CWS Market Review – February 1, 2019

“Financially, I just say: Keep it simple.” – Rob Gronkowski

When I put together each week’s CWS Market Review, sometimes there’s little news to cover, and sometimes there’s a lot. This week, it’s the latter. We had seven Buy List earnings reports, plus nine more to preview for next week. On Wednesday, Stryker soared 11.4% to a new all-time high. We also saw new highs from stocks like Danaher, AFLAC and Fiserv. In fact, AFLAC just raised its dividend for the 36th year in a row.

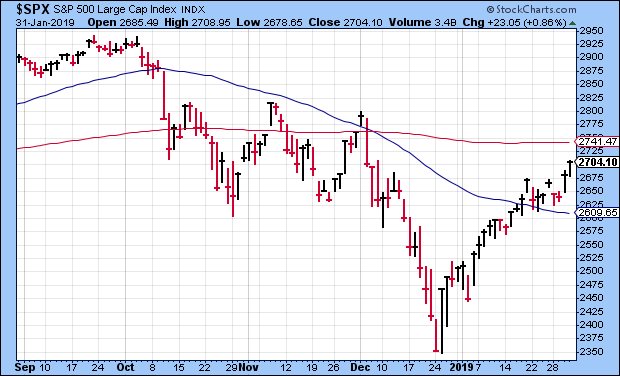

The S&P 500 finished January at its highest close in two months. The stock market had its best January in 32 years. (That’s right, 1987 got off to a great start.)

If that’s not enough, we have a jobs report later today, plus we had an important Fed meeting earlier this week. The good news is that the Fed finally appears to “get it” about the economy. After Wednesday’s policy statement came out, the stock market rallied, and the Dow broke 25,000.

There’s a lot of earnings news to get to, but first I want to talk about why the market loved what the Fed had to say.

The Federal Reserve Finally Gets It

The Federal Reserve met this week on Tuesday and Wednesday. The central bank didn’t raise rates, and no one was expecting it to, but Fed watchers were busy looking for any clue as to what the Fed’s thinking. (They used to look at the size of Alan Greenspan’s briefcase. I wish I were making this up.)

This week, they got their clue, and the Fed wasn’t exactly hiding the message. I’ll skip all the econo-babble and jump to the key sentence in the Fed’s policy statement. Here goes: “In light of global economic and financial developments and muted inflation pressures, the Committee will be patient as it determines what future adjustments to the target range for the federal-funds rate may be appropriate to support these outcomes.”

Those five words in bold are a big honking deal. Allow me to translate into plain English. The Fed’s saying, “dude, we get it. We’ll chill it on the rate hikes.” They had to. The Fed had gotten way ahead of the economy, and I think they came close to doing real damage. Remember in October when all those building stocks had a panic attack? Fortunately, mortgage rates are down a good deal since November.

Last week, I mentioned the futures market. This is where traders can bet on what the Fed will do. They were saying the Fed won’t touch rates at all this year. I think that may be right. There’s even a growing minority that thinks the next move will be a rate cut.

Inflation has been well-behaved. The dollar is doing well, and the stock market is recovering nicely. Since January 3, the S&P 500 is up over 10%. As soon as the Fed’s statement came out on Wednesday afternoon, the market started to rally, and the buying carried over into Thursday.

Some folks think we’re at the top of the cycle. I’m not so sure. The Fed may raise rates sometime down the road. For now, this is a great time to be in the market. Rates are steady, earnings are rising and many stocks are still well below their highs. With that said, let’s take a look at our busy week of Buy List earnings.

Earnings Beats from Danaher, Stryker and Check Point

On Tuesday morning, Danaher (DHR) reported Q4 earnings of $1.28 per share. That beat the Street by a penny. Honestly, I had been expecting a little bit more, but this is still a very good result. The diversified manufacturer’s previous guidance had been for $1.25 to $1.28 per share, so they hit the top-end of their own range. For the full year, Danaher made $4.52 per share.

Thomas P. Joyce, Jr., President and Chief Executive Officer, stated, “We are very pleased with our fourth-quarter results, which wrapped up a tremendous 2018. During the year, we delivered strong revenue growth and operating-margin expansion, leading to double-digit adjusted earnings per share and free cash-flow growth.”

Danaher said the dental spin-off is on pace for the second half of this year. Now let’s look at guidance. For Q1, DHR expects $1 to $1.03 per share. Wall Street had expected $1.03 per share. For all of 2019, the company sees earnings between $4.75 and $4.85 per share. I said I expected them to say $4.75 to $4.80 per share.

Bottom line: Danaher is a very good company. The shares got to a new high on Thursday. This week, I’m lifting our Buy Below on Danaher to $114 per share.

Now for this week’s star pupil. After the bell on Tuesday, Stryker (SYK) reported Q4 earnings of $2.18 per share. That’s an increase of 11.2% over Q4 2017, and it was three cents better than expectations. Stryker had given us a range of $2.13 to $2.18 per share, and like Danaher, they hit the top end of that. For the quarter, net sales rose 9.4% to $3.8 billion. Organic sales were up 8.6%, and operating margins rose to 27.5%. For the year, Stryker made $7.31 per share. That’s an increase of 12.6% over the $6.49 per share they made last year.

“We had an excellent finish to 2018 with the best organic sales growth in a decade, and strong adjusted-earnings performance,” said Kevin A. Lobo, Chairman and Chief Executive Officer. “Our multi-year momentum reflects the strength of our diversified model, progress on globalization and outstanding people and culture. We are well positioned to deliver for our customers, employees and shareholders in 2019 and beyond.”

For Q1, Stryker says it expects earnings to range between $1.80 and $1.85. Wall Street was at $1.84, which I thought might be too high. For the year, Stryker sees earnings between $8 and $8.20 per share. Wall Street was expecting $8.01.

Stryker jumped 11.4% on Wednesday. We now have a 13.3% gain on the year. For now, I’m keeping my Buy Below at $181 per share.

On Wednesday, Check Point Software (CHKP) reported Q4 earnings of $1.68 per share. That’s an increase of 6%, and it beat Wall Street’s estimate by five cents per share. Revenue rose 4% to $526 million. During Q4, the cyber-security firm bought back 2.8 million shares for $305 million. Daniel Ives, an analyst at Wedbush Securities, summed it up well: “This was a rock-solid quarter as the company is firing on all cylinders with cyber-security spending accelerating into 2019.”

For the year, Check Point earned $5.71 per share. That’s an increase of 7% over 2017. Revenue fell 3% to $1.916 billion. Over the course of the year, the company bought back 10.3 million shares for $1.1 billion.

For 2019, Check Point sees revenues ranging between $1.94 and $2.04 billion and earnings between $5.85 and $6.25 per share. For Q1, Check Point sees revenues between $460 and $480 million and EPS between $1.28 and $1.34. This week, the stock touched an eight-week high. Check Point is a buy up to $120 per share.

Four Earnings Reports on Thursday

Thursday was an especially busy day for us with four Buy List earnings reports. Let’s start with Sherwin-Williams (SHW) because they warned us that this was not going to be a good report. Well, they were right. To be fair, the news isn’t as bad as it could have been.

While the company said that Q4 was weak, they also noted that it was mostly due to October and November, while the December numbers looked better. Sherwin said they were going to earn $18.53 per share for the year, and that’s what Thursday’s report confirmed. Quarterly earnings were for $3.54 per share.

Let’s look at guidance. For 2019, Sherwin sees net sales rising 4% to 7% and earnings coming in between $20.40 and $21.40 per share. That’s a pretty good forecast, and it tells me the issues they had in Q4 are over. SHW rallied 4% on Thursday. I’m lifting our Buy Below on Sherwin-Williams to $430 per share.

Also on Thursday, Raytheon (RTN) said they made $2.93 per share for their fourth quarter. Quarterly sales were up 8.5% to $7.4 billion.

In October, Raytheon raised its full-year guidance range from $9.77 to $9.97 per share to $10.10 to $10.11 per share. The final result was $10.15 per share. The company said the quarterly increase was “primarily driven by operational improvements and lower taxes primarily associated with tax reform.” The CEO noted that Raytheon ended the year with record bookings and backlog which positions them “well for 2019 and beyond.”

For 2019, Raytheon expects EPS of $11.40 to $11.60 on sales of $28.6 to $29.1 billion. That’s a little light; I had been expecting $11.50 to $12 per share. The shares pulled back 3.9% on Thursday. Still, business is going well. Despite the pullback, I’m raising my Buy Below on Raytheon to $169 per share.

Hershey‘s (HSY) Q4 wasn’t so sweet. Comparable-sales growth was flat. In North America, comparable sales fell 0.3%. Earnings came in at $1.26 per share, which was a penny below estimates. For the moment, the problem is pricing pressure. Quarterly sales rose 2.5% to $1.99 billion.

For 2019, Hershey sees earnings ranging between $5.63 and $5.74 per share. Wall Street had been expecting $5.65 per share. The stock initially dropped after the report but gradually rallied back and closed higher on Thursday by 0.5%.

Our final report this week came after the close on Thursday when AFLAC (AFL) said it made $1.02 per share for Q4. That was eight cents more than expectations. Interestingly, the exchange rate had no impact on earnings. For the year, the duck stock made $4.16 per share, of which four cents were due to the exchange rate.

AFLAC also raised its dividend by 3.8%. The quarterly payout is increasing from 26 to 27 cents per share. This is AFLAC’s 36th consecutive annual dividend increase. I love companies that consistently reward shareholders. (Remember the Gronk’s wisdom.)

For 2019, AFLAC is looking for earnings of $4.10 to $4.30 per share. That assumes the yen trades at ¥110.39 to the dollar. I’m raising the Buy Below on AFLAC to $50 per share.

Nine Buy List Earnings Reports Next Week

Now let’s look at next week’s slate of earnings. We’ll begin with five that are scheduled for Tuesday.

Cerner (CERN) had a tough year for us in 2018. For Q4, the healthcare-IT outfit expects revenues between $1.37 billion to $1.42 billion. The midpoint of that range is 6% growth. For Q4 earnings, Cerner expects 62 to 64 cents per share. Cerner’s outlook puts its full-year forecast at $2.45 to $2.47 per share. The stock is down about 12% since its last earnings report.

Church & Dwight (CHD) had a very good report for Q3. For Q4, the household-products company expects earnings of 57 cents per share, which makes the full-year total $2.27 per share. CHD sees full-year organic growth of 3.5% to 4%. This is one of four stocks that are in the red for us this year (though not by much).

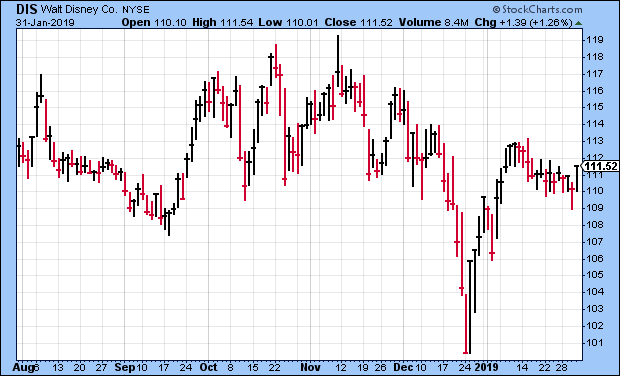

I have high hopes for Disney (DIS) this year. Fandango recently listed the 10 most-anticipated movies of 2019, and seven are Disney movies. By the way, that doesn’t include Frozen 2. I’ll go out on a limb and say that one will do well at the box office. Wall Street expects the mouse house to report $1.55 per share. Look for an earnings beat.

Becton, Dickinson (BDX) is recovering from a nasty fall in December. I’m not sure what traders were expecting. Last year, BDX raised its full-year guidance three times. On Tuesday, the company will report earnings for the first quarter of its fiscal year. For 2019, BDX expects earnings between $12.05 and $12.15 per share. Wall Street expects earnings of $2.62 per share.

Torchmark (TMK) sees 2018 earnings between $6.08 and $6.14 per share. That implies Q4 earnings of $1.51 to $1.57 per share. Wall Street had been expecting $1.56 per share. In October, the life insurer gave initial guidance for 2019. The company sees this year ranging between $6.45 and $6.75 per share.

Cognizant Technology Solutions (CTSH) is due to report on Wednesday. For Q4, the IT outsourcer sees earnings of at least $1.05 per share and full-year earnings of at least $4.50 per share. Cognizant sees Q4 revenue between $4.09 billion and $4.13 billion. The stock is up nearly 10% for us so far this year.

Finally, we have three more reports on Thursday, February 7. Broadridge Financial Solutions (BR) is one of our new stocks this year. For Q4, Wall Street expects earnings of 71 cents per share which is down from the 79 cents they made in Q4 of 2017. The stock is down sharply since the summer. I think BR could be a big winner for us this year.

In October, Fiserv (FISV) raised the lower end of its full-year guidance. The range had been $3.02 to $3.15 per share. Now it’s $3.10 to $3.15 per share. That represents growth of 25% to 27%. That translates to a Q4 range of 84 to 89 cents per share. With next week’s earnings report, Fiserv will confirm its 33rd year in a row of double-digit earnings growth.

Last quarter, Intercontinental Exchange (ICE) had its 22nd quarter in a row of year-over-year revenue growth. The owner of the NYSE didn’t provide any financial guidance for Q4, but Wall Street expects 92 cents per share. It’s nice being a near-monopoly.

That’s all for now. There will be lots more earnings reports next week, including five Buy List reports on Tuesday. On Monday, we’ll get the report on factory orders. Also on Tuesday, we’ll see the latest ISM Non-Manufacturing report. On Wednesday, we’ll get the productivity report. On Thursday, we’ll get another jobless-claims report, and we can see what impact the shutdown had. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on February 1st, 2019 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His