CWS Market Review – May 20, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Moody’s Downgrades America

On Friday, one of our Buy List stocks made international news. Moody’s cut its rating on the United States of America’s debt by one notch. The USofA is now rated Aa1. Prior to the cut, Moody’s had given the U.S.A. the biggest prize in finance, the coveted AAA rating. Moody’s had rated America’s debt AAA since 1917.

The other two big debt raters, Fitch and S&P, had already cut their ratings on America’s debt. Moody’s was the lone holdout.

Is this something to worry about? Eh, not really. Personally, I don’t get too worked up about these kinds of things. These events generate headlines more than they tell you about finance. For one, S&P cut its rating in 2013. Fitch joined in two years ago. I doubt that many people even noticed.

Also, I think it’s a little silly. Having a rating on America’s debt is like having an opinion on the sun. What is there to say?

It’s true that America’s debt has reached a staggering level. According to the “Debt to the Penny” website, our public debt stands at $36,215,714,628,553.09. In Washington, both parties are busy blaming each other for the mess. That’s hardly a surprise. The immediate cause for the debt downgrade is President Trump’s “One Big Beautiful Bill Act,” which he’s been pushing Congress to pass.

Moody’s said “the decision to downgrade debt was influenced by ‘the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns.’” If that’s true, then a downgrade could have come at any time in the last several years. I don’t know why they’re choosing now.

When Ronald Reagan was asked if he was worried about the budget deficit, he said no, it’s “big enough to take care of itself.”

One upshot is that Moody’s doesn’t appear to be interested in cutting its rating again. The company rates America’s debt as stable. Well, that’s good to know.

In a sense, America’s debt is judged every day—in fact, every minute of every hour of every day—by the global bond and currency markets.

It’s true that our government has been remarkably irresponsible with our finances, and there’s plenty of blame to go around. However, there’s an inescapable fact that investors all over the world want to own our debt, and they’re willing to pay for it. That tells me a lot more than what Moody’s has to say. Bear in mind that the S&P 500 just ran off 17 up days in the last 20 trading sessions. If it were truly a big deal, then markets would reflect it.

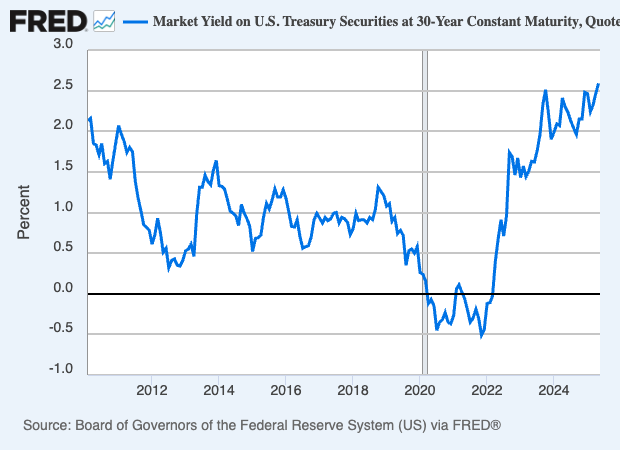

To be honest, I have been concerned by the recent rise in Treasury yields. The yield on the 30-year Treasury recently spiked above 5%, and the yield on the 10-year Treasury is close to 4.5%.

I also like to watch the TIPs yields which are adjusted-for-inflation bonds. The yield on the 30-year TIPs is now about 2.6% which is close to as high as these bonds have ever traded, with data going back more than 20 years. As recently as three years ago, the yield on the 30-year TIPs was negative. In a sense, we’re returning to normal.

The stock market tends to perform worse when TIPs yields are high, and that makes perfect sense. I suspect that the higher yield on TIPs reflects a change in risk tolerance.

Overall, I’m concerned about America’s fiscal standing, but I’m watching the market’s reaction rather than a ratings agency.

I Missed Out With Costco

I’m going to engage in a bit of self-criticism, and I hope to convey some important lessons about investing. I’m a big fan of Costco, and I completely screwed up with it.

I studied the company intently. I even wandered up and down the aisles and took notes. (It’s a wonder I was never kicked out!) Gradually, I became a huge Costco fan.

It’s a very well-run company and its earnings have grown consistently for many years. Costco has a renewal rate of 93%. The company has all the qualities I look for in a stock, except one: Costco has a very high valuation. Very high.

This fact had led me to decline from adding it to the portfolio. No matter how many times I ran the numbers, it always looked to me that Costco was way too pricey, and I can say that with full confidence, I was dead wrong.

The stock kept moving higher. Just because it was overpriced was apparently no barrier to it becoming even more overpriced.

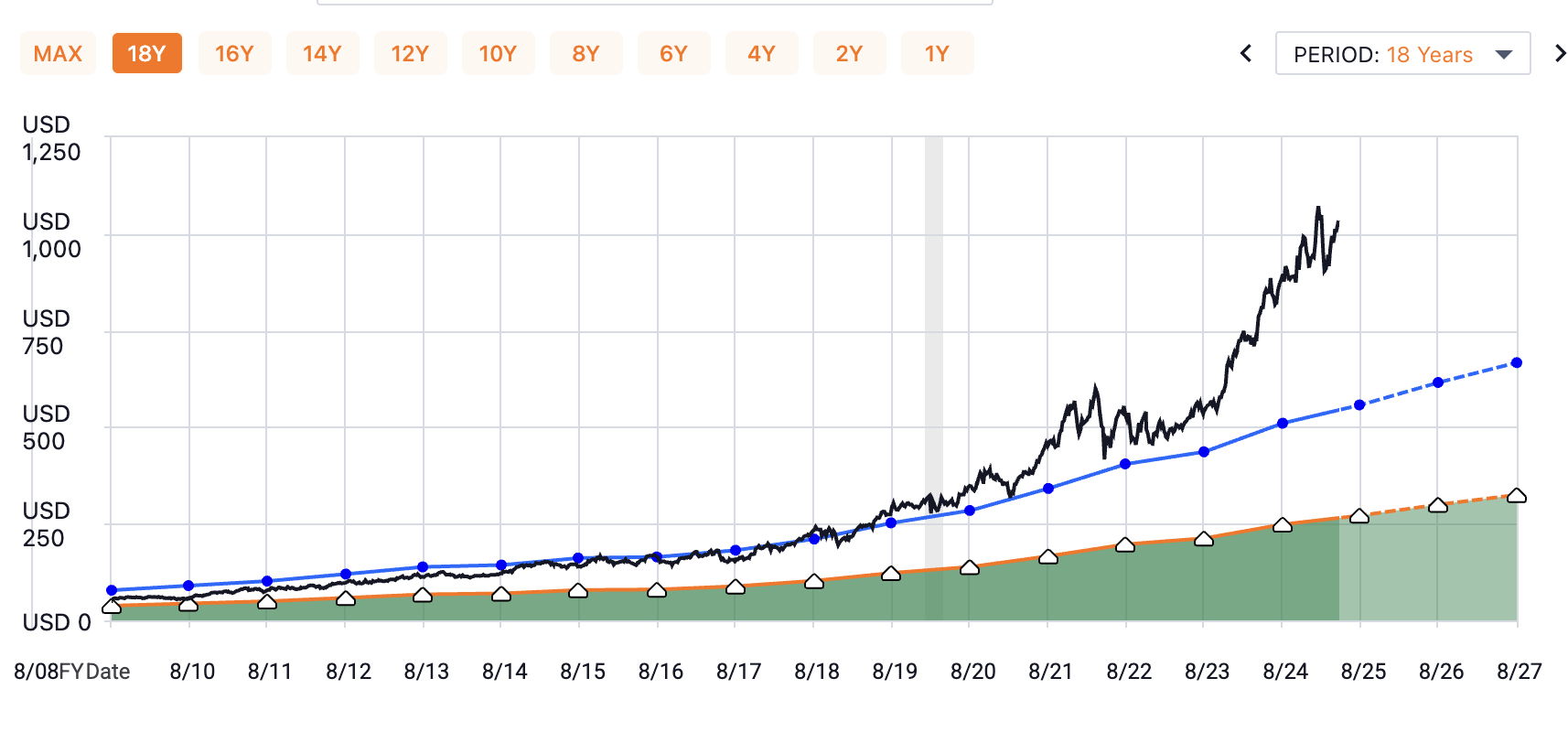

Check out this chart. In 16 years, Costco is up 35-fold. I don’t know if there ever was a bad time to buy it.

Let me go into more detail why I’m such a Costco fan. For one, I love Costco’s business model, and its customer base is very loyal. Some might say cult-like. Importantly, the company generates recurring revenue from its membership fees, and the cash flow is stable. As investors, we love recurring revenue.

The idea is simple. There’s a lot of savings in buying in bulk. If you need to buy a 17-pound tub of mayonnaise, Costco is the place to go. In addition to bulk-buying, Costco is obsessed with efficiency.

The company runs about 800 warehouses, and the average location generates about $275 million in revenue per year. The margins are very thin, meaning the markups are quite small.

For the last fiscal year which ended in August, Costco generated a profit of $7.4 billion off sales of $250 billion. That works out to about 3%. I don’t think people realize how tiny that is.

At its core, Costco is really a business dedicated to turnover and efficiency. As soon as a product is on their shelf, they want to get rid of it as soon as possible. Costco runs a very tight ship. Walmart carries about 10 times the number of items. Costco keeps it simple.

From Fast Graphs, this is Costco’s stock (in black) along with 30 times its earnings (in blue) and dividends (in tan).

The blue line is a P/E Ratio of 30, which isn’t cheap, and you can see how the black has quickly run past that.

Costco also runs its own private label Kirkland brand which makes up for about one-quarter of Costco’s overall sales. That by itself is a major business. Costco is also very good at using popular items as loss leaders like rotisserie chickens or their famous $1.50 hotdogs.

Costco knows that if you get people in the store, and feed them, they’ll probably stick around and buy something. In fact, people seem to enjoy the price-hunting experience. Costco, of course, has no plans to change the price of its hotdogs.

I also like that Costco tends to be countercyclical. In plain English, that means Costco does well when the economy runs off the road. That’s when people are looking for discounts. They have a helpful and knowledgeable staff. Costco employees are generally paid more than their competitors.

Have you ever seen an ad for Costco? Now that I think of it, I don’t believe I ever have. They do advertise, but not very much. Instead, they rely on word-of-mouth.

The membership model also encourages shoppers to go to a store. It’s a sunk cost. That’s because they already bought a membership so they figure they might as well use it.

Costco was also a point of contention between Warren Buffett and Charlie Munger. Charlie loved the stock, but Buffett was skeptical, and he never liked retail. Charlie was able to convince Warren to buy Costco and it became a huge winner for them. Costco even added Munger to its board.

After Munger passed away, Buffett decided to sell Costco, yet the stock continued to rally. Buffett conceded that his friend had been right all along.

In March, Costco posted a rare earnings miss. For its fiscal Q2, Costco earned $4.02 per share. That was nine cents below expectations. In six days, the stock fell 15%. The sale didn’t last long, and Costco has made back nearly everything it lost.

For this fiscal year, Costco is expected to make $18.12 per share. That means the stock is trading at 57 times earnings. Sorry, but that still seems way too expensive. (But I’ve been wrong before!)

In retrospect, my mistake was placing too much attention on the share price when I should have been focusing on what makes Costco so different.

Later this week, we’ll get reports on new and existing home sales. Next week, the Fed will release the minutes of its most recent meeting. Also, the government will update its report on Q1 GDP growth. The initial report said that the U.S. economy grew at a meager 0.3% for the first three months of this year.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on May 20th, 2025 at 5:19 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His