CWS Market Review – April 12, 2019

“If markets were rational, I’d be waiting tables for a living.” – Warren Buffett

After a seemingly endless wait, first-quarter earnings season has finally arrived, fashionably late but as dramatic as ever. Over the next few weeks, Corporate America will tell us how things went during the first three months of the year.

This will be a key earnings season for Wall Street because we’re expecting a modest earnings decline. I should add that results have beaten expectations for the last 39 quarters in a row. (Come to think of it, shouldn’t that read: analysts have missed reality?) In any event, this will be the first time in ten years when revenues are higher but earnings are lower. In other words, margins are falling.

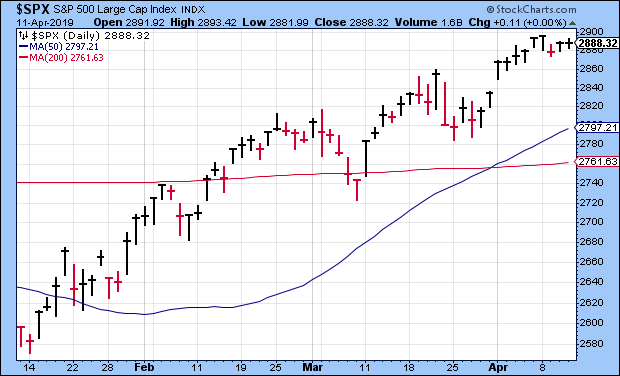

The market’s been quite happy this week. The S&P 500 has rallied nine times in the last ten days. On Monday, the index closed at another six-month high. We’re close to erasing everything lost during last year’s unpleasantness.

We have a few of our Buy List stocks due to report next week. In this week’s CWS Market Review, I’ll preview next week’s earnings reports. We also had great news from Cerner. Thanks to a major buyback announcement, the healthcare-IT stock jumped more than 10% for us on Tuesday. I’ll have all the details. But first, let’s see why the yield-curve hysteria has probably passed us by.

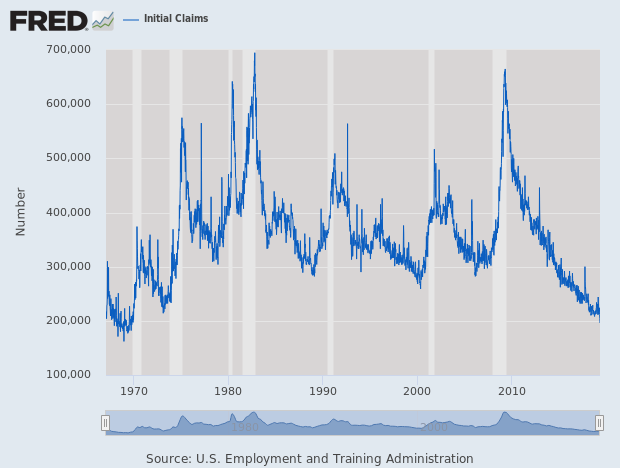

The Best Jobless-Claims Report in 50 Years

Last Friday, the government said the U.S. economy created 196,000 net new jobs in March. That’s a good number, and it’s a welcome relief after the lousy number from February. (By the way, the February was revised upward modestly.)

It seems that the sluggish start we had at the beginning of the year may have already passed. I suspect that a lot of companies will take advantage of the diminished expectations for this earnings season to pass off bum accounting issues. If Wall Street isn’t expecting much, then this is a good time to book a loss on that investment that went south. We may see a lot of that.

I think the government shutdown, combined with issues from China, put a damper on economic growth during Q1. However, that may have already passed, and we could be accelerating at this point. Let me highlight a few stats.

On Thursday, we got the lowest initial jobless-claims report since October 1969. This is interesting because this is one of the few data series that ticked higher during the shutdown. To me, this suggests that things have gotten better.

There are also signs of green shoots from China. The government there has done just about everything to get the economy back on its feet. In fact, the IMF recently bumped up its forecast for Chinese economic growth. Plus, the Chinese stock market has rallied impressively off its low. I never thought I’d see a Communist government cut taxes to spur growth, but here we are.

I’ve also noticed the recent uptick in energy prices which could presage positive signs for the global economy.

This is a bit of a U-turn in my thinking, but I try to follow the evidence. I recently talked about the flattening of the yield and its impact on the economy. I was surprised by the amount of bearish commentary I saw on the yield curve. Sure, an inverted curve isn’t ideal, but it’s hardly reason to panic.

It seems that the yield curve has already backed off some. The 10-year Treasury yield is back above the three-month yield. Also, the odds of a Fed rate cut later this year have diminished. Within the next five months, the futures market thinks there’s only a 30% chance of a rate cut. Even that seems high to me.

This week, we got the minutes from the last Fed meeting, and members are still open to raising rates. I think it’s a long shot, but it’s not unthinkable. I suspect that the Fed realizes the December hike was a mistake, and for now, they’re not going to move much in either direction.

The key variable continues to be the economy, and that’s why earnings season is so important. Now let’s look at what we can expect next week.

Next Week’s Earnings Reports

Here’s a preliminary calendar of this seasons earnings reports for our Buy List stocks. Twenty of our 25 stocks report on this cycle. Not every company has said when it’ll report, but I’ve tried to have the latest info.

| Company | Ticker | Date | Estimate |

| Eagle Bancorp | EGBN | 17-Apr | $1.12 |

| Signature Bank | SBNY | 17-Apr | $2.76 |

| Torchmark | TMK | 17-Apr | $1.59 |

| Check Point Software | CHKP | 18-Apr | $1.31 |

| Danaher | DHR | 18-Apr | $1.01 |

| Sherwin-Williams | SHW | 23-Apr | $3.70 |

| Stryker | SYK | 23-Apr | $1.84 |

| Moody’s | MOC | 24-Apr | $1.92 |

| AFLAC | AFL | 25-Apr | $1.06 |

| Cerner | CERN | 25-Apr | $0.61 |

| Hershey | HSY | 25-Apr | $1.46 |

| Raytheon | RTN | 25-Apr | $2.49 |

| Church & Dwight | CHD | 2-May | $0.66 |

| Intercontinental Exchange | ICE | 2-May | $0.90 |

| Disney | DIS | 8-May | $1.59 |

| Becton, Dickinson | BDX | 9-May | $2.58 |

| Broadridge Financial | BR | TBA | $1.50 |

| Cognizant Technology Solutions | CTSH | TBA | $1.04 |

| Continental Building Products | CBPX | TBA | $0.35 |

| Fiserv | FISV | TBA | $0.82 |

Eagle Bancorp (EGBN) is due to report on Wednesday, April 17. Three months ago, the bank released an impressive earnings report. The bank earned $1.17 per share, which was four cents better than estimates. Last year was a very good year for Eagle.

When looking at banks, there’s a key metric to watch which is called the “efficiency ratio.” It’s their overhead as a percent of revenue. Basically, the efficiency ratio tells us how well-run the bank is. The lower the number, the better. As a general rule, anything below 50% is considered good. For all of 2018, Eagle’s efficiency ratio was 37.3%. Despite the good results, shares of Eagle plunged more than 10% the day after the report came out.

This is where it gets weird. Eagle turned around and marched up to $60 per share in February, then plunged to $48 in March. EGBN is back up to $55, and I think it’s a good value here. The consensus is for earnings of $1.12 per share.

Signature Bank (SBNY) will also report on Wednesday. SBNY has been a big winner for us this year (+28.5%). In January, the bank reported a knockout quarter. For Q4, SBNY’s net interest margin was 2.90% and its efficiency ratio was 34.94%. Those are pretty good numbers. Interestingly, the bank also launched Signet, a “new proprietary, blockchain-based digital-payments platform.” Wall Street expects earnings of $2.76 per share. Expect to see a beat.

Also on Wednesday, Torchmark (TMK) is due to report. Their last earnings report matched expectations. For all of 2019, TMK sees earnings of $6.50 to $6.70 per share. For the Q1 report, Wall Street expects $1.59 per share which sounds about right.

Check Point Software (CHKP) is also due to report on Thursday, April 18. The stock looks to be a big winner for us this year. For Q1, Check Point sees revenues between $460 and $480 million and EPS between $1.28 and $1.34. For all of 2019, Check Point sees revenues ranging between $1.94 and $2.04 billion and earnings between $5.85 and $6.25 per share.

Danaher (DHR) is also due to report on Thursday. For Q1, DHR expects $1 to $1.03 per share. Wall Street had expected $1.03 per share. For all of 2019, the company sees earnings between $4.75 and $4.85 per share. The dental spin-off is expected to happen in the second half of this year.

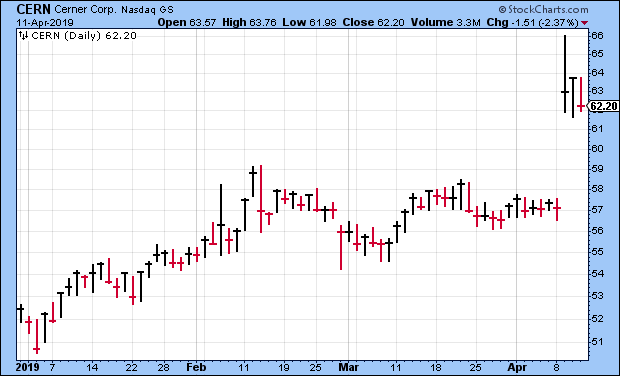

Cerner Is a Buy up to $66 per Share

On Tuesday, Cerner (CERN) said it had reached an agreement with Starboard Value, an activist shop. That’s one of those firms that takes a position in a company, and then advocates for changes. We’ve done well in recent years thanks to the work of activists. After some back and forth, Cerner and Starboard reached an agreement to make some changes at Cerner.

Most of the details aren’t terribly important for our purposes (you can read them here), but I want to highlight two. One is that the healthcare-IT firm will initiate a dividend. The other is that Cerner’s buyback authorization has been increased by $1.2 billion. That’s a big chunk of change. The company now has approval to repurchase $1.5 billion worth of CERN stock.

The stock jumped 10% on Tuesday. The company will report earnings on April 25. For Q1, Cerner expects earnings between 60 and 62 cents per share on revenue of $1.365 billion to $1.415 billion. For all of 2019, the company is looking for earnings between $2.57 and $2.67 per share on revenue of $5.65 billion to $5.85 billion. This week, I’m raising my Buy Below on Cerner to $66 per share.

On Thursday, Disney (DIS) unveiled its new streaming service. The service will be called Disney+. It will be ad-free and will launch on November 12. The service will cost $7 per month or $70 annually. This is Disney’s plan to attack Netflix. The shares fell 56 cents on Thursday to close at $116.60. The next earnings report is due out May 8.

That’s all for now. Next week will be dominated by earnings news. There will be a few key economic reports as well. The industrial-production report is due out on Tuesday. On Wednesday, the beige-book report comes out. The retail-sales report comes out on Thursday. Then on Friday, we get the latest report on housing starts. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on April 12th, 2019 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His