-

Morning News: April 3, 2024

Posted by Eddy Elfenbein on April 3rd, 2024 at 7:03 amChina’s Service Economy Expands Further, Adding to Signs of Recovery

Milei Races Against Time to Ease Pain Unleashed by Shock Therapy

South Africa Tax Agency to Target ‘Professional Enablers’ of Organized Crime

Inflation Cools in Eurozone, Nearing Central Bank’s Target

Bank of England sets out conditions for ‘digital sandbox’

Canada’s RBC Struggles to Go Green While Financing Oil

Fed Blocks Tough Global Climate-Risk Rules for Wall Street Banks

Exxon’s $60 Billion Fight With Chevron Will Reshape Big Oil

LNG Demand Shift to Developing Nations Is Transforming the Market

US, EU Are Set to Miss a Critical Minerals Agreement This Week

Pimco Boosts Bond Bets That Fed Will Cut Less Than Global Peers

Chase Bank to Let Advertisers Target Customers Based on Spending Data

I’m an Economist. Don’t Worry. Be Happy.

Biden and Corporate America? It’s ‘Complicated.’

The Jobs Numbers Aren’t Adding Up. Immigration Helps Explain Why

10,000 Migrant Crossings a Day Upend the US Presidential Election

Donald Trump’s Lenders of Last Resort: Subprime Auto King and Online Bank

The World’s Richest Person 2024

AI Enthusiasm Hides Little VC Investor Excitement for US Startups

Alibaba Ramps Up Share Buybacks

Archer Sees 2025 Air-Taxi Debut, Setting Up Rivalry With Joby

Tesla Shares Tumble Toward Make-or-Break Level in Latest Wipeout

What Tesla’s Troubles Signal for the E.V. Revolution

Amazon to Remove ‘Just Walk Out’ Checkout Technology at U.S. Grocery Stores

Switching From iPhone to Android Is Easy. It’s the Aftermath That Stings

Disney Moving Closer to Win Over Trian With Vanguard Backing

How Bluey Became a $2 Billion Smash Hit—With an Uncertain Future

Be sure to follow me on Twitter.

-

CWS Market Review – April 2, 2024

Posted by Eddy Elfenbein on April 2nd, 2024 at 6:16 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Over the weekend, I posted what I thought was a harmless joke on Twitter (or X, or whatever we’re supposed to call it these days):

A great way to make passive income is to take $3 million and buy an 8% Treasury bond.

You'll make $20,000 a month just by doing nothing.

— Eddy Elfenbein (@EddyElfenbein) March 30, 2024

Most people who saw my tweet took it as an obvious joke. At last count, the tweet had over 10,000 “likes.” Indeed, it’s hard to parody some of the financial advice you see on TikTok (check out the brilliant @TikTokInvestors for a sample).

However, not everyone saw my tweet as humor. Of course, U.S. Treasuries yield nowhere close to 8%, and most people don’t have a handy three million dollars lying around. This is a reminder of Poe’s Law that any sarcasm, no matter how absurd, will be taken seriously by someone, and those someones were angry at me. Very angry.

You may wonder: how could our meek, humble, dutiful editor ever cause anyone any distress? Alas, it can happen.

My tweet even got a famous Community Note attached to it. They literally fact-checked a joke.

If I were the pedantic type, I’d point out that the Community Note is incorrect because a two-month treasury is a bill, not a bond. Happily, I’m not, so I won’t bother to mention it.

How to Invest $100,000

I’ve always believed that one should try to turn an unpleasant experience unto something positive. Therefore, in today’s issue, I want to show you how you can safely build an income-producing stock portfolio. Unfortunately, it won’t yield 8%, but it can do a good job.

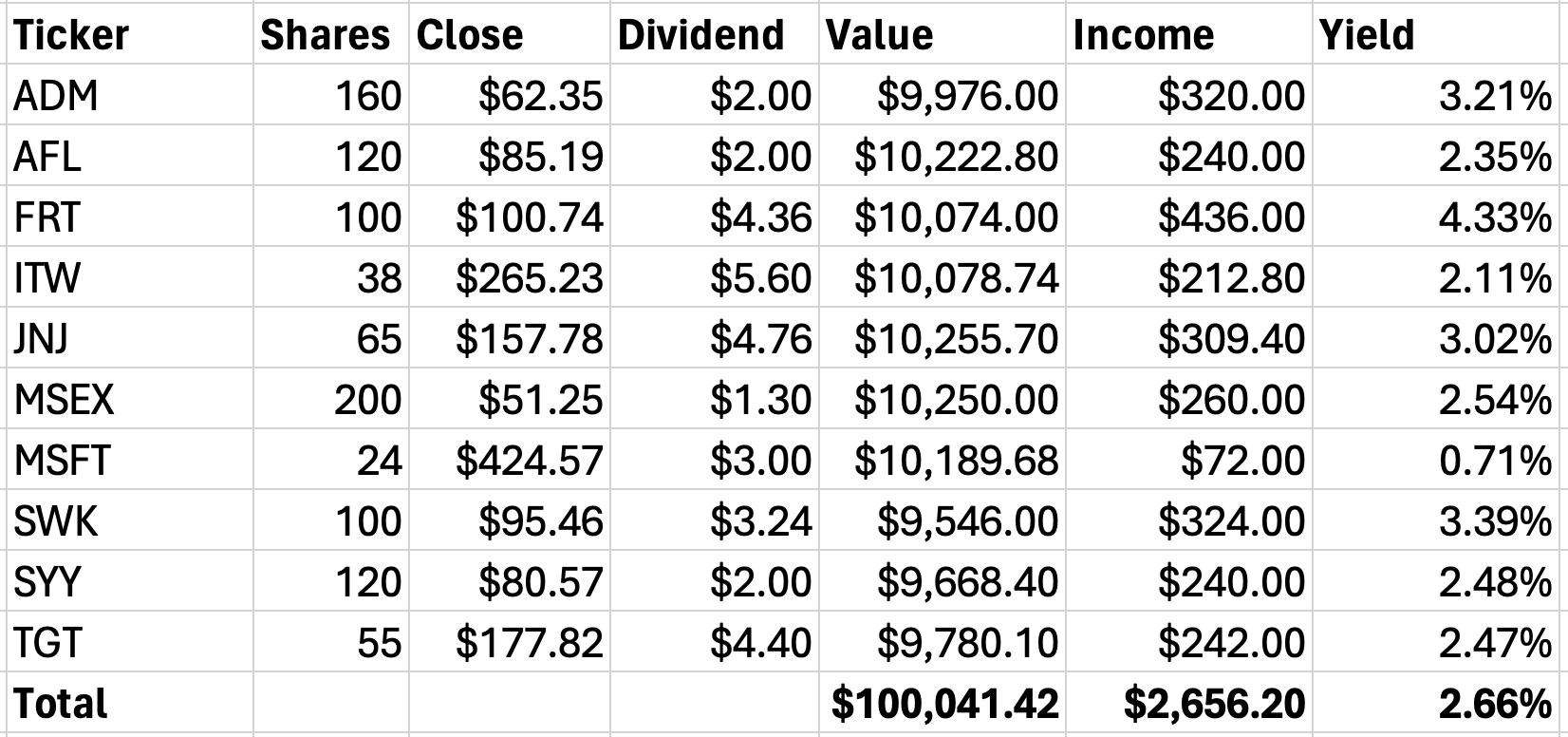

Let’s start with these ten blue chip stocks. Most have long histories of increasing their dividends, and several of them also have above-market dividend yields.

AFLAC (AFL)

Archer-Daniels-Midland (ADM)

Federal Realty (FRT)

Illinois Tool Works (ITW)

Johnson & Johnson (JNJ)

Microsoft (MSFT)

Middlesex Water (MSEX)

Stanley Black & Decker (SWK)

Sysco (SYY)

Target (TGT)The only exception is Microsoft. I added the tech giant for diversification even though it pays a small dividend.

The point I want to stress is that building a portfolio isn’t simply selecting names you like. I selected these ten because they make for a well-rounded portfolio. A portfolio is a cohesive whole. It all needs to work together. It’s like a baseball lineup. For example, we have retail, consumer, industrials, financials, utilities and REITs. Some will do well when others are lagging.

Also, bear in mind that this is a portfolio designed to produce income. It’s not going to be a fast grower. Go to crypto if you want excitement. This portfolio won’t be exciting, but it should hold up well in rapid bull markets.

My goal with this portfolio is to show you the key concepts in designing a portfolio with a specific goal in mind.

A good portfolio can be well diversified with as few as eight stocks, and it can be poorly diversified with 100 stocks.

Here’s a sample portfolio with our ten names:

I’ve listed each stock’s ticker symbol, total number of shares, Monday’s closing price, dividend per share, the value of each position, projected dividend income and the yield.

I used $100,000 as a sample, but feel free to multiply or divide these positions to satisfy your portfolio needs.

As you can see, this portfolio yields a healthy 2.66% per year, plus these are safe and secure stocks.

Next, I want to show you the power of dividend income. What if we had bought those ten stocks 20 years ago? Here’s how much you would be yielding on those stocks today if you had bought them in April 2004:

It’s odd to think that you would be yielding close to 10% with JNJ, but that’s what it would be based on a 20-year-old original purchase price.

Sure, 20 years is a long holding period, but the important point is that with investing, time is on your side.

Consider this thought exercise. Let’s say there’s a stock that currently yields 0.5%. Many income investors would quickly overlook it.

Let’s also say that this company grows its earnings and dividend consistently by 15% each year. If the valuation stays the same, then the dividend yield is always 0.5, but that’s masking how strong those dividends have been. In reality, the dividend income has strongly aided your returns. That’s why Einstein called compound interest, “the Eighth Wonder of the World.”

ISM Manufacturing Increases to 50.3

I should caution you that the stock market has looked a little weaker in recent days. There’s nothing to be alarmed about. After all, the market has had a strong run over the last five months, so some weariness is to be expected.

The S&P 500 was weak on Monday, and it was down over 1.1% today before it wandered higher this afternoon. So far, the bulls have been able to repulse any bear attacks, but I wonder how much longer that can last.

Tech stocks were especially weak today. The Nasdaq Composite lost nearly 1%. Tesla, which was already the worst-performing stock in the S&P 500 during Q1, lost another 5% today.

Oil rallied to $85 per barrel while the yield on the 10-year Treasury got up to 4.36%. That’s the highest this year.

I wanted to mention yesterday’s impressive ISM Manufacturing for March. The reading increased from 47.8 to 50.3. This is important because any number above 50 means that the factory sector of the economy is expanding. The ISM had been contracting for 16 consecutive months.

I also like to look at the ISM because it’s out fairly quickly. Most economic stats take a while to compute, but the ISM report is usually out on the first working day of each month.

Tuesday’s report on job openings said that openings are largely unchanged at 8.8 million. That report was for February. Over the last year, job openings are down by 11%. Also on Tuesday, the Census Bureau said that construction spending fell by 0.3% in February. Private spending was unchanged, but public spending fell.

The next big test for the market comes this Friday with the March jobs report. Wall Street thinks the U.S. economy created 200,000 new jobs last month. I’ll be curious what the wage numbers are. The consensus on Wall Street is that average hourly earnings increased by 0.3% last month.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

-

Morning News: April 2, 2024

Posted by Eddy Elfenbein on April 2nd, 2024 at 7:03 amRussia’s Seaborne Crude Exports Surge to the Highest This Year

Oil Hits $85 for First Time Since October as Market Tightens

Shell Says Support for the Energy Shift Will Wane If Prices Soar

The $40 Billion Fund That’s Gambling With Europe’s Climate Goal

Poor Nations Are Writing a New Handbook for Getting Rich

Australia’s Central Bank Says Risks Around Economy a Little More Balanced

South Korea’s Inflation Tops 3% for Second Straight Month

Bond Comments by China’s Xi Hint at Possible Expansion of PBOC Toolkit

Is China’s Economy Finally Bottoming Out?

A Million Simulations, One Verdict for US Economy: Debt Danger Ahead

A Higher-for-Longer Good Friday From the Fed

Markets Are Back to Seeing Fewer Rate Cuts Than the Fed

UBS to Launch Buyback of Up to $2 Billion

Trump-and-Dump: Speculators Bet on Truth Social ‘Meme’ Stock

Apple Flirts With Support Levels After Worst Quarter in a Decade

Regulators Force Another Microsoft Split

Legal Battle Kicks Off to Minimize Baltimore Bridge Liabilities

Americans Are Buying Cheaper Cars

Xiaomi’s Unproven EV Is Proving a Hit With Investors

Tesla Cyberbeast Heads to Auction in First Test of Resale Value

China Developers’ Shares Suspended in Hong Kong for Missing Results Deadline

How One Tech Skeptic Decided A.I. Might Benefit the Middle Class

GE Completes Three-Way Split to Start Trading As Separate Companies

Verve Tumbles After Pausing Gene-Editing Trial on Safety Issues

You Can Bet on Caitlin Clark Making Threes. The N.C.A.A. Isn’t Happy

The Battle Lines in the War Over Disney’s Board

Be sure to follow me on Twitter.

-

Morning News: April 1, 2024

Posted by Eddy Elfenbein on April 1st, 2024 at 7:06 amWhat 10 Years of Modi Rule Has Meant for India’s Economy

South Korean Export Growth Continued in March

China Industrial Upswing Is Latest Sign of Economic Recovery

Bank of Japan Tankan Survey Shows Mixed Results Amid Rate-Hike Speculation

Fertility Startups in Japan Step In as Treatment Demand Soars

Japan’s Top Utility Pilots Ammonia Use to Reduce Coal Emissions

US Oil Suppliers Muscling Into OPEC+ Markets All Over the World

Gold Jumps to Record as Favored Fed Inflation Gauge Stokes Rally

Relentless US Credit Demand Seen Driving Second-Quarter Rally

The Dollar Is More Armored Division Than Currency

Texas Federal Judge Blocks Updated Fair Lending Rules

Biden’s Economic Plan for Latin America Begins to Take Shape

Young Voters Are More Concerned With the Economy. That’s Bad for Biden

39,000 Lost Jobs Undercut Biden’s Manufacturing Wins

Bridgewater CEO’s Turnaround Hinges on Wooing Restless Clients

Capital One-Discover Merger Deal Termination Fee Set at $1.38 Billion

Rakuten Group Aims to Integrate Bank, Fintech Units

Chip & Joanna Gaines Vivify the Dangers of Antitrust

Baltimore Ship Accident Has East Coast Ports Scrambling to Absorb Cargo

Ships Have Become Supersized Since Baltimore Bridge Was Built

Tesla Has Wall Street Worried About How Many Cars It Just Sold

Auto Execs Call for New Measures as E.V. Wars Heat Up

French New Car Sales Decline 1.5% in March, PFA Association Says

You Don’t Need to Freak Out About Boeing Planes (but Boeing Sure Does)

Chile Telecom Operator WOM Files for Bankruptcy in the US

This Disney War Has Already Paid Off

A Look at Hasbro’s ‘Monopoly’ To Calm the Nerves of Monetarists

As Graffiti Moves From Eyesore to Amenity, Landlords Try to Cash In

How Street Art Is Gentrifying Neighborhoods

Be sure to follow me on Twitter.

-

Morning News: March 29, 2024

Posted by Eddy Elfenbein on March 29th, 2024 at 7:03 amGreece to Increase Minimum Wage by €50 a Month from April 1

Japan FX Chief Calls Yen’s Slump Unusual, Vows to Act if Needed

Korean Banks Say to Compensate Investors for China-Linked Notes

Stock Market Surges to Start the Year: 22 Record Highs in 3 Months

Bankman-Fried Is Sentenced to 25 Years in Prison Over FTX Collapse

Sam Bankman-Fried’s Sentence Is a Warning to Crypto

Robinhood’s Credit Card Offers 3% Cash Back. Can It Last?

Those Billion-Dollar Lottery ‘Jackpots’ Aren’t Even Half That Big

Giant Merger Deals Stage a Comeback

Huawei Stages Comeback With Annual Net Profit More Than Doubling

Apple Plans New iPad Pro for May as Production Ramps Up Overseas

How the Israel-Hamas War Has Roiled TikTok Internally

San Francisco’s ‘Twitter Menace’ or True Believer? He Might Be Both

Syngenta Pulls China IPO Application After Three-Year Wait

Viavi Says Its Spirent Bid Has Certain Value Amid Bidding War

US Approves $60 Million in Urgent Funds for Baltimore Bridge

Auto Industry Expects Minimal Disruption From Port Shutdown

Plans for World’s Fastest Train Service Delayed as Japan Ditches 2027 Target

Xiaomi Prices First EV Competitively, Seeks Pole Position in Crowded Market

Tesla’s Terrible Quarter Catches Some Analysts Asleep at the Wheel

Tesla Dives Into Advertising After Years of Resistance

Renault to Build Electric Vans at Plant in Northern France

Young Indians More Likely to Be Jobless If They’re Educated

Harvard Applications Drop 5% After Tumultuous Year on Campus

Building Diversity When Affirmative Action Is Banned

Can Reed Hastings Disrupt Skiing?

Be sure to follow me on Twitter.

-

Morning News: March 28, 2024

Posted by Eddy Elfenbein on March 28th, 2024 at 7:06 amChina Property Crisis Is Rippling Through Its Biggest Banks

Russia Sends Cuba First Oil in a Year to Ease Blackouts and Unrest

Dalio Says China Must Fix Debt Problems or Face ‘Lost Decade’

As Relations Thaw, China Lifts Tariffs on Australian Wine

BOJ Summary Hints at Cautious Approach to Further Rate Increases

UK Confirmed in Recession at End of 2023

Fed Hawks Put the Dollar on Track for Best Quarter Since 2022

Fed’s Waller Says No Rush to Cut Interest Rates

Biden Is Breaking Campaign Rule No. 1. And It Just Might Work

Ad Forecaster Raises 2024 Prediction Amid Improving Economic Outlook

UBS Makes Ermotti Europe’s Best-Paid Bank Boss with $16 Million Package

UBS Banker’s Frustration Exposes Cracks in World of Climate Finance

SBF Prison Time Hangs on Persuading Judge He Is No Bernie Madoff

Harvey Schwartz Spends First Year at Carlyle Tending Old Wounds

The Dali Is a Big Ship. But Not the Biggest

Baltimore Bridge May Trigger Historic Marine Loss, Says Lloyd’s of London

4 Takeaways About Boeing’s Quality Problems

‘Shortcuts Everywhere’: How Boeing Favored Speed Over Quality

EVs Are Splitting the Auto World Into Two: Made in China, or Not

Tesla’s $25,000 Car Means Tossing Out the 100-Year-Old Assembly Line

Mercedes Is Liable for Emissions Cheating Device, Court Rules

Can a Legally Binding Treaty Fix the World’s Plastic Problem?

Alibaba’s Plan to Split Is Being Replaced by Greater Focus on Its Core

Home Depot Buys Roofing Distributor in Deal Valued at $18 Billion Including Debt

The Cautionary Tale of Wirecutter and the Internet’s Favorite Wok

‘Winners and Losers’ as $20 Fast-Food Wage Nears in California

Walgreens Suffers $6 Billion Loss As VillageMD Clinic Investment Sours

Big Tobacco Is Now Under the Zynfluence

Be sure to follow me on Twitter.

-

Morning News: March 27, 2024

Posted by Eddy Elfenbein on March 27th, 2024 at 6:57 amAmerican Business Stalls in China

Xi Says US CEOs Should Invest in China, Economy Hasn’t Peaked

Japan Steps Closer to Intervention as Yen Hits Lowest Since 1990

The Real Bridge Too Far Is Financing

Rising Minimum Wage Risks Stoking Inflation, Says CBI Chief

In a Passive World, These Stockpickers Are Thriving

Nvidia Catapults EM Stock Picker to Top Ranking and Irks Rivals

UBS Sells $8 Billion of Credit Suisse Assets to Apollo

Visa and Mastercard Agree to Cap Their Swipe Fees in Settlement

In US Antitrust War, Bet on Brandeis Not Bork

Using Your Premium Credit Card May Cost More After Visa-Mastercard Deal

Robinhood Ventures Further Beyond Trading with New Credit Card

Why BlackRock’s C.E.O. Wants to Rethink Retirement

Gates-Backed Startup Hits Milestone, Races Ahead on Green Steel

The U.S. Investors Caught in the Scrum Over TikTok

The U.S.’s Forced Sale of TikTok Is the Stuff of Third World Nations

Tesla’s Hunt for Self-Driving Revenue

A Pivot to China Saved Elon Musk. It Also Binds Him to Beijing

Chinese Train Maker CRRC Drops Bid for $665 Million Bulgarian Contract

Gamestop Set to Fall Most in Nine Months After Revenue Plunges

Nestle to Spend $132 Million to Improve Supplier Sustainability in East and Southern Africa

How Michael Rubin Ended Up Holding All the Cards

H&M Outlook on Track as Sales Pick Up

NBC Drops Former RNC Chief Ronna McDaniel Amid Backlash

Trump’s Media Company Ticker Leads to Fleeting Windfall

Be sure to follow me on Twitter.

-

CWS Market Review – March 26, 2024

Posted by Eddy Elfenbein on March 26th, 2024 at 6:34 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

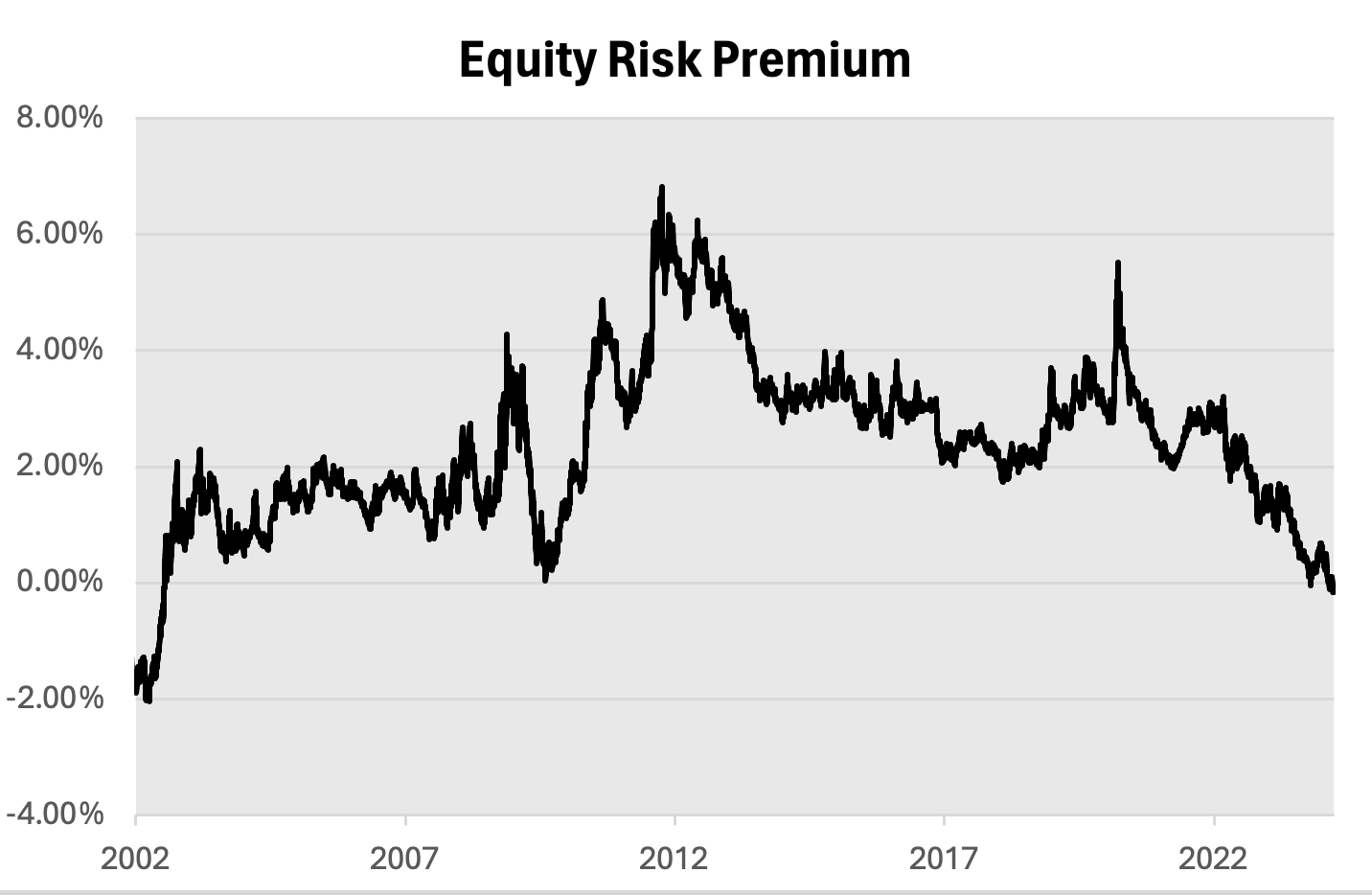

The Equity Risk Premium Goes to Zero

The stock market did something recently it hasn’t done in over 20 years. The yield on the 10-year Treasury exceeded the earnings yield for the S&P 500.

What am I talking about? Let’s dive in.

By earnings yield, I mean the S&P 500’s earnings divided by its price. That’s the inverse of the market’s price/earnings ratio.

To be more technical, the equity risk premium has gone to zero. Typically, one would expect a benefit from owning stocks. According to the theory, this is the reward shareholders get for shouldering more risk. Sometime the benefit is a lot, sometimes it’s a little. Right now, it doesn’t exist.

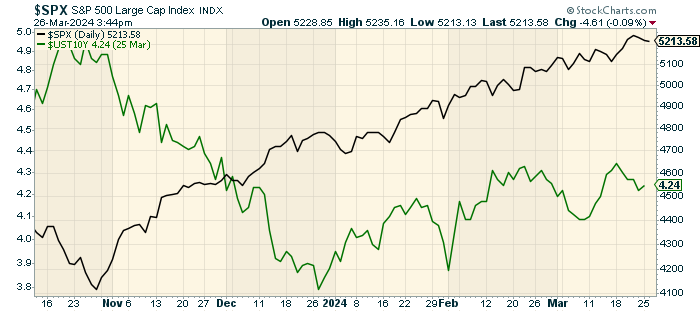

Here’s a look at the yield on the 10-year Treasury (in black) along with the S&P 500’s earnings yield (in purple).

Here’s how it works, or at least how it’s supposed to work (my apologies for getting mathy).

Take the 10-year Treasury yield. Right now, that’s around 4.25%. Add 2% to that for the risk premium (so 6.25%). Then take the inverse of that (1/0.0625 = 16) and that should roughly be the stock market’s price/earnings ratio. In this case, that’s 16.

Except, right now, it’s not even close. The stock market’s current price/earnings ratio is currently at 24. That’s roughly 50% higher than where the model thinks it should be.

As of Friday, the 10-year Treasury yield was 4.27% while the earnings yield of the S&P 500 was 4.10%. That means that investors are being punished by 17 basis points for owning stocks. This is also why we pay so much attention to what the Fed has to say about interest rates.

Let me add some very cautious words about this kind of analysis. I’m not a fan of trying to model the stock market. Many have tried but the market gods have left many a ruined spreadsheet in their wake. To quote Isaac Newton, “I can calculate the motion of heavenly bodies, but not the madness of people.”

The model isn’t saying that stocks are overpriced. Rather, it’s saying that stocks are richly valued relative to bonds compared with previous periods. That’s quite a different takeaway.

Here’s a look at the Equity Risk Premium which is how much stock investors are being paid to buy stocks instead of bonds.

Still, even bad models can make a point. This one is telling us a very basic fact that we can’t ignore. That is that stock prices have gone up a lot over the past five months. Meanwhile, bond prices have been creeping lower.

At some point, bonds are a better deal than stocks. I don’t know where that line is, but I do know two things: it’s out there somewhere, and we’re much closer to it than we’ve been in quite some time.

This isn’t to scare you. I have no plans to sell all my stocks, but it’s responsible to ensure that investors are aware of the current climate.

Interestingly, stocks reached their most recent low point in late October right as the 10-year Treasury peaked near 5%. (It came very close to breaking above 5% but couldn’t quite do it.)

Since then, stocks have rallied, and the 10-year Treasury yield fell, but that came to an end just before New Year’s. We went from Stocks-Up, Bonds-Up to Stocks-Up, Bonds-Down. The first one can last a long time, but the second one is a lot less stable. Last week, the 10-year yield got above 4.3%.

While I don’t plan on selling anything, I certainly can understand the mindset of some investors who look at the current prices and realize that they can sit out the volatility of the stock market and lock-in, say, a one-year Treasury for 5%. That’s the equivalent of 2,000 Dow points. For zero risk!

It’s not for me, but I get why some people are happy to take it. This shows us how distorting higher interest rates can be. This also tells me that sometime soon, the Fed will cut rates not because it wants to, but because it has too.

The odds of a rate cut in June are at 70%, and that rises to 84% for a cut by July. The odds for two cuts by July are low (now around 30%). It may soon be that we’ll get one cut, in June or July, but which month isn’t yet clear.

The Reddit Rally

Last week, I told you about the weakness in many defensive sectors. That’s exactly the outcome of diverging stock and bond markets. Last week, I mentioned how one of our favorite defensive stocks, Hershey (HSY), has been acting poorly of late. This is exactly the kind of stock that leads the market when the economy gets soft.

I mentioned that the chocolate giant has been squeezed by higher cocoa prices. Due to heavy rains in west Africa, there’s been a massive shortage of cocoa. That’s where 70% of the world’s cocoa comes from. So far, Hershey has been able to pass along some of these price increases.

Cocoa is outperforming Nvidia this year. Earlier today, BNP Paribas Exane downgraded Hershey from outperform to neutral.

The cocoa rally, however, has gone into overdrive, and Easter is one of the biggest times of the year for chocolate consumption. For the first time ever, cocoa is trading north of $10,000 per metric ton. Hershey says it predicts flat earnings this year. At some point soon, I expect cocoa prices to plunge back to earth.

But this is a different outcome from the same driver. Investors are ignoring risk. Cocoa isn’t the only place we’re seeing surging prices. Last week, Reddit (RDDT) went public, and the stock has performed very well.

I wanted to show you just how extreme some of the valuations are. Let’s take a closer look at Reddit’s business.

Last year, Reddit had revenue of $804 million and operating income of negative $140 million. In other words, the company is running at an operating loss. Add in $50 million in other income and Reddit lost about $90 million for the year. That works out to minus 57 cents per share.

Despite running a loss, shares of Reddit were priced at $34. Once trading started, the shares took off. Earlier today, the stock came close to $75 per share. That means the business is trading for more than 130 times its loss from the year.

I understand that one shouldn’t value nontraditional companies with traditional metrics. Still, at some point, one has to view this as extreme. This is exactly what happens when the equity risk premium goes to zero. When being risky pays off, the market will follow what’s working.

Reddit is worth $75 per share in the same way cocoa is worth $10,000 per metric ton, or the S&P 500 is worth 24 times earnings. “The voice of reason is small, but very persistent.” — Sigmund Freud.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

-

Morning News: March 26, 2024

Posted by Eddy Elfenbein on March 26th, 2024 at 6:57 amRussia’s Crude Shipments Rebound Even as Sanctions Snare Tankers

US CEOs Extend China Stay on Last-Minute Invite to Meet Xi

China’s Battery Champion Says Geopolitical Tensions Won’t Derail U.S. Expansion

German Consumer Confidence Improves Marginally, Defying Fragile Economy

Savings May Not be Europe’s Super Weapon in Economic Battle

Closing Australia’s Gender Pay Gap Will Take a Rethink of Senior Roles, Agency Says

How a New Rule Could Change the Way Advisers Handle Your Retirement Money

BOE’s Mann Says Markets Pricing Too Many UK Rate Cuts This Year

Wall Street’s Most Bullish Strategist Cites a ‘Big Surprise’ Pushing Stocks Higher

The Great Rates Descent Will Be Nasty, Brutish and Long

Chocoholics Won’t Be the Only Victims of Cocoa’s Surge

Raging Storms Pushed Disaster Damages Above $100 Billion in 2023

In France, the Future Is Arriving on a Barge

Fisker Deal Talks with Big Automaker Collapse, NYSE to Delist Stock

Elon Musk’s Starlink Terminals Are Falling Into the Wrong Hands

Amazon’s AI Awakening: Why AMZN Stock Is the Magnificent Seven’s Sleeping Giant

TikTok Can’t Get Enough Boeing Jokes. Guess Who’s Not Laughing

Biggest Challenge Facing New Boeing CEO Is Winning Over Airlines

Adam Neumann and Partners Offer More Than $500 Million for WeWork

This AI Startup is Trying to Make Fax Machines Work Better for Health Care

Bertelsmann Posts Higher Profit, Adjusts 2026 Targets

Flutter Entertainment Pretax Loss Widens Despite Strong Growth in U.S.

Lofty Valuation Carries Trump’s Social Media Company Into First Trading Day

McDonald’s to Sell Krispy Kreme Doughnuts Across the US

Chick-fil-A Modifies Its ‘No Antibiotic’ Chicken Policy

Be sure to follow me on Twitter.

-

Morning News: March 25, 2024

Posted by Eddy Elfenbein on March 25th, 2024 at 6:59 amBurned Before, Bond Markets Resume Rate-Cutting Trades Worldwide

Egypt’s $50 Billion Rescue Betrays Depth of Its Economic Crisis

Asia Private Equity Deals Set for Worst Q1 Since 2015, Data Shows

Yuan Rebounds as PBOC Sends Strong Message of Support Via Fixing

Once High-Flying Bankers in Hong Kong Become a Lost Generation

Japan’s Currency Chief Warns Against Speculative Moves in Market

Russian Brokers Launch Frozen Asset Swap Scheme

Stocks on Inflation Stand-By as Intervention Watch Dogs Yen

Goldman Sachs Digital Asset Head Says Crypto Rally Driven by Retail Investors

In a Bumper Year for CEO Pay, a $161 Million Award Swells to $1.3 Billion

There’s No Such Thing As ‘Easy Money,’ There’s Just Production

Famously Obstinate, Bill Ackman Is Now Real-Life Famous. What Next?

US Announces $6 Billion to Clean Up Heavy Manufacturing

Apple, Google, Meta Probed by EU in Test of New Digital Law

Reddit to the Moon Won’t Launch an IPO Boom

Big Tech’s Latest Obsession Is Finding Enough Energy

Germany’s Solar Panel Industry, Once a Leader, Is Getting Squeezed

Nissan Motor Plans to Sell More Than a Dozen New EV Models by 2026

CATL Working With Tesla on Fast-Charging Cells, Supplying Nevada

PetroChina Profits Surge to Record on Rebound in Gas Demand

Has China Lost Its Taste for the iPhone?

Gucci’s China Shock Reverberates Across the Luxury Landscape

Big Hotel Chains and Unbranded-Hotel Owners Find They Need Each Other

US Homebuyers Expecting $10,000 Savings Face Tough Reality

Kingfisher Remains Cautious With Lower Profit, Weak Demand Outlook

Be sure to follow me on Twitter.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His