoman Yellen will hold a post-meeting press conference. I expect to hear another $10 billion taper announcement. That will bring their monthly bond purchases down to $15 billion starting in October. Next week, we’ll also get the Industrial Production report on Monday and the CPI report on Wednesday. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – June 27, 2014

Eddy Elfenbein, June 27th, 2014 at 7:07 am“And ye shall hear of wars and rumors of wars: see that ye be not troubled: for

all these things must come to pass, but the end is not yet.” – Matthew 24:6Tomorrow is the 100th anniversary of the assassination of Archduke Franz Ferdinand in Sarajevo. The assassination sparked the July Crisis, which eventually led to the First World War. Once the war started, the New York Stock Exchange decided to close down. No one knew the war would last for so long. Soon traders were meeting outside the exchange to do their business (traders never change, do they?). After four months, the NYSE relented and reopened for business.

One hundred years ago today, the Dow Jones Industrial Average was around 80 (it’s not exactly comparable with today’s index, but close enough for our purposes). Since then, the index has doubled, doubled again, doubled again, and doubled four more times—and it’s close to doubling a fifth time. Last Friday, the Dow reached a new all-time high and came within 22 points of cracking 17,000.

It’s been a good century for investors. Of course, 100 years is, shall we say, a rather optimistic time horizon for an individual investor, but my point is to underscore the power of the long term. That’s what stock investing is all about. To quote the Rolling Stones, “time is on my side.” Time is on the side of all disciplined investors, and that was true even when the world was heading towards disaster.

Fortunately for us, we live in a far more peaceful world, but the lessons are the same. In this week’s CWS Market Review, I want discuss the latest mega-deal for one of our Buy List stocks. Oracle ($ORCL) is on the merger warpath again, and this time, they’re buying Micros Systems ($MCRS) for $5.3 billion.

I’ll also discuss the latest plunge in Bed Bath & Beyond ($BBBY). The home furnishing store disappointed Wall Street yet again. The stock dropped more than 7% on Thursday. Here’s the thing: They actually reaffirmed their full-year earnings. I’ll have full details in a bit.

We’ll also look at the horrible GDP revision for Q1. It turns out the economy had its worst quarter in five years. Fortunately, the news looks much better for the rest of this year. I’ll tell you what it all means, but first, what the heck’s going wrong with Bed Bath & Beyond?

Bloodbath & Beyond

After the close on Wednesday, Bed Bath & Beyond ($BBBY) reported Q1 earnings of 93 cents per share. This was one penny below Wall Street’s forecast, although it was within the company’s guidance of 92 to 97 cents per share. Quarterly sales rose 1.7% to $2.657 billion, and the all-important metric for retailers, comparable-store sales, was up 0.4%.

In my opinion, this was a mildly disappointing earnings report, but it’s far from a disaster. The market, however, was very displeased. Shares of BBBY dropped as much as 10% on Wednesday, and this came at the top of a very bad six months for them. The stock eventually closed the day at $56.70, for a loss of 7.2%. That’s its lowest close in 16 months. Yuck!

I realize I’m starting to sound like a broken record, but the problems Bed Bath & Beyond is having aren’t nearly as severe as the market’s behavior suggests. Yes, they’re in a rough spot, but they’re still very profitable. Unfortunately, this is how markets often behave—a stock can either do nothing right or do nothing wrong. Wall Street traders don’t exactly have a dimmer switch. The truth is that BBBY is a sound company that’s working through some issues. The company has been making investments to modernize its systems, and that’s cut into profit margins. They’ve also been hurt by a weak housing market. These are temporary factors.

Let’s look at its guidance. For Q2 (June, July, August), BBBY sees earnings ranging between $1.08 and $1.16 per share. Wall Street has been expecting $1.16 per share. That probably explains much of Wednesday’s sell-off. But here’s the important part. They kept their full-year guidance exactly the same, calling for a “mid-single digit” increase in earnings-per-share. BBBY made $4.79 per share last year. If we take “mid-single digits” to mean 4% to 6%, that works out to a range of $4.98 to $5.08 per share. In other words, the stock is now going for roughly 11 times forward earnings.

Here’s another important fact. Compared with last year’s first quarter, BBBY has 7.2% fewer weighted shares outstanding. In English, they’re gobbling up their own stock at a rapid clip. Unlike so many other companies, BBBY is truly reducing their share count. Plus, the company also has zero long-term debt. I apologize for the volatility, but I think this is one worth sticking with. This week, I’m lowering our Buy Below to $61 per share.

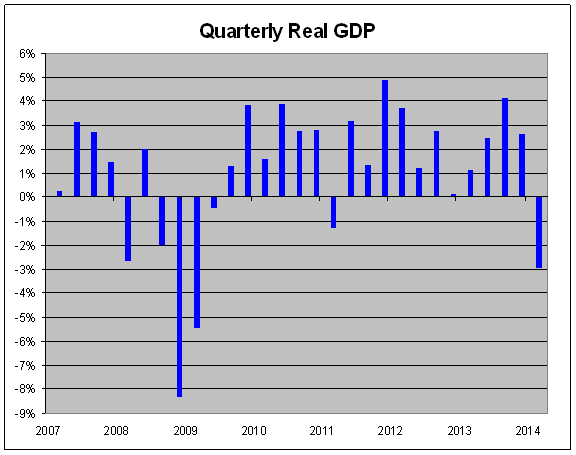

The Economy Dropped by 2.9% in Q1

Wall Street was stunned this week when the government dramatically lowered its report for Q1 GDP growth. The Commerce Department now says that the economy shrank by 2.9% in the first three months of this year (note that GDP figures are annualized and after inflation). That’s the worst quarter for the economy in five years.

Two months ago, the initial report for Q1 GDP showed growth of 0.1%. Last month, that was revised to a drop of 1%. Now it’s down to -2.9%. That’s the biggest downward revision between the second and third reports since records began nearly 40 years ago.

Although these numbers are shocking, I’m pretty skeptical. I’m not saying they’re wrong. I’m just saying…it’s complicated. First, let’s remember that this data is a bit old. It’s for Q1, which was January, February and March, and we’re nearly done with Q2. Also, a huge part of the downward revision had to do with healthcare, since Q1 was the quarter of the Obamacare rollout.

But my major concern is that the GDP numbers don’t line up with more recent data that hint at much stronger growth. Last week, I mentioned that some of the regional Fed surveys are quite optimistic. The trend in jobs is slowly improving. We’ll get the June jobs report next Thursday. Several other metrics like consumer confidence, the ISM reports and industrial production have also looked good. If the economy were truly deteriorating, we would see confirmation in other places. The key weak spot continues to be housing (and by extension, places like BBBY), but that should improve as well.

As investors, our concern isn’t the macro economy but corporate profits. Monday is the end of the second quarter, and soon Corporate America will report earnings results. What’s interesting is that this earnings season will be the first one in several quarters in which we haven’t seen forecasts lowered just before earnings came out. As we all know, Wall Street loves playing the game of guiding analysts lower, then beating those much-reduced expectations.

This time, earnings forecasts have come down some, but not much. The consensus on Wall Street is for the S&P 500 to report earnings of $29.40 for Q2 (that’s an index-adjusted figure). That’s down about 2.5% in the last year, which is very small compared with recent quarters. Typically, analysts overestimate early on, and the forecasts are gradually pared back as earnings season approaches. For now, Wall Street expects full-year earnings of $119.60 for the S&P 500, which means the index is going for about 16.4 times this year’s earnings. That’s slightly on the pricey side, but nowhere near bubble territory.

Next week we’ll get important economic reports that should shed some light on how well Q2 went. Next Tuesday, the June ISM report comes out. The ISM reports have improved for the last four months, and I expect another good number. Due to July 4th´s falling on a Friday, the jobs report for June will come out next Thursday. I think we’ll continue to see improvement of 200,000 to 250,000 jobs. The bottom line is that the Q1 GDP report is an outlier, and it’s old news. The recent data suggest that the economy is poised to grow at 3% annually for the next few quarters.

Oracle Buys Micros for $5.3 Billion

We’ve had a rash of deals on our Buy List. First, DirecTV ($DTV) and AT&T ($T) decided to hook up. Then Medtronic ($MDT) did a big deal with Ireland’s Covidien ($COV). Now Oracle ($ORCL) announces it’s buying Micros Systems ($MCRS) for $5.3 billion.

The deal is for $68 per share, which is a modest premium. However, shares of Micros jumped the Tuesday before last, when initial reports of a deal came out. In the last few years, Oracle has been a merger machine. Over the course of a decade, it has shelled out more than $50 billion to buy about 100 companies. Apparently, Larry Ellison isn’t done. This is Oracle’s biggest deal since they snatched up Sun Microsystems for $7.4 billion four years go. In the last 16 months, Oracle has announced 11 deals.

Micros, by the way, has been an amazing performer. In 1988, the shares were going for just 12.5 cents. The buyout price is 544 times that. Not bad for 26 years. The Micros deal is expected to close by the end of the year. Remember, of course, that any deal has the potential of falling through.

Last week, Oracle missed earnings by three cents per share, and the stock got punished. Fortunately, their guidance was a little better. I think this Micros deal is good for Oracle, and I’m pleased to see them on the offensive. Oracle remains a good buy up to $44 per share.

Buy List Update

This Monday is the final day of trading for the first half of the year. I’ll have a complete review of how the Buy List’s performing. But before then, I can tell you that the Buy List is currently up 1.96% for the year—less than the S&P 500, which has gained 5.89%. Those numbers don’t include dividends. As I’ve mentioned many times, our Buy List has beaten the S&P 500 for the last seven years in a row, and it looks like our streak may be in jeopardy this year. I’m not ready to concede just yet, nor will I depart from our proven strategy, but I want my readers to know exactly where we stand.

Big losers like Bed Bath & Beyond have weighed heavily on our Buy List this year (BBBY is close to a 30% loser YTD). But we’ve also had some bright spots recently. Microsoft ($MSFT), for example, just made another multi-year high on Wednesday. Wells Fargo ($WFC) is also close to a new high. Ford Motor ($F) has shown some strength lately. The automaker just hit an eight-month high on Thursday, and I think it has more room to run. Some of the top bargains on our Buy List include AFLAC ($AFL), Ross Stores ($ROST), eBay ($EBAY) and Cognizant ($CTSH).

That’s all for now. Next week will be an unusual week, since July 4th falls on a Friday. The stock market will be closed on Friday, and it closes at 1 p.m. on Thursday. Expect very light volume, however, since it’s the start of the month. We’ll also be getting the big June jobs report on Thursday morning. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – June 20, 2014

Eddy Elfenbein, June 20th, 2014 at 7:06 am“In this game, the market has to keep pitching, but you don’t have to swing. You can stand there with the bat on your shoulder for six months until you get a fat pitch.” – Warren Buffett

The news got a lot more interesting this week. First, Medtronic ($MDT) announced a mega-merger deal with Ireland’s Covidien. The shares celebrated by jumping to an all-time high. MDT is a 13% winner on the year for us.

Also this week, the Federal Reserve decided on another taper, their fifth in a row. Investors liked what they saw, and the S&P 500 has now rallied for five days in a row. That’s our longest winning streak since April. The index just notched its 21st record high this year. The Nasdaq touched a 14-year high (see below), and the Volatility Index plunged to an 88-month low.

In this issue of CWS Market Review, I’ll walk you through the Medtronic-Covidien deal. Frankly, it’s not ideal, but I recognize that Medtronic had to make a move, and it’s probably the best deal they could get. I’ll also take a look at the recent earnings report from Oracle, and we’ll preview next week’s earnings report from Bed Bath & Beyond. BBBY has gotten beaten down this year, and I think it’s going for a very good price here. I’ll also discuss the Fed’s latest taper move and why the economy is finally looking better (no, really). But first, let’s take a closer look at the $42.9-billion deal Medtronic did with Covidien.

Medtronic Buys Covidien for $42.9 Billion

Two weeks ago, I told you that Medtronic ($MDT) was seriously considering a merger with Smith & Nephew ($SNN). This past weekend, however, the company announced that it’s buying Ireland’s Covidien ($COV) for $42.9 billion. In 2007, Covidien was spun off from Tyco International ($TYC).

What makes this deal interesting is that it’s an “inversion,” which means that Medtronic’s HQ will move from Minneapolis to Ireland, where corporate taxes are much lower. Americans are often surprised to learn that our corporate tax rate is higher than many European countries’ rates. The main corporate rate in Ireland is 12.5%, compared with 35% in the U.S. I think we can expect to see more of these inversion deals in the future. In Medtronic’s case, the tax savings won’t be that dramatic since they already have a modest tax bill thanks to R&D tax breaks.

The deal calls for Medtronic to pay $93.22 per share for Covidien ($35.19 in cash and 0.956 shares of MDT). That was a 29% premium to Covidien’s share price. As an interesting footnote, to qualify as an inversion, the deal has to be at least 20% in stock. With acquisitions, the rule of thumb is that the acquirer’s stock falls. Not this time. Shares of Medtronic initially stumbled, but then a rash of upgrades caused traders to push MDT as high as $65.50 per share on Thursday. That’s an all-time high.

Is this a good deal for Medtronic? It’s complicated. I’m not a fan of mega-mergers. Small rollups are fine, but trying to merge two large enterprises is often more difficult than the planners realize. Having said that, I realize that Medtronic had to make a move. All medical device companies need to. After all, their customers (hospitals and physician groups) have been merging for the last few years, and the device makers are facing those same economic pressures. You can be sure that many of these upcoming deals will be inversions, so expect to hear more talk about Stryker ($SYK) and Britain’s Smith & Nephew.

Ironically, by setting up in Ireland, Medtronic will be able to free up more cash, which they can reinvest in the United States. Medtronic said they plan to invest $10 billion in the U.S. over the next ten years. A lot of these inversions will be between companies that make strange bedfellows, but Medtronic and Covidien are a natural fit. For all the options Medtronic faced, this was the best deal for them to make, so I cautiously support this deal.

As if there’s not enough Medtronic news this week, the company also announced an 8.9% increase to its dividend. I love me a good dividend increase. The quarterly dividend will rise from 28 cents per share to 30.5 cents per share. For the year, that’s $1.22 per share. This is the 37th year in a row that Medtronic has increased its dividend. Going by Thursday’s close, Medtronic yields 1.9%. This week, I’m raising my Buy Below on Medtronic to $67 per share.

The Fed Tapers Again

The Federal Reserve held a two-day meeting this week, and as everyone expected, the central bank tapered its bond purchases again. Starting in July, the Fed will purchase $20 billion in Treasuries each month, plus $15 billion per month in mortgage-backed securities. This is the fifth-straight meeting in which the Fed has tapered.

Tapering by $10 billion at each meeting ($5 billion in Treasuries and $5 billion in MBS) has been the Fed’s game plan all year, and they’ve stuck to it, even when the economy got polar-vortexed earlier this year. In their post-meeting statement, the Fed said that the economy is slowly improving, although housing remains weak.

The Fed has four more meetings left this year. So if we assume they stay on course, they’ll be done with Quantitative Easing (QE) by the end of the year. (I’m assuming the final $5 billion in Treasuries will be tapered in December, but there could be a clear-the-decks move in October.) Janet Yellen has said to expect a rate increase about six months after the end of QE.

As part of this Fed meeting, they also updated their economic projections. You can see them here. Let me caution you that the Fed isn’t exactly known for its accuracy, but it’s interesting to see what its assumptions are. Here’s where it gets interesting. Check out Figure 2 on the PDF. The broad consensus is that the first rate hike will come next year. Twelve of the 16 members agree on that, and I think they’re right. But the consensus falls apart for year-end 2015. There’s a small clustering around 1% to 1.25%, which means that real rates are projected to be negative for at least another 18 months. As long as the lid stays on inflation, that’s very good for the stock market and our Buy List. One of the basic rules about finance is that the stock market loves cheap money.

This week’s inflation report shows that inflation continues to trend upward. Of course, we’re still far from it being a problem, but the rate of inflation is no longer falling. That’s key. The Bureau of Labor Statistics reported on Tuesday that core inflation rose at its fastest rate since October 2009, which is still quite modest. Only now is inflation finally moving into the Fed’s target area.

The Fed’s consensus for year-end 2016 is even more scattered. Their range for short-term interest rates goes from 0.5% to 4.25%, and there are never more than two members that agree on any one rate. I don’t expect a consensus, but I’m shocked to see so little agreement on where the economy will be in 30 months. In short, they see rates going up, but there’s no agreement on how high.

I should point out that two Fed regional surveys this week were quite optimistic. The Philly Fed Manufacturing Survey noticed a big increase in activity this month. Also, the Empire State survey showed that activity in New York is quite good. On Monday, the Fed reported that Industrial Production rose a healthy 0.6% last month. For the first time in a long time, we can say that things are looking up for the economy. Expect to see the economy average over 3% annualized growth for the next few quarters. After five years, the recovery is beginning to be felt on Main Street.

Oracle Misses Earnings by Three Cents per Share

After the closing bell on Thursday, Oracle ($ORCL) reported fiscal Q4 earnings of 92 cents per share. Frankly, that’s disappointing; it’s three cents below Wall Street’s consensus. Oracle said they lost two cents per share due to the currency loss in Venezuela. Shares of ORCL, which had rallied to a 14-year high during the day on Thursday, got smacked around for a 6% loss in the after-hours market.

Three months ago, Oracle said to expect Q4 earnings to range between 92 and 99 cents per share. As it turns out, they hit the low end of their guidance, and business was pretty sluggish in Q4. Quarterly revenue rose 3.4% to $11.32 billion, which was $160 million below expectations.

One of the keys for Oracle‘s business is sales of new software licenses. For Q4, that came in at $3.77 billion, which is flat. Their hardware revenue, now finally growing, rose only 2% to $1.5 billion. One bright spot is that Oracle’s cloud revenue jumped 23% to $327 million. There have also been rumors that Oracle is considering buying Micros Systems ($MCRS) for $5 billion, which would be their largest deal since they bought Sun Microsystems four years ago. Micros makes software for hotels, restaurants and retailers.

Now for guidance. On the earnings call, Oracle said they see Q1 earnings ranging between 62 and 66 cents per share. That’s not so bad. Wall Street had been expecting 64 cents per share. Oracle sees quarterly revenue growth between 4% and 6%. Breaking that down, they expect new software-license revenue to be up by 6% to 8%. Hardware will be between -1% and 3%, but cloud revenue is expected to be up by 25% to 35%. If this guidance is accurate, that tells us that last quarter’s weakness won’t last. Oracle remains a good buy up to $44 per share.

Stay Tuned for Bed Bath & Beyond’s Earnings Report

Our biggest dud this year, by far, has been Bed Bath & Beyond ($BBBY). The stock is off more than 24% YTD. Last week, the shares traded below $60 for the first time in 15 months.

I apologize for the rough ride with this one, but make no mistake, I haven’t given up on BBBY. In the CWS Market Review from May 9, I announced that I was ready to pound the tables for BBBY. This coming Wednesday, June 25, is our first big test. That’s when BBBY will report their fiscal Q1 earnings.

Let’s review where we stand. Three months ago, Bed Bath & Beyond reported terrible results for Q4 (December, January, February). The home-furnishings store earned $1.60 per share. That was eight cents lower than the year before. That was quite a shock, because BBBY delivered earnings increases like clockwork. They estimated that poor weather knocked six to seven cents off their bottom line.

For their Q1 outlook, BBBY had more bad news. They said to expect earnings to range between 92 and 97 cents per share. The consensus on Wall Street had been for $1.03 per share. They made $4.79 all of last year, and for this fiscal year, they expect earnings to rise by “mid-single digits.” If we take that to mean 4% to 6%, their guidance works out to a range of $4.98 to $5.08 per share. Wall Street had been expecting $5.27 per share.

Now let’s look at the items in BBBY’s favor. First is the low share price. The stock is going for about 12 times forward earnings. If we look at one of my favorite valuation metrics, Enterprise Value/EBITDA, BBBY’s is down to 6.15, which is quite low. The company also has a very clean balance sheet: no debt and lots of cash. Let’s remember that the store is well managed, and they’ve ridden through storms such as this before. As the Fed indicated this week, the housing market is still weak, but that won’t last, and stronger housing helps BBBY. You need to be patient with this one, but Bed Bath & Beyond remains a very good buy up to $66 per share.

That’s all for now. Next week is the last full week of Q2. On Wednesday, the government will revise its Q1 report for the second time. The initial report showed growth of 0.1%, but last month it was revised down to -1%. I’m curious to see what happens this time. Also on Wednesday, we’ll get a key report on orders for durable goods. On Thursday, we’ll get the report on personal income. Also on Wednesday, we’ll get the earnings report from Bed Bath & Beyond. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – June 13, 2014

Eddy Elfenbein, June 13th, 2014 at 7:04 am“If you have trouble imagining a 20% loss in the stock market, you shouldn’t be in stocks.” – Jack Bogle

After rallying 11 times in 13 days, the S&P 500 has now pulled back for three days in a row. Despite Wall Street’s give and take, the truly interesting aspects of this market have been the low volatility and very low trading volume. Consider this: Thursday was the market’s worst day in four weeks, and even that was a measly 0.74% loss. It’s been more than two months since the S&P 500 dropped more than 1% in a single day (see chart below). Overall, this has been a very placid spring.

Now some folks are worried about—wait for it—the market’s complacency! Sheesh, some folks aren’t happy unless they’re worried about something. Personally, I’m not too worried about other people worrying about the lack of worrying. They say that bull markets crawl a wall of worry, and that’s certainly true. As usual, we look past our emotions and concentrate on the facts. We’re nearly halfway though the year, and the outlook continues to be moderately favorable for stocks. Sure, the market got a little spooked this week by the troubling events in Iraq, and the price of oil surged higher, but the fundamentals of this market remain quite good. I’ll go into more details in a bit.

I also want to cover the news of the latest jobs report and tell you what it means for us and our portfolios. My take: It’s mostly good news. The economy is improving, but at a tepid rate. The Fed is still on our side, and I’ll let you know what Buy List stocks look especially good here.

This week, we also had a small dividend increase from CR Bard, and I’ll discuss the latest from a former Buy List favorite, Nicholas Financial. The used-car loan company has officially pulled out of its merger deal with Prospect Capital. (Frankly, I didn’t like that deal from Day One.) I’ll also highlight the upcoming earnings reports from Oracle. But first, let’s look at the (mostly) good news from last Friday’s jobs report.

The Economy Added 217,000 Jobs Last Month

Shortly after I sent out last week’s CWS Market Review, the government released the big May jobs report. According to the Labor Department, the U.S. economy created 217,000 jobs last month. (That’s net, of course. The economy is always creating and destroying jobs at the same time.) That’s a decent number, but I’d like to see monthly jobs gains close to 300,000. The unemployment rate was unchanged at 6.3%.

These jobs numbers certainly aren’t great, but they are an improvement. In fact, this latest jobs report marked an important milestone: The number of nonfarm payrolls finally surpassed the pre-recession peak. Of course, the population has grown over that time as well.

This raises the other concern about the jobs market, which is the dramatic decline in workforce participation. To put it bluntly, more and more people have simply left the workforce. The workforce participation rate is at a 35-year low. According to the government’s numbers, when you stop looking for a job, you’re not even counted as unemployed.

An important stat I like to watch is the number of people working compared with the total population. (Note: For population, econo-nerds like to track the civilian non-institutional population over the age of 16.) The ratio of people working to the population has barely budged since the recovery started (check out the chart see below). Part of this can be explained by demographics. Baby Boomers have started to retire, and that’s not going to stop anytime soon. But demographics don’t explain all of the lower participation.

I should add an important caveat to the government’s jobs report. It’s just an estimate, and by the government’s admission, it carries a high error range. They also revise the figures, sometimes considerably, each month. We should pay more attention to the overall trend rather than obsess over an individual statistic.

How is the jobs report important to us as investors? There are two main reasons it’s important. For one, it gives us a good read of where the economy is at the moment. Believe it or not, at the end of this month, the U.S. economy’s recovery officially turns five years old. But many Americans haven’t experienced a recovery at all.

In response to the recession, U.S. companies cut back on their overheads, and that means lower labor costs. The good news is that profit margins soared. While that is good news because it means companies became leaner and meaner, the problem is that profit margins can’t keep rising forever. At some point, you need to get more folks coming through the front door. More consumers come from more employed folks, and that’s how a recovery becomes a positive cycle, each turn reinforcing the next.

Corporate profits and dividends are still growing, although the rate of growth has slowly come down. The latest numbers from S&P 500 show that Wall Street expects index-adjusted earnings from the S&P 500 of $119.65 for this year and $137.30 for 2015. I strongly suspect the latter figure is too high, but let’s work with it for now. If we put a multiple of 16 to it, that gives us a S&P 500 of nearly 2,200 at the end of next year. That’s a gain of 13.8% in a little over 18 months. Please don’t mistake this for a target price for the market. Instead, I want to see if the current valuation is reasonable, and I think it clearly is. For now, any bubble talk is nonsense (although there are some tech values I´m suspicious of).

The other reason why the jobs report is important to us is due to inflation. Once the jobs market gets tight, employment costs start to rise, and that leads to a rise in consumer prices. According to last week’s jobs report, hourly earnings are up 2.1% over the last year. The problem with the lower workforce participation is that we don’t really know how much slack there is in the labor force. The old rules no longer seem to apply.

A lot of commentators have predicted that increased inflation, even hyperinflation, is just around the corner. Please. Every single one of those predictions has fallen flat on its face. Now, however, there are some quiet signs of a little more inflation. Or more accurately, the decline of inflation (disinflation) has come to an end. This is what Janet Yellen and her friends inside the Fed are watching. Remember that inflation is the vital enemy of all central bankers, and the Fed doesn’t want us to go back to the 1970s. Chairwoman Yellen has indicated the Fed will start raising interest rates about one year from now, give or take. Last Friday’s jobs report was another sign that the free-money party will be coming to an end. The Fed meets again next week, and we can expect to hear another taper announcement.

As long as the Fed is on our side, stocks are a good place to be. Some of the best bargains on our Buy List include AFLAC ($AFL), Bed Bath & Beyond ($BBBY), Ford ($F), Oracle ($ORCL), Ross Stores ($ROST) and eBay ($EBAY). Be disciplined with your buying, and don’t chase stocks. Pay attention to my Buy Below prices.

CR Bard’s Amazing Dividend Streak

At the end of last week’s issue, I said to expect a dividend increase very soon from CR Bard ($BCR). That’s exactly what happened a few days later. I wish I could say that this was due to my most amazing powers of prognostication. Sadly, it’s not. Bard has increased its dividend every year since 1972, and they kept that streak going one more year.

Actually, that sums up our investing strategy. We predict the perfectly obvious and wait until the payoff is good. Whenever I hear that someone predicted this or forecast that, I’m immediately suspicious. Bard said they’re raising their quarterly payout from 21 to 22 cents per share. That’s an increase of 4.76%, which isn’t much, but I’ll take it. The dividend is payable on August 1 to shareholders of record at the close of business on July 21.

Shares of Bard have gotten dinged recently. Given the new dividend, the medical-equipment company now yields 0.62%. CR Bard remains a good buy up to $151 per share.

Earnings Preview for Oracle

Oracle ($ORCL) has been one of the hotter stocks on our Buy List. The shares are up nearly 10% for the year, and they just hit another 14-year high. We’re closing in on Oracle’s all-time high of $46.47 from September 1, 2000. Oracle is due to release its fiscal fourth-quarter earnings report after the closing bell on Thursday, June 19. The stock has perked up lately, which is nice to see because there are a lot of Oracle haters.

In March, Oracle reported earnings of 68 cents per share, which was two cents below consensus. Interestingly, Oracle got pounded in after-hours trading. Fortunately, we don’t get involved in the short-term trading game. Instead, we sat back and waited. Sure enough, sense returned to the market, and Oracle is up significantly since then.

On the March earnings call, Oracle said that Q4 earnings should range between 92 and 99 cents per share. That’s a decent forecast. The Street had been expecting 96 cents per share. Oracle also said Q4 sales should rise between 3% and 7%. The company gave a range of 0% to 10% for hardware sales, new software-license revenue and cloud sales. Last quarter was the first increase in hardware sales since Oracle bought Sun Microsystems four years ago.

A lot of techies will be looking out for the guidance Oracle offers for Q1. Wall Street currently expects earnings of 64 cents per share. I suspect that might be at the high end of Oracle’s range, but I’m not yet sure. For FY 2015 (ending next May), we can expect earnings of about $3.20 per share, which means the stock is still going for a good value. Tech writer Ashlee Vance pointed out what “Oracle has done perhaps better than any other major business software maker, which is make the transition from the old to the new in a highly profitable way.” Oracle remains a solid buy up to $44 per share.

The Prospect Capital/Nicholas Financial Deal Is Dead

I wanted to give you an update on one of our old Buy List stocks, Nicholas Financial ($NICK). I took NICK off this year’s Buy List after the company got a buyout offer from Prospect Capital ($PSEC). I wasn’t thrilled with the deal, as I thought NICK was selling itself for too little.

According to the terms of the deal, if it wasn’t closed by June 12, then NICK had the right to walk away. As soon as the deal was announced, there were problems. The SEC wanted PSEC to restate their financials, and that caused the deal to drag on and on.

Finally, on June 11, the SEC reversed itself and said PSEC didn’t have to restate their financials. But that wasn’t enough to placate Nicholas Financial. NICK’s board met and decided to terminate the deal. That’s a difficult call, but I think it was the right decision.

I honestly don’t know where this leaves NICK. The stock dropped down to $14.68 by Thursday’s close. I think the most likely outcome is that another bidder will come along to snatch them up, but who knows when or at what price? I think a private equity firm could get a very good deal, but the bottom line is that I don’t believe NICK is an attractive buy here.

The lesson for us is that merger deals can be tricky things. Never expect some white knight to come along to solve all your problems. This same lesson can be applied to the AT&T/DirecTV deal. While I think that deal will eventually close, we have to keep in mind that it, too, has risks. Anything from shareholder objections to government regulations can trip up the deal. No deal is a sure thing.

That’s all for now. The Federal Reserve meets again next week. Expect to hear another $10 billion taper announcement on Wednesday afternoon. We’ll also get the Industrial Production report on Monday and the Consumer Price Inflation report on Tuesday. The last two CPI reports have shown emerging signs of inflation. It will be interesting to see if this trend continues. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – April 4, 2014

Eddy Elfenbein, April 4th, 2014 at 6:58 am“There will be growth in the spring.” – Chauncey Gardiner

T.S. Eliot famously called April “the cruelest month,” but it’s not so bad for the stock market (Eliot himself was a Lloyd’s Bank employee). Since 1950, the S&P 500 has rallied 44 times in April while losing ground 20 times, and recent Aprils have been especially good. In the last eight years, the S&P 500 has averaged over 3% in April.

This April has gotten off to a good start as well. On Thursday, the S&P 500 got as high as 1,893.80, which is yet another all-time intra-day high. I’m not much of a fan of the Dow Jones, but I should note that until this week, the Dow 30 had failed to break its high from December 31. Some bears claimed that this lack of “confirmation” was a bad omen. Well, that mark fell as well. On Thursday, the Dow broke 16,600 for the first time ever.

What’s the cause for the recent rally? That’s hard to say exactly, but I suspect that the cooling-off of tensions in Eastern Europe has helped a lot. Investors were also buoyed by some remarks made by Fed Chair Janet Yellen. We also got some decent economic news this week, and there seems to be some optimism for Friday’s jobs report (as usual, I’m writing this before the report comes out.)

But the next big event for investors is the Q1 earnings season, which starts next week. We already know that crummy weather held back consumers this winter, but it will be interesting to hear what kind of guidance companies have for the spring. In this week’s CWS Market Review, I’ll preview this earnings season. I’ll also focus on two Buy List earnings reports for next week: Bed Bath & Beyond and Wells Fargo. I also have several new Buy Below prices for you. But first, I want to take a look at a question that keeps popping up on Wall Street.

Are We in Another Bubble?

There’s been a lot of loose talk lately about how today is similar to the Great Millennium Bubble. A few days ago, the New York Times ran a story titled “In Some Ways, It’s Looking Like 1999 in the Stock Market.”

Oh, please. This is nonsense. Sure, stock prices have rallied, and yes, valuations are higher, but c’mon, we’re nowhere close to the kind of crazy numbers we saw in the late 90s. Back then, all you needed was a dot-com address, a sock puppet and some clever ads, and presto, investors would throw billions of dollars your way.

Actually, your company didn’t even need to be that fancy. I’ll give you a good example. General Electric ($GE) is about the bluest blue chip you can find. The stock is currently going for $26.23 per share. That’s half of where it was 14 years ago, yet the company is expected to earn $1.70 per share this year. Compare that to 2000, when GE’s bottom line was $1.27 per share. So profits are up 34% in 14 years (not so good), while the stock price is down by 50%. GE’s Price/Earnings Ratio has dropped from 42 to 15. My point is that people have forgotten what a real bubble looks like.

To be sure, there are areas of the market looking bubbly. Actually, to be more specific, it’s areas outside the market that look troublesome. Tech companies are paying some hefty prices for start-ups with little or no revenue.

Last year, Yahoo shelled out $1.1 billion to buy Tumblr. The company has so little revenue that Yahoo isn’t even required to list it in its financial statements. In business jargon, that’s what we like to call “not good.” A few weeks ago, Facebook paid a massive amount, $19 billion, for WhatsApp, a company with 55 employees. I freely admit that I can’t judge the value of enterprise like that, but there seems to be a fear in Silicon Valley of being left behind in this week’s app of the century, so these prices are getting carried away.

But that’s not the kind of investing we’ve been doing, and our stocks haven’t done many mega-deals lately (though Oracle did a few years ago). My advice is to ignore all the silly bubble talk, and let’s focus on what the numbers say.

Breaking down Q1 Earnings Season

Now let’s take at a look at some current numbers and the outlook for Q1 earnings. Last year, the S&P 500 earned $107.30 (that’s the index-adjusted number; to convert to actual dollar amounts, multiple by 8.9 billion). Currently, Wall Street expects the index make $120.04 for this year and $137.20 for 2015. In my opinion, both numbers are too high, but I’ll get to that in a bit.

For Q1, Wall Street currently expects earnings of $27.60. Those estimates have drifted lower over the past several months. One year ago, the Street had been expecting over $29 for Q1. As a general rule, earnings estimates start high and gradually fall as earnings season gets closer, so don’t be alarmed about the reduced estimates. By the time earnings season arrives, estimates are often too low. This is part of a game the Street likes to play. There’s nothing Wall Street likes better than beating expectations, so companies know how to play the expectations game. The current Q1 estimate of $27.60 works out to an increase of 7.1% over last year’s Q1. That sounds about right. I think we’ll probably be at about $28 by the time all the reports have come in.

I also want to touch on an important and often-overlooked point, which is dividends. Payouts have been growing impressively for the last few quarters. Dividends for the S&P 500 grew by 15.1% for Q1. Technically, I should say “dividends-per-share,” because the stock market has been helped by a reduced share count, thanks to stock buybacks.

Over the last three years, dividends are up by 55%. The S&P 500 paid out $34.99 in dividends last year, and I think it will pay out $40 for this year. Going by Thursday’s close, that gives the index a yield of 2.12%. That’s not bad at all, especially in an environment where interest rates are near 0%, and we know they’ll be stuck on the ground for another year.

Instead of the $120 that Wall Street expects in earnings from the S&P 500, I think $115 is a more reasonable estimate. (I don’t know if it will be more accurate, but I think it’s a safer assumption.) That gives the S&P 500 a forward P/E Ratio of 16.4, which is quite reasonable. Historically, more bull markets are upended by deteriorating fundamentals than by excessive valuations. How far the markets fall, however, is usually determined by valuations. As long as profits continue to grow, the stock market is a good place to be.

Is the U.S. Stock Market Rigged?

This week, Wall Street has been buzzing about Sunday’s 60 Minutes segment with Michael Lewis. He was on to discuss his new book, “Flash Boys,” which covers High Frequency Trading. In the interview, Lewis said that the U.S. stock market is “rigged.” I was disappointed to hear him say that. Lewis is a gifted writer, but I’m afraid he drew an overly simplistic narrative for a complicated issue.

Let me put your fears to rest. The U.S. stock market is not rigged. Individual investors have no reason to fear that a bunch of super computers are ripping them off. There are serious concerns about HFT, but saying that the market is rigged deflects the debate in a pointless direction.

I wanted cover this topic because it’s made so much news on Wall Street this week, including an acrimonious debate on CNBC, and I’m afraid Lewis’s interview rattled investors. The issue with HFT is an issue we often see: technology is changing the way we do business. Some of the changes are good, and some are bad. Instead of having floor traders, guys who make funny hand signals at each other, the modern market is governed by very fast computers. The HFT guys provide liquidity, and they get paid for it. On balance, that’s much better than the system we used to have.

I have concerns about HFT causing more numerous and more severe Flash Crashes, and I like to see that addressed. Fortunately, our strategy isn’t based on trading. I change the Buy List just once a year. I guess you could call us Low Frequency Traders. But I want to assure investors that the U.S. market is not rigged.

Don’t Count out Bed Bath & Beyond

This Wednesday, April 9, Bed Bath & Beyond ($BBBY) will release its fiscal Q4 earnings report. Let me fill you in on the back story. In early January, BBBY cut their Q4 (Dec/Jan/Feb) earnings estimate. They had been expecting earnings to range between $1.70 and $1.77 per share. Now they said it would be between $1.60 and $1.67 per share.

The stock market wrecked the shares. In one day, BBBY plunged from $80 to $70. It continued to fall for the rest of January, and it got as low as $62 per share in early February. If that wasn’t enough, one month ago, the company lowered their Q4 estimates again. This time it was due to the lousy weather. Now they expect earnings between $1.57 and $1.61 per share.

So where do we stand now? I still like Bed Bath & Beyond, and this is why we have a locked-and-sealed Buy List. We didn’t jump ship in a panic, and the shares have started to rebound. Yesterday, BBBY came within a penny of hitting $70 for the first time in three months. I think the market has basically written off the Q4 earnings report and is now focused on their guidance for Q1.

For last year’s Q1, BBBY earned 93 cents per share. The Street currently expects $1.03 per share. I’m going to hold off making a forecast, but I’m still optimistic for BBBY. The company has a rock-solid balance, they’re well run and the recovery in housing is good for them. For now, I’m going to keep our Buy Below for BBBY at $71 per share. Don’t count these guys out.

Wells Fargo Is a Buy up to $54 Per Share

Next Friday, Wells Fargo ($WFC) will be our first Buy List stock to report for this earnings cycle. As I mentioned last week, Wells passed the Federal Reserve’s stress test with flying colors. The Fed also had no objection to WFC’s capital plan, which included a 16.7% increase to their dividend. Wells now pays 35 cents per share each quarter.

In my opinion, Wells is the best-run big bank in America, and it’s better than a lot of small banks. The shares came very close to breaking $50 this week. Wall Street currently expects earnings of 96 cents per share. My numbers say that’s about right, so don’t expect any major earnings beat. The new dividend gives Wells a yield of 2.81%. I’m keeping our Buy Below at $54 per share.

Six New Buy Below Prices

The recent rally has been very good to us. Through Thursday, our Buy List is up 3.29% for the year, which is ahead of the S&P 500’s gain of 2.19%. Three of our stocks, DirecTV ($DTV), Stryker ($SYK) and CR Bard ($BCR), are already up more than 10% this year. Plus, Microsoft ($MSFT) and Wells Fargo ($WFC) aren’t far behind. This week, I’m raising the Buy Belows on six of our stocks.

Two weeks ago, I said that I expected Oracle ($ORCL) to soon break through $40 per share, and that’s exactly what happened. In fact, the stock hit $42 per share on Tuesday. Oracle hasn’t been this high in 14 years. (Remember how the stock dropped after the last earnings report? It’s funny how quickly people forget those short-term reactions.) This week, I’m bumping up my Buy Below on Oracle to $44 per share. I really like this stock.

Ford Motor ($F) has been especially strong lately. Two months ago, the shares pulled back below $14.50, and it recently closed at $16.39. Ford just reported very good sales for March. I’ll repeat what I’ve said before: I think Ford is worth $22 per share. I’m raising my Buy Below on Ford to $18 per share.

Three of our healthcare stocks, CR Bard ($BCR), Medtronic ($MDT) and Stryker ($SYK), broke out to new highs this week. I’m expecting more good earnings news from all of them. I’m raising my Buy Below on Bard to $152 per share. Medtronic is going up to $65, and Stryker’s is rising to $90 per share.

I’ve raised my Buy Below on Qualcomm ($QCOM) for the past two weeks, so I might as well make it three in a row. This stock continues to rally higher for us. On Thursday, QCOM topped $81 per share for another 14-year high. I’m raising Qualcomm’s Buy Below to $87 per share. This could be a break-out star for us.

That’s all for now. First-quarter earnings season kicks off next week. Bed Bath & Beyond reports on Wednesday. Then the big banks start to chime in Friday when Wells Fargo reports. Investors will also be paying attention to the latest Fed minutes, which come out on Wednesday. If you recall, the market was rather confused by Janet Yellen’s press conference. The minutes may clear things up. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – March 21, 2014

Eddy Elfenbein, March 21st, 2014 at 8:56 am“…something on the order of six months.” – Janet Yellen

With those words, the new Fed Chairwoman sent world markets into a tizzy. How could that be, and what, pray tell, did she mean?

Fear not, gentle reader, for I am well versed in the convoluted sub-dialect of Fed-speak, and I’ll lead you through Wall Street’s latest hissy fit. The bottom line, as I’ll explain later, is not to worry. Traders are freaking out over nothing special.

After six painful years, the economy is slowly returning to something approaching normal. Soon, workers will be able to demand higher wages, and consumer prices will rise. This is good news—it’s what we want to happen. A side effect is that we’re soon going to return more traditional monetary policies, and that will apparently take some getting used to. In this week’s CWS Market Review, I’ll explain what you need to know.

I’ll also walk you through the latest earnings report from Oracle. The bottom line number was a tad disappointing, but that was more than made up for by rather rosy guidance. I expect the enterprise software giant soon to hit $40 per share, which it last touched 14 years ago. I’ll break it down in a bit, but first, let’s look at this week’s Fed meeting and why everyone’s scratching their heads.

The Fed Ditches the Evans Rule

Before I get into this week’s Federal Reserve meeting, let’s back up a bit and explain how we got where we are. When the economy plunged into recession, the Federal Reserve responded by dramatically cutting interest rates in an attempt to cushion the blow and hopefully turn things around. Soon, the Fed got to 0% and couldn’t cut any more. Many of the top economic models said that short-term interest rates should be negative—pay people to borrow money!

The Fed decided the best way to get below 0% was to buy bonds. Lots and lots of bonds. The fancy term for this is Quantitative Easing or QE. They tried this a few times for limited periods, but it wasn’t enough. Finally, they threw up their hands and said, “we’re going to buy bonds until things get better.” Specifically, the plan was to purchase $85 billion each month in Treasuries and mortgage-backed bonds.

The market loved the plan, and stock prices soared. But investors wanted to know: How long would the bond-buying party last? The idea floated by Charles Evans of the Chicago Fed was to lay out a specific unemployment number and say, “we won’t end QE until we hit this number.” The Fed adopted the Evans Rule and said that 6.5% unemployment was their threshold. (The Evans Rule also included 2.5% for inflation, but we’re a long way from that.)

Stock prices continued to climb, and the unemployment rated started to fall. Then some investors got nervous because we were getting close to 6.5% on jobs, but the economy obviously needed more QE. The reason is that so many people had left the workforce, and as a result weren’t counted as part of that 6.5%. In other words, the economy is weaker than that unemployment number suggests. As a result, the belief was that the Fed would soon abandon the Evans Rule (I first mentioned this in January), and that’s exactly what happened this week. The Fed ditched the Evans Rule.

Yellen Confuses the Market

Now that leads us to the next step, and here’s where things get a little complicated. Last June, the Fed signaled that it was planning to pare back on its bond purchases. The market, predictably, freaked out. This was the famous Taper Tantrum. In four months, the three-year Treasury jumped from 0.3% to nearly 1%.

Investors believed, incorrectly, that the entire rally was due to QE, so once that was gone, the market was toast. Not only did they get that wrong, but they completely misjudged the timing of the Fed’s taper decision (to be fair, the miscommunication was mostly the Fed’s fault). Ultimately, it wasn’t until December that the Fed decided to taper its monthly bond-buying by $10 billion. In January, the Fed tapered by another $10 billion, and they did it again this week.