Archive for September, 2007

-

West Side Story at 50

Eddy Elfenbein, September 28th, 2007 at 7:36 pmWest Side Story opened 50 years ago this week.

-

Bed Bath & Beyond’s Earnings

Eddy Elfenbein, September 28th, 2007 at 12:55 pmI didn’t have a chance to write about this before but Bed Bath & Beyond (BBBY) earned 55 cents a share for its fiscal second quarter.

Here are the earnings results going back a few years:Quarter Sales Gross Profit Operating Profit Net Profit EPS $356,633 $146,214 $28,015 $17,883 $0.06 $451,715 $185,570 $53,580 $33,247 $0.12 $480,145 $196,784 $50,607 $31,707 $0.11 $569,012 $238,233 $77,138 $48,392 $0.17 $459,163 $187,293 $36,339 $23,364 $0.08 $589,381 $241,284 $70,009 $43,578 $0.15 $602,004 $246,080 $64,592 $40,665 $0.14 $746,107 $311,802 $101,898 $64,315 $0.22 $575,833 $234,959 $45,602 $30,007 $0.10 $713,636 $291,342 $84,672 $53,954 $0.18 $759,438 $311,030 $83,749 $52,964 $0.18 $879,055 $370,235 $132,077 $82,674 $0.28 $776,798 $318,362 $72,701 $46,299 $0.15 $903,044 $370,335 $119,687 $75,459 $0.25 $936,030 $386,224 $119,228 $75,112 $0.25 $1,049,292 $443,626 $168,441 $105,309 $0.35 $893,868 $367,180 $90,450 $57,508 $0.19 $1,111,445 $459,145 $155,867 $97,208 $0.32 $1,174,740 $486,987 $161,459 $100,506 $0.33 $1,297,928 $563,352 $231,567 $144,248 $0.47 $1,100,917 $456,774 $128,707 $82,049 $0.27 $1,273,960 $530,829 $189,108 $120,008 $0.39 $1,305,155 $548,152 $190,978 $121,927 $0.40 $1,467,646 $650,546 $283,621 $180,980 $0.59 $1,244,421 $520,781 $150,884 $98,903 $0.33 $1,431,182 $601,784 $217,877 $141,402 $0.47 $1,448,680 $615,363 $205,493 $134,620 $0.45 $1,685,279 $747,820 $304,917 $197,922 $0.67 $1,395,963 $590,098 $148,750 $100,431 $0.35 $1,607,239 $678,249 $219,622 $145,535 $0.51 $1,619,240 $704,073 $211,134 $142,436 $0.50 $1,994,987 $862,982 $309,895 $205,842 $0.72 $1,553,293 $646,109 $154,391 $104,647 $0.38 $1,767,716 $732,158 $211,037 $147,008 $0.55 -

Stocks and Bonds Unite

Eddy Elfenbein, September 28th, 2007 at 10:29 amHere’s an unusual recent development.

From July 3 to September 19, the stock and bond markets moved in opposite directions 80% of the time (I’m using the SPX & TLT).

But in the six trading days since, they’ve moved in different directions just once.

Obviously, it’s too early to read any major significance into this, but it’s something worth watching. There’s also the question of what the consequences are.

If the stock and bond markets are indeed, converging, I’m inclined to think it’s a healthy sign for both markets. -

Paul Kedrosky on Wall Strip

Eddy Elfenbein, September 28th, 2007 at 9:23 amPaul Kedrosky runs Infectious Greed, one of my favorite blogs. Here he is on Wall Strip.

-

How to Make a lot of Money in Five Easy Steps

Eddy Elfenbein, September 27th, 2007 at 7:04 amStep #1: Sell everything you own. Sell it all. Stocks, bonds, real estate. eBay your couch, you dog. Everything.

Step #2: Then convert it all into pre-1982 copper pennies.

Step #3: Meltdown the pennies.

Step #4: Sell the copper.

Step #5: Now use your proceeds to buy back all the stuff you sold. You’ll have more than enough left over.

The material in a pre-1982 penny is currently worth about 2-1/2 cents.

Update: It’s not exactly legal. -

Integrity Boosts Returns

Eddy Elfenbein, September 26th, 2007 at 10:28 amHmmm.

People know that integrity will help them in the business world. It can also boost their investment results. That’s the finding of a recent survey of advisers at Ameriprise Financial Services. The study sought to find out the impact of various adviser traits on their investment results.

It studied 12 emotional and moral competencies, such as client service and self-confidence.

The results showed that the adviser’s level of integrity played the biggest part in posting strong investment returns.

“Most people we deal with are high performers,” said Rick Aberman, a founding partner of consulting firm Lennick Aberman Group, which like Ameriprise is based in Minneapolis and assisted with the survey. “We wanted to look at what differentiated those who are successful from those who are really successful.”

Ameriprise paid for the study. It sought to find out whether emotional competency and integrity led to better performance, says Kris Petersen, the firm’s general manager of financial planning and advice.

“I assumed the results would be better (for those who had more integrity), but not by as much as it was,” she said.

Integrity showed up in advisers’ ability to act the way they believe and to do what they say they will, Aberman says.During my career, I’ve worked for three different brokerage firms and there I met some of the most dishonest people I’ve ever met in my life.

-

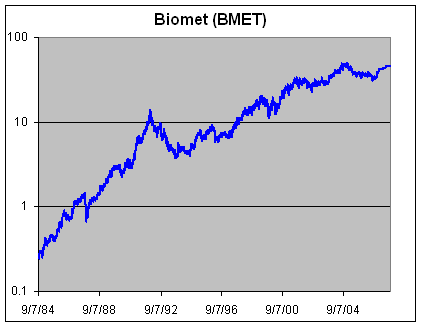

Biomet Trades No More

Eddy Elfenbein, September 26th, 2007 at 9:58 amBiomet was taken off the market yesterday for $46 a share. Here’s a look at the stock’s amazing run. In 23 years, the stock went up by more than 200-fold.

I have to do a little housekeeping for my Buy List. This will be a dull post, but since we now know how important integrity is to our returns, I want to be as thorough as possible.

I’ll go over the rules again. At the start of each year, I pick 20 stocks for the Buy List. I’m not allowed to make any changes during the entire year. I assume a portfolio of $1 million, with $50,000 invested in each position.

For track record purposes, I’m going to take the Biomet proceeds and invest them equally in the 19 other stocks. I thought about keeping the proceeds in cash until the end of the year, but that doesn’t seem right.

At the start of the year, the Buy List had 1211.5338 shares of Biomet at $41.27. With the $46 buy-out price, that gives us a total of $55,730.5548. Divided 19 ways, that means we invest $2,933.1871 in each stock.

Here’s how I calculated the new number of shares:

Stock……..9/25 Close……..New Shares…….Starting Shares……..New Total

AFL………….$55.94………….52.4345………….1086.9565………….1139.3910

APH…………$39.22………….74.7880………….1610.8248………….1685.6128

BBBY………..$33.20………….88.3490………….1312.3360………….1400.6850

DCI………….$41.52………….70.6452………….1440.5071………….1511.1523

DHR…………$83.82………….34.9939……………690.2264…………..725.2203

FDS………….$66.10………….44.3750……………885.2691…………..929.6441

FIC…………..$36.11………….81.2292………….1230.0123………….1311.2415

FISV………….$50.46………….58.1290…………..953.8344………….1011.9634

GGG………….$38.10………….76.9865…………1261.9889………….1338.9754

HOG………….$46.51………….63.0657………….709.5218……………772.5875

JOSB………….$35.08………….83.6142………..1703.5775………….1787.1917

MDT…………..$56.26………….52.1363………….934.4048……………986.5411

NICK………….$8.93………….328.4644…………4237.2881………….4565.7525

RESP………….$48.74…………60.1803………….1324.5033………….1384.6836

SEIC………….$25.92………..113.1631………….1678.9792………….1792.1423

SYY…………..$34.70………….84.5299………….1360.1741………….1444.7040

UNH………….$49.48………….59.2803…………..930.5788……………989.8591

VAR…………..$39.09………….75.0368………….1051.0826………….1126.1194

BER…………..$28.99…………101.1793…………1448.8554………….1550.0347 -

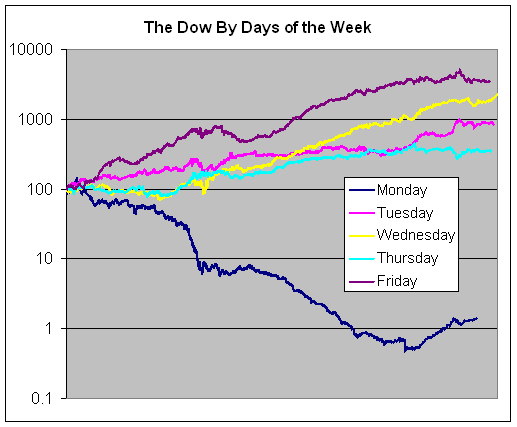

The Dow By Each Day of the Week

Eddy Elfenbein, September 26th, 2007 at 9:31 amHere’s how the Dow Industrials have performed by each day of the week going back to 1896.

Note that the lines aren’t exactly lined up because there aren’t the same number of trading days for each day.

Yuck, that Monday line is horrible. In fact, the Dow is down 58% for Monday, Tuesday and Thursday combined. So much Efficient Market Theory! To be fair, Monday has recovered a lot since 1987.

The big winner is Friday, but Wednesday has slowly closed the gap over the past few decades. And as I’ve written before, Wednesday has been the big winner of the past few years. In fact, all of the market’s gain has come on Wednesday.

Here are the average returns for each day:

Monday…………..-0.0784%

Tuesday…………..0.0379%

Wednesday………0.0550%

Thursday………….0.0220%

Friday………………0.0634%

Here are the standard deviations:

Monday…………..1.3849%

Tuesday…………..1.0616%

Wednesday………1.1106%

Thursday………….1.0350%

Friday………………1.0536% -

Wall Strip on United Industrial

Eddy Elfenbein, September 26th, 2007 at 9:07 am -

Smithtown Bancorp (SMTB)

Eddy Elfenbein, September 25th, 2007 at 3:04 pmHere’s a small one. Check out these numbers for Smithtown Bancorp (SMTB).

Date EPS

1997 0.29

1998 0.31

1999 0.4

2000 0.47

2001 0.59

2002 0.79

2003 0.92

2004 1.02

2005 1.13

2006 1.43

The bank earned 73 cents a share for the first six months of this year.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His